PDF Attached

USDA

– 182,020 corn was sold to Mexico. Soybean oil and oats were the only major CBOT ag markets to appreciate today, other than CBOT crush bias nearly positions. Soybeans, corn and wheat were under pressure mainly on technical selling ahead of the weekend.

Weather

MOST

IMPORTANT WEATHER IN THE WORLD

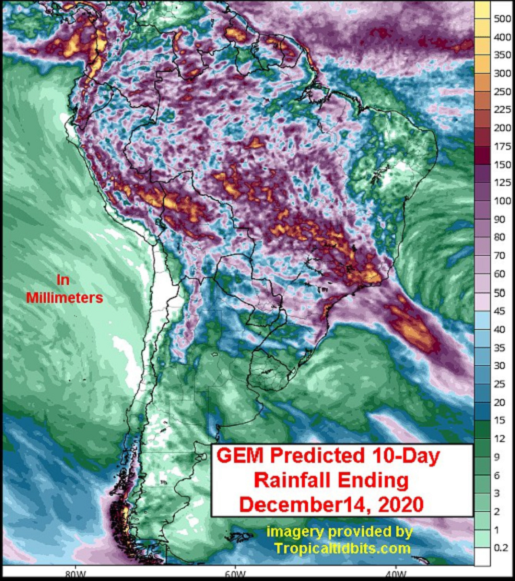

- Argentina

will need to be closely monitored over the next ten days - Soil

moisture this week has been the best seen so far this growing season - However,

portions of the southwest still need significant moisture - Good

subsoil moisture in Buenos Aires and neighboring areas to the north will carry crops through much of the coming week of net drying - Western

crop areas will need timely rainfall sooner than the east to maintain the best possible crop development - Rain

expected late next week and into the following weekend will not be a general soaking, but it will likely buy some crops more time before greater stress evolves - The

key to Argentina production this year will be in the timeliness of rainfall not the quantity – so far early season corn and sunseed have lost yield potential, but more recently planted crops have benefited from the timelier rainfall - Warmer

temperatures during the drier periods will have much more influence on soil moisture as time moves along making it more difficult to keep good soil moisture present between rain events - Past

La Nina events of similarity have kept a very stressful environment present in Argentina through December and then improving conditions occurred in January and February – that does not mean the same will occur this year - Brazil

has still not turned the corner on soil moisture even though there has been great “talk” about improving conditions; however, the change is still expected this weekend and especially next week - Substantial

improvements have already occurred in southern Paraguay, southwestern Parana and some immediate neighboring areas from rain this week - Rio

Grande do Sul topsoil moisture has also temporarily improved, but more rain will be needed especially after a full week of net drying that is anticipated - Mato

Grosso and southern Goias has some of the worst soil conditions and crop stress they have seen in many years, but only the early planted crops have likely suffered a notable decline in production potential, but those crops were not planted nearly as aggressively

as usual because of poorly distributed rainfall in September and early October - Many

more crops were planted more recently when there was a little more timeliness to rainfall keeping their production potential a little better - Rain

advertised for Mato Grosso and Goias in the next couple of weeks will be imperative for saving the states’ crop production potential - Minas

Gerais will receive the greatest and most frequent rainfall over the next two weeks

- Some

areas might become a little too wet - The

bottom line for Brazil is still one of improvement beginning with greater rainfall that will evolve this weekend through all of next week in center south and center west. Far southern Brazil will likely dry out again raising concern over crop conditions there

during mid-month. Until then the areas that will dry down most significantly will be Bahia and Piaui where subsoil moisture is still favorable today, but will decline as time moves along - GFS

model run has exaggerated precipitation potentials for U.S. hard red winter wheat areas during the Dec. 11-13 period - The

region will have a chance for “some” precipitation, but it will not be enough to seriously change soil conditions in the west - Net

drying is expected in U.S. hard red winter wheat areas in the coming week - Australia’s

hottest temperatures are abating, but the past week has been brutal for some of the dryland crop and livestock areas in the nation - Unirrigated

cotton sorghum and other crops in Queensland and may have to be replanted when rain finally resumes; however, not much precipitation is expected for a while - Temperatures

will continue warmer than usual, but not as oppressively hot as they have been

- Some

shower activity will increase Dec. 11-17 - Australia’s

dryness in unirrigated summer crop areas is a big concern and recent livestock stress has returned some concern over the long range outlook for these areas. Bush and forest fires could become a problem again later this summer if there is not significant rain

soon. - Southern

Russia and other areas near the Black Sea will experience a little more precipitation in December than in November and there will be “some” increase in soil moisture for the region and a little snow cover at times, too; however, moisture deficits will remain

in at least a part of this region - Central

and western Ukraine will receive some periodic rain and snow in the next week to ten days while precipitation in Russia’s Southern region and eastern Ukraine is more limited - South

