PDF attached

Morning

CBOT soybeans are finding bull spreading on higher meal while soybean oil is lower following a plunge in Malaysian palm oil. CBOT corn and wheat are seeing a follow through lower trade. China has been quiet this for US soybeans and corn. US wheat was not included in Egypt’s purchase of 480,000 tons of wheat yesterday as they sourced it from four other countries.

MARKET WEATHER MENTALITY FOR CORN AND SOYBEANS:

Not much has changed overnight. Brazil weather will remain well mixed supporting full season crops and late season soybeans. Enough dry weather will support soybean harvesting and Safrinha crop planting. Excessive rain noted in Paraguay and a few other areas recently induced some flash flooding, but most crops likely “weathered” the situation relatively well. There have been local areas of crop quality declines because of recent wet weather in Brazil, but the nation’s crop is mostly rated favorably.

Central Argentina soil moisture was bolstered in a major way late last week and during the weekend. Crop development in Cordoba, northern Buenos Aires, central and southern Santa Fe and parts of Entre Rios will advance favorably during the next two weeks, despite net drying for a while. Crop areas in the far south may struggle for moisture at times, but the remainder of the nation will either receive timely rain or crops will feed off of favorable subsoil moisture. Some rain in southern Buenos Aires and La Pampa Sunday into Monday will offer some short-term relief from dryness.

South Africa summer crop conditions remain very good with little change likely. Australia’s dryland sorghum and other crops would benefit from more routine rainfall, especially in Queensland, but that is not likely for a while.

India winter crops are beginning to reproduce and timely rain is needed to support the best possible yields. Crop conditions are rated favorably. Rain this week is not likely to seriously bolster soil moisture, but every drop of moisture will be good for reproduction. More rain is desired, though.

China and Europe crops are dormant and will remain in favorable condition for the next few weeks. Western Europe has become a little too wet.

Overall, weather today will likely provide a neutral to slightly bearish bias to market mentality.

MARKET WEATHER MENTALITY FOR WHEAT: Concern remains over snow free areas in southwestern Canada’s Prairies and the northwestern and west-central U.S. Plains as colder air settles into those areas for a while late this week and through the weekend. Snow should precede the bitter cold to adequately protect dormant winter crops from winterkill. A close monitoring of the region will be warranted when the coldest conditions arrive to make sure snow cover is adequate to protect all crops.

Snow cover in northern Russia and northeastern Europe is sufficient to support crop needs during the colder periods that may evolve later this week and deeper into February. Snow free areas in southern Europe, Ukraine and Russia’s Southern Region should not be threatened by damaging cold weather in the next week.

China, India and Europe winter crops are in mostly good condition. Rain is needed in India during reproduction in February and a close watch on rain potentials is warranted over the next few weeks. Showers later this week over the next few days in the far north and extreme east will be welcome, but greater volumes of rain will still be desired.

Morocco rain expected Thursday into the weekend will improve topsoil moisture for better wheat development potential in the spring. However, drought during the planting season may have permanently cut production in a small part of the nation. A boost in precipitation is still needed across all other areas in northern Africa, but no area is drier than southwestern Morocco.

Recent increases in Middle East rainfall has improved field condition so that some improvement in crop conditions may follow.

Overall, weather today will likely provide a mixed influence on market mentality.

Source: World Weather Inc. and FI

Wednesday, Feb 3:

- EIA weekly U.S. ethanol inventories, production, 10:30am

- New Zealand Commodity Price

Thursday, Feb 4:

- FAO World Food Price Index; cereals supply/demand brief

- USDA weekly crop net-export sales for corn, soybeans, wheat, cotton, pork, beef, 8:30am

- Port of Rouen data on French grain exports

Friday, Feb 5:

- US Trade Balance

- Statcan reports on wheat, soy, durum, canola and barley stockpiles in Canada

- ICE Futures Europe weekly commitments of traders report, 1:30pm (6:30pm London)

- CFTC commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm

- China’s CNGOIC to publish soybean and corn reports

US ADP Employment Change Jan: 174K (est 50K; prevR -78K; prev -123K)

- Corn futures are lower on fund liquidation. China has been quiet this for US soybeans and corn.

- Mexico’s AgMin sees 2020 corn imports dropping 9%, or about 1.5MMT, as they plan to scale back on genetically modified grains and increase local corn plantings. In the “Corn for Mexico program”, aims to replace 30% of Mexico’s current volume of imports with national production by 2024. Mexico imported 13 million tons of corn recently from the US. Mexico produced about 25 million tons of white corn and about 3 million tons of yellow corn.

- Reuters noted (commercial) stocks of corn held by Chinese feed makers and other end users reached multi-year highs in some areas, and indication of stockpiling amid concerns over future shortages. Local corn prices increased 50% higher during 2020. https://fingfx.thomsonreuters.com/gfx/ce/jbyvrnwkkve/ChinavsUSCornPricesFeb2021.png From October 1 through January 10, commercials purchased 62.79 million tons of corn from farmers, up from 50.77 million tons previous year, according to National Food and Strategic Reserves Administration, effectively pulling the amount of commercial corn stocks to a 15-year high. Dalian Commodity Exchange warehouses receipts hit 100,000 tons for the first time last month. Imports are driven by shortages, poor local quality, and supply fears amid rebound in the pig crop. https://fingfx.thomsonreuters.com/gfx/ce/xlbvgyeblvq/ChinacornImportsvsDCEstocks.png

- Bulgaria found a case of H5N8, first in seven months.

- German plans to cull 14,000 turkeys after H5N8 bird flu was discovered in the eastern German state of Brandenburg.

- Argentine had some disruptions to grain exports after protestors set up roadblocks at some Buenos Aires terminals, according to CIARA chamber of export companies. We heard there are some disruptions in the south, an area were vessels top off commodities before they set sail. A source mentioned wheat and barley was at least affected. Some think the strike will expand.

{kind=link}

{kind=link}

- China will sell 30,000 tons of frozen pork from state reserves on February 4, and another 30,000 tons on Feb. 9.

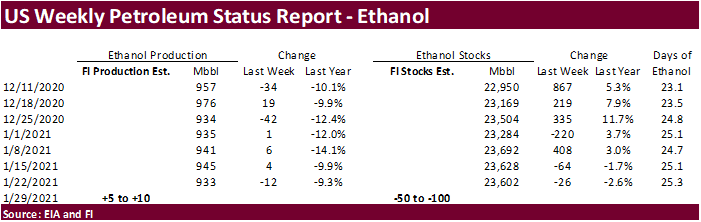

- A Bloomberg poll looks for weekly US ethanol production to be down 1,000 at 932,000 barrels (918-941 range) from the previous week and stocks up to 83,000 barrels to 23.685 million.

Corn Export Developments

· None reported