From: Terry Reilly

Sent: Friday, March 27, 2020 8:17:55 AM (UTC-06:00) Central Time (US & Canada)

Subject: FI Morning Grain Comments 03/27/20

PDF attached

Morning.

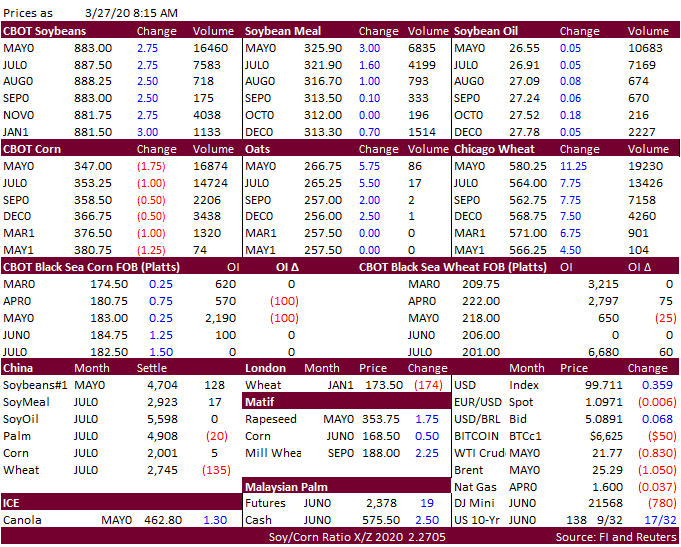

Russia

plans to limit grain exports. US stocks are lower, USD slightly higher and gold lower. US agriculture markets are mostly higher, with exception of corn.

There

are reports the virus may peak in early to mid-April in the US, but time will tell. This is for sure something that will be in the history books for children to read in years to come.

![]()