From: Terry Reilly

Sent: Tuesday, January 28, 2020 5:11:38 PM (UTC-06:00) Central Time (US & Canada)

Subject: FI Evening Grain Comments 01/28/20

PDF attached

Coronavirus fears continue to weigh on selected commodities. Malaysian palm oil market crashed on Tuesday.

MARKET WEATHER MENTALITY FOR CORN AND SOYBEANS:

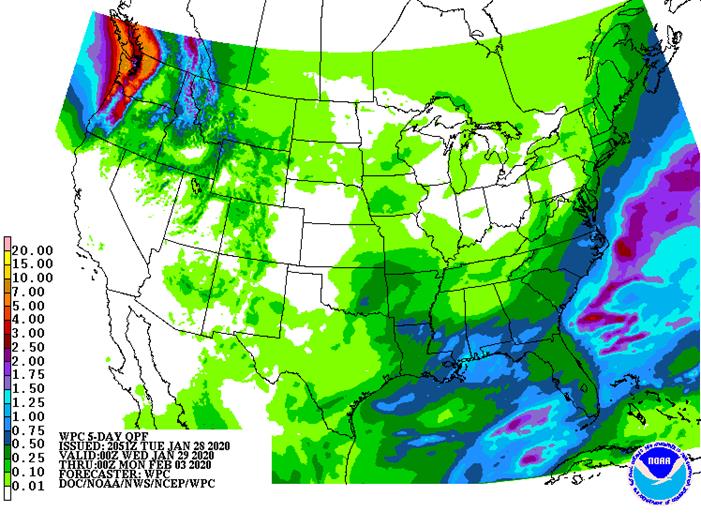

There is still not much reason for concern over Brazil summer crop conditions, but Argentina is still a little worry. Argentina is not likely to see failing rainfall over a large enough area to move markets in a big manner especially not with Brazil’s weather so good.

Weather in eastern Australia improved briefly during the weekend, but this week will trend drier again. South Africa will dry down for a while raising some potential for mild crop stress.

Southeast Asia rainfall will be well mixed and mostly supportive of palm oil development. Rain in China and India will be typical of this time of year with winter crops poised for improvement as spring approaches because of recent past precipitation.

Southeastern Europe remains too dry, but there is potential for some rain and mountain snow this week from there into Kazakhstan possibly easing long term dryness in Romania, the lower Danube River Basin and parts of Ukraine. The moisture boost will be important for spring planting and early season winter rapeseed development.

Overall, weather today will produce a neutral to slightly bearish bias to market mentality.

MARKET WEATHER MENTALITY FOR WHEAT:

There is still no risk of winterkill around the world for the next couple of weeks. That will leave winter crop conditions mostly unchanged. China crops will improve in the spring because of recent precipitation. India’s crops are still expected to yield extremely well.

There is still some concern over Morocco weather and the lack of rain in the southwest may harm production. A few other areas in northern Africa will also need some timely rain in February to protect production potentials.

Middle East wheat conditions are rated favorably, but would benefit from some greater rain. Southeastern Europe, Ukraine, southern Russia and Kazakhstan may get some needed precipitation in the next two weeks to improve soil moisture for spring crop development. Warm weather will continue to minimize the risk of winterkill and some areas may become snow free.

U.S. crops are not likely to experience much change in the next two weeks and the same is true for southeastern Canada.

Overall, weather today will have a neutral bias on market mentality.

Source: World Weather Inc. and FI

- AmSpec, Intertek, SGS: Malaysia’s Jan. 1-25 Palm Oil Exports, Kuala Lumpur

- HOLIDAY: China, Hong Kong

WEDNESDAY, JAN. 29:

- EIA U.S. weekly ethanol inventories, production, 10:30am

- HOLIDAY: China

THURSDAY, JAN. 30:

- USDA weekly crop net-export sales for corn, soybeans, wheat, 8:30am

- GUS Polish pig population data, Warsaw

- HOLIDAY: China

FRIDAY, JAN. 31:

- ICE Futures Europe weekly commitments of traders report on coffee, cocoa, sugar positions ~1:30pm (~6:30pm London)

- CFTC commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm

- U.S. agricultural prices paid and received, cattle inventory

- Paris Grain Day conference. Topics include outlook for Black Sea/Europe grains and challenges facing the oilseed market

- AmSpec, Intertek, SGS: Malaysia’s Jan. 1-31 Palm Oil Exports, Kuala Lumpur

Source: Bloomberg and FI

Macros.

US Durable Goods (DecP): 2.4% (est 0.4%, prevR -3.1%)

Durable Ex Transportation (DecP): -0.1% (est 0.3%, prevR -0.4%)

Corn.

· Corn futures were higher on spreading, in our opinion, and talk of the possibility US courts may overturn some of the EPA small refinery biofuel waivers. Traders bearish soybeans were hedging by spreading against corn.

· Also lending support to corn is the steady demand despite the coronavirus spread and inferred weaker demand. We are not seeing it fade in the US as Brazil is running low on supplies and Argentina’s higher prices. The US will enjoy a 2 to 3-month window steady exports. The active 24-hour window has seen reported corn sales for a sixth day in a row.

· If the biofuel waivers are taken back, then the companies will still need to comply with RFS mandates.

· 2800 CH0 traded 384.75 between 385.5 @ 10:14am CT.

· Technically, CH0 pushed through its 50-day moving average and spurred additional buying but was unable to break the 20-day moving average.

· The Baltic Dry Index fell 7 points or 1.3 percent to 539, a 4-year low.

· President Trump is expected to sign the USMCA on Wednesday.

· Funds were an estimated net buyer of 21,000 corn contracts.

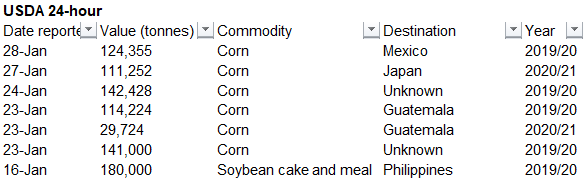

- Under the 24-hour reporting system, private exporters sold 124,355 tons of corn for delivery to Mexico during the 2019-20 marketing year.

· CBOT soybeans and oil traded lower after Malaysian palm oil fell 10 percent overnight. Cases of the coronavirus are booming, and more than 100 deaths are recorded. While the virus is in its infancy, its tracking much attention. The 10 percent drop in palm oil overnight is incomprehensible. We were thinking this might be a buying opportunity, at least for soybean oil.

· Oil World this morning made a good comment. They noted in 2003, during the severe SARS epidemic, vegetable oil consumption in China continued to grow by 8-9%. China domestic soybean meal consumption declined to 19.547 million tons in 2003-04 from 20.157 million in 2002-03. In 2018-19 domestic meal consumption was 66.405 million tons, down from 70.105 million in 2017-18.

· March SBO tested a 31.30 cent support level by trading through it but held the 200-day moving average and bounced to finish marginally lower, but well above the overnight lows.

· Brazilian real was slightly stronger at 4.2053. USD was up 16.

· Funds were an estimated net seller of 3,000 net soybean, 2,000 net soybean meal, and a net 1,000 bean oil contracts.