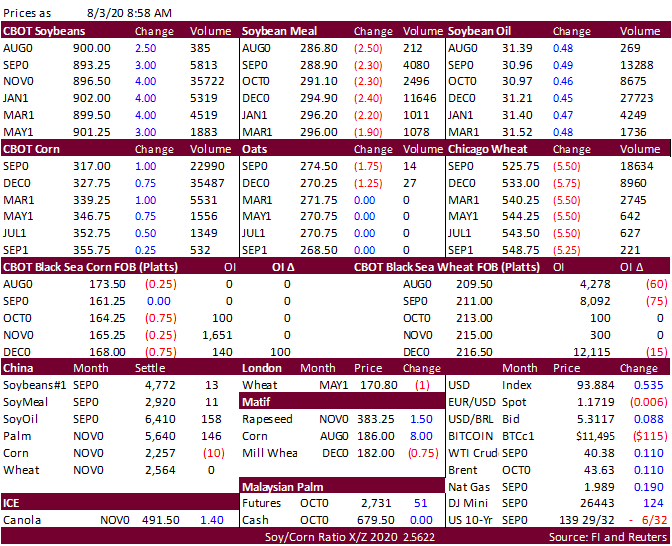

FI Morning Grain Comments 08/03/20 Aug 3, 2020 PDF attached USDA reported 260,000 tons of soybeans to unknown.