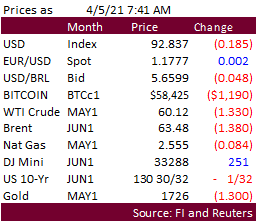

PDF attached

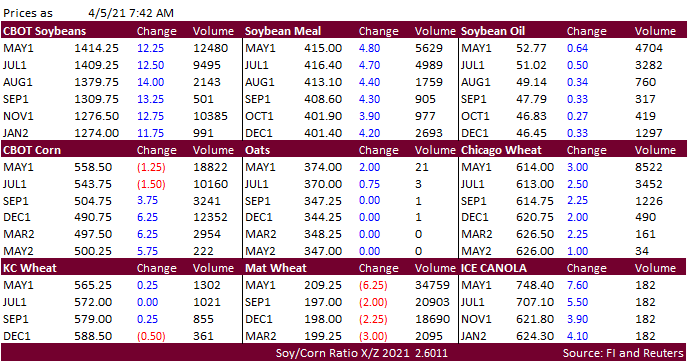

The soybean complex is higher on technical buying despite good US weather and bearish USDA NASS crush reported for the month of February. Energies were lower overnight led by heating oil. Corn is mixed from bear spreading. Wheat opened lower Sunday night, but most contracts rebounded on rising concerns over net drying across parts of the Great Plains. KC sold off before the electronic close. Several countries are on holiday today (Latin America, EU). China traded Friday with beans and meal lower and vegetable oils higher. Palm after a two day period settled down on 2 MYR (Fri & Mon combined). Brazil dries down this week while Argentina will see rain. US weather looks good. Rain returns to the Delta, SE and parts of the Midwest but no significant delays to fieldwork activity is expected. CME raised soybean futures maintenance margins by 11.7% to $3,350 per contract from $3,000 for May 2021, effective April 5. Initial margins are 110% of that level. US unemployment report released on Friday was friendly for US stock futures, according to business wires.

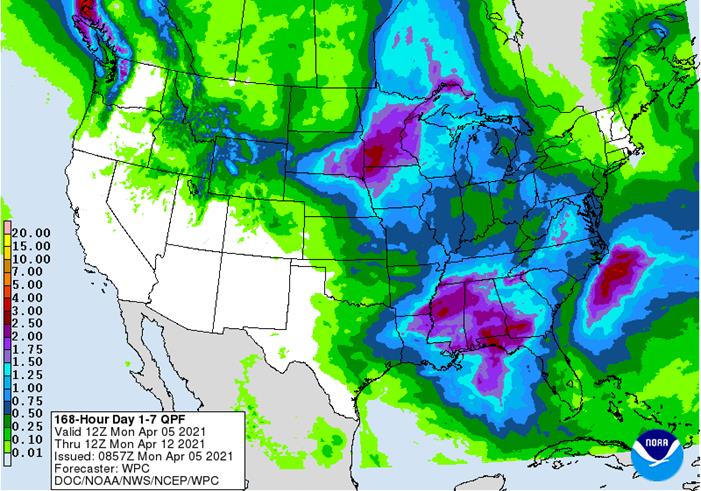

World Weather Inc.

UNITED STATES

- Western hard red winter wheat areas and crop areas south into West Texas will remain dry next ten days

- Central Washington into Oregon unirrigated winter crop areas will continue dry next ten days

- South and West Texas cotton, corn and sorghum areas will continue dry next ten days to two weeks

- Upper U.S. Midwest will receive plenty of moisture this week

- Areas from South Dakota and northern and eastern Nebraska to Michigan will receive enough rain to moisten the ground favorably

- Second storm system in the northern Plains and upper Midwest next week may be a little overdone, but there is potential for more precipitation in the region

- World Weather, Inc. believes this event may come a little later than advertised

- A good distribution of precipitation is advertised for the lower Midwest, Delta and southeastern states in the sense of producing a good mix of rain and sunshine during the next two weeks supporting fieldwork and crop development

- Northwestern U.S. Plains will continue to stay dry biased along with neighboring areas of Canada’s Prairies, despite a few showers

ARGENTINA

- Rain Wednesday through Saturday will be sufficient in restoring favorable topsoil moisture after recent drying

