From: Terry Reilly

Sent: Monday, August 27, 2018 6:00:28 PM (UTC-06:00) Central Time (US & Canada)

Subject: FI Evening Grain Comments 08/27/18

PDF attached

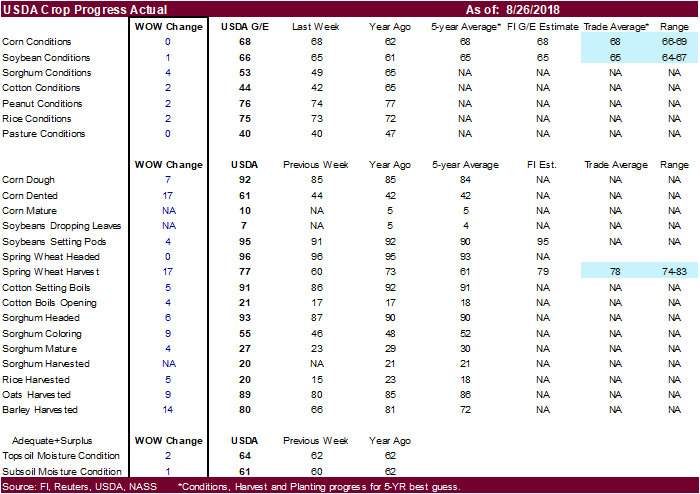

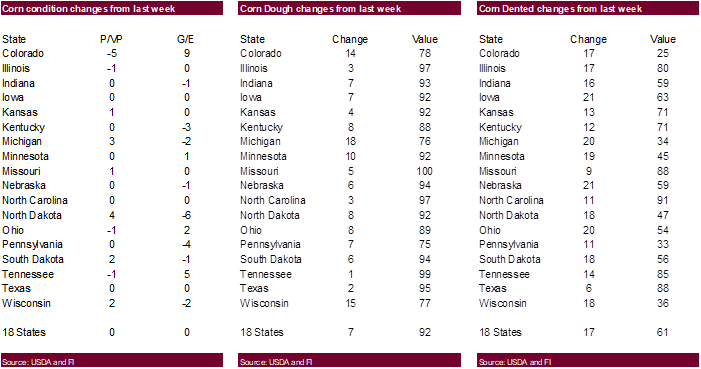

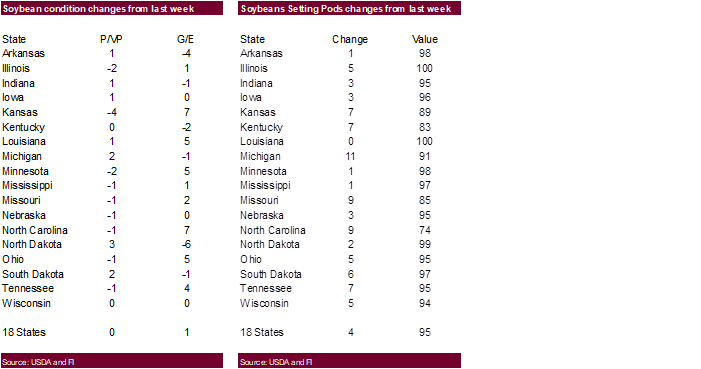

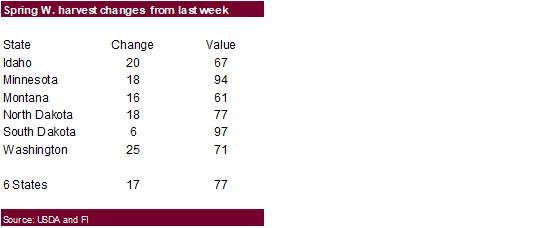

· US crop conditions were unchanged in the combined good/excellent categories for corn (down one good and up one in excellent). The trade was looking for unchanged. For soybeans G/E conditions increased one point (up one in excellent). The trade was looking for unchanged. Spring wheat harvesting progress increased 17 points to 77 percent, one point below a Reuters estimate, and 16 points above a 5-year average.

