From: Terry Reilly

Sent: Tuesday, February 18, 2020 8:03:18 AM (UTC-06:00) Central Time (US & Canada)

Subject: FI Morning Grain Comments 02/18/20

PDF attached

Morning.

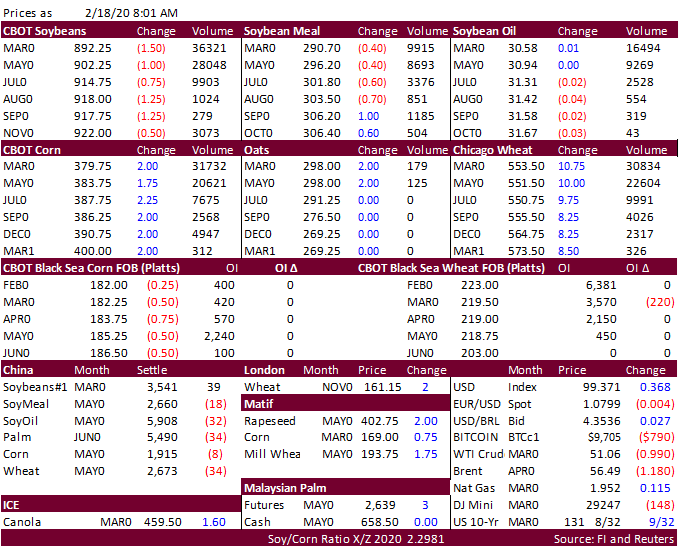

US is back from holiday. Wheat is the leader today. Locust swarms with a 40-mile reach (length) that have been destroying farm crops Africa could now threaten Southwest

Asian countries. Coronavirus continues to hit selected markets, such and India chicken demand and Indonesia palm export shipments to China. Truck strikes in Brazil are disrupting port loadings, especially at Santos.