FOMC

Benchmark Interest Rate Unchanged; Target Range Stands At 0.00% – 0.25%

–

Interest Rate On Excess Reserves Unchanged At 0.10%

sees 0% rates thru 2023

Choppy

trade but nearby soybean meal proved resilient to on and off pressure in soybeans and soybean oil amid Argentina strike concerns. Corn bounced higher possibly on unwinding of recent soybean/corn spreading and wheat fell on lack of US export developments.

![]()

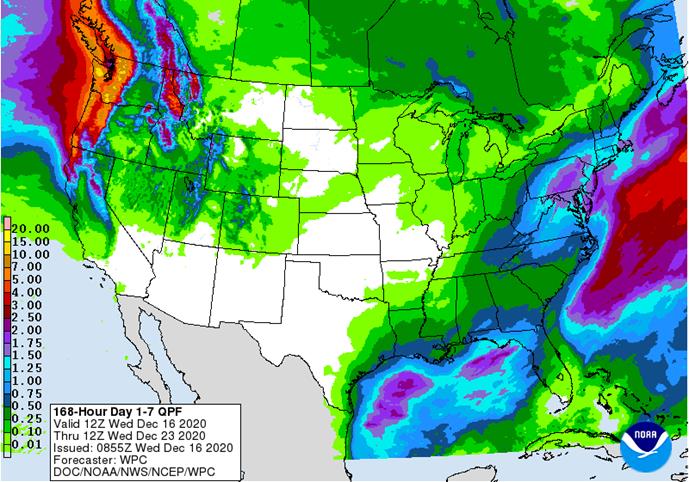

EARLY

MORNING WEATHER UPDATE

- Argentina’s

rain forecast for Friday into Saturday was notably reduced by the GFS model run overnight, but that was a badly needed change - The

European model run was also a little lighter on rainfall, but our official forecast has not changed much today because we did not buy into the GFS solution Tuesday - Rainfall

of 0.40 to 1.50 inches is expected to be most likely with a few locations to get up to 2.25 inches

- All

of the precipitation will be welcome, but with the following seven days expected to be dry there is not going to be a lasting break from the dryness and concern over returning stress sooner than the market was expecting following some forecasts released Tuesday

has the market a little bullish today - Argentina

is not on a path to see huge improvements in weather and its production potential is certainly not set in stone. Early season crop losses have already occurred, but the bulk of summer crops are still being planted and their fate will be largely determined

by weather in January and February. La Nina will not go away fast enough to allow good rainfall into Argentina on a more routine basis and that will keep the worry over crop conditions running high for at least a few more weeks, despite periodic bouts of erratic

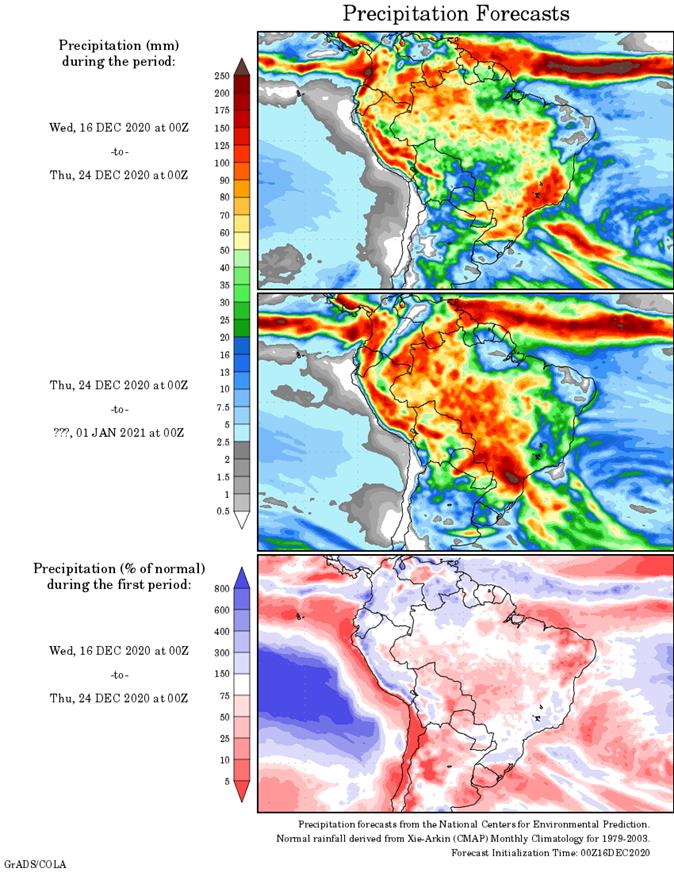

rain. - Brazil’s

weather outlook has not changed much - There

is still some worry over erratic rainfall advertised in Mato Grosso, northern Mato Grosso do Sul, Bolivia, southern Goias and areas northeast into Piaui and Bahia today - These

areas will be driest through the weekend, but next week’s rain is still expected to be erratic and lighter than desired in some areas and the situation will still be closely monitored - However,

from a soil moisture perspective many areas in Brazil will continue to experience a good environment for improved crop development - Interior

southern and center south Brazil crop areas are still expecting sufficient rain to support long term crop development - Southern