· Eastern Australia’s saw as expected rain over the weekend.

· Western Australia could see rain Tuesday and Wednesday.

· Argentina was dry.

· Argentina will receive rain Wednesday into Friday of this week.

· Frost possible in northwestern U.S. Plains and southwestern Canada’s Prairies Tuesday.

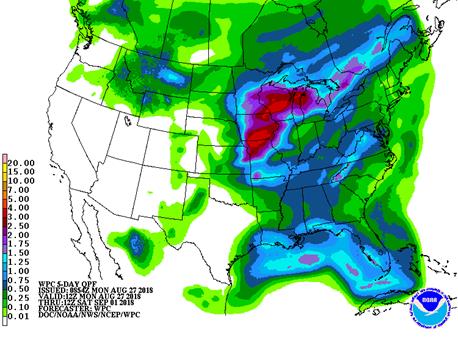

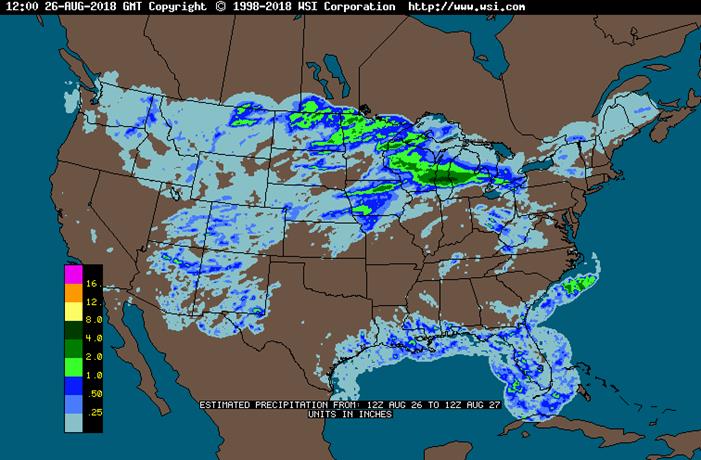

· Central Missouri, parts of TN, northern MI and northern Minnesota are still in need of rain.

· The Delta will see rain this week.

· The two-week outlook calls for favorable weather across the US.

· West Texas will experience net drying over the coming week.

· Eastern China will see net drying through at least August 29.

· Canada’s Prairies will see badly needed rain today.

· Indonesia and Malaysia rainfall are slowing and some attribute the below normal rainfall to El Nino.

SIGNIFICANT CORN AND SOYBEAN BELT PRECIPITATION EVENTS

WEST CORN BELT EAST CORN BELT

Tdy-Tue 70% cvg of 0.35-1.40”

and local amts to 2.50”

from Ks. to Wi. with up

to 0.65” and locally

more elsewhere

Tue-Wed 85% cvg of up to 0.75”

and local amts to 1.50”;

wettest NW

Wed 15% cvg of up to 0.40”

and locally more;

far south wettest

Thu 20% cvg of up to 0.40”

and local amts to 0.85”;

wettest south

Thu-Fri 75% cvg of up to 0.75”

and local amts to 1.50”

with some 1.50-3.50”

amts in the south; far

NW driest

Fri-Sun 85% cvg of up to 0.75”

and local amts to 1.50”

with some 1.50-3.0”

amts in the west

Sat-Sun 35% cvg of up to 0.75”

and local amts to 2.0”;

wettest south

Sep 3-5 10-25% daily cvg of

up to 0.75” and locally

more each day;

wettest north

Sep 3-6 5-20% daily cvg of up

to 0.30” and locally

more each day

Sep 6-8 65% cvg of up to 0.70”

and locally more

Sep 7-9 60% cvg of up to 0.50”

and locally more

Sep 9-10 10-25% daily cvg of

up to 0.35” and locally

more each day

U.S. DELTA/SOUTHEAST SIGNIFICANT PRECIPITATION EVENTS

DELTA SOUTHEAST

Tdu-Tue 10-25% daily cvg of

up to 0.35” and locally

more each day;

wettest south

Tue 25% cvg of up to 0.40”

and locally more;

wettest south

Wed-Thu 85% cvg of up to 0.75”

and local amts to 1.50”

