PDF Attached

![]()

CBOT

soybean complex, corn and wheat sold off post USDA report. US wheat futures remained underpinned on Russia’s plan to impose a wheat export tax and quota. The USDA report was viewed as neutral. Earlier in the day USDA export sales showed soybean complex

sales on the lower end of expectations and grains lower than what was reported from the previous week.

MPOB

issued a bearish Malaysian palm production report but third month palm futures rallied 47 ringgits. China made no changes to their corn & soybean balances.

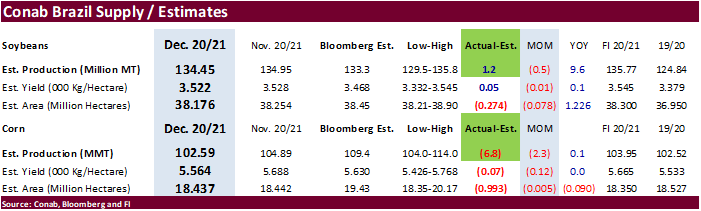

Conab surprised the trade by lowering total Brazil corn production by 2.3 million tons to 102.59 million, 6.8 million below a Bloomberg trade estimate. Conab reported Brazil soybean production at 134.45 million tons, 0.5 below the previous

month and 1.2 million tons above a Bloomberg trade average.

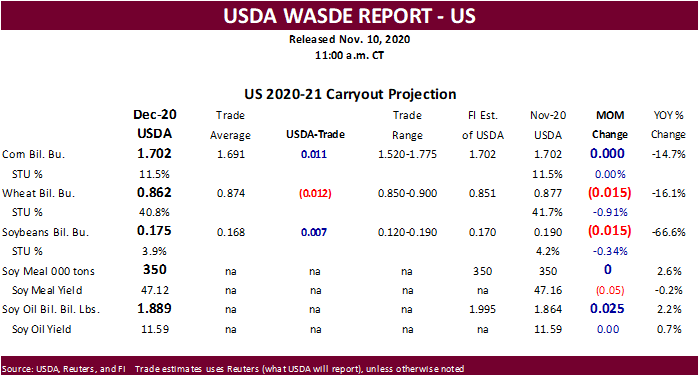

US

soybean stocks were lowered a less than expected 15 million bushels to 175 million. USDA took the US crush up 15 million bushels to 2.195 billion versus 2.165 billion for 2019-20. US soybean meal exports were taken up 500,000 short tons and imports were

raised 200,000 short tons. Meal production was increased 300,000. Soybean oil production was raised 175 million pounds. USDA lifted the US soybean export forecast by 150 million pounds resulting in a 25 million pound boost to ending stocks. USDA left the

US corn balance unchanged. Traders were looking for a slight downward revision in US corn stocks. For wheat, they lowered imports by 5 million bushels and raised exports by 10 million to 985 million. We are at 995 million for US exports.

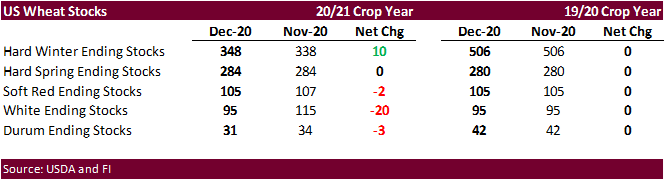

We

think US wheat prices traded out of alignment post USDA report based on US wheat by class changes in USDA’s December update.

Weather

National

Weather Service proposes limiting data availability because of bandwidth shortage

https://www.chron.com/news/article/National-Weather-Service-proposes-limiting-data-15789570.php

MOST

IMPORTANT WEATHER OF THE DAY

- Argentina

temperatures trended hotter Wednesday with afternoon highs more solidly in the 90s Fahrenheit resulting in accelerated drying; extreme highs in the middle and upper 90s to 102 degrees occurred in most of the west - Argentina

was dry Wednesday and that in combination with the heat accelerated moisture stress in the driest crop areas; however, some rain developed in southern Buenos Aires overnight - Rainfall

through dawn today varied up to 0.25 inch in southern parts of Buenos Aires which was not enough to counter moisture losses from Wednesday, but additional rain will occur today - Argentina

weather will be warm biased and will include erratically distributed rainfall during the coming ten days - The

moisture will all be welcome, but its distribution will leave some areas drier than others and concern over production potential will rise in the driest areas - Additional

rain in western and central Buenos Aires today will produce 0.10 to 0.60 inch of moisture with a few totals pushing up close to 1.00 inch - Most

of the precipitation will be too light for a notable change in soil moisture - Argentina’s

rain will shift northward Friday into Saturday with the greatest amounts and coverage in northeastern parts of the nation Saturday when favorable soil moisture will be maintained in Corrientes, northern Santa Fe and southeastern Chaco - Some

periodic showers and thunderstorms will occur over the following week in northern parts of the nation leaving the south in a net drying mode with increasing crop stress - Southern

