PDF Attached

.

WORLD

WEATHER ISSUES FOR TODAY

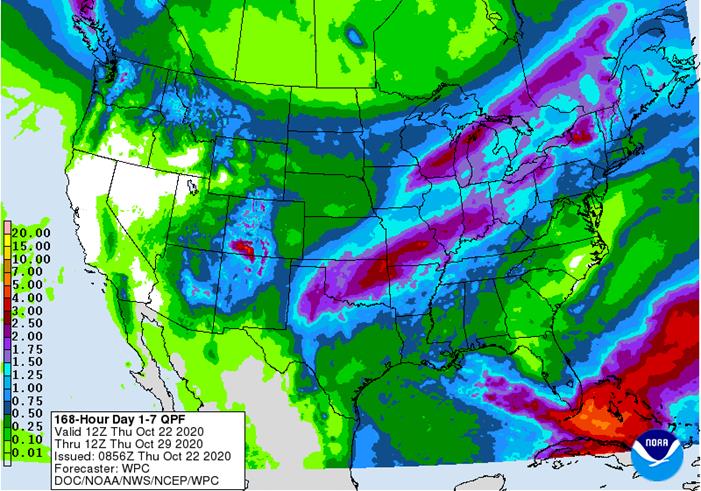

- U.S.

Northern Plains and upper Midwest dealing with another snowstorm today - Accumulations

through dawn today have range from 1 to 4 inches in northern South Dakota and southern North Dakota with 12 inches unconfirmed at Herreid, South Dakota - Snowfall

of 4 to 7 inches has been reported in central Minnesota and northwestern Wisconsin - New

snowfall today will vary from 3 to 9 inches across these same areas causing travel delays, livestock stress and some disruption to commerce - One

more snowstorm is expected in the northwestern and central U.S. Plains late Friday through the weekend with snowfall of 2 to 6 inches expected - Western

South Dakota, Montana and parts of Wyoming and western Nebraska will get the greatest snowfall - Lighter

snow will fall farther south in Kansas, Colorado and the Texas Panhandle with moisture totals of a few hundredths of an inch to 0.25 inch most likely - Eastern

U.S. hard red winter wheat areas will see greater rainfall with 0.20 to 0.75 inch of moisture possible from north-central Texas to eastern wheat areas of Kansas and parts of eastern Nebraska this weekend into early next week - U.S.

Hard Red Winter Wheat bottom line is one of partial improvement of wheat establishment in the high Plains region. More precipitation will be needed, but not likely to occur with warmer than usual temperatures expected late next week through the first full

week of November and little to no rain - Russia’s

Southern has seen some partial relief from dryness this week (see our special reported sent earlier this morning) - Delayed

data received from Russia overnight has further verified our forecast of earlier this week for a band of rain from Krasnodar to northwestern Kazakhstan Monday and Tuesday - The

moisture was welcome, but not great enough for a huge lasting change outside of a small portion of the overall production region - More

rain is needed and not likely to occur for the next ten days to nearly two weeks except in the northernmost parts of Russia’s Southern region where some light precipitation is expected.

- Eastern

Australia will be closely monitored for too much rain over the next few weeks, but for now most of the wheat, barley and canola is still rated favorably and rain expected will benefit the planting and emergence of dryland summer crops - Rain

in eastern Queensland Wednesday may have disrupted fieldwork, but the moisture was great for sugarcane and eastern cotton areas where planting in dryland fields will get under way soon if it has not already begun - Western

Australia is not likely to see much more than a few showers in the far south - South

