PDF attached includes snapshot of major changes for USDA’s S&D

USDA released their June supply and demand outlook

Reaction: Bullish corn, neutral wheat and bearish to neutral soybeans. Look for the trade to quickly shift focus on crop conditions, weather, and June Acreage report due out at the end of the month.

We raised our nearby corn price trading range and made slight adjustments to products and MN wheat. (see below)

Next major report is June Acreage, followed by the July S&D. USDA typically does not adjust supply for corn and soybeans in July, but if corn conditions continue to decline at a rapid pace, there is a chance USDA could cut the July yield from May/June. At this point we don’t think it will be revised. USDA’s first survey of spring wheat is July.

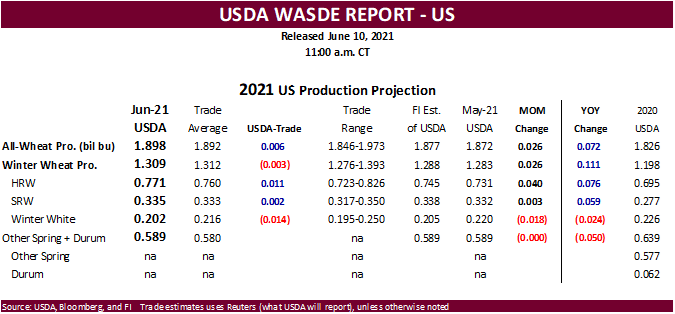

US old-crop corn carryout was cut 150 million bushels to 1.357 billion, a tight 7.4 percent STU, due to a more than expected increase in corn for ethanol use of 75 million and upward revision to the exports by 75 million (Brazil). We were surprised USDA lowered the Brazil corn crop by only 3.5 million tons to 98.5 million, 1.2 million above an average trade guess. Argentina corn was unchanged. Back to the US corn balance, USDA made no changes to new-crop categories other than reflecting the lower carry in. We thought the US soybean and wheat ending stock revisions were neutral. New crop all-wheat exports were lowered only 4 million bushels. Beginning stocks were lowered 20 million bushels to reflect higher old crop exports (crop year ended), which was offset by an upward revision to all-wheat production by 26 million to 1.898 billion bushels. USDA raised feed use for 2021-22 by 10 million to 180 million, 80 million higher than 2020-21. Wheat production by class below.

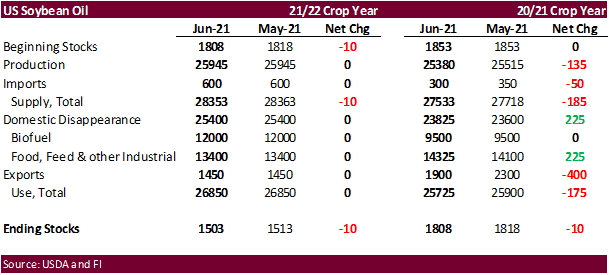

USDA raised Brazil’s soybean production by 1 million tons. Argentina was left unchanged. USDA left 2020-21 US exports unchanged but unexpectedly cut the crush by 15 million bushels to 2.175 billion. We think it will end up higher than that unless some plants are unable to source the soybeans during the summer or crush margins erode. For new-crop, USDA raised the crush by 15 million, which was needed given the strong demand for new-crop soybean oil for renewable diesel. Speaking of which, USDA made no changes to old and new crop biofuel demand, but increased food use for 2020-21 by 225 million pounds to 14.325 billion. We agree. Old crop SBO exports were lowered 400 million pounds. Note export sales shipments have been low recently. Imports were lowered 50 million. Production was lowered 135 million reflecting the lower crush. The result lowered the carryout by 10 million pounds. New crop soybean oil categories were unchanged other than to reflect a lower carry in. Soybean meal production for old crop was taken down 200,000 short ton. Imports were increased 50,000 short tons (Canada?) to 700,000 tons and domestic use taken down 150,000 tons. With a healthy May and June crush rate, we are surprised exports were not lifted higher given the amount of meal in the pipeline. New crop was unchanged. The increase in US soybean stocks by 15 million initially caught the trade off guard, but prices paired losses in new-crop from higher corn.

As we mentioned above, crop conditions and weather are back on the table. Look for volatility in these markets to last into FH July, unless NA weather significantly improves.

USDA OCE Secretary Briefing

https://www.usda.gov/sites/default/files/documents/june-2021-wasde-lockup-briefing.pdf

July corn seen in a $6.50 and $7.50 range (up 50, up 25)

December corn is seen in a $4.75-$7.00 range.

July soybeans are seen in a $15.00-$16.25 (up 25); November $12.75-$15.00

Soybean meal – July $360-$410 (unch, dn $10); December $380-$460

Soybean oil – July 68-74 (down 100 for both); December 57-70 cent range

July Chicago wheat is seen in a $6.30-$7.15 range

July KC wheat is seen in a $5.95-$6.70

July MN wheat is seen in a $7.50-$8.25 (unch, down 25)

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International

One Lincoln Center

18 W 140 Butterfield Rd.

Oakbrook Terrace, Il. 60181

W: 312.604.1366

ICE IM: treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.