PDF attached

WASHINGTON,

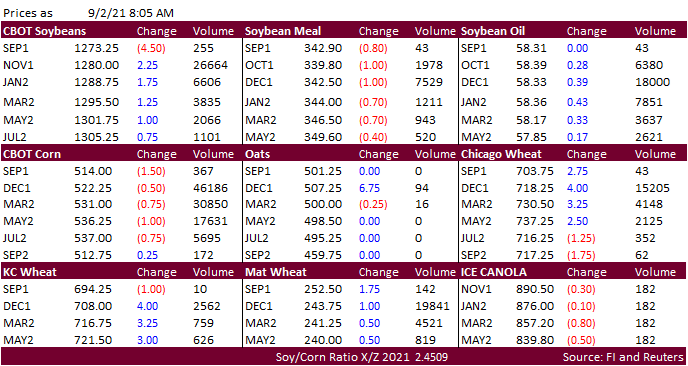

September 2, 2021—Private exporters reported to the U.S. Department of Agriculture export sales of 126,000 metric tons of soybeans for delivery to China during the 2021/2022 marketing year.

Export

sales for new-crop soybeans and soybean meal were every good. Corn is lower for the fourth consecutive session while soybeans traded two-sided several times overnight. Soybean oil is higher led by a 65 MYR increase in Malaysian palm oil overnight. Cash

palm was up $5.00/ton at $1095/ton. Soybean meal is lower, but losses are limited on steady US domestic feed demand and the slowdown in the US summer crush. China soybean complex futures were mixed. Wheat is mixed. Traders are wondering if USDA will make

changes to its US acreage in the upcoming September Crop Production report after NASS issued a press release yesterday hinting, they may review and incorporate data issued by the FSA office’s Prevented Planting report issued mid-August. We think corn and

soybean acres could be revised higher. An upward revision of 500 to 1000 thousand acres for corn and 200 to 450 thousand acres for soybeans could be bearish if USDA leaves unchanged or increases yields on September 10. Trade estimates may be out as early

as Friday night and with the long holiday weekend, look for some traders to take positions off the table before Friday’s close. Late yesterday afternoon we heard the lower Mississippi river is starting to reopen now that some power had been restored.

![]()