PDF Attached

We are bullish soybeans, corn, and wheat, in that order.

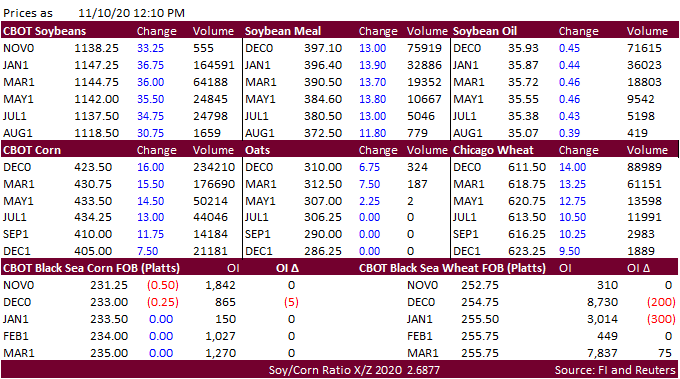

USDA released their November S&D report

Reaction: Bullish all around. Largest surprise was USDA lowered its US soybean carryout to 190 million bushels, without changing exports. Reduction in US soybean and corn production and China corn trade were some of the main features.

USDA NASS and OCE executive summaries

https://www.nass.usda.gov/Newsroom/Executive_Briefings/index.php

https://www.usda.gov/oce/commodity/wasde/Secretary_Briefing/index.htm

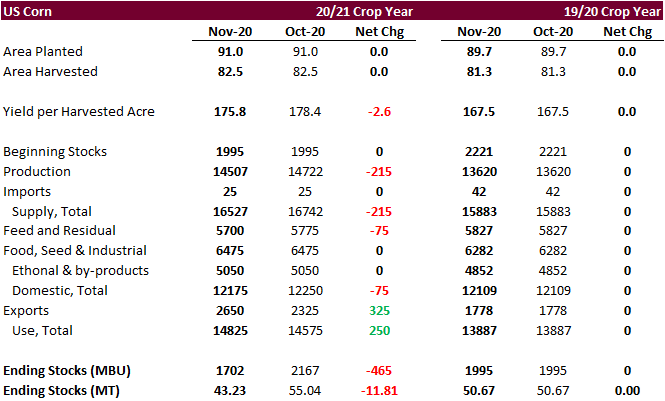

Corn.

- USDA took US corn production down 215 million bushels to 14.507 billion bushels in large part to a 2.6 bushel reduction in the yield to 175.8. The trade was looking for 177.7. USDA left their area unchanged.

- Production for US corn and soybeans came in below trade expectations, by 152 and 81 million bushels, respectively.

- USDA lowered the 2020-21 US corn carryout by 465 million bushels. USDA lowered feed use by 75 million bushels, partially offsetting the 215-million-bushel reduction in supply.

- But USDA decided to raise the US corn export forecast by 325 million bushels to 2.650 billion, above 1.778 billion from 2019-20.

- Global corn production was slashed 14.2 million tons to 1.145 million, 2.5 percent above last year. Stocks were taken down 9.0 million tons. US stocks were down 11.8 million tons.

- There were finally major changes to China’s corn balance sheet for 2020-21. Imports were lifted 6 million tons to 13 million tons, but well below the 22 million tons projected by USDA’s Attaché. Note USDA increased the US export projection by 8.2 million tons. The boost in the US export projection reflected not only China imports, but a massive reduction in Ukraine exports to 22.50 million tons from 30.5 million tons.

March corn is seen trading up into the $4.45-$4.55 area.

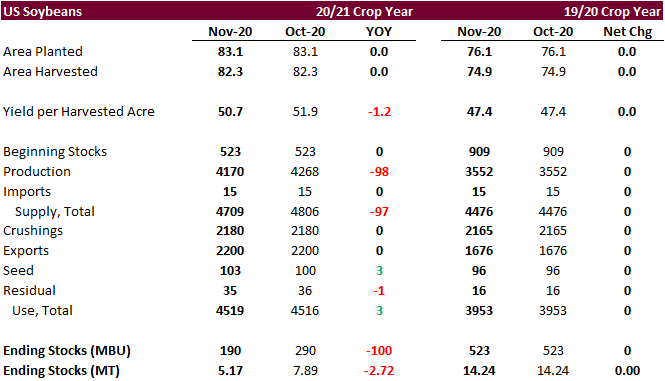

- Another large chop to the US soybean carryout again sent futures flying higher on USDA report day.

- USDA reported the USDA soybean yield down 0.9/bu from the previous month to 50.7 bushels per acre. The trade was looking for 51.6. USDA left the area unchanged.

