From: Terry Reilly [mailto:treilly@futures-int.com]

Sent: Wednesday, June 20, 2018 4:49 PM

Subject: FI Evening Grain Comments 06/20/18

PDF attached

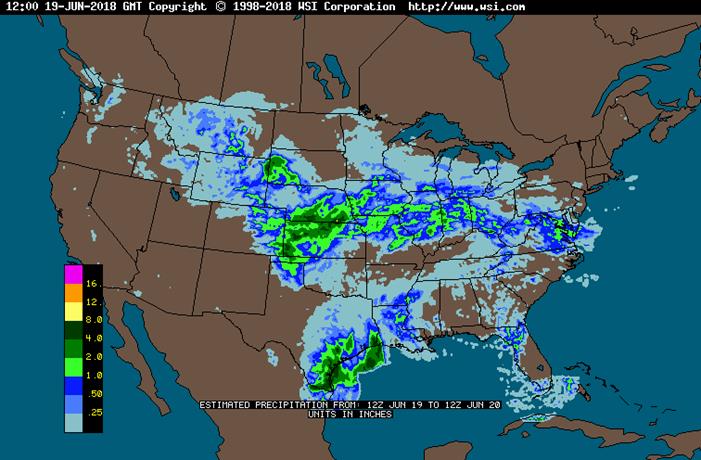

· Greatest rainfall will occur in Kansas, Nebraska, northeastern Colorado, and southwestern portions of the Corn Belt.

· In late June through early July, a higher-pressure ridge will return across the middle of the United States, resulting in drier and warmer conditions. June 30-July 4 is when the models are putting the ridge in. Note this ridge is not expected to be strong with all the moisture on the ground, and rain may result when hot air mixes with cooler air.

· Some rain is also still expected in West Texas through early next week.

· The Canada’s Prairies will dry down this week with above normal temperatures.

· North China Plain will additional rain June 20-22 aiding corn and soybeans. 90% of the winter wheat crop had been collected.

· France and Germany will dry down this week.

· Western Australia will see another chance for rain, but won’t occur until early next week.

· Drought will continue in Queensland and northern New South Wales through June 27.

Source: World Weather Inc. and FI

SIGNIFICANT CORN AND SOYBEAN BELT PRECIPITATION EVENTS

WEST CORN BELT EAST CORN BELT

Tdy-Thu 65% cvg of up to 0.75”

and local amts to 2.0”

with a few 2.0-4.0”

bands from east-central

and SE S.D. to south

Mn.; N.D. to north

Wisc. driest

Tdy-Fri 90-100% cvg of 0.20-1.30”

and local amts to 2.50”

with a few 2.50-3.50”

bands and lighter rain in

a few areas; Mi. driest

Fri-Sun 15-30% daily cvg of

up to 0.40” and locally

more each day; central

areas driest

Sat-Sun 20-40% daily cvg of up

to 0.50” and local amts

over 1.0” each day;

wettest south

Mon 15% cvg of up to 0.20”

and locally more;

wettest west

Mon-Jun 27 75% cvg of up to 0.75”

and local amts to 2.0”;

wettest south

Tue-Jun 27 75% cvg of up to 0.75”

and local amts to 2.0”;

wettest west

Jun 28 25% cvg of up to 0.65”

and locally more

Jun 28-29 10-25% daily cvg of

up to 0.30” and locally

more each day

Jun 29-Jul 1 70% cvg of up to 0.75”

and locally more

Jun 30-Jul 2 75% cvg of up to 0.75”

and locally more

Jul 2-4 15-30% daily cvg of

up to 0.35” and locally

more each day

Jul 3-4 15-30% daily cvg of

up to 0.35” and locally

more each day

U.S. DELTA/SOUTHEAST SIGNIFICANT PRECIPITATION EVENTS

DELTA SOUTHEAST

Tdy-Thu 100% cvg of 0.25-1.40”

and local amts to 3.0”;

far north driest

Tdy-Fri 80% cvg of up to 0.75”

and local amts to 2.0”;

west and north wettest

Fri-Sun 45% cvg of up to 0.75”

and local amts to 2.0”;

wettest north

Sat-Sun 10-25% daily cvg of

up to 0.60” and locally

more each day

Mon-Jun 27 5-20% daily cvg of up

to 0.25” and locally

more each day

Mon-Tue 65% cvg of up to 0.75”

and local amts to 2.0”