Paraguay and southwestern Parana along with a few far southern Mato Grosso do Sul locations should be wettest in the coming several days - After

that, southern Minas Gerais and northeastern Sao Paulo will be wettest - The

greatest rain advertised for Brazil’s center west and northeastern crop areas evolves next week especially mid- to late week - Center

west Brazil will continue to be a little warm over the next several days while rainfall is most restricted and light.

- Indonesia

and Malaysia rainfall recently has become a little lackluster and a boost in precipitation will eventually be needed - No

area is dry enough to pose a threat to short rooted crops, but greater volumes of rain would be welcome - The

pattern of erratic rainfall that is a little lighter than usual may prevail through the end of this month - U.S.

weather Tuesday brought more snow to the central Plains and into a part of the lower Midwest overnight while rain evolved in the Delta and was advancing northeastward today - Snow

accumulations of 1 to 5 inches occurred in parts of hard red winter wheat country - Local

accumulations to 8 inches occurred in northwestern Kansas while up to 10 inches occurred near Woodward, Oklahoma (located in the northwest part of that state) - Moisture

totals were not more than 0.23 inch through dawn today – at least officially, although Doppler radar suggested a few areas in west-central and northwestern Oklahoma received up to 0.40 inch - Snow

accumulations in the lower Midwest were mostly 1 to 2 inches, but portions of central Indiana received 2 to 4 inches - Light

rain fell in the middle and lower Delta and from there into the interior southeastern states and moisture totals through dawn today varied from 0.05 to 0.75 inch, although much of the precipitation had been light - Temperatures

were quite cold again this morning in the U.S. Plains - Lows

in the teens occurred in West Texas and in the negative and positive single digits across eastern Colorado and far western Kansas - No

crop threatening conditions were suspected - U.S.

weather is expected to be tranquil for a while - Today’s

storm in the lower eastern Midwest, Delta and southeast will shift to the middle and northern Atlantic Coastal States today and early Thursday - Heavy

snow will fall from the mountains of Virginia through central and eastern Pennsylvania to southern New York and parts of southern New England - Accumulations

of one to two feet will occur in central Pennsylvania while 4 to 10 inches occurs around that area - Lighter

snowfall will occur in the eastern Midwest with 1 to 2 inches expected - Another

frontal system moving through the Midwest this weekend will produce some additional snow and rain with some rain in the Delta as well - One

more storm system will move through the Midwest in the middle to latter part of next week and it too will impact the southeastern states with some more precipitation as well - Temperatures

will be warmer than usual in the north-central states in the coming week and then trend a little cooler during the last week of this month - No

extreme cold is expected, but temperatures will come closer to normal - U.S.

northern Plains moisture is expected to continue limited over the next ten days - U.S.

southwestern Plains will fail to get much “meaningful” moisture in the next ten days - Far

southwestern U.S. crop areas will remain drier biased over the next two weeks - U.S.

Delta and southeastern states will remain plenty moist over the next two weeks especially in the southeastern states - Eastern

Australia’s recent precipitation induced some flooding along the upper New South Wales and lower Queensland coasts

- Some

damage to sugarcane may have occurred, but other crops were not seriously impacted - Australia’s

rain in the coming ten days will advance a little farther inland, but “western” cotton and sorghum areas are not likely to get much precipitation - Central

and eastern cotton and sorghum areas of Queensland and northeastern New South Wales will get some much needed rain to help improve planting prospects for sorghum and late season cotton - Far

southern India will receive additional rain through the weekend and then drier biased conditions are likely - Sporadic

showers will occur in other central, eastern and far northern crop areas, but most of them will not produce enough moisture to change soil or crop conditions - South

Africa will continue to receive erratic rainfall over the next two weeks resulting in good soil moisture in the central and east eventually, but some greater precipitation will be needed

- Rainfall

through this weekend will be erratic and light favoring the central and east, but a bigger boost in rainfall might be needed - Western

crop areas will get needed rain during mid- to late-week next week and that will eventually spread to the east improving soil moisture at that time - Northern

and central China winter crops will not experience much precipitation for a while and crops will remain dormant - Southern

China will experience precipitation most often during the next two weeks with next week wettest - Some

disruption to sugarcane harvest might occur - Southern

Vietnam, Thailand and Cambodia will trend drier over the coming week after recent rain

