PDF Attached

USDA released their May supply and demand outlook

Reaction: Neutral to bearish feedgrains, at least for new crop, and neutral to friendly for soybeans. Bottom line is if the US realizes larger soybean and corn plantings when NASS updates the area at the end of June, look for USDA to increase selected demand categories for those US balance sheets in July. Therefore, we expect new-crop corn and soybean prices to remain above $5 and $12, respectively, through the summer growing season, unless US crop conditions suggest yields well above trend. Old crop prices should continue to be underpinned on tight global stocks.

USDA OCE Secretary Briefing

https://www.usda.gov/sites/default/files/documents/may-2021-wasde-lockup-briefing.pdf

We remain bullish the soybean complex based on strong global crush demand and China import demand. One figure that stood out was new-crop China corn imports projected at 26 million tons, same as the current crop-year. Note the USDA Attaché put corn imports below the current year in anticipation of a larger 2021 China corn production.

USDA’s data dump didn’t really have any other eye-catching surprises, but there were a few notable items that caught the trade off guard. Old and new crop US wheat ending stocks came in 26 and 44 million bushels above expectations, respectively. Old crop US corn ending stocks were a little tighter than expected but new-crop was reported 163 million bushels above expectations at 1.507 billion, a level that would be “comfortable.” US soybean old and new-crop stocks were reported near expectations.

Looking new-crop (2021-22) global stocks, USDA looks for the world corn carryout to increase 3.1% from 2020-21, wheat to be near unchanged, and soybeans to increase 5.3% from the current crop-year. As expected, USDA reported very large new-crop South American corn and soybean production estimates. USDA cut Brazil’s 2020-21 corn production by 7 million tons to 102 million. We are near 98 million tons. For new crop they see Brazil corn production rising to 118 million tons, and that could put a dent in US exports. USDA looks for new-crop Argentina corn output to increase 4 million tons from this year. China corn production for 2021-22 is expected to increase 7.3 million tons to 268 million but as mentioned above imports are expected to remain strong. USDA looks for China domestic corn use to increase a modest 5 million tons. We think this is light given their initiative to expand animal unit production and use more corn for ethanol use. For soybeans, USDA sees new-crop Brazil production increasing 5.9% or 8 million tons to a record 144 million tons, and for Argentina new-crop output to increase 10.6% to 52 million tons. We think if the US export campaign falls short of expectations for 2021-22, much of the balance of what is not exported could be used by crushers as renewable fuel demand increase. Brazil 2021-22 soybean exports were projected at 93 million tons, up 7 million tons from 2020-21, a good reason to justify for a contraction in new-crop US exports from the current year.

USDA increased its US hard winter and hard spring ending stocks by 12 million bushels each, increased soft red winter by 8, and lowered white and durum stocks by 11 and 1 million, respectively. USDA looks for new-crop feed wheat to increase 70 million bushels to 170 million from the current crop year. I think some of the trade was penciling in higher wheat for feed for the current marketing year due to the rise in corn prices but remember most of the wheat that is used for feed occurs during the summer quarter. US wheat ending stocks, along with the global carryout, is seen comfortable.

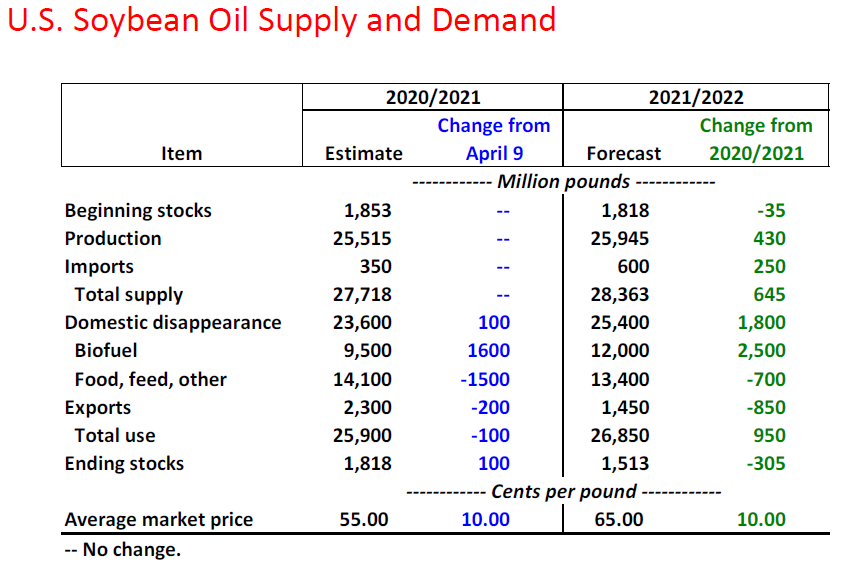

USDA’s US soybean oil biofuel category indicates strong demand for soybean oil, in part to the emerging renewable biodiesel industry.

July is seen in a $6.00 and $7.75 range

December corn is seen in a $4.75-$7.00 range.

July soybeans are seen in a $14.75-$16.50; November $12.75-$15.00

Soybean meal – July $400-$460; December $380-$460

Soybean oil – July 60-68; December 48-60 cent range

July Chicago wheat is seen in a $6.75-$8.00 range

July KC wheat is seen in a $6.60-$7.50

July MN wheat is seen in a $7.25-$8.25

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International

One Lincoln Center

18 W 140 Butterfield Rd.

Oakbrook Terrace, Il. 60181

W: 312.604.1366

ICE IM: treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.