Jun 27-30 5-20% daily cvg of up

to 0.30” and locally

more each day

Jun 28-30 5-20% daily cvg of up

to 0.30” and locally

more each day

Jul 1-4 10-25% daily cvg of 10-25% daily cvg of

up to 0.30” and locally up to 0.40” and locally

more each day more each day

SIGNIFICANT PRECIPITATION EVENTS FOR BRAZIL

Thu-Sat 15% cvg of up to 0.60” and local amts to 1.20”;

far south wettest

Sun-Tue 15% cvg of up to 0.75” and local amts to 2.0”;

south Parana and north Santa Catarina wettest

Jun 27-28 15% cvg of up to 0.65” and locally morel;

far south wettest

Jun 29-Jul 1 5-20% daily cvg of up to 0.30” and locally more

each day; wettest NE

Jul 2-4 15% cvg of up to 0.75” and locally more;

wettest south

SIGNIFICANT PRECIPITATION EVENTS FOR ARGENTINA

Tdy-Fri 5-15% daily cvg of up to 0.25” and locally

more each day; Entre Rios wettest

Sat 25% cvg of up to 0.40” and locally more;

Corrientes wettest

Sun-Tue Up to 15% daily cvg of up to 0.20” and locally

more each day; some days may be dry

Jun 27-28 15% cvg of up to 0.50” and locally more;

wettest NE

Jun 29-Jul 1 20% cvg of up to 0.60” and locally more;

wettest SE

Jul 2-4 Up to 20% daily cvg of up to 0.25” and locally

more each day

Source: World Weather Inc. and FI

THURSDAY, JUNE 21:

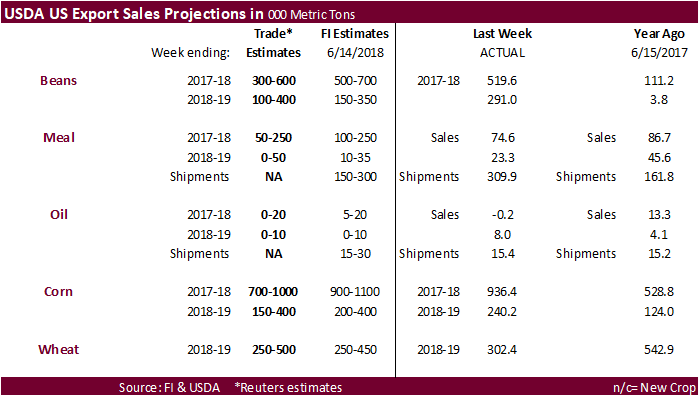

- USDA weekly crop net-export sales for corn, wheat, soy, cotton, 8:30am

- USDA red meat production data for May, 3pm

- Buenos Aires Grain Exchange weekly crop report

- EU weekly grain, oilseed import and export data

- Port of Rouen data on French grain exports

- Bloomberg weekly survey of analysts’ expectations on grain, sugar prices

FRIDAY, JUNE 22:

- USDA cold-storage report, cattle-on-feed figures for May, both at 3pm

- FranceAgriMer weekly updates on French crop conditions

- ICE Futures Europe commitments of traders weekly report on coffee, cocoa, sugar positions, ~1:30pm ET (~6:30pm London)

- CFTC commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm

SATURDAY, JUNE 23:

- China scheduled to release May commodities trade data (final), including imports of palm oil, cotton, 2:30am ET (2:30pm Beijing)

Corn.

