From: Terry Reilly

Sent: Friday, September 28, 2018 5:03:51 PM (UTC-06:00) Central Time (US & Canada)

Subject: FI Evening Grain Comments 09/28/18

PDF attached

USDA released their Grain Stocks as of September 1 and Small Grains Summary

· USDA Links to reports

http://usda.mannlib.cornell.edu/MannUsda/viewDocumentInfo.do?documentID=1079

http://usda.mannlib.cornell.edu/MannUsda/viewDocumentInfo.do?documentID=1268

· Executive Briefings

https://www.nass.usda.gov/Newsroom/Executive_Briefings/index.php

USDA report initial reaction

· Bearish CBOT grain and oilseeds commodities.

· September 1 grain stocks were all above trade expectations, and prices were quickly to respond. After wheat began to stabilize, buyers rushed to the market which turned prices around, but then wheat prices turned lower in afternoon trading. Corn and soybean futures began to pair losses shortly after the report but made new session lows after buying activity dried.

Weather and crop conditions

· Upper Midwest temperatures are going to be very cool over the weekend.

· Mato Grosso will see daily showers through October 12th but amounts will be light on and off.

· Mato Grosso do Sul to Sao Paulo southward into Paraguay and far southern Brazil will see regular rounds of showers through the next two weeks that will induce some increases in soil moisture.

· Frequent showers will occur in the Delta through Tuesday.

· The Midwest will also be active starting later this week which should slow harvesting before a couple more days of net drying occurs outside the Ohio River Valley region.

· HRW wheat areas will see a mixture of sunshine and rain.

· Improving weather across Europe and the CIS is bearish for wheat.

SIGNIFICANT CORN AND SOYBEAN BELT PRECIPITATION EVENTS

WEST CORN BELT EAST CORN BELT

Tdy-Sat 40% cvg of up to 0.35” 5-20% daily cvg of up

and local amts to 0.55”; to 0.30” and locally;

south Ia. wettest more each day; north

Il. wettest

Sun 20% cvg of up to 0.35”

and local amts to 0.60”;

wettest north

Sun-Mon 75% cvg of 0.35-1.40”

and local amts to 2.30”

from south Ia. to Wi.

with up to 0.60” and

locally more elsewhere;

driest south

Mon-Tue 50% cvg of up to 0.40”

and local amts to 1.0”;

west Il. to central In.

driest

Tue-Wed 50% cvg of up to 0.75”

and local amts to 2.0”;

wettest north

Wed-Thu 60% cvg of up to 0.40”

and local amts to 1.0”;

wettest north

Thu-Oct 5 80% cvg of up to 0.75”

and local amts to 2.0”

Oct 5-6 80% cvg of up to 0.75”

and local amts to 1.50”

Oct 6-7 Up to 20% daily cvg of

up to 0.25” and locally

more each day

Oct 7-9 Up to 20% daily cvg of

up to 0.25” and locally

more each day

Oct 8-10 65% cvg of up to 0.75”

and locally more

Oct 10-11 60% cvg of up to 0.65”

and locally more

Oct 11-12 5-20% daily cvg of up

to 0.25” and locally

more each day

U.S. DELTA/SOUTHEAST SIGNIFICANT PRECIPITATION EVENTS

DELTA SOUTHEAST

Tdy-Sat Up to 15% daily cvg of

up to 0.25” and locally

more each day; some

days may be dry

Tdy-Sun 25-45% daily cvg of

up to 0.65” and locally

more each day; south

and east wettest

Sun-Tue 10-25% daily cvg of

up to 0.35” and locally

more each day

Mon-Tue 10-25% daily cvg of

up to 0.40” and locally

more each day;

wettest south

Wed-Thu Up to 20% daily cvg of

up to 0.20” and locally

more each day; some

days may be dry

Wed-Oct 5 Up to 20% daily cvg of

up to 0.20” and locally

more each day; some

days may be dry

Oct 5-6 80% cvg of up to 0.75”

and local amts to 1.50”

Oct 6-7 75% cvg of up to 0.75”

and local amts to 1.50”