Wed-Fri 80% cvg of up to 0.75”

and local amts to 1.50”

Fri-Sep 3 5-20% daily cvg of up

to 0.30” and locally

more each day

Sat-Sep 3 15-35% daily cvg of

up to 0.40” and locally

more each day

Sep 4-7 5-20% daily cvg of up 5-20% daily cvg of up

to 0.30” and locally to 0.35” and locally

more each day more each day

Sep 8-10 10-25% daily cvg of 10-25% daily cvg of

up to 0.35” and locally up to 0.35” and locally

more each day more each day

Source: World Weather and FI

Bloomberg weekly agenda

MONDAY, AUG. 27:

- U.K. summer bank holiday

- SGS data for Malaysia’s Aug. 1-25 palm oil exports, 3am ET (3pm Kuala Lumpur)

- EU’s monthly Monitoring Agricultural Resources (MARS) bulletin on crop progress and weather conditions in Europe, 7am ET (noon London)

- EU weekly grain, oilseed import and export data, 10am ET (3pm London)

- USDA weekly corn, soybean, wheat export inspections, 11am

- USDA weekly crop progress report, 4pm

- Ivory Coast weekly cocoa arrivals

TUESDAY, AUG. 28:

- Palm Oil Trade Fair & Seminar in Kuala Lumpur, Aug. 28-29. Speakers include Oil World Executive Director Thomas Mielke, LMC Intl Chairman James Fry and Godrej Director Dorab Mistry

WEDNESDAY, AUG. 29:

- EIA U.S. weekly ethanol inventories, output, 10:30am

THURSDAY, AUG. 30:

- USDA weekly net-export sales for corn, wheat, soy, cotton, 8:30am

- Port of Rouen data on French grain exports

- Buenos Aires Grain Exchange weekly crop report

- Bloomberg weekly survey of analysts’ expectations on grain, sugar prices

FRIDAY, AUG. 31:

- Malaysia on holiday; No palm oil futures trading on Bursa Malaysia Derivatives

- Statistics Canada’s domestic crop production report for July, 8:30am ET

- FranceAgriMer weekly updates on French crop conditions

- ICE Futures Europe commitments of traders weekly report on coffee, cocoa, sugar positions, ~1:30pm ET (~6:30pm London)

- CFTC commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm

CME plans to increase storage fees for corn and soybeans.