· Corn ended slightly higher (0.50 cent July and 0.25 December) after contracts reach all-time lows on Tuesday. Traders backed away from China/US trade tensions.

· Funds sold an estimated net 3,000 corn contracts.

· The US House may revote on the Farm Bill on June 22. Immigration is still a hot topic.

· US ethanol exports to China should hit a standstill. China will increase its taxes on US ethanol soon to 70%, consisting of a 25% import duty added to the already established 15% tax place in April and 30% general import tariff that existed since last year.

· Look for an announcement on 2019 biofuel policy on Friday or sometime next week.

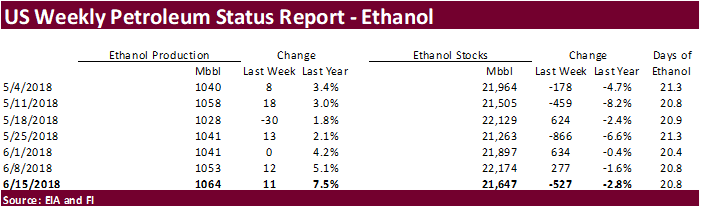

· Weekly production is about 7.5% above this time a year ago and stocks are 2.8% lower.

· Crop-year to date ethanol production (Sep-Jun 15) is running 2.5% above a year ago.

· Days of inventory are running at 20.8, versus 20.9 last month and 22.8 a year ago.

· Total ethanol blended into finished motor gasoline was running at 92.8%, slightly down from the previous week.

· We are using 5.585 billion bushels for corn for ethanol usage, 10 million above USDA.

· South Korea’s MFG bought 138,000 tons of corn at $207.99/ton c&f for November arrival.

· South Korea bought a combined 1.5 million tons of corn so far in June. They are taking advantage of the lower prices.

· Brazil looks to sell corn out of reserves soon.

· China sold an estimated 44.7 million tons of corn out of reserves since April 12.

· Soybeans ended mixed in a choppy trade. Soybeans were down hard earlier but rebounded after a report Brazil was having trouble delivering soybeans for export. Soybean meal ended lower and soybean oil finished strong in part to higher crude oil and rally in the (ethanol) RIN market.

· Funds sold 4,000 soybeans, sold 3,000 soybean meal, and bought 5,000 soybean oil.

· Brazil’s National Agriculture Confederation (CNA) said 6.8 million tons of soybeans and soymeal exports were delayed due unresolved truck freight prices between trucker companies and grain handlers. About 60 ships have been impacted by delays and losses are estimated at 135 million reals from fines. Brazil’s high court said truckers and companies will try to reach an agreement on freight prices by next week. (Reuters)

· We heard Sep Brazil soybeans were offered at 200 over this afternoon, up 60 from a week ago.

· China soybean stocks at ports are running at 8.63 million tons as of late last week, according to the CNGOIC, up 1.89 million tons from the previous week. June soybean imports are seen at 9.5 million tons, July at 9.0 million tons and August at 8.8 million tons. The CNGOIC also noted China may see a shortage on soybean supplies during Q4 from thinning SA availability.

· Cargo surveyor SGS reported June 1-20 Malaysian palm exports at 670,442 tons, down 74,867 tons or 10% from the same period a month ago and down 39,880 tons from the same period a year ago (6% decrease). AmSpec reported palm exports at 690,015 tons.

· Sunflower plantings are projected by APK-Inform to increase 4.9% in Ukraine and Russia sunflower plantings were estimated to increase 1.3% according to SovEcon. The oilseed crop may yield better crop returns over corn and wheat in 2018-19.