Oct 7-8 5-20% daily cvg of up

to 0.30” and locally

more each day

Oct 8-9 5-20% daily cvg of up

to 0.30” and locally

more each day

Oct 9-12 Up to 20% daily cvg of

up to 0.20” and locally

more each day

Oct 10-12 Up to 20% daily cvg of

up to 0.20” and locally

more each day

Source: World Weather Inc. and FI

- USDA grain stockpiles for 3Q, including corn, soy, wheat, barley, noon

- USDA wheat production report for September, noon

- Polish crop estimates

- FranceAgriMer weekly updates on French crop conditions

- Globoil vegetable oil conference in Mumbai, final day

- ICE Futures Europe commitments of traders weekly report on coffee, cocoa, sugar positions, ~1:30pm ET (~6:30pm London)

- CFTC commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm

MONDAY, OCT. 1:

- China’s financial markets are closed through Oct. 7 for national holidays

- Futures trading including corn, wheat, sugar, palm oil, cotton will be halted in Shanghai, Dalian and Zhengzhou

- Australia on holiday

- AmSpec and SGS release their respective data on Malaysia’s palm oil exports for September

- USDA weekly corn, soybean, wheat export inspections, 11am

- USDA soybean crush for August, 3pm

- USDA weekly crop progress report including corn, soybeans, 4pm

- Ivory Coast weekly cocoa arrivals, and start date for main-crop harvest

- EARNINGS: Cal-Maine Foods

TUESDAY, OCT. 2:

- New Zealand dairy auction on Global Dairy Trade online market starts ~7am ET (~noon London, ~11pm Wellington)

- EARNINGS: PepsiCo

WEDNESDAY, OCT. 3:

- EIA U.S. weekly ethanol inventories, output, 10:30am

THURSDAY, 0CT. 4:

- FAO food index for September, 4am ET (9am London)

- USDA weekly net-export sales for corn, wheat, soy, cotton, 8:30am

- Port of Rouen data on French grain exports

- Buenos Aires Grain Exchange weekly crop report

- Bloomberg weekly survey of analysts’ expectations on grain, sugar prices

FRIDAY, OCT. 5:

- FranceAgriMer weekly updates on French crop conditions

- ICE Futures Europe commitments of traders weekly report on coffee, cocoa, sugar positions, ~1:30pm ET (~6:30pm London)

- CFTC commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm

Source: Bloomberg and FI

· There are no new record net short soybean oil positions for the week ending September 25.

· The traditional funds were more long than estimated for all the major agriculture commodities.

· US Crude Oil Futures Settle Up $1.13, 1.57 Pct At $73.25/bbl

· Brent Crude Futures Settle Up $1.00 or 1.22 pct at $82.72/bbl

· US Personal Income (M/M) Aug: 0.3% (est 0.4%; prev 0.3%)

– – Personal Spending (M/M) Aug: 0.3% (est 0.3%; prev 0.4%)

– – PCE Core (M/M) Aug: 0.0% (est 0.1%; prev 0.2%)

– – PCE Core (Y/Y) Aug: 2.0% (est 2.0%; prev 2.0%)

– – PCE Deflator (M/M) Aug: 0.1% (est 0.1%; prev 0.1%)

– – PCE Deflator (Y/Y) Aug: 2.2% (est 2.2%; prev 2.3%)

· Canadian GDP (M/M) Jul: 0.2% (est 0.1%; prev 0.0%)

Corn.

- Corn futures were trading near unchanged (two-sided) prior to the USDA report, and fell hard after USDA reported higher than expected September 1 corn stocks. Ongoing higher use of sorghum, DDGS, and soybean meal for feed, continues to eat into corn for feed. Corn basis at some US domestic locations eased on Thursday as US harvesting increased.

- December corn settled 8.50 cents lower, below its 20-day MA.

- Corn took the hardest hit out of the three major agriculture commodities as prices were higher five out of the six sessions.

- Funds sold an estimated 22,000 corn contracts.

· CFTC Commitment of traders showed for the week ending September 25th, managed money funds added net 28,497 net longs in corn, with the position at net short 112,779 contracts. (F&O combined).

- After USDA reported higher than expected stocks for soybeans, corn and wheat, we are concerned storage supplies will be tight this fall after the bumper corn and soybean crops are collected.

- France harvested 31 percent of their corn crop as of September 24, up from 8 percent week earlier.

· Safras & Mercado 2018-19 corn production was altered to 94.2 million tons from 93.05 previously.

