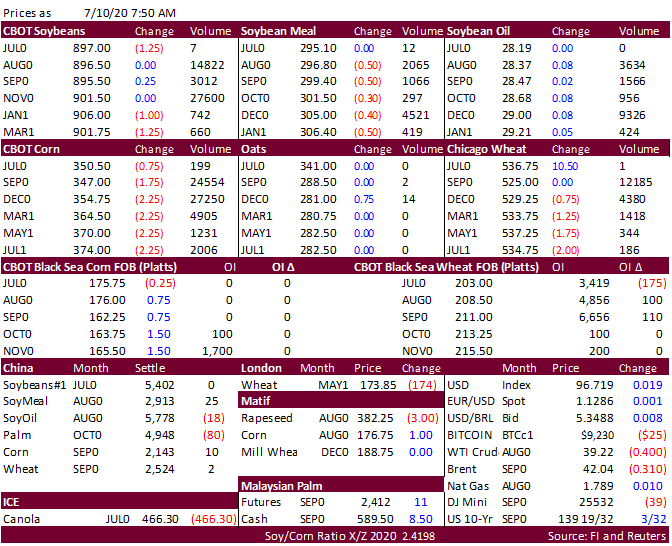

FI Morning Grain Comments 07/10/20 Jul 10, 2020 PDF attached Morning. Higher trade on follow through weather rally, an upward revision to China demand, and positioning ahead of the July USDA S&D report. US weather for this weekend appears to be not as hot as previous. Second week remains hot. China futures ended mixed. In its monthly S&D update, China increased 2019-20 corn and soybean imports by 2 and 3 million tons respectively. China cash crush are slightly higher. Palm was up 9MYR. Malaysian palm oil production during June was reported at an unusually high 1.886 million tons, 102,000 above trade expectations, a marketing year high, while end of June palm oil stocks were reported 34,500 tons below expectations at 1.9 million tons. This bullish undertone was partially offset by a decline in July exports. Cargo surveyors ITS and AmSpec reported a 17.8 percent and 16.8 percent decrease in June 1-10 palm oil shipments from month earlier. Corn is higher while US wheat mixed. US soybean conditions are expected to decline 1-2 on Monday and corn 2-4. Spring wheat could be down 1 and winter wheat will not be reported. French wheat futures are higher after France reported a one-point decline in crop conditions. Argentina is on holiday. FI snapshot for the USDA report is attached.