- Subsoil moisture is still fine

- Long term crop outlook is still very good

- Drying is expected late this weekend through much of next week

BRAZIL

- Interior southern parts of Brazil will be drying down additional in the coming week

- Mato Grosso do Sul, Parana, Sao Paulo and parts of Minas Gerais will be drying out along with Tocantins and Bahia

- Drying in some of these areas will raise greater concern over declining topsoil moisture

- Drying in Bahia is great for cotton and other crop maturation and harvesting

- Poor rainfall in Safrinha corn areas of interior southern Brazil will be a concern especially in areas that planted in wet fields where root systems may be short

- Well timed rainfall is expected in Mato Grosso and Goias during the next ten days to two weeks supporting Safrinha crops

REST OF WORLD

- Tropical Cyclone Seroja will reach the central Western Australia Coast south of Shark Bay and north of Geraldton this weekend and early next week bringing a disruption to port activity and then bringing needed moisture in Western Australia’s wheat, barley and canola country after the storm moves inland

- Western Europe is drying down, but warmer weather during the weekend was good

- Russia still has snow on the ground in much of the west and north, but greening is beginning in Ukraine and Russia’s Southern region

Source: World Weather inc.

Bloomberg Ag Calendar

Friday, April 2:

- CFTC commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm

- HOLIDAY: Good Friday holiday across most of Europe, Africa, Americas and parts of Asia

Monday, April 5:

- USDA export inspections – corn, soybeans, wheat, 11am

- EU weekly grain, oilseed import and export data

- ICE Futures Europe’s weekly commitments of traders report for week ended March 30, publication at noon London time (delayed from April 2 because of Good Friday holiday)

- Malaysian Palm Oil Council’s Pointers seminar (April 5-11)

- U.S. cotton plantings, winter wheat condition

- HOLIDAY: Easter Monday holiday in several countries

Tuesday, April 6:

- Purdue Agriculture Sentiment

- New Zealand global dairy trade auction

- HOLIDAY: Hong Kong, Thailand

Wednesday, April 7:

- EIA weekly U.S. ethanol inventories, production

- ANZ Commodity Price

Thursday, April 8:

- FAO World Food Price Index

- USDA weekly crop net-export sales for corn, soybeans, wheat, cotton, pork, beef, 8:30am

- China’s CNGOIC to publish soybean and corn reports

- Conab’s data on yield, area and output of corn and soybeans in Brazil

- Port of Rouen data on French grain exports

Friday, April 9:

- USDA’s monthly World Agricultural Supply and Demand (WASDE) report, noon

- ICE Futures Europe weekly commitments of traders report (6:30pm London)

- CFTC commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm

- FranceAgriMer weekly update on crop conditions

Source: Bloomberg and FI

Traders again missed the traditional fund net long estimate for corn but considering there was an increase in volatility ahead of the USDA reports, a miss of 44,600 contracts could be viewed as having little influence on prices. Funds for soybeans were also much more long than expected, by 31,000 contracts, and funds were more long for soybean oil by 30,400 contracts. Managed money positions declined for soybeans, SBO and wheat and increased for corn. Meal net long for managed money was up 600 contracts.

SUPPLEMENTAL Non-Comm Indexes Comm

Net Chg Net Chg Net Chg

Corn 362,124 6,642 418,986 978 -746,116 3,180

Soybeans 98,701 -27,685 164,864 -1,735 -249,398 35,489

Soyoil 48,822 -12,388 121,138 -930 -184,837 20,412

CBOT wheat -39,927 -19,154 157,379 -1,213 -105,191 21,511

KCBT wheat 1,654 -3,640 64,274 -2,277 -63,538 6,803

=================================================================================