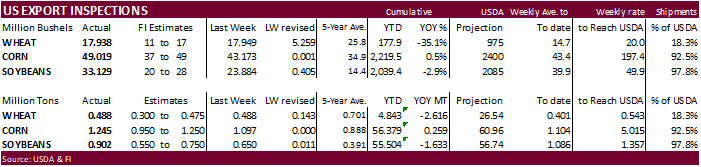

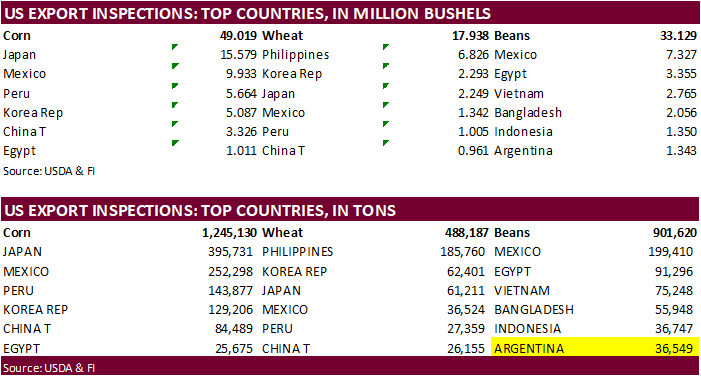

USDA inspections versus Reuters trade range

Wheat 488,187 versus 300000-500000 range

Corn 1,245,130 versus 900000-1250000 range

Soybeans 901,620 versus 500000-850000 range

GRAINS INSPECTED AND/OR WEIGHED FOR EXPORT

REPORTED IN WEEK ENDING AUG 23, 2018

— METRIC TONS —

CURRENT PREVIOUS

———– WEEK ENDING ———- MARKET YEAR MARKET YEAR

GRAIN 08/23/2018 08/16/2018 08/24/2017 TO DATE TO DATE

BARLEY 514 367 0 2,397 12,227

CORN 1,245,130 1,096,647 835,796 56,378,641 56,119,547

FLAXSEED 24 0 98 170 3,575

MIXED 0 0 0 24 24

OATS 0 0 0 1,198 1,497

RYE 0 0 0 0 0

SORGHUM 90,296 76,306 124,496 5,062,112 5,933,909

SOYBEANS 901,620 650,021 738,552 55,503,869 57,136,551

SUNFLOWER 0 0 0 335 383

WHEAT 488,187 488,489 690,707 4,842,725 7,458,784

Total 2,725,771 2,311,830 2,389,649 121,791,471 126,666,497

CROP MARKETING YEARS BEGIN JUNE 1 FOR WHEAT, RYE, OATS, BARLEY AND

FLAXSEED; SEPTEMBER 1 FOR CORN, SORGHUM, SOYBEANS AND SUNFLOWER SEEDS.

INCLUDES WATERWAY SHIPMENTS TO CANADA.

USDA announcement on trade damage assistance (partial)

U.S. Secretary of Agriculture Sonny Perdue today announced details of actions the U.S. Department of Agriculture (USDA) will take to assist farmers in response to trade damage from unjustified retaliation by foreign nations. President Donald J. Trump directed Secretary Perdue to craft a short-term relief strategy to protect agricultural producers while the Administration works on free, fair, and reciprocal trade deals to open more markets in the long run to help American farmers compete globally. As announced last month, USDA will authorize up to $12 billion in programs, consistent with our World Trade Organization obligations.

“Early on, the President instructed me, as Secretary of Agriculture, to make sure our farmers did not bear the brunt of unfair retaliatory tariffs. After careful analysis by our team at USDA, we have formulated our strategy to mitigate the trade damages sustained by our farmers. Our farmers work hard, and are the most productive in the world, and we aim to protect them,” said Secretary Perdue.

These programs will assist agricultural producers to meet the costs of disrupted markets:

· USDA’s Farm Service Agency (FSA) will administer the Market Facilitation Program (MFP) to provide payments to corn, cotton, dairy, hog, sorghum, soybean, and wheat producers starting September 4, 2018. An announcement about further payments will be made in the coming months, if warranted.

· USDA’s Agricultural Marketing Service (AMS) will administer a Food Purchase and Distribution Program to purchase up to $1.2 billion in commodities unfairly targeted by unjustified retaliation. USDA’s Food and Nutrition Service (FNS) will distribute these commodities through nutrition assistance programs such as The Emergency Food Assistance Program (TEFAP) and child nutrition programs.

· Through the Foreign Agricultural Service’s (FAS) Agricultural Trade Promotion Program (ATP), $200 million will be made available to develop foreign markets for U.S. agricultural products. The program will help U.S. agricultural exporters identify and access new markets and help mitigate the adverse effects of other countries’ restrictions.

“President Trump has been standing up to China and other nations, sending the clear message that the United States will no longer tolerate their unfair trade practices, which include non-tariff trade barriers and the theft of intellectual property. In short, the President has taken action to benefit all sectors of the American economy – including agriculture – in the long run,” said Secretary Perdue. “It’s important to note all of this could go away tomorrow, if China and the other nations simply correct their behavior. But in the meantime, the programs we are announcing today buys time for the President to strike long-lasting trade deals to benefit our entire economy.”

