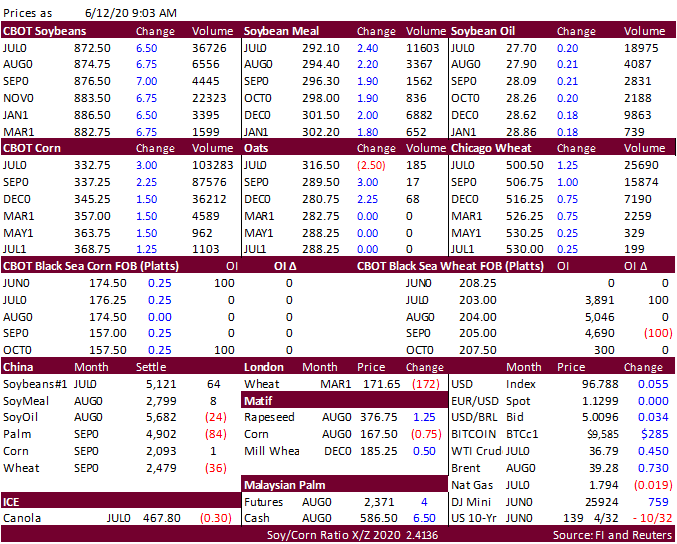

FI Morning Grain Comments 06/12/20 Jun 12, 2020 PDF attached Morning. We made a mistake in our PM comment leaving out AM prices in at the top of the comment. Sorry for the confusion. Drier weather forecast for the US growing areas will be in focus over the next week. News is light this morning.