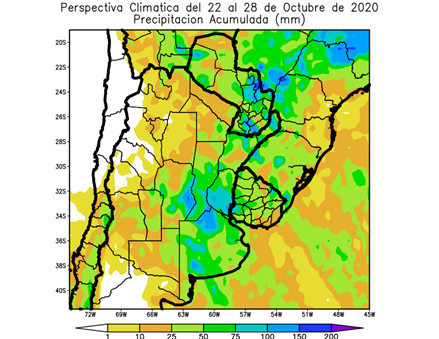

Australia, Victoria and southern New South Wales winter crop conditions remain very good with little change likely - Argentina

rainfall overnight was greater than expected and continued to benefit winter wheat and future planting of corn, sunseed and soybeans - Argentina’s

rainfall this week has already improved soil moisture for many areas and the outlook is for continued improvement with yet another weather system expected this weekend that will follow additional scattered showers today - Dryness

is expected in the second week of the outlook, but that will serve as an excellent opportunity for summer crop planting and to support winter wheat in the south - Brazil

rainfall will be erratic over the next two weeks benefiting some areas far more than others and a close watch on its distribution is warranted - All

of the nation’s corn, soybean, rice, sugarcane, citrus and coffee production areas will get rain at one time or another, but amounts in the interior south will be a little light and may leave a growing need for greater precipitation - Wheat

conditions in far southern Brazil are better than they have been in years with little change likely - Brazil’s

greatest rainfall is expected in the Oct. 30-Nov. 6 period from Minas Gerais to Mato Grosso - Bitter

cold air is still expected in the northern U.S. Plains and a part of Canada’s Prairies over the next several days

- Extreme

lows in the negative and positive single digits Fahrenheit will occur from Montana, Wyoming and the far western parts of the Dakotas northward into the heart of the Canadian Prairies - Some

single digit lows will occur into western Nebraska and northeastern Colorado

- The

cold and snow that precedes it will stress livestock - Snow

will fall in the central Plains Sunday into Tuesday with accumulations of 1 to 3 inches common from Nebraska to eastern Colorado with local totals of 4 to 5 inches probably favoring northeastern Colorado and far southwestern Nebraska, although confidence is

low - Montana

wheat planting and emergence is incomplete and temperatures will be cold enough for a long enough period of time to raise concern about that planting getting completed - Warming

is expected late next week through the following weekend - U.S.

Midwest harvest delays will occur through mid-week next week due to waves of rain and some snow - Drier

weather is expected in the following week to improve harvest progress, although a period of drying will be required after some significant moisture impacts the region - Snowmelt

will keep the upper Midwest wet for a longer period of time extending the harvest delays - West

Texas cotton and other summer crop harvesting will be delayed by precipitation during the late weekend and early part of next week - No

serious impact on fiber quality is expected - Drier

and warmer weather will return late next week through the first week in November supporting better harvest conditions

- The

sunny and warm conditions will bleach the fiber white again - U.S.

Delta and southeastern states weather will be disrupted by periods of rain over the next week to ten days - Some

of the advertised rain may be overdone and future model forecasts will bring some better field working conditions, but progress will still advance slowly.

- U.S.

Pacific Northwest will receive some rain and mountain snow Friday into the weekend resulting in a short term boost in topsoil moisture that will favor improved winter wheat planting in dryland areas - U.S.

far west will continue drier than usual through much of the next couple of weeks, especially south of the Columbia River Basin - Hurricane

Epsilon is a huge storm, but will pass to the east of Bermuda over the next couple of days and should then turn away from North America posing no land impact - Typhoon

Saudel was located west of the Philippines this morning and was becoming better organized

- Saudel

will move westerly today and Friday and then turn to the west southwest this weekend - Some

weakening is expected as the storm approaches Vietnam - Landfall

is expected in central Vietnam late Sunday or early Monday - Heavy

rain will bring on some additional flooding to water-logged areas of central Vietnam - South