USDA

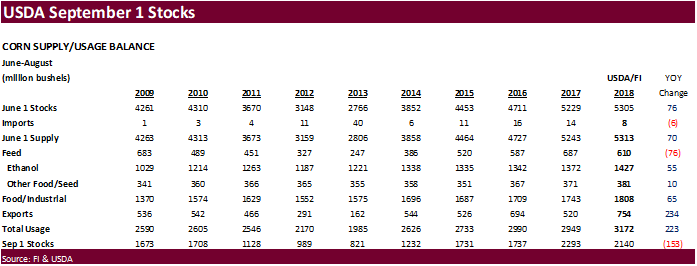

· USDA September 1 corn stocks came in 130 million bushels above the trade guess at 2.140 billion bushels (last year 58 below), down from 2.293 billion at the end of 2016-17. Our 2017-18 US corn for feed is estimated at 5.308 billion bushels, versus 5.450 billion for USDA.

· China sold 575,469 tons of corn at auction of state reserves at average price of 1,447 yuan ($210.21) per ton, 14.41 percent of total corn available for the auction. Yesterday China sold 2,903,808 tons of corn at auction of state reserves at an average price of 1,550 yuan ($225.49) per ton, 73.49 percent of total corn available at the auction.

· China will sell 8 million tons of corn for the week ending October 5.

· China sold about 85.5 million tons of corn out of reserves this season and some are predicting up to 100 million tons will be sold by the end of the marketing season.

Argentina corn remains most expensive for selected major exporting countries

Source: Reuters and FI

· December corn may trade in a $3.50-$3.80 range; March $3.25-$4.00

· CBOT soybeans fell 9.50 cents in the nearby two positions on higher than expected US September 1 soybean stocks. Soybean meal and soybean oil basis December fell $2.80/short ton and 16 points lower.

· Soybean oil futures over the next week could see limited downside on the recent firming of basis across the ECB and Gulf, but energy and palm prices will continue to have a good influence in price fluctuations.

· Funds sold an estimated 9,000 soybean contracts, sold 4,000 soybean meal and sold 3,000 soybean oil.

· CFTC Commitment of traders showed for the week ending September 25th, managed money funds added net 11,199 net longs in soybeans, with the position at net short 58,614 contracts. (F&O combined).

· Money managers last week reversed their record net short position by adding net 24,168 longs (F&O combined).

· China SBM hit multi month highs overnight.

· Safras & Mercado 2018-19 soybean production was altered to 121 million tons from 119.8 previously.

· Taiwan signed a ceremonial deal to buy $1.56 billion of soybeans from Iowa and Minnesota. (up to 3.9MMT).

· The European Commission increased its estimate for the rapeseed crop to 19.7MMT t from 19.2 last month, below 21.95 in 2017-18.

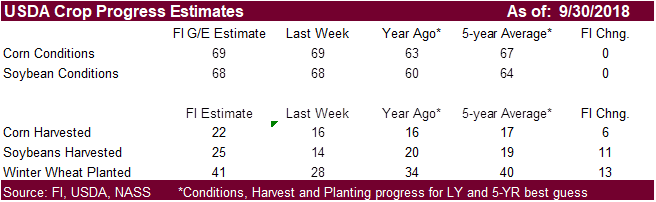

· US harvesting delays are in the spotlight but we think US harvest progress could advance a healthy 11 points to 25 percent, 6 points above average.

· Next week China is on a week-long holiday.

· China soybean crush margins on our analysis are running at 163 cents, up from 142 cents last session and compares to 115 late last week and 85 cents a year ago.

· One analyst expects India’s rapeseed crop to increase to 7 million tons from 6 million tons previously.

· Dorab Mistry expects Indonesian palm production to hit 40 million tons in 2018, up from previous forecast of 38.5 million tons, and noted palm prices to needed to decline to 2100MYR or $507.25/ton to remain competitive.

· Oil World looks for a 41MMT Indonesian palm output and 20.3MMT Malaysian palm production. Palm prices could trade between 2200-2600MRY in FH 2019.

· The USDA NASS crush report will be out on Monday. Reuters is using a 169.3 bu/ac crush and Bloomberg 168.3.