Argentina’s best rain potential does not return until the week of Dec. 21 and confidence is low over its distribution

- Brazil’s

rainfall over the next ten days will be least significant in Bahia and southeastern Piaui, but there will be some occasionally rainfall in a few west-central and southwestern Bahia locations to benefit cotton, corn and soybeans - Eastern

cocoa and coffee production areas will not get much rain for a while - Brazil

rainfall will also be a little light in northern Mato Grosso do Sul, southeastern Bolivia and some immediate neighboring areas, but there will be at least some rain in these areas periodically to prevent a complete absence of moisture - Minas

Gerais, Brazil will be the wettest state in Brazil during the coming two weeks with some potential for localized flooding - Most

of the rain in Minas Gerais will be spread out over time helping to limit the potential for serious flooding - Neighboring

areas of Espirito Santo and Rio de Janeiro will also be sufficiently moist while rain in Sao Paulo will be a little sporadic - Another

round of welcome rain will come out of Paraguay and into Parana, southern Mato Grosso do Sul, Santa Catarina and southwestern Sao Paulo, Brazil Sunday into Wednesday of next week - This

rain event will be well timed after some drying occurs through the weekend and will help to maintain a very good moisture environment for developing summer crops - Rainfall

of 1.00 to 3.00 inches and local totals to more than 4.00 inches will result - Rainfall

in Brazil may become more sporadic and light again for a little while during the second week of the outlook and a close watch on its distribution both prior to and during that period of time is warranted to ensure sufficient amounts of rain occur to support

the best crop development potential. - Brazil’s

bottom line is still one of improvement in this coming week to ten days. Greater rain intensity and amounts will be needed in the far south, northeast and in few other random areas. Some production cuts have occurred in many areas, but the key to soybean production

will be during pod setting and filling which will be evolving later this month and in January. That is the time period that will be most important time in determining yield.

- Eastern

Australia’s generalized rain potentials are very low over the coming week, although some scattered showers will occur

- Rain

will fall along the lower Queensland and upper New South Wales coast where amounts will be great enough to bolster soil moisture, but only a few agricultural areas will benefit - Sugarcane,

far eastern cotton and far eastern sorghum areas will be most impacted - Temperatures

in eastern Australia will be cooler than they have been during the coming week, but warming is expected again Dec. 16-23 - Australia’s

winter crop harvest in the south should be winding down soon and it has been a good harvest season - South

Africa will be favorably mixed with periods of rain and sunshine impacting summer grain, oilseed and cotton production areas - Planting

progress should advance favorably around periods of rain - Dryness

is of most concern today in central and western Free States and eastern Northern Cape - Eastern

China weather has improved recently with less rain allowing rapeseed and southern wheat production areas a chance to dry down after being too wet earlier this season - China’s

weather over the next two weeks will keep most winter crops dormant or semi-dormant and precipitation will concentrate on the Yangtze River Basin where a wintry mix of precipitation types is expected late this weekend into next week - Winter

crops are well established and poised to perform well in the spring - Sugarcane

harvesting in the south will advance relatively well for a while due to expected dry weather - India’s

far south is beginning to dry down - Too

much rain recently has delayed summer crop maturation and harvesting in Tamil Nadu and southern Andhra Pradesh where some cotton, rice and groundnut quality concerns have evolved

- Drying

will get harvest progress back on the right track - Central

and far northern India showers over the next seven days will benefit a few winter crops, but greater rain will be needed in the heart of the nation - Most

winter crops are favorably rated, however, with little change likely - Any

moisture will be welcome and of some benefit to winter crops - Southern

Vietnam and Cambodia will trend wetter than usual late this week and into next week with some of that moisture reaching far southern Thailand as well