Africa rainfall will scatter across the nation over the next ten days benefiting most summer crop areas and improving early season emergence and growth eventually - Portions

of the nation are still a little too dry for optimum crop development, but the rain coming should bring improvement

- Free

State, western North West and eastern Northern Cape are among the driest areas - Tamil

Nadu, India and northern Sri Lanka were impacted by Tropical Cyclone Burevi Wednesday and Thursday, but little damage resulted - The

storm will linger in far southern Tamil Nadu and southern Kerala today before moving out to sea in the Arabian Sea this weekend - The

storm will produce additional moderate to heavy rain in Tamil Nadu and Kerala possibly resulting in some local flooding and minor amount of damage to personal property and agriculture - Additional

waves of rain will continue far southern India and Sri Lanka through early next week, although amounts will be much lighter - Total

rainfall of 2.00 to 5.00 inches will occur with locally more - Sugarcane,

rice and some cotton will be most impacted by the abundant moisture - Other

areas in India will experience good weather for crop maturation and harvest progress - U.S.

weather will be trending drier this weekend after an eastern storm system moves out to sea

- Rain

will also impact Florida and some central Gulf of Mexico coastal areas late this weekend into Monday - U.S.

weather next week will bring another storm from the southwestern states into the southern Plains during the second half of the week and then northeast to the Great Lakes region in the following weekend - A

couple of follow up storm systems will impact the nation in the week of Dec. 14.

- U.S.

temperatures will be quite warm in the north-central states and New England in this first week of the outlook and then cooling is expected in many areas in the central and northwestern parts of the nation in the following week - Snow

cover in CIS winter crop areas continues restricted in some areas, but there has been no threatening cold in recent days and none was expected through the next ten days - Bitter

cold will be confined to the eastern New Lands and Kazakhstan - Brief

periods of light snow and rain will impact the western CIS over the next ten days; not much improvement in soil moisture is expected in the drier areas leaving parts of Ukraine, Russia’s Southern Region and Kazakhstan still in need of greater moisture - Temperatures

will be close to normal west of the Ural Mountains and below average to the east - Europe

precipitation is expected to be erratic over the next ten days to two weeks with sufficient amounts in some areas to bolster soil moisture for use in the spring - Italy,

the eastern Adriatic Sea region, parts of the Iberian Peninsula France and the U.K. will be wettest - Soil

moisture is still favorable in much of the continent - Temperatures

will be seasonable with a cool bias in the west and a warm bias in the east - North

Africa rainfall will be greatest and most frequent in the coming week to ten days in northern Algeria, although some beneficial moisture will also impact northeastern Morocco and a few northern areas of Tunisia - Greater

rain is needed in Morocco and northwestern Algeria to improve planting conditions for wheat and barley - China

weather over the next two weeks will include restricted amounts of precipitation and temperatures will be near to slightly below average except in the far northeast where they will be a little warmer biased - East-central

parts of the nation will be wettest keeping some southern wheat and rapeseed areas plenty moist - Indonesia,

Malaysia and Philippines weather during the next two weeks will be routinely moist with frequent showers and thunderstorms supporting long term crop development - Interior

parts of mainland Southeastern Asia will be mostly dry over the next ten days - Some

frequent rain will occur along the Vietnam coast due to a strong northeast monsoon flow pattern - Local

flooding may occur, but mostly next week - Southern

Oscillation Index was +8.72 today; the index will hold steady or slowly rise over the next week.

