PDF Attached

Morning.

USDA

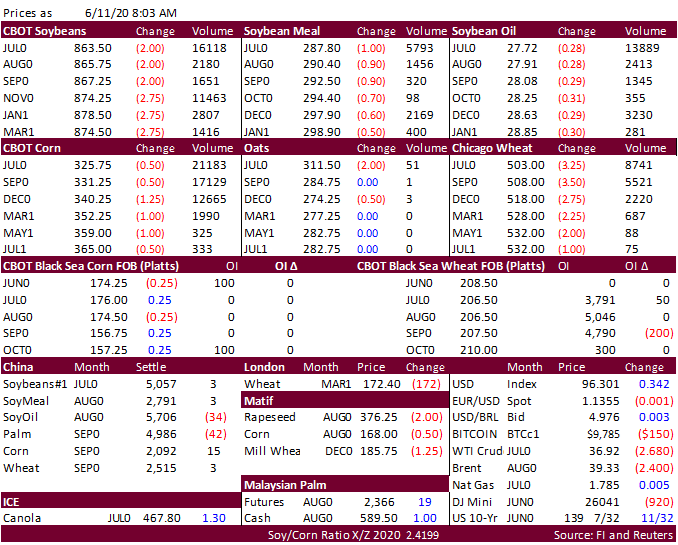

reported 720,000 tons of soybeans were sold to China. USDA

due out later. China S&D’s unchanged for 2020-21. USD is higher and WTI crude sharply lower. US Dow futures are down nearly 900 points. The US Fed estimates a three-year recovery in GDP.

![]()