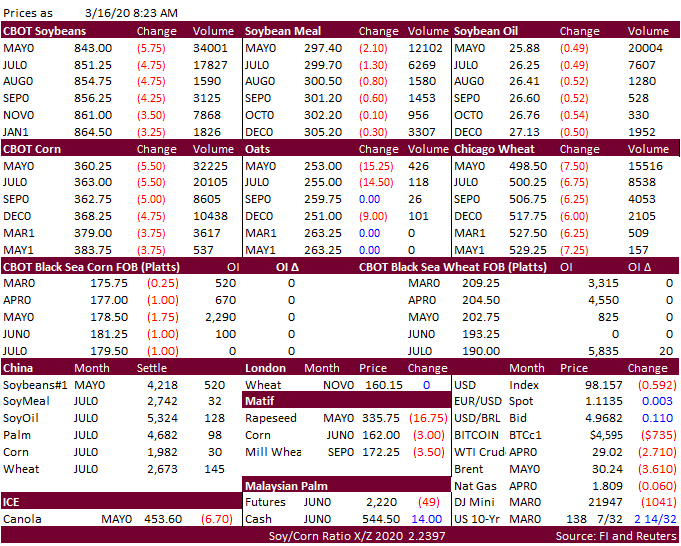

FW: FI Morning Grain Comments 03/16/20 Mar 16, 2020 From: Terry Reilly Sent: Monday, March 16, 2020 8:24:44 AM (UTC-06:00) Central Time (US & Canada) Subject: FI Morning Grain Comments 03/16/20 PDF attached Morning. Fed Slashes Rates to Near Zero, Deploys Massive Bond Buying of $700 bil. Macros continue to dictate prices. Fundamentals will return eventually. Source: Reuters and FI