- The

moisture will delay harvest progress for many crops, but no serious crop quality changes are likely - Winter

crops will benefit, though - Routinely

occurring precipitation is expected in Philippines, Indonesia and Malaysia over the next two weeks - A

tropical cyclone has been advertised for southern Philippines late next week, but it is too soon to have high confidence in that event - Russia’s

Southern Region had eastern Ukraine will continue missing significant precipitation for the next ten days leaving dormant winter crops in need for greater soil moisture to be used in the spring - Winter

crops are still not as well established as they should be - Showers

will occur briefly next week, but the resulting moisture will not be very great - Greece,

Bulgaria, eastern and southern Romania, Moldova and western Ukraine will all receive significant moisture late this week into early next week bolstering topsoil moisture for better winter crop establishment and growth potential in the spring - Portions

of the U.K., France and the Iberian Peninsula will also receive periodic rainfall during the next two weeks along with Italy and the eastern Adriatic Sea region

- Some

local flooding is possible in many of these areas - North

Africa rainfall will be greatest in northern Algeria and coastal areas of Tunisia during the coming ten days. The moisture will be welcome - Some

moisture will also reach into far north-central Morocco, but there is need for more rain in the remainder of that nation and in particular the southwest - Morocco

continues trying to recover from last year’s drought - U.S.

weather was mostly dry and mild to warm Wednesday; temperatures were well above average in a part of the central states and in neighboring areas of Canada - U.S.

storm late this week will impact areas from eastern Texas, eastern Oklahoma, Arkansas and Missouri to Michigan and New York with rain and some snow - Heavy

snow will impact parts of northern and western Michigan while light snow trails to the southwest into Nebraska and eastern Colorado - Another

weak weather system will move from the central Plains to the Delta and southeastern states this weekend - An

active weather pattern in the Dec 16-25 period will bring another storm to the eastern Midwest, Delta and middle and northern Atlantic Coast States during the middle to latter part of next week followed by a couple of other storm systems moving through the

eastern United States Dec. 19-25 - Temperatures

over the next seven days will be warmer than usual in much of the nation - Cooling

is expected in the western and north-central states Dec. 18-24 - Southern

Oscillation Index was at +10.17 today and it will remain strongly positive for a while - Mexico

precipitation will be quite limited over the coming week except in the northwest today when a storm system brings moisture to Sonora, Baja California, Sinaloa, northwestern Durango and Chihuahua

- Rainfall

of 0.10 to 0.75 inch and local totals to 1.00 inch will result disrupting summer crop harvesting, but benefiting winter crops - Southeastern

Mexico crop areas will only receive light rainfall from scattered showers and harvesting will advance favorably - Portions

of Central America will continue to receive periodic rainfall over the next couple of weeks, but the intensity and frequency will be low enough to support some farming activity - Costa

Rica will be wettest this workweek

·

West-central Africa will experience greater than usual rainfall over the coming week and some of the moisture might interfere with harvesting and could also induce some isolated flowering of coffee and cocoa in areas that get

the greatest moisture.

·

East-central Africa rain will be erratic and light in Ethiopia, Kenya and Uganda while rainfall will be greatest over Tanzania

·

New Zealand rainfall will be limited in North Island and northern parts of South Island over the coming week while showers impact western and southern South Island

- Temperatures

will be near to below average

Source:

World Weather Inc. and FI

Thursday,

Dec. 10:

- China’s

agriculture ministry (CASDE) releases monthly report on supply, demand, 10am local - Malaysian

Palm Oil Board releases data on November stockpiles, exports, production, 12:30pm local - FranceAgriMer

monthly crop report - Agroinvestor

Russian agriculture conference - Port

of Rouen data on French grain exports - Conab’s

data on area, output and yield of soybeans and corn in Brazil, 7am - National

Grain & Feed Association Country Elevator Conference, 10am - USDA

weekly crop net-export sales for corn, soybeans, wheat, cotton, pork, beef, 8:30am - USDA’s

monthly World Agricultural Supply and Demand (WASDE) report, 12pm - HOLIDAY:

Thailand

Friday,

Dec. 11:

- ICE

Futures Europe weekly commitments of traders report - HOLIDAY:

Thailand

Source:

Bloomberg and FI

USDA

export sales

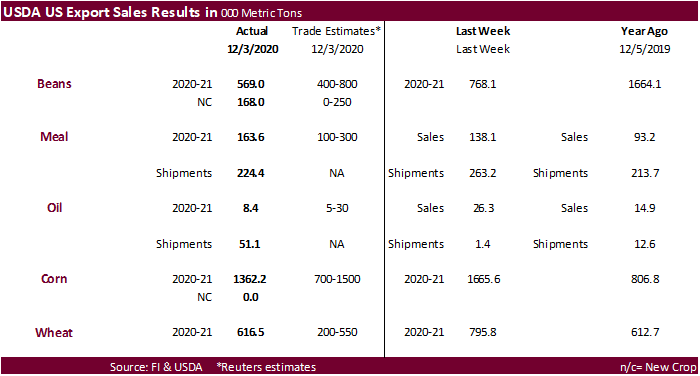

-

USDA

soybean export sales were a low 569,000 tons, down from 768,100 tons previous week and 1.664 million tons year ago. China booked 685,400 tons but 459,000 tons of that was switched from unknown.

-

Soybean

meal sales were also low at 163,600 tons (shipments 224,400 tons) and soybean oil sales were only 8,400 tons, down from 26,300 tons previous week. SBO shipments were very good at 51,100 tons and included 34,600 for South Korea and 10,600 tons for China.

-

USDA

corn export sales were 1.362 million tons, within expectations and down from 1.666 million previous week. Corn sales included 141,200 tons for China and 422,200 tons for unknown.

-

USDA

sorghum export sales came in at 123,000 tons and included 67,900 tons for China.

-

Pork

sales were 26,500 tons and included 6,300 tons for China. -

USDA

all-wheat export sales of 616,500 tons were down slightly from 795,800 tons previous week. China booked 68,300 tons of wheat.

US

Initial Jobless Claims Dec 5: 853K (est 725K; prevR 716K; prev 712K)

US

Continuing Claims Nov 28: 5757K (est 5210K; prevR 5527K; prev 5520K)

US

CPI (M/M) Nov: 0.2% (est 0.1%; prev 0.0%)

US

CPI Ex Food, Energy (M/M) Nov: 0.2% (est 0.1%; prev 0.0%)

US

CPI (Y/Y) Nov: 1.2% (est 1.1%; prev 1.2%)

US

CPI Ex Food, Energy (M/M) Nov: 1.6% (est 1.5%; prev 1.6%)

US

Real Avg Hourly Earnings (Y/Y) Nov: 3.2% (prev 3.2%)

US

Real Avg Weekly Earnings (Y/Y) Nov: 4.7% (prev 4.4%)

US

EIA Natural Gas Storage Change (BCF) 04-Dec: -91 (est -86; prev -1)

–

Salt Dome Cavern Natural Gas Storage Change (BCF): -7 (prev +12)

ECB

GDP Forecasts:

ECB

Sees 2020 GDP Growth At -7.3% (vs. -8% Seen In Sept)

Sees

2021 GDP Growth At 3.9% (vs. 5% In Sept)

Sees

2022 GDP Growth At 4.2% (vs. 3.2% In Sept)

Sees

2023 GDP Growth At 2.1%

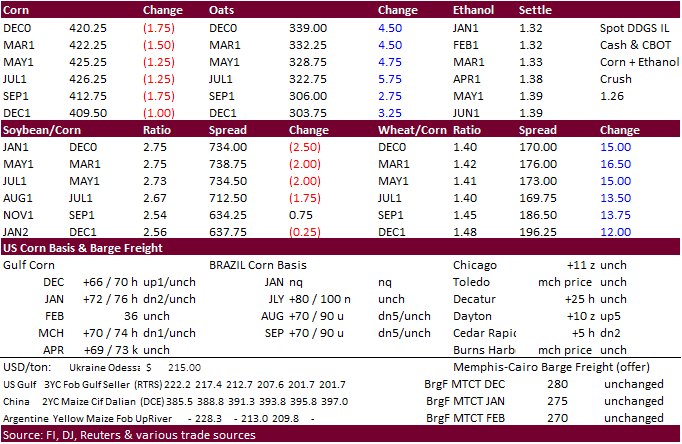

Corn.

-

CBOT

March corn started the day higher following wheat and positioning ahead of the USDA report, but broke after USDA left their corn US balance sheet unchanged. Profit taking was noted. The trade will shift their focus back to SA weather and US demand. Next

set of major reports will be released second week of January. March corn ended 2.50 cents lower.