USDA

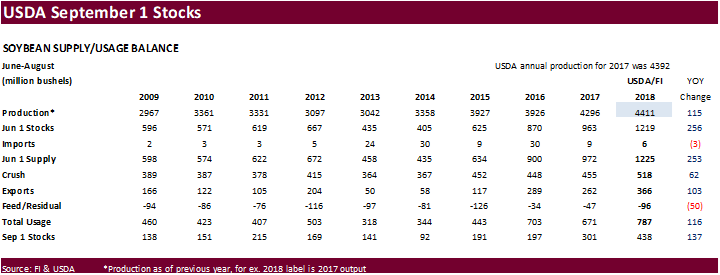

· 2017 soybean production is revised up 19.1 million bushels from the previous estimate. USDA noted the planted area was unchanged at 90.1 million acres, and harvested area is unchanged at 89.5 million acres. The 2017 yield, at 49.3 bushels per acre, is up 0.2 bushel from the previous estimate.

· For state changes, USDA increased 2017 soybean production for IA by 5.0 million bushels, KS by 2.6, MN by 4.0, Missouri by 3.0, and ND at 3.5 million bushels.

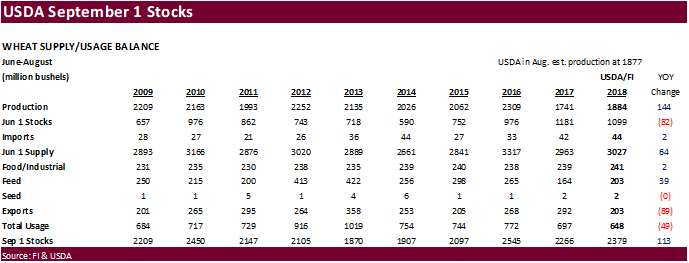

· See table after the text…

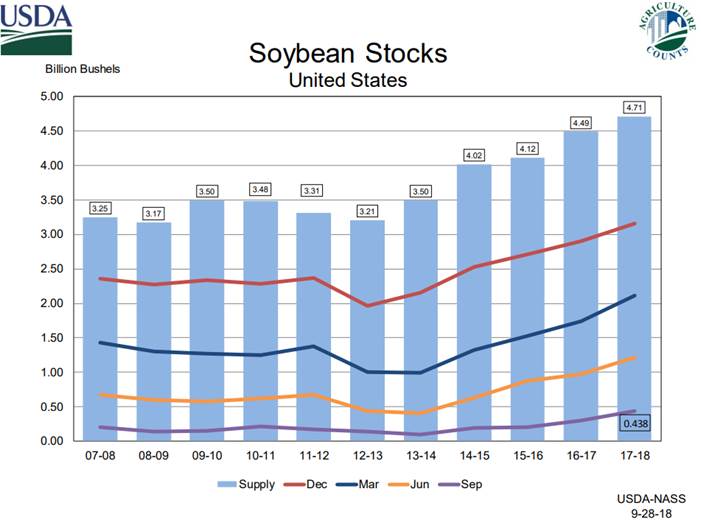

· US soybean stocks as of September 1 were reported at 428 million bushels, 37 million above a Reuters trade guess (last year soybeans were reported 37 million below the trade guess), and above 302 million at the end of 2016-17. We estimate the crop-year residual at 13 million bushels versus 32 million by USDA.

- China will offer 100,000 tons of soybeans out of reserves on October 10.

Source: Reuters and FI

· November soybeans are seen in a $8.05-$8.85 range, March $7.85-$9.15

· December soybean meal $305-$340 range; March $295-$400

· December soybean oil 27.80-30.50; March 28.60-31.50

· US wheat ended lower ked by KC and MN. Chicago wheat was mixed and KC & MN mostly weaker prior to the Small Grains Summery. After USDA increased 2018 wheat production and reported a higher September 1 all-wheat stocks, prices turned lower, rebounded on a short burst of fund buying, and traded lower again to settle lower.

· Chicago finished 1.25-4.00 cents lower, KC 2.50-6.50 lower and MN 2.25-7.50 cents lower.

- Funds sold 5,000 SRW wheat contracts.

· CFTC Commitment of traders showed, from the previous week, managed money funds added a small amount of net longs in SRW wheat, sold net 3,054 KC longs, and added only 53 longs in MN. (F&O combined).

· Ukraine planted 3.3 million hectares of the planned 7.2 million hectares for winter grains, or 46 percent, including 3.1 million hectares of winter wheat.