- The

recent moisture delayed harvest progress for some crops, but no serious crop quality changes are likely - Winter

crops benefitted from the expected moisture - Routinely

occurring precipitation is expected in Philippines, Indonesia and Malaysia over the next two weeks - A

tropical disturbance will move through much of the nation Thursday through Monday producing some significant rainfall and possible flooding - Another

tropical cyclone may form in the South China Sea Sunday into Monday and drift toward southern coastal areas of Vietnam while weakening later next week - Indonesia

and Malaysia rainfall will continue erratic and lighter than usual - Recent

weeks of precipitation has been lighter than usual and more sporadic leaving some areas with less than usual moisture, but soil conditions are still rated mostly good - A

boost in rainfall will have to occur soon, but may not take place for a while - Isolated

to scattered showers will occur at times, however - Russia’s

Southern Region had eastern Ukraine will receive some rain and snow over the next few days - Moisture

totals are unlikely to be great enough to seriously change soil moisture and crops are dormant and unlikely to respond - Moisture

totals will vary up to 0.20 inch - Some

follow up precipitation is “possible” next week and again later this month, but resulting precipitation in each event will be limited - The

bottom line remains one of concern, but World Weather, Inc. believes there will be some increase in soil moisture from periodic precipitation this winter and spring to give crops a chance to improve during the spring. Some increase in snow cover in northern

parts of the production region will help protect crops against any harsh winter weather that comes along - Temperatures

will be a little warmer than usual over the next two weeks - Europe

precipitation during the coming week will be greatest in France, the U.K., northwestern parts of Spain, Portugal and a few other areas in the North Sea region - Some

local flooding is possible in many of these areas - Net

drying is expected in the Baltic Plain and areas south into the lower Danube River Basin this week - Temperatures

will be warmer than usual - North

Africa will receive sporadic rain for a while except in coastal areas of northeastern Algeria - Morocco

remains in need of significant rain and should get some today, although it will be light - Greater

rain may continue to elude the region for the next couple of weeks, despite a few light showers - Southern

Oscillation Index was at +11.67 today and it will remain strongly positive for a while - Tropical

Cyclone Zazu and Tropical Cyclone Yasa in the southwestern Pacific Ocean will not impact any major agricultural area, but the storm systems will move through some of the smaller Pacific Islands this week - Zazu

was dissipating today, but Yasa was a powerful storm that may impact a part of the Fiji Islands over the next few days - Mexico

precipitation will be quite limited over the coming week - Portions

of Central America will continue to receive erratic rainfall over the next couple of weeks, but the intensity and frequency will be low enough to support some farming activity - Costa

Rica and Caribbean coastal areas of both Nicaragua and Honduras will be wettest this workweek

- West-central

Africa will experience unusually great rainfall this week stalling harvest progress and raising a little worry over cocoa and coffee conditions - Some

rain will also reach into southwestern Ghana and Senegal - Drier

weather is needed; this is normally the start of the dry season - East-central

Africa rain will be erratic and light in Ethiopia, Kenya and Uganda while rainfall will be greatest over Tanzania this week - Some

rain will develop this weekend into next week in Ethiopia, Kenya and it may increase in Uganda - New

Zealand will be drier than usual this week from northern and central parts of South Island to North Island while rain falls to the southwest - Temperatures

will be near to above average

Source:

World Weather Inc. and FI

Thursday,

Dec. 17:

- USDA

weekly crop net-export sales for corn, soybeans, wheat, cotton, pork, beef, 8:30am - USDA

Total Milk Production, 3pm - Port

of Rouen data on French grain exports - Conab’s

estimate for 2020 Brazil coffee crop - Poland

publishes crop output figures for 2020

Friday,

Dec. 18:

- ICE

Futures Europe weekly commitments of traders report, 1:30pm (6:30pm London) - CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm - U.S.

Cattle on Feed

Source:

Bloomberg and FI

FOMC

Benchmark Interest Rate Unchanged; Target Range Stands At 0.00% – 0.25%

–

Interest Rate On Excess Reserves Unchanged At 0.10%

sees 0% rates thru 2023

US

DoE Crude Oil Inventories (W/W) 11-Dec: -3135K (est -2200K; prev 15189K)

–

Distillate Inventories (W/W): 167K (est 850K; prev 5222K)

–

Cushing OK Crude Inventories (W/W): 198K (prev -1364K)

–

Gasoline Inventories (W/W): 1020K (est 1874K; prev 4221K)

–

Refinery Utilization: -0.80% (est 0.50%; prev 1.70%)

US

Retail Sales Advance (M/M) Nov: -1.1% (est -0.3%; prevR -0.1%; prev 0.3%)