-

Funds

sold an estimated net 12,000 corn contracts. -

USDA

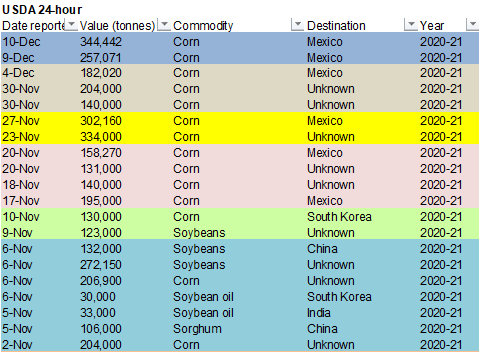

announced another flash sale to Mexico. 344,442 tons were sold for 2020-21 delivery.

-

Conab

surprised the trade by lowering total Brazil corn production by 2.3 million tons to 102.59 million, 6.8 million below a Bloomberg trade estimate. The area came in nearly 1 million hectares below expectations.

-

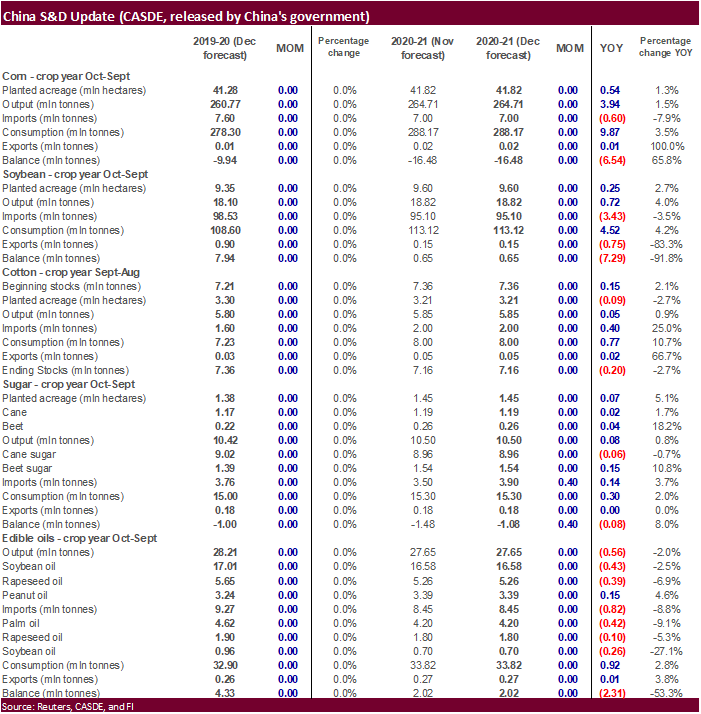

China

made no changes to their corn & soybean balances. China left corn production and imports unchanged from the previous month in their CASDE report, at 264.7 million tons and 7.00 million, respectively. Trade estimates for corn production range from 250.0 to

264.7 million tons. They left 2020-21 corn imports unchanged at 7.0 million tons despite data calling for more than 13 million tons.

-

Separately

China’s statistics bureau reported 2020 corn production was 260.67 million tons, below 264.7 million tons projected by CASDE. China’s statistics bureau estimated grain production increased 0.9% to 669.49 million tons, and the planted area increased 0.6% to

116.8 million hectares. -

Today

was day 4 of the Goldman Roll. -

Germany

is asking China to end the pork import ban, at least for product from regions unaffected by the ASF outbreak. Around 240 ASF cases have been confirmed in Germany since Sept. 10. All were in wild animals.

-

France

reported a second bird flu outbreak, in the Landes region in southwest France.

-

Coceral

2021 EU + UK corn production was estimated at 63.1 million tons versus 62.8 million tons in 2020.

-

President

elect Biden picked Tom Vilsack as the US Secretary of Agriculture.

Corn

Export Developments

- Under

the 24-hour announcement system, private exporters sold 344,442 tons of corn to Mexico for 2020-21 delivery.

- South

Korea’s Korea Corn Processing Industry Association (KOCOPIA) bought 60,000 tons of corn from the United States at an estimated $250.25 a ton c&f for arrival around April 1.

Updated

11/30/20

March

corn is seen

trading in a $4.15 and $4.40 range.