Additional facts/FI comments in italic

· USDA SAYS PAYMENTS TO WHEAT FARMERS 14 CENTS PER BUSHEL TIMES 50 PCT OF PRODUCTION; SORGHUM 86 CENTS PER BUSHEL; SOYBEANS $1.65 PER BUSHEL; CORN 1 CENT PER BUSHEL; COTTON 6 CENTS PER POUND

· We think this was a one-time deal, so it should not influence 2019 planting decisions.

· USDA SAYS HOG FARMER PAYMENTS $8 PER PIG TIMES 50 PCT AUG 1 PRODUCTION; DAIRY FARMERS ALSO ELIGIBLE FOR PAYMENTS

· USDA SAYS DIRECT PAYMENTS TO FARMERS TO BE WORTH $4.7 BLN; MAY BE LATER PAYMENT; $3.6 BLN OF THAT IS SOYBEANS The $3.6 billion does not cover the real cost of China pulling the rug under US soybean exports

· USDA SAYS PLANS $1.2 BLN IN COMMODITY PURCHASES TO BE SPREAD OUT OVER SEVERAL MONTHS, INCLUDING PORK AND DAIRY PRODUCTS

· USDA SAYS DIRECT PAYMENT LIMIT $125,000 PER PERSON (Reuters) We think this is the total payment.

· Payments are for the 2018-19 crop year

· Most of the producers are in the farm program. Many large producers are not in the program because of the restrictions by the government.

· We figure this program will apply to up to about 1500 acres for soybeans.

Corn.

- Corn futures traded lower but settled well off session lows after the US and Mexico reached a trade deal. December corn hit its lowest level since July 16 before pairing some of its losses.

- Funds sold an estimated net 6,000 contracts.

· US crop conditions were unchanged in the combined good/excellent categories for corn (down one good and up one in excellent). The trade was looking for unchanged.

- Mexico and US made a trade deal. https://www.whitehouse.gov/briefings-statements/remarks-president-trump-phone-call-president-pena-nieto-mexico-united-states-mexico-trade-agreement/

- This news underpinned US hog and cattle futures and paired losses for corn futures.

- Details of the agreement are lacking, but it will likely encompass free trade in agriculture.

- One thing is for sure. Mexico already bought a large amount of corn from the United States for 2017-18 and made large purchases already for 2018-19.

- Mexico imported 14.3MMT of corn from the US in 2016-17. USDA 2017-18 export sales commitments for Mexico are running at 15.3MMT, up from 13.94MMT a year ago.

- Canada and the US plan to meet as early as Tuesday.

- USDA US corn export inspections as of August 23, 2018 were 1,245,130 tons, within a range of trade expectations, above 1,096,647 tons previous week and compares to 835,796 tons year ago. Major countries included Japan for 395,731 tons, Mexico for 252,298 tons, and Peru for 143,877 tons.

- Purdue University Extension school in a report indicated U.S. farm income, on average, for 2018 could end up near early 2000’s levels, and 35% to 40% lower than average income during the 2011 through 2014 years.

· The European Union crop monitoring service, MARS, lower the EU rapeseed yield to 2.87 tons/hectare from 2.89 last month.

- South Africa’s CEC on August 28 will update their corn production next week and a Reuters poll calls for 13.11 million tons, down 0.7 percent from the 13.207 million tons in July.

- South Korea increased food safety controls after African swine fever was discovered in China.

- China’s swine fever has prompted Shandong banned live hogs and products from entering the province.

US crop conditions.

· US crop conditions were unchanged in the combined good/excellent categories for corn (down one good and up one in excellent). The trade was looking for unchanged.

· Our weighted rating was unchanged from the previous week at 82.2, a tenth below a 5-year average.

· Our September corn yield estimate is 175.5 bushels per acre.

· Our US corn production is 14.355 billion bushels, 231 million below last year.

· FC Stone is due out with US production estimates on August 30.

· ProFarmer is at 14.501 billion bushels with a yield of 177.3.

· Another 4 million tons of China corn reserves will be offered on Thursday and Friday.

· China sold about 65.4 million tons of corn out of reserves this season.

