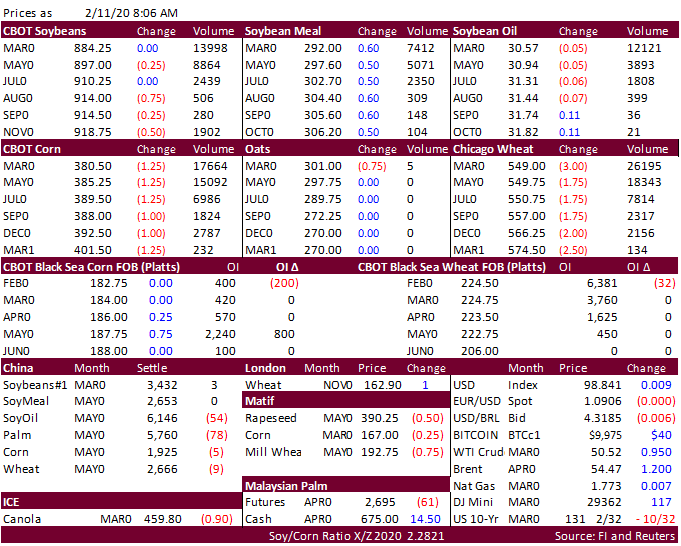

FW: FI Morning Grain Comments 02/11/20 Feb 11, 2020 From: Terry Reilly Sent: Tuesday, February 11, 2020 8:08:59 AM (UTC-06:00) Central Time (US & Canada) Subject: FI Morning Grain Comments 02/11/20 PDF attached Morning. Look for a choppy session ahead of USDA report (estimates attached). Algeria, Egypt, Jordan, and talk Saudi Arabia (soon) are in for wheat. SK is in for corn. Conab soybean production fell short of expectations by 1.1MMT. China left their 2019-20 soybean and corn balance sheets unchanged from the previous month.