FUTURES + OPTS Managed Swaps Producer

Net Chg Net Chg Net Chg

Corn 395,584 7,410 248,782 5,827 -726,557 -3,751

Soybeans 141,880 -20,972 91,598 -49 -236,854 35,948

Soymeal 58,235 616 70,587 -965 -177,974 1,022

Soyoil 80,840 -13,136 97,741 4,619 -205,327 14,887

CBOT wheat -14,711 -22,871 98,508 4,978 -92,009 17,386

KCBT wheat 21,722 -4,520 42,110 -1,271 -55,059 8,211

MGEX wheat 10,384 -4,840 5,280 343 -17,367 8,402

———- ———- ———- ———- ———- ———-

Total wheat 17,395 -32,231 145,898 4,050 -164,435 33,999

Live cattle 83,237 3,680 84,646 211 -174,626 -6,683

Feeder cattle 5,111 4,404 7,570 116 -3,800 -1,112

Lean hogs 78,112 2,017 58,455 -3 -146,436 -4,829

Other NonReport Open

Net Chg Net Chg Interest Chg

Corn 117,185 1,314 -34,994 -10,800 2,320,111 -20,948

Soybeans 17,542 -8,858 -14,166 -6,068 1,175,658 -1,115

Soymeal 20,640 2,403 28,511 -3,076 470,594 -1,873

Soyoil 11,868 725 14,876 -7,096 589,479 -25,815

CBOT wheat 20,474 1,652 -12,261 -1,146 511,903 -3,797

KCBT wheat -6,383 -1,535 -2,390 -886 242,246 3,403

MGEX wheat -327 -1,669 2,031 -2,236 85,271 -4,218

———- ———- ———- ———- ———- ———-

Total wheat 13,764 -1,552 -12,620 -4,268 839,420 -4,612

Live cattle 20,122 2,722 -13,378 69 392,487 3,620

Feeder cattle 4,351 -512 -13,233 -2,895 53,357 -1,480

Lean hogs 16,653 1,561 -6,785 1,253 355,881 14,569

Source: Reuters and FI

Macro

US Non-Farm Payrolls (Mar): 916K (est 639K, prevR 468K)

Unemployment Rate: 6% (est 6%, prev 6.2%)

Manufacturing Payrolls: 53K (est 33K, prevR 18K)

Average Earnings (Y/Y): 4.2% (est 4.5%, prevR 5.2%)

Average Earnings (M/M): -0.1% (est 0.2%, prevR 0.3%)

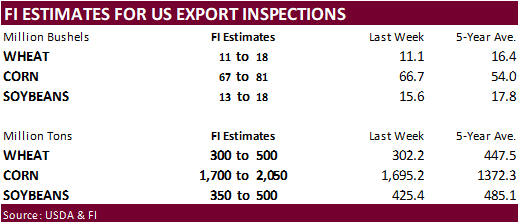

- CBOT corn traded two-sided overnight, near an 8-year high, but bear spreading dragged the front months lower. US weather looks good for fieldwork activity this week, but some rain events will occur. With many countries on holiday, look for a quiet trade. We see corn inspections in a 1.7-2.05 million ton range.

- Ukrainian corn exports fell by 25% in the first half of the 2020-21 October-September season to 15.9 million tons (APK-Inform). Ukraine exported 6 million tons of corn to China, 5.0 million tons to the European Union, 1.7 million tons to Egypt and 3.2 million tons to other destinations.

- The ASF problem in China has not slowed feed demand. China last week decided to release and auction off 2 million tons of rice from state reserves to feed producers. On Wednesday they sold between 1.4 million and 1.5 million tons of rice at about 1,500 yuan ($228.62) a ton, 70% of what was offered, bringing combined 2021 sales to about 5 million tons. This is on top of about 25 million tons of wheat sold.

- Funds on Thursday sold an estimated net 4,000 corn contracts.

- Late last week StoneX estimated Brazil second corn crop at 77.65 million tons, down from 81.3 million tons previous. DataGro sees the Brazil corn crop at 109.30 million tons, down from 109.62 million tons previous.