US

Retail Sales Ex-Auto (M/M) Nov: -0.9% (est 0.1%; prevR -0.1%; prev – 0.2%)

US

Retail Sales Ex-Auto, Gas Nov: -0.8% (est 0.1%; prevR -0.1%; prev 0.2%)

US

Retail Sales Control Group Nov: -0.5% (est 0.2%; prevR -0.1%; prev 0.1%)

Canadian

CPI NSA (M/M) Nov: 0.1% (est 0.0%; prev 0.4%)

Canadian

CPI (Y/Y) Nov: 1.0% (est 0.8%; prev 0.7%)

Canadian

CPI Core – Median (Y/Y) Nov: 1.9% (est 1.9%; prev 1.9%)

Canadian

CPI Core – Common (Y/Y) Nov: 1.5% (est 1.6%; prev 1.6%)

Canadian

CPI Core – Trim (Y/Y) Nov: 1.7% (est 1.8%; prev 1.8%)

Canadian

International Securities Transactions Oct: 6.92B (prev 4.46B)

Canadian

Wholesale Trade Sales (M/M) Oct: 1.0% (est 0.7%; prev 0.9%)

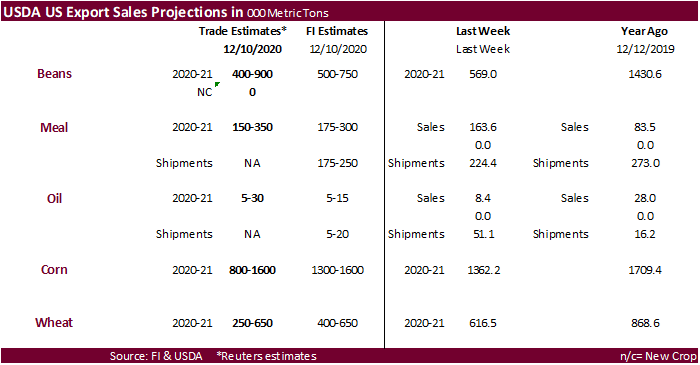

Corn.

-

CBOT

March corn traded

two-sided with March ending 2.50 cents higher and May up 2.0 cents. Lack of fresh news kept corn from rallying early but as soybeans paired gains by mid-morning, unwinding of recent soybean/corn spreading underpinned corn futures.

-

Funds

bought an estimated net 8,000 corn contracts. -

Bloomberg

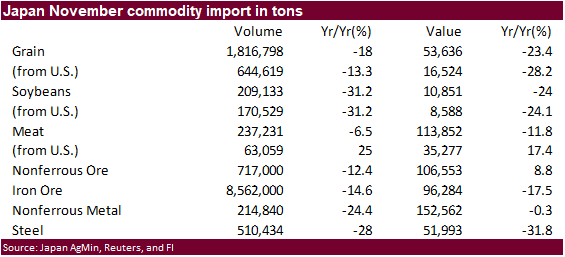

reported China is close to securing a trade deal with China to supply corn. Talks are in advanced stages and many of the technical issues have been resolved.

-

China

corn futures fell to their lowest level since September 30. -

China’s

Heilongjiang plans to offer 714,516 tons of 2015 corn from state reserves on Thursday. -

China

will offer to sell 20,000 tons of pork sales from reserves on Thursday. The Chinese government expects hog numbers to rebound back to pre‐ASF levels by mid‐2021. -

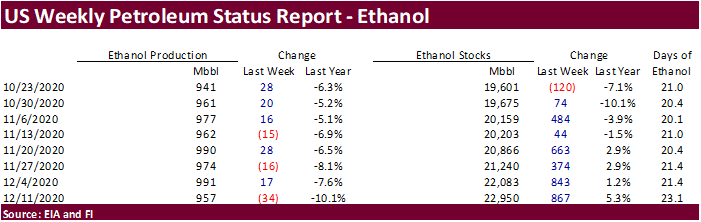

EIA

weekly US ethanol production for the week ending 12/11 was reported at 957,000 barrels per day, down 34,000 barrels from the previous week, bearish in our opinion for US corn futures. Weekly ethanol stocks were up a large 867,000 barrels to 22.950 million

barrels. A Bloomberg poll looked for weekly US ethanol production to be down 9,000 from the previous week and stocks up to 320,000 barrels. Weekly ethanol production slipped to its lowest level since mid-November. September to date ethanol production is

running 6.3 percent below the same period year ago. Ethanol stocks are highest since May 22. Ethanol blended into gasoline were 7.94 million barrels, representing 89.3 percent of blend rate into finished motor gasoline.

Corn

Export Developments

- None

reported

Updated

11/30/20

March

corn is seen

trading in a $4.15 and $4.40 range.