- Mexico

precipitation will be quite limited over the coming week favoring summer crop maturation - Southern

areas will be wettest and only light rainfall from scattered showers will result - Portions

of Central America will continue to receive periodic rainfall over the next couple of weeks, but the intensity and frequency of rain will be low in the north - Costa

Rica and Panama will be wettest along with southern Nicaragua this workweek

·

West-central Africa will experience erratic rain through the next ten days favoring crop areas close to the coast

·

East-central Africa rain will be erratic and light over the coming week

·

New Zealand rainfall will be erratically distributed over the next ten days benefiting most areas

- Amounts

will be near to above average along the west coast of South Island and in a few southern areas of North Island in this first week of the outlook and below average elsewhere - Temperatures

will be a little cooler than usual

Source:

World Weather Inc. and FI

Friday,

Dec. 4:

- ICE

Futures Europe weekly commitments of traders report, 1:30pm (6:30pm London) - CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm - China’s

CNGOIC to publish monthly soy and corn reports - FranceAgriMer

weekly update on crop conditions

Monday,

Dec. 7:

- China

trade data on soybean and meat imports for November - Ivory

Coast cocoa arrivals - USDA

weekly corn, soybean, wheat export inspections, 11am - HOLIDAY:

Thailand

Tuesday,

Dec. 8:

- Australia’s

Abares releases quarterly agricultural commodities report - French

agriculture ministry to publish crop estimates - UkrAgroConsult

Black Sea Grain conference - BRF

Day - Brazil

Unica cane crush, sugar production (tentative) - National

Grain & Feed Association Country Elevator Conference, 10am

Wednesday,

Dec. 9:

- EIA

U.S. weekly ethanol inventories, production, 10:30am - National

Grain & Feed Association Country Elevator Conference, 10am

Thursday,

Dec. 10:

- China’s

agriculture ministry (CASDE) releases monthly report on supply, demand, 10am local - Malaysian

Palm Oil Board releases data on November stockpiles, exports, production, 12:30pm local - FranceAgriMer

monthly crop report - Agroinvestor

Russian agriculture conference - Port

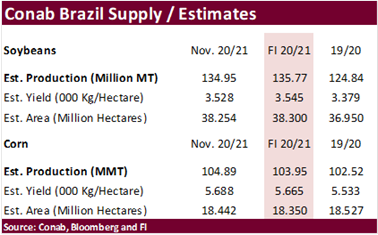

of Rouen data on French grain exports - Conab’s

data on area, output and yield of soybeans and corn in Brazil, 7am - National

Grain & Feed Association Country Elevator Conference, 10am - USDA

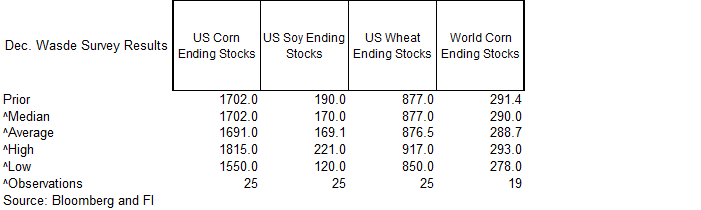

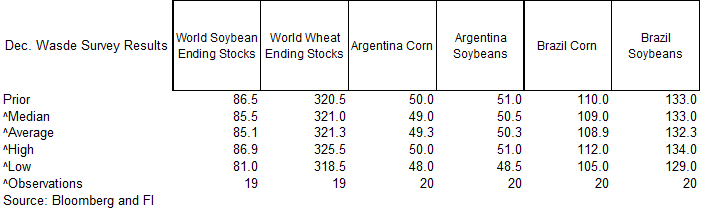

weekly crop net-export sales for corn, soybeans, wheat, cotton, pork, beef, 8:30am - USDA’s

monthly World Agricultural Supply and Demand (WASDE) report, 12pm - HOLIDAY:

Thailand

Friday,

Dec. 11:

- ICE

Futures Europe weekly commitments of traders report - HOLIDAY:

Thailand

Source:

Bloomberg and FI

Bloomberg

Trade Estimates:

Attached

is our updated Baltic Dry Index chart

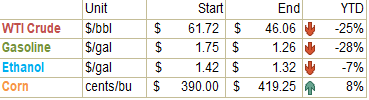

LT

1,189 on 12/3/20, down 6% month over month, up 9% from December 31, 2019. CRB Index is up 8.4% from this time last month and down 14.3% from the end of 2019.