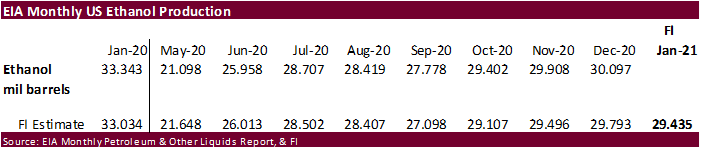

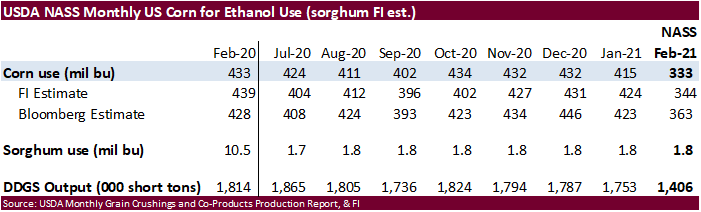

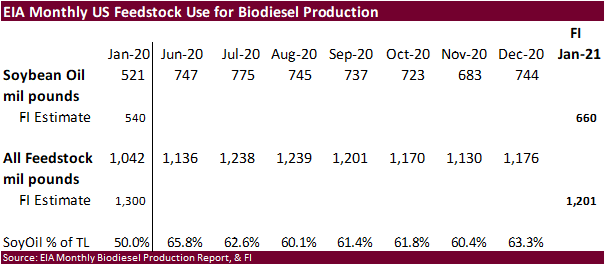

- US February corn use for ethanol came in below trade expectations during the month of February and with ethanol production rebounding at a slower rate during the start of the spring months, this could prompt USDA to lower its corn for ethanol use by 25 million bushels from 4.950 billion to 4.925 billion.

Export developments.

- None reported

- The soybean complex is higher on technical buying despite good US weather and bearish USDA NASS crush reported for the month of February. Energies were lower overnight led by heating oil. Many countries are on holiday so there is little lead from outside markets. Palm was down slightly when combining Friday and Monday prices.

- CBOT soybeans volatility last week prompted CME to raise margins for soybean futures maintenance margins by 11.7% to $3,350 per contract from $3,000 effective April 5.

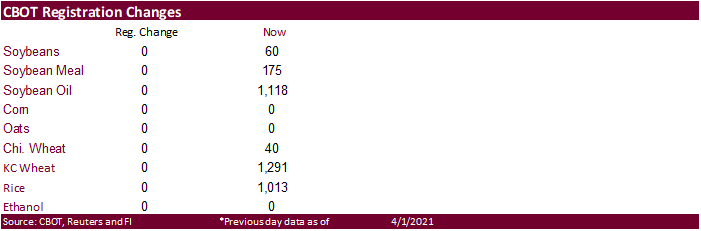

- There were no changes to CBOT registrations.

- Ukrainian sunflower oil prices decreased by $35 ton over the past week, according to APK-Inform to a range of $1,485 – $1,495 per ton FOB Black Sea from $1,520 – $1,530 a week earlier. Record high was $1,710 and $1,725 per ton FOB in early March.

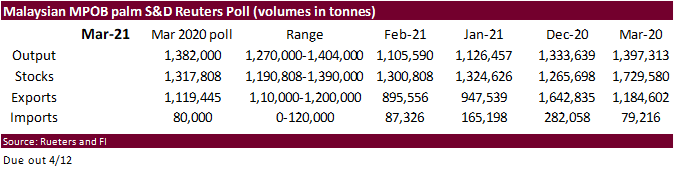

- A Reuters poll for Malaysia’s palm oil inventories shows March stocks expected to rise 1.3% from February to 1.32 million tons, production to slightly decline, and exports to be up 25% to 1.12 million tons. The Malaysian Palm Oil Board will release the official data on April 12.

- The Malaysian Palm Oil Council (MPOC) looks for crude palm oil price to average 3,846 ringgit a ton during the first half of the year, peaking at 4,190 ringgit a ton.

- Funds on Thursday sold an estimated net 8,000 soybean contracts, sold 8,000 soybean meal and sold an estimated 2,000 soybean oil.

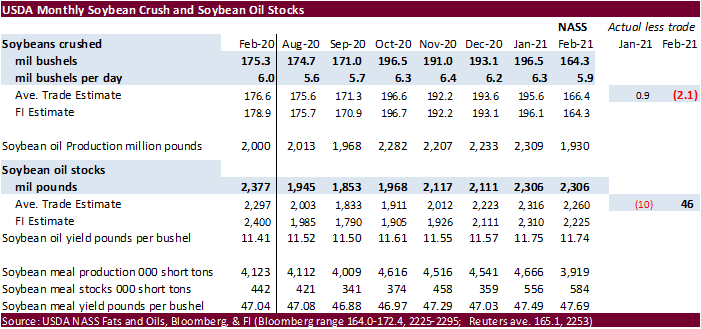

- US February US NASS crush came in 2.1 million bushels less than expectations and soybean oil stocks 46 million pounds below a Bloomberg trade guess. Soybean meal stocks were 584,000 short tons, up from 556,000 at the end of January and above 442,000 short tons year ago. Implied product demand was less than expected during February.