· Soybean prices hit session lows early and paired some losses for several reasons. USDA unveiled their trade damage payment plan for producers and soybean and pork farmers appear will benefit most from the program. $3.6 billion of the $4.7 billion set aside for producer payments will go to soybean producers (with a cap for each producer). About 1500 acres max could take benefits, in our view. The US also announced a trade deal with Mexico which helped bring the soybean market back. USDA export inspections showed soybeans for Argentina (36,549 tons). What pressured the market early was the Friday afternoon results of the ProFarmer crop tour that pegged the soybean yield above USDA’s August estimate. Technicals are bearish. US weather forecast remains favorable for the most part. Eastern Australia saw rain over the weekend which is good for canola production.

· Soybeans ended 10 above their lows, down 7.25 cents in September and 7.00 cents in November. November soybeans hit a mid-July low.

· Soybean meal fell $3.320-6.40 led by the nearly contracts. December meal hit its lowest level since September 14.

· Soybean oil ended higher on strength in WTI and unwinding of meal/oil spreading.

· Funds sold 6,000 soybeans, sold 5,000 soybean meal and bought 4,000 soybean oil.

· US soybean crop conditions in the combined G/E categories increased one point (up one in excellent). The trade was looking for unchanged.

- USDA US soybean export inspections as of August 23, 2018 were 901,620 tons, above a range of trade expectations, above 650,021 tons previous week and compares to 738,552 tons year ago. Major countries included Mexico for 199,410 tons, Egypt for 91,296 tons, and Vietnam for 75,248 tons.

- Note First Notice Deliveries are on Friday. There are only 12 soybean registrations, zero meal and 3,719 soybean oil.

- Brazil’s top court plans to rule on the constitutionality of the recent freight law.

· The European Union crop monitoring service, MARS, lower the EU corn yield to 7.57 tons/hectare from 7.64 last month.

· Cargo surveyor SGS reported month to date August 25 Malaysian palm exports at 786,947 tons, 123,827 tons below the same period a month ago or down 14%, and 169,600 tons below the same period a year ago or down 18%.

· AmSpec reported August 1-25 Malaysian palm exports at 821,485 tons, down 9 percent from the same period a month ago.

· ITS reported August 1-25 Malaysian palm exports at 835,134 tons, down 9.4 percent from the same period a month ago.

· November Malaysian palm decreased 20MYR to 2199, a one-week low.

· On Monday China soybean meal futures hit a 6-week low.

· China has been increasing hog slaughter while replacement piglets are slowing.

US crop conditions.

· US soybean crop conditions in the combined G/E categories increased one point (up one in excellent). The trade was looking for unchanged.

· Our weighted rating increased 0.3% to 81.8, matching a 5-year average. This is the first increase for our weighted index since July 22.

· We increased our US soybean yield by a 0.5 bu/ac to 50.5 bushels. USDA is at 51.6 bushels.

· Our US soybean production estimate is 4.481 billion bushels, 44 million above the previous week, and 89 million above last year.

· FC Stone is due out with US production estimates on August 30.

· ProFarmer is at 53.0 bushels per acre and 4.683-billion-bushels.

· Egypt’s GASC seeks at least 30,000 tons of soyoil and 10,000 tons of sunflower oil on Wednesday for arrival Oct 1-15.

· South Korea seeks 15,000 tons of non-GMO soybeans on September 4 for Nov/Dec arrival.

· The CCC seeks 15,610 tons of crude degummed soybean oil on August 29 for export to Pakistan. Shipment was for Sep 27 to Oct 7.

- USDA seeks 5,000 tons of refined oil for the export program on September 5 for October shipment.

- During the week ending August 31, China plans to sell 301,200 tons of 2013 soybeans, 60,100 tons of 2011-2013 rapeseed oil, and 53,800 tons of imported 2011 soybean oil.

- China sold nearly 1.3MMT of soybeans out of reserves this season.

- Iran seeks 30,000 tons of sunflower oil on September 24.

