PDF attached includes Broiler Report charts, Cattle on Feed estimates and USDA export sales charts

Morning.

US

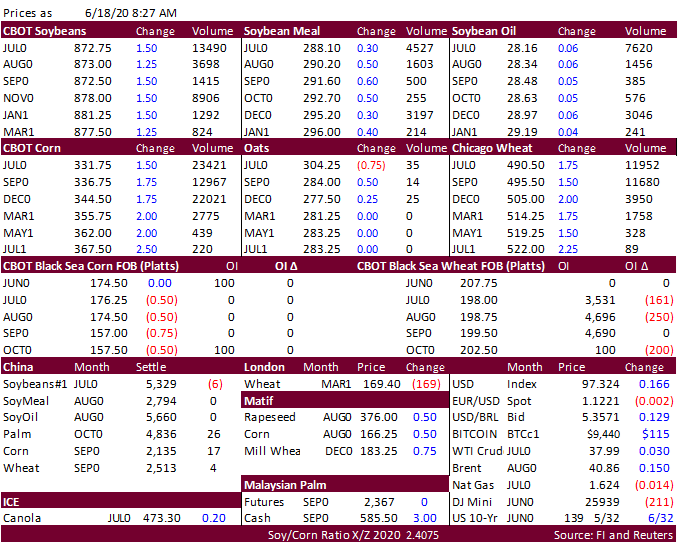

weather is the primary focus for the CBOT agriculture markets. Rumors China bought a small amount of US agriculture goods was in play yesterday, but we can’t confirm sales. USDA export sales were ok for soybeans, low for corn, SBM & SBO, and good for wheat.

![]()