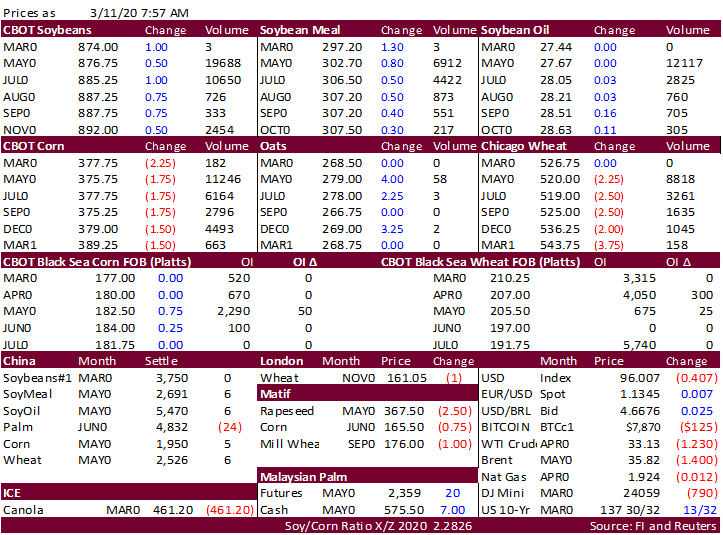

FW: FI Morning Grain Comments 03/11/20 Mar 11, 2020 From: Terry Reilly Sent: Wednesday, March 11, 2020 8:13:24 AM (UTC-06:00) Central Time (US & Canada) Subject: FI Morning Grain Comments 03/11/20 PDF attached Morning. Mixed trade in ags. USD was down 37 earlier. Stocks are selling off. BOE lowered interest rates by 50 points to 1 percent.