From: Terry Reilly

Sent: Friday, February 14, 2020 8:11:11 AM (UTC-06:00) Central Time (US & Canada)

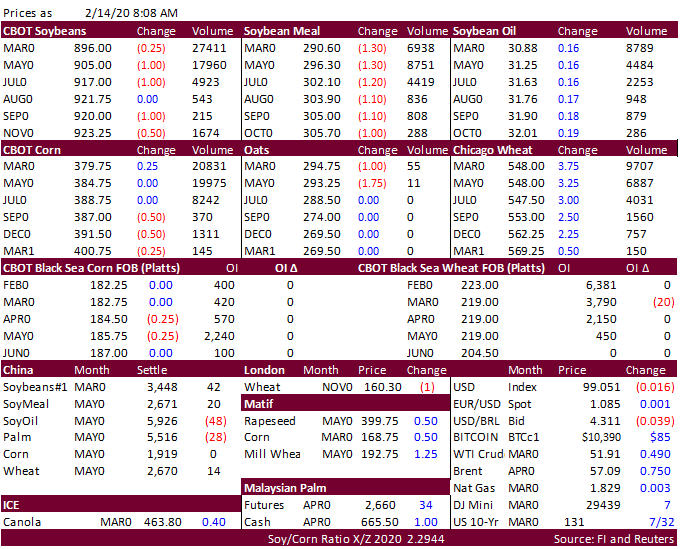

Subject: FI Morning Grain Comments 02/14/20

PDF attached

US

is on holiday Monday. Positioning is seen today. Covid-19 continues to hang over the markets.

USDA

later today will release its 2020:

·

Agriculture projections at 11:00 am CT

https://www.ers.usda.gov/publications/

·

Agriculture Baseline Database at 2:00 PM CT

https://www.ers.usda.gov/calendar/?month=2&year=2020&day=14

![]()