CFTC

Commitment of Traders

Funds

were again more long than expected as of last Tuesday for corn and soybeans, and were more long for wheat, meal and soybean oil.

SUPPLEMENTAL

Non-Comm Indexes Comm

Net Chg Net Chg Net Chg

Corn

296,452 -13,390 389,281 1,148 -657,758 18,543

Soybeans

166,311 -10,646 186,233

-7,727 -350,615 23,090

Soyoil

75,735 -4,995 129,988 -607 -224,269 6,200

CBOT

wheat -28,845 -21,891 136,967 -2,387 -90,400 26,195

KCBT

wheat 23,263 -581 69,156 -2,541 -94,078 2,489

=================================================================================

FUTURES

+ OPTS Managed Swaps Producer

Net Chg Net Chg Net Chg

Corn

270,633 -16,967 241,804 2,498 -628,469 18,543

Soybeans

194,683 -9,127 118,029 -4,808 -353,324 23,060

Soymeal

70,386 -749 71,120 -882 -189,186 5,075

Soyoil

104,715 -626 89,777 -2,270 -232,405 8,109

CBOT

wheat -4,397 -19,696 87,549 334 -80,497 22,288

KCBT

wheat 44,506 -3,915 42,319 -998 -89,769 2,578

MGEX

wheat 4,755 -1,099 2,099 -23 -10,478 3,948

———- ———- ———- ———- ———- ———-

Total

wheat 44,864 -24,710 131,967 -687 -180,744 28,814

Live

cattle 39,813 -211 65,455 -2,906 -117,591 -1,203

Feeder

cattle 1,067 1,764 7,749 671 -3,686 -758

Lean

hogs 38,359 1,926 48,004 -69 -87,999 -2,320

Other NonReport Open

Net Chg Net Chg Interest Chg

Corn

144,006 2,227 -27,974 -6,300 2,078,871 -57,572

Soybeans

42,539 -4,408 -1,928 -4,717 1,253,881 -8,466

Soymeal

22,209 -1,662 25,470 -1,782 475,823 -9,372

Soyoil

19,365 -4,615 18,547 -599 545,609 8,864

CBOT

wheat 15,066 -1,008 -17,721 -1,918 475,976 -15,536

KCBT

wheat 1,286 1,701 1,658 633 223,335 -8,644

MGEX

wheat 3,429 -197 195 -2,627 66,959 -2,417

———- ———- ———- ———- ———- ———-

Total

wheat 19,781 496 -15,868 -3,912 766,270 -26,597

Live

cattle 25,408 4,048 -13,084 272 326,450 -269

Feeder

cattle 1,888 27 -7,019 -1,706 43,860 2,144

Lean

hogs 14,615 -1,210 -12,979 1,674 250,974 -313

US

Non-Farm Payrolls (Nov): 245K (est 469K, prevR 610K)

·

Unemployment Rate (Nov): 6.7% (est 6.8%, prev 6.9%)

·

Average Earnings (Nov) Y/Y: 4.4% (est 4.3%, prev 4.5%)

US

Private Payrolls (Nov): 344K (est 589K, prevR 877K)

·

US Manufacturing Payrolls (Nov): 27K (est 43K, prevR 33K)

·

US Average Earnings (M/M) Nov: 0.3% (est 0.1%, prev 0.1%)

·

US Average Workweek Hours (Nov): 34.8 (est 34.8, prev 34.8)

US

Trade Balance (Oct): $-63.1Bln (est -$64.8Bln, prevR -$62.1Bln)

Canada

Net Change In Employment (Nov): 62.1K (est 20K, prev 83.6K)

·

Unemployment Rate (Nov): 8.5% (est 9%, prev 8.9%)

·

Full Time Employment Change (Nov): 99.4 (prev 69.1)

·

Part Time Employment Change (Nov): -37.4 (prev 14.5)

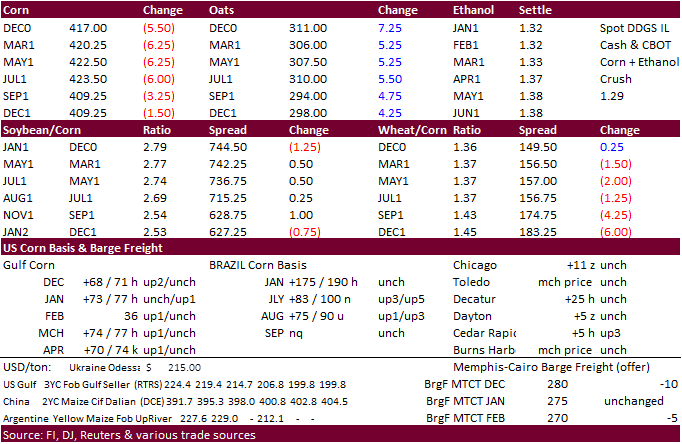

Corn.