· US wheat futures ended lower (for the sixth straight session) after eastern Australia saw rain over the weekend. Russia export wheat prices fell last week. US weather forecast remains favorable.

· China announced they will release wheat out of reserves. China summer wheat production fell 2.4 percent to 128.35 million tons.

· Chicago December wheat hit its lowest level since July 18, KC December reached its lowest level since July 24 and December Minneapolis July 25 low.

· Funds sold 8,000 Chicago wheat.

· After the close Egypt’s GASC announced they seek optional origin wheat for October 11-20 shipment.

- USDA US all-wheat export inspections as of August 23, 2018 were 488,187 tons, within a range of trade expectations, below 488,489 tons previous week and compares to 690,707 tons year ago. Major countries included Philippines for 185,760 tons, Korea Rep for 62,401 tons, and Japan for 61,211 tons.

· EU December wheat was 3.75 euro lower at 199.00 euros, down nearly 1.9%.

· Weekly EU trade data is delayed.

· The European Union crop monitoring service, MARS, lower the EU soft wheat yield to 5.70 tons/hectare from 5.82 last month.

- Russia wheat export prices softened last week on harvest pressure. IKAR reported 12.5% at $225.00/ton fob, down $5/ton from previous week. SovEcon reported $225/ton, down $2.

- Ukraine does not have any plans to revisit the export cap of 8 million tons of milling wheat for the current crop-year.

US spring wheat harvesting progress increased 17 points to 77 percent, one point below a Reuters estimate, and 16 points above a 5-year average.

Export Developments.

· China sold 5,631 tons of 2013 imported wheat at 2,379 yuan per ton ($346.09/ton), 0.35 percent of what was offered.

· Jordan seeks 120,000 tons of feed barley on August 28.

· Jordan seeks 120,000 tons of hard milling wheat on Aug 29 for Nov/Dec shipment.

- Japan in a SBS import tender seeks 120,000 tons of feed wheat and 200,000 tons of barley on August 29 for arrival by January 31.

· Taiwan seeks 110,500 tons of US milling wheat from the US on August 31 fir October/November shipment.

Rice/Other

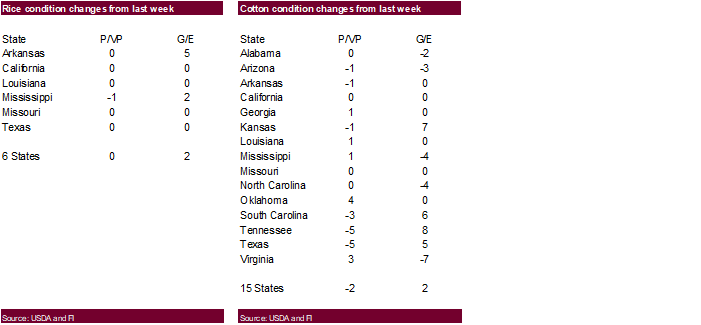

· China sold 51,873 tons of rice from reserves at 2,653 yuan per ton ($385.95/ton), 6 percent of what was offered.

· The Philippines will imports 132,000 tons of rice soon.

· South Korea seeks 92,783 tons of rice on Aug. 31 for Nov/Dec arrival.

TONNES(M/T) GRAIN TYPE ARRIVAL/PORT

10,000 Brown medium Nov 30/Gwangyang

10,000 Brown medium Dec 31/Busan

20,000 Brown medium Dec 31/Gunsan

20,000 Brown medium Dec 31/Mokpo

20,000 Brown medium Dec 31/Donghae

12,783 Brown long Nov 30/Masan

· Results awaited: Egypt’s ESIIC seeks 100,000 tons (150k previously) of raw sugar for shipment within the first half of September and two 50,000-ton shipments from September 15-Oct 15.

· Results awaited: Thailand plans to sell 120k tons of raw sugar on Aug. 22.

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International │190 S LaSalle St., Suite 410│Chicago, IL 60603

W: 312.604.1366

AIM: fi_treilly

ICE IM: treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.