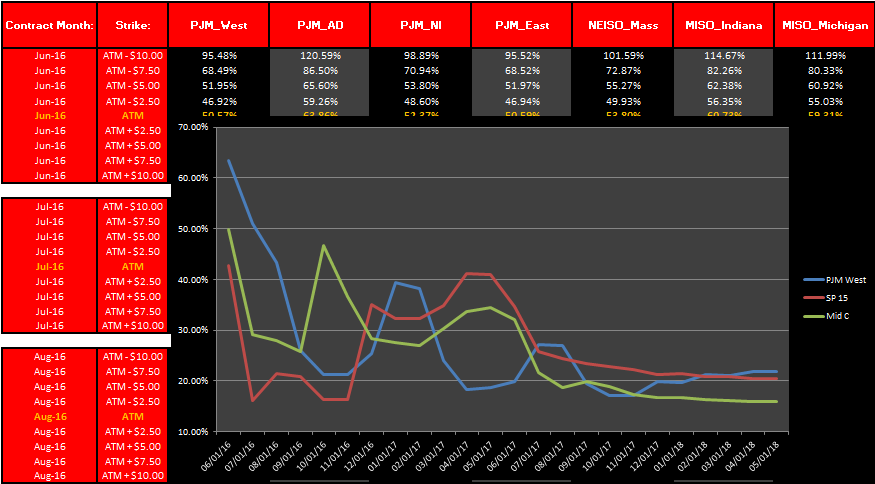

Power Implied Volatilities

The power implied volatilities provide an independent and thorough view into the North American electricity market. Detailing important liquid trading hubs, the implied volatility data gives customers insight into potential price movements. Volatilities are delivered daily before 4:00 pm EST providing customers an early start to their end of day processes.

MARKETS COVERED

OTCGH covers daily assessments of Power Implied Volatility at 15 locations in North America. Liquid hubs are covered in the following ISO/RTOs: PJM, MISO, NEISO, NYSIO, and ERCOT.

KEY FEATURES

- PJM West, CAISO SP 15, WECC Mid C, MISO Indiana, NYISO Zone A, ERCOT North, NEISO Mass (Straddles included)

- Historical volatilities

- Bid ask spreads on volatilities

- 24-month forward tenor produced daily