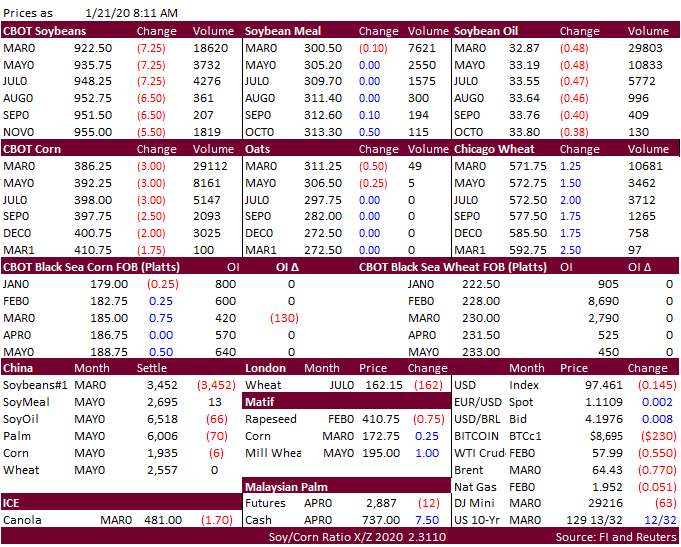

FW: FI Evening Grain Comments 01/21/20 Jan 21, 2020 From: Terry Reilly Sent: Tuesday, January 21, 2020 8:12:50 AM (UTC-06:00) Central Time (US & Canada) Subject: FI Evening Grain Comments 01/21/20 PDF attached Morning. There were no 24-hour announcements this morning. Soybeans and corn are lower in a risk off session. Chicago wheat getting a little help from higher Paris wheat futures. Real is weaker and USD is lower. Weather