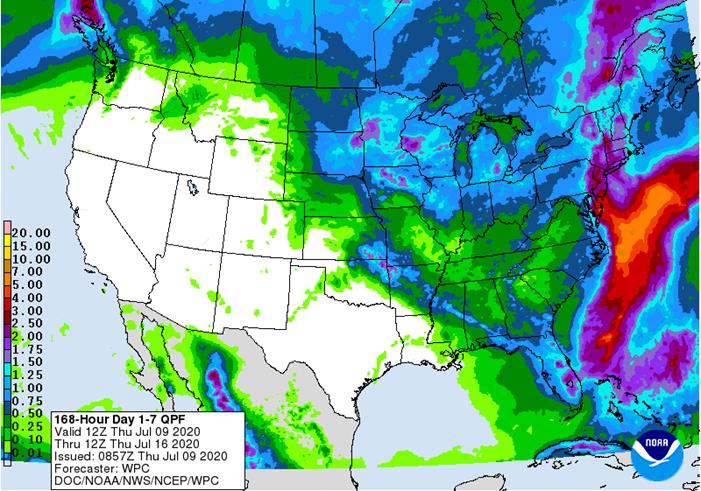

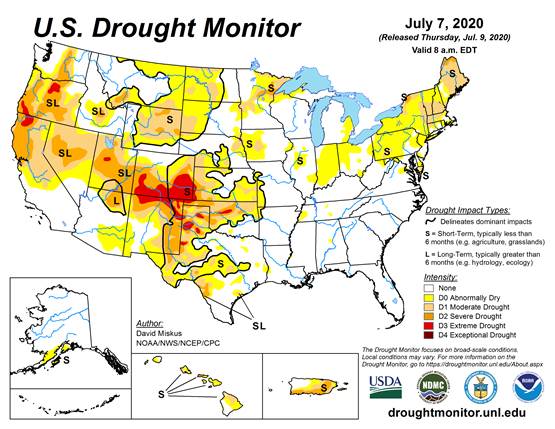

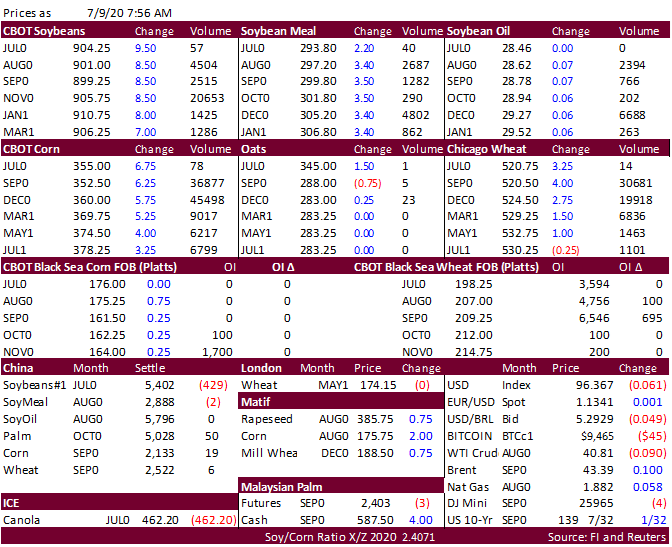

FI Morning Grain Comments 07/09/20 Jul 9, 2020 PDF attached Morning. Back to trading a weather market. Weather models look warmer and drier for week one and week two for the US. The most notable change was a drier forecast for week two for lower Midwest to 2/3 of the Midwest. This lifted corn and soybeans sharply higher overnight. Soybean products are mixed with a firm undertone in meal and weaker SBO. Although Rotterdam vegetable oils were leading CBOT sharply higher this morning. Wheat is mostly higher on follow through buying yesterday. China sold all of its 4 million tons of corn out of auction, bringing cumulative sales to 28 million tons. Funds yesterday were most active in Chicago wheat on the buy side since last December, using daily estimates. Argentina is on holiday. After the CBOT close, we learned the Rosario Grains Exchange lowered their outlook for the 2020 Argentina wheat crop to 18-19 million tons from 21-22 million tons previously, based on a lower area.