-

March

corn started the day session lower and the contract dropped below a long-term (Aug-present) trend line on technical selling. March ended 6.0 cents lower at $4.2050, a bearish signal. We saw risk off today ahead of the weekend. Funds are still long and some

of the longs don’t want to go home with positions in case South American weather models happen to change by Sunday night.

Lack

of bullish news added to the negative sentiment. For the week, corn futures posted their first weekly loss since October (same with soybeans). Many of Brazil’s driest areas should see rain next week. About 90 percent of Argentina’s crop production area should

see drought relief by mid-December, according to Commodity Weather Group.

-

Funds

sold an estimated net 20,000 corn contracts. -

Argentina

Jan-Oct corn exports hit a record 34.5 million tons, up 10 percent from the same period last year (AgriCensus).

-

Argentina’s

markets will be closed Monday and Tuesday for holiday. -

The

USD was 9 points higher and WTI crude was $0.40 higher, during midafternoon trading.

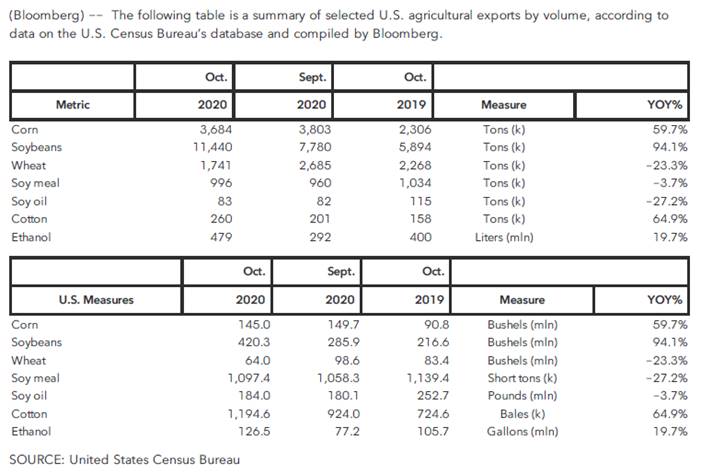

-

US

October corn exports were up 60 percent from the previous year. See table above the macro section. It is too early for us to revise our corn exports for the current year, projected at 2.550 billion bushels, 100 million less than USDA. We would like to see

more confirmation in shipments, expected to be back loaded this marketing year. On Friday we heard China was looking at importing Brazilian corn during Q4 corn crop year (summer months). If they procure from Brazil, the bulk of US shipments may occur during

the October through May period. -

AgRural

lowered their Brazil summer corn crop estimate to 19.4 million tons from 20.7 million previous.

Corn

Export Developments

- Under

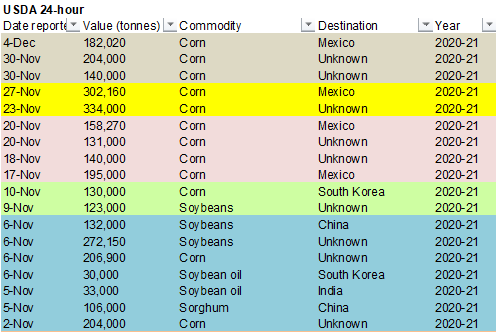

the 24-hour announcement system, private exporters sold 182,020 tons of corn to Mexico for 2020-21 delivery.

- South

Korea’s MFG bought 68,000 tons of optional origin corn at $240.19/ton c&f for arrival around May 15. This is on top of the 68,000 tons they bought on Thursday at $239.90.

- Algeria

bought 35,000 tons of corn at around $235/ton c&f for shipment by January 5.

Updated

11/30/20

March

corn is seen

trading in a $4.15 and $4.40 range.