- Late last week StoneX pegged the Brazil soybean crop at 134 million tons, up from 133.47 million tons previously. DataGro sees the Brazil soybean crop at 135.47 million tons, down from 135.68 million tons previous.

- China cash crush margins on our analysis were 144 vs. 144 cents late last week and compares to 214 cents year earlier.

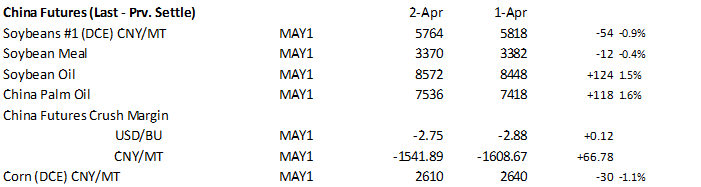

China futures:

Malaysian palm oil: (uses settle price)

Friday Changes

Friday & Monday Combined

Export Developments

- The USDA seeks 540 tons refined veg oil, under the McGovern-Dole Food for Education export program (470 tons in 4-liter cans and 70 tons in 4-liter plastic bottles/cans) on April 6 for May 1-31 (May 16 – Jun 15 for plants at ports) shipment.

- Chicago wheat turned higher (MN higher/KC lower) on rising concerns over net drying across parts of the US Great Plains and Canadian Prairies. Egypt is in this week for wheat for August 1-10 shipment. Europe is on holiday so no trading in Paris wheat. Saudi Arabia bought 295,000 tons of hard milling wheat at around $269-270/ton.

- Russian 12.5% protein wheat export prices fell $12 last week to $245 a ton FOB – IKAR. SovEcon showed wheat and barley prices fell by $5 to $248 a ton and $235 a ton, respectively.

- APK-Inform reported Ukrainian wheat export prices fell $9 a ton in the past week. High-quality soft milling wheat decreased to $245-$251 from $254-$260 a ton FOB Black Sea

- Egypt plans to buy 4 million tons of local wheat in 2021 between April 15 and July 15-Supply Minister. Both wheat and sugar reserves are currently at 3.6 months. Vegetable oil supplies are at 3.7 months and rice until October.

- Last week China offered 2 million tons of rice from state reserves and sold between 1.4 million and 1.5 million tons of rice at 1,500 yuan ($228.62) a ton, 70% of the total volume. China has also sold close to 5 million tons of rice from reserves this year. Note sales of wheat from auction reached 25 million tons.

- Funds on Thursday sold an estimated net 7,000 CBOT SRW wheat contracts.

- SovEcon lowered its forecast for Russia’s 2020-21 wheat exports by 0.2 million tons to 38.9 million tons.

- Ukraine grain exports so far this season are running 23 percent below year earlier. They sold 14.4 million tons of wheat, 16.6 million tons of corn and 4.1 million tons of barley.

- French soft wheat crop conditions were unchanged for the week ending March 29 at 87 percent from the previous week and compares to 62 percent from year ago. Winter barley conditions declined 1 point to 84 percent from the previous week. Durum dropped 1 point to 91 percent.

- Egypt seeks wheat for August 1-10 shipment on Tuesday, April 6, with offers valid for 24 hours.

- Jordan seeks 120,000 tons of animal feed barley on April 6.

- Ethiopia seeks 400,000 tons of optional origin milling wheat, on April 20, valid for 30 days. In January Ethiopia cancelled 600,000 tons of wheat from a November import tender because of contractual disagreements.

Rice/Other

· Iraq seeks 30,000 tons of rice on April 5, valid until April 8.

· Mauritius seeks 4,000 tons of optional origin long grain white rice on April 16 for delivery between June 1 and July 31.

· Syria seeks 39,400 tons of white rice on April 19. Origin and type might be White Chinese rice or Egyptian short grain rice.

· Ethiopia seeks 170,000 tons of parboiled rice on April 20.

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International

One Lincoln Center

18 W 140 Butterfield Rd.

Oakbrook Terrace, Il. 60181

W: 312.604.1366

ICE IM: treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.