PDF attached

USDA

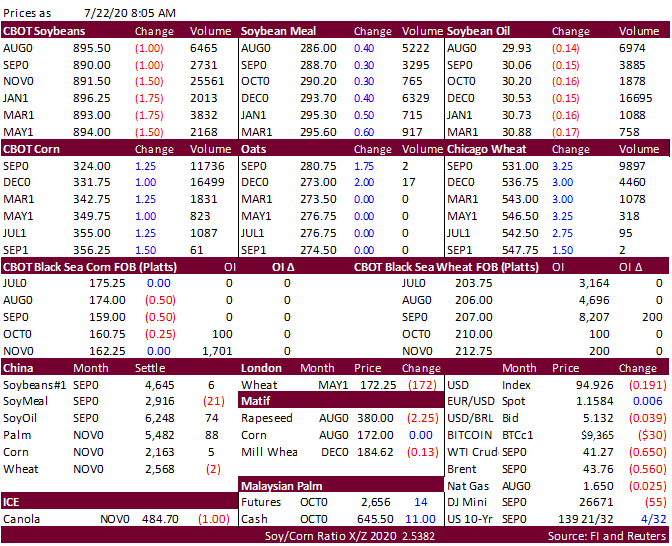

announced 7-8 soybean cargoes were sold to China and 3-4 cargoes to unknown. Lower trade for soybeans while corn and wheat are higher. China/US trade tensions are back in focus as the US ordered China to close its Houston consulate. Pakistan bought 300k

wheat, Taiwan bought 98,230 tons of US wheat, Japan passed on feed wheat, and South Korea’s KFA passed on corn. Jordan is back in for wheat. GFS model still shows good rains over the next week for the majority of the central and upper Midwest. Offshore

values are leading soybean meal and oil higher. CBOT soybean oil registrations fell 170 to 2,786 lots. USD was 26 lower this morning while WTI was down about $0.67. South American corn basis is firm. A Bloomberg poll looks for weekly US ethanol production

to be up 18,000 at 949,000 barrels (938-960 range) from the previous week and stocks to increase 244,000 barrels to 20.885 million. Russia’s Agriculture Ministry raised the estimate of wheat plantings by 1.2% to 29.1 million hectares.