USDA

· 2018 all-wheat production was upward revised 7 million bushels but came in 12 million bushels above trade expectations. USDA upward revised the other spring wheat crop by 9 million bushels to 623 million, 14 million above expectations. USDA also took up the durum crop by 4 million bushels from its August estimate and revised lower the winter wheat crop by 5 million bushels.

· As a result, wheat prices took a hit, but rebounded, only to trade lower gain in afternoon trading. We look for a good area expansion in 2019 amid expansion in winter wheat plantings. Prices are higher than this time last year.

· September 1 all wheat stocks of 2.379 billion bushels were 36 million above trade expectations (trade missed last year’s number, with it 48 higher). We look for USDA to lower its 2018-19 US wheat for feed by 5 million bushels on October 11 to 125 million bushels.

- China sold 5,959 tons of imported 2013 wheat at auction of state reserves at an average price of 2,200 yuan ($319.82) per ton, 0.64 percent of total wheat available at the auction.

- Postponed: UAE seeks 60,000 tons of wheat for Oct/Nov shipment.

- Results awaited: Ethiopia seeks 200,000 tons of milling wheat for shipment two months after contract signing. Ethiopia got offers from 7 firms. Lowest offer was for 100,000 tons at $272.05/ton, c&f.

- Morocco seeks 336,364 tons of US durum wheat on September 28 for arrival by December 31.

- Bahrain seeks 25,000 tons of wheat on October 2 for Nov shipment.

- Taiwan seeks 110,000 tons of US wheat on October 2 for Nov-Dec shipment.

- Jordan retendered for another 100,000 tons of feed barley on October 3.

- Bangladesh seeks 50,000 tons of 12.5 percent wheat on October 9, optional origin.

- Japan in a SBS import tender seeks 120,000 tons of feed wheat and 200,000 tons of barley on October 10 for arrival by late February.

Rice/Other

· The Philippines seek 250,000 tons of rice on October 18 for arrival by late November.

· Mauritius seeks 9,000 tons of rice for delivery between Nov. 15, 2018, and March 31, 2019, set to close is Sept. 27.

· Thailand seeks to sell 120,000 tons of sugar on October 3.

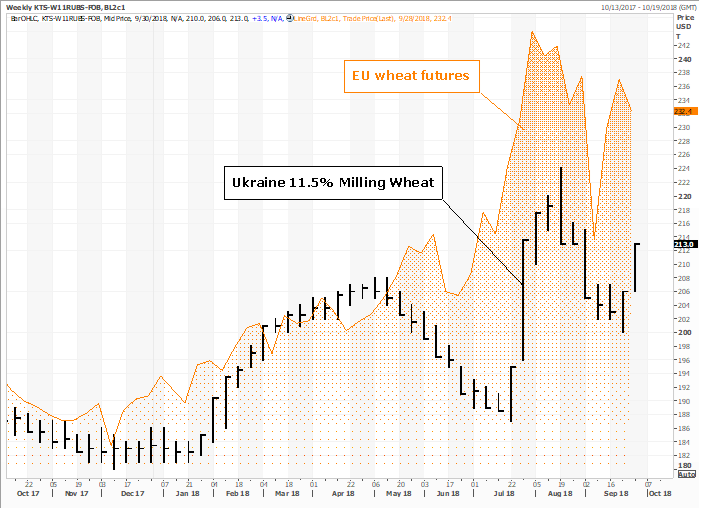

EU wheat remains at a hefty premium over Ukraine milling wheat

Source: Reuters and FI

9/28/18. Trading ranges:

- December Chicago wheat $4.95-$5.25; March $5.10-$5.90.

- December KC $5.00-$5.35; March $5.00-$6.00. (remain tight with Chicago)

- December MN $5.60-$6.25 range; March $5.75-$7.00

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International │190 S LaSalle St., Suite 410│Chicago, IL 60603

W: 312.604.1366

AIM: fi_treilly

ICE IM: treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.

This email, any information contained herein and any files transmitted with it (collectively, the Material) are the sole property of OTC Global Holdings LP and its affiliates (OTCGH); are confidential, may be legally privileged and are intended solely for the use of the individual or entity to whom they are addressed. Unauthorized disclosure, copying or distribution of the Material, is strictly prohibited and the recipient shall not redistribute the Material in any form to a third party. Please notify the sender immediately by email if you have received this email by mistake, delete this email from your system and destroy any hard copies. OTCGH waives no privilege or confidentiality due to any mistaken transmission of this email.