- USDA lowered the US soybean carryout by 100 million bushels to 190 million bushels, 45 million below trade expectations. This was the largest surprise in today’s report. The reduction of 465 million bushels in the corn carryout may rival it. 2020-21 soybean stocks are now projected 64 percent below 2019-20.

- Remarkably, even after Census reported a higher than expected September soybean figurer, USDA left its export forecast unchanged at 2.20 billion bushels, still well above 1.676 billion for 2019-20.

- The US crush was also left unchanged. They took sed use up 3 million bushels.

- USDA adjusted their 2019-20 US carry out to reflect NASS crush and Census trade balance. The US 2020-21 soybean meal carrying was lowered 59,000 short tons. USDA took 2020-21 US soybean meal production up 9,000 short tons, resulting in a 50,000 short ton decline in supply. USDA left its 2020-21 US soybean meal demand unchanged, resulting in a 50,000 short ton reduction to the carryout to 350,000 short tons.

- Recall USDA reported end of September soybean oil stocks at 1.849 billion pounds. After adjusting for the latest trade balance, USDA decided to raised biodiesel by 50 million pounds for the 2019-20 marketing year to 7.900 billion. This compares to their unchanged outlook for soybean oil for biodiesel use of 8.100 billion pounds for 2019-20.

- US soybean oil stocks for 2020-21 declined 109 million pounds to 1.864 billion as USDA left production and demand unchanged for the current marketing year.

- Global soybean production was taken down 5.8 million tons to 362.6 million tons, 26 million higher than 2019-20, largely to changes in US output and 2.5 million ton decrease in Argentina output. Brazil was unchanged.

- China soybean imports were left unchanged at 100 million, above 98.5 million tons in 2019-20.

- 2020-21 global soybean stocks were taken down 2.2 million tons to 86.5 million, 9.3 percent below 2019-20. Global demand is expected to be very strong this crop year.

January soybeans are seen in a $11.10-$12.10 range

January soybean meal is seen trading above $4.20 range

January soybean oil is seen trading above 37.50.

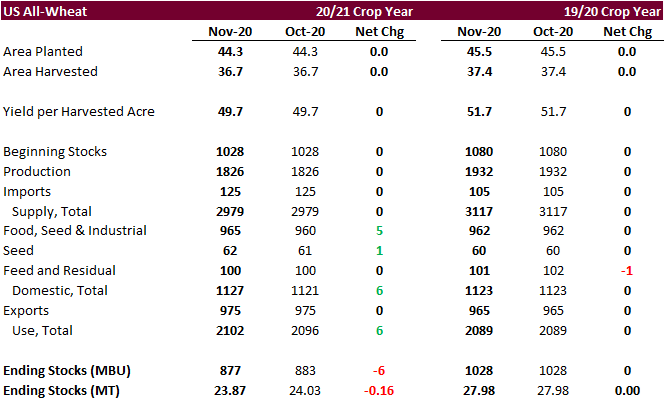

- US wheat futures followed corn and soybeans higher.

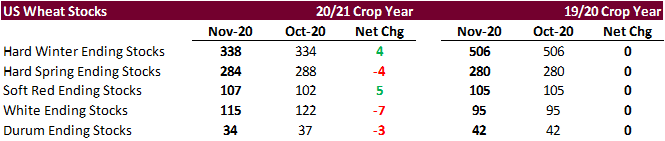

- USDA lowered the US all-wheat carryout by 6 million bushels, in part to adjusting wheat for food use higher by 5 million bushels and seed use by 1 million bushels.

- USDA raised HRW wheat stocks by 4 million tons to 338 million, well below 506 million at the end of 2019-20. Soft wheat stocks were taken up 5 million bushels to 107 million bushels. White stocks were downward revised 7 million and durum was lowered 3 million bushels.

- Global wheat production was taken down 0.7 million tons to 772.4 million tons.

- Argentina wheat production was taken down 1 million tons to 18 million tons, which still could be too high.

- China wheat imports were taken up 0.5 million tons to 8 million, nearly up 50 percent from 2019-20.

- Global wheat stocks of 320.5 million tons are down 1.0 million from last month and 6.5 percent higher from 2019-20.

March Chicago wheat is seen in a $6.05-$6.45 range

March KC wheat is seen in a $5.50-$5.90 range

March MN wheat is seen in a $5.60-$6.10 range

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International

One Lincoln Center

18 W 140 Butterfield Rd.

Oakbrook Terrace, Il. 60181

W: 312.604.1366

ICE IM: treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.