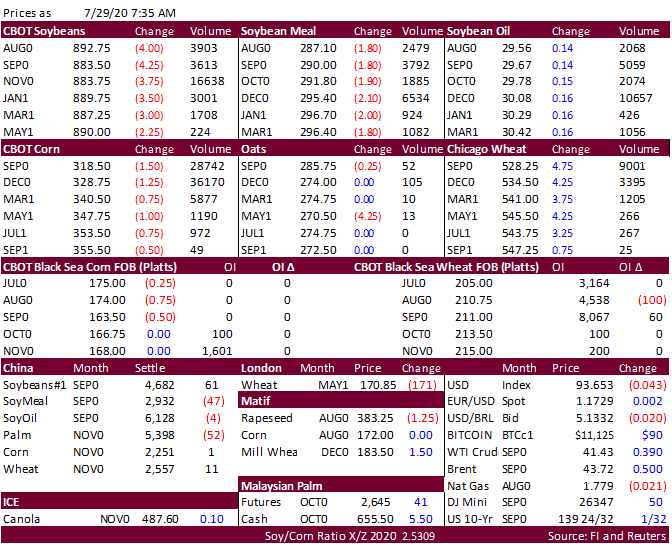

FI Morning Grain Comments 07/29/20 Jul 29, 2020 PDF attached As we approach the end of the month, US weather continues to remain the driver of the weakness in US agriculture commodities. But today we are seeing technical buying in corn and wheat. Some Chicago wheat contracts failed to close below key moving averages yesterday. Corn looks like a dead cat bounce. Soybeans were slightly lower led by weakness in soybeans meal. Soybean oil was higher in part to a upside reversal in Malaysian palm oil.