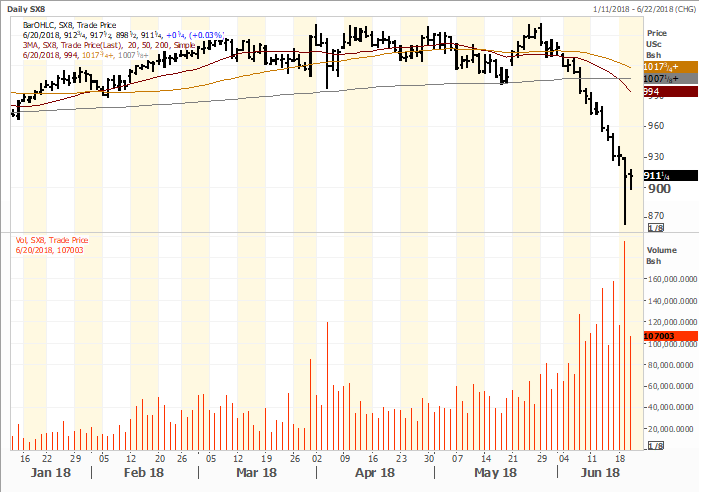

CBOT November soybean prices and volume

Source: Reuters and FI

Export Developments

· China sold 77,782 tons of 2013 crop-year soybeans from state reserves, 25.4% of what was offered at an average price of 2995 yuan per ton ($462.18/ton). Sales to date total 270,106 tons.

· China plans to auction off 60,000 tons of soybean oil on June 22 using a base price of 5,000 yuan/ton.

· China plans to offer to sell 500,000 tons of soybeans and 50,000 tons of soybean oil from state reserves on June 27.

· Iran seeks 30,000 tons of sunflower oil on July 10.

· Iran seeks 30,000 tons of palm olein oils on July 10.

· Iran seeks 30,000 tons of soybean oil on August 1.

· US wheat futures settled higher from technical buying after settling sharply lower on Tuesday.

· Funds in Chicago were buyers of an estimated net 5,000 SRW wheat futures, according to Reuters.

· UkrAgroConsult lowered its Russian wheat production to 70 million tons from 74 million, and left exports unchanged at 33 million tons (carry in stocks are high). SovEcon looks for Russia wheat exports to total 37 million tons, down from 40.9 million in 2017-18.

· Russia started selling some wheat out of inventories for export (2009-2013 crop years).

· Ukraine collected 610,000 tons of grain with an average yield of 3.17 tons per hectare. The Ukraine AgMin said grain exports so far this season total 38.6 million tons, down from 42.8 million tons a year ago. The AgMin maintained a 60 million ton crop.

· Some of the dry pockets across the US southwestern states will see rain and top soil moisture should improve.

Export Developments.

· China sold 1,486 tons of imported wheat out of reserves or less than 0.1% of what was offered.

· The EU awarded 21,582 tons of duty free wheat imports.

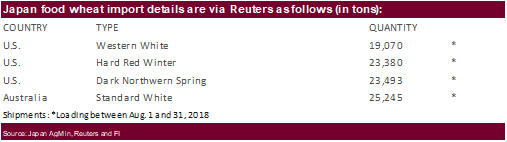

· Japan in a SBS import tender received no offers for 120,000 tons of feed wheat and 200,000 tons of barley for arrival by November 30.

· Japan in a SBS import tender seeks 120,000 tons of feed wheat and 200,000 tons of barley on June 27.

· Japan seeks 91,188 tons of milling wheat on June 21. Origins were open to Australia and US. No Canada.

· Taiwan seeks 95,350 tons of US wheat on June 26 for Aug/early Sep shipment, depending on origin.

· Jordan seeks 120,000 tons of barley on June 26.

· Jordan seeks 120,000 tons of wheat on June 27.

· Syria seeks 200,000 tons of wheat on July 2 for Aug 1-Sep 30 shipment. Origins include Russian, Romania and/or Bulgaria.

· Bangladesh seeks 50,000 tons of wheat on July 3.

Rice/Other

· Iran seeks 50,000 tons of rice from Thailand on July 3.

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International │190 S LaSalle St., Suite 410│Chicago, IL 60603

W: 312.604.1366

AIM: fi_treilly

ICE IM: treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.