Africa will experience showers erratically over the central and eastern parts of the nation during the coming week with some potential for greater rain in the following week - Generalized

rain is needed to support spring and summer planting - La

Nina should help ensure a good rainy season this summer - India’s

monsoon will start withdrawing a little faster over the next several days ending rain and harvest delays in Gujarat, northern Maharashtra and western Madhya Pradesh over the next couple of days - Rain

will fall frequently in far southern India and in the extreme east for much of the coming week to ten days - Europe

will experience increasing precipitation in the west over this coming week while eastern areas are relatively dry biased and a little warmer than usual - Winter

crops are establishing well in much of the continent, despite less than ideal early season planting conditions - China

weather will be almost ideal for winter wheat and rapeseed planting and summer crop harvesting during the next ten days - Soil

moisture will be good for quick winter crop germination and plant emergence - Disturbed

tropical weather in the Caribbean Sea and southeastern Gulf of Mexico the remainder of this week will be closely monitored but there is no sign or tropical cyclone development for the next few days

- The

system may impact Cuba and Florida with increasing rainfall Friday and this weekend - Southern

Oscillation Index fell during the weekend down to +8.12 and the index will level off over the next few days after a recent fall of significance.

- Southeastern

Canada and the U.S. Great Lakes region will continue to experience frequent precipitation over the coming week causing additional delay to farming activity - Recent

precipitation frequency has been too high for much fieldwork and this trend will linger for a while longer.

- Southeast

Asia rainfall over the next two weeks will be erratic, but all areas will be impacted multiple times supporting most crop needs; some flood potentials will gradually rise in localized areas - Mexico

precipitation will be scattered over far southern crop areas during the coming week - Net

drying is expected for many other summer crop areas supporting crop maturation and harvest progress - Central

America will be wetter than usual over the next ten days to two weeks keeping late season crop maturation and harvest progress slow, but the moisture is improving long term water supply.

- Some

flooding is possible

·

West-central Africa will experience erratic rain through the next ten days favoring coffee, cocoa, sugarcane, rice and other crops

- Daily

rainfall is expected to be decreasing as time moves along which is normal for this time of year - Cotton

areas will benefit from drier weather

·

East-central Africa rain will be erratic and light over the next couple of weeks, but most of Uganda and southwestern Kenya will be impacted while Tanzania and Ethiopia rainfall is erratic and light

- Some

heavy rain may fall in Uganda

·

New Zealand rainfall will be increasing across North Island and western areas of South Island over the coming week

- Temperatures

will be seasonable with a slight cooler bias in the south

Source:

World Weather Inc.

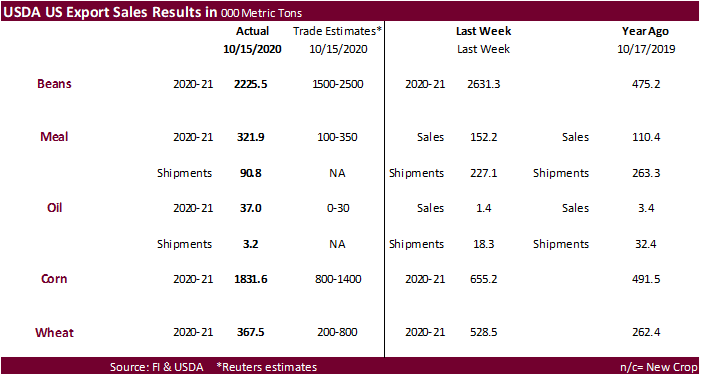

- USDA

weekly crop net-export sales for corn, soybeans, wheat, cotton, pork, beef, 8:30am - Port

of Rouen data on French grain exports - USDA

red meat production, 3pm - U.S.

cold storage data – pork, beef, poultry

Friday,

Oct. 23:

- China

customs publishes trade data on imports of corn, wheat, sugar and cotton - ICE

Futures Europe weekly commitments of traders report, 1:30pm (6:30pm London) - CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm - FranceAgriMer

weekly update on crop conditions - Unica

data on Brazil’s cane crush, sugar production (tentative) - U.S.

cattle on feed, poultry slaughter, 3pm - HOLIDAY:

Thailand

USDA

Export Sales

showed China expanding purchases to soybean meal, oil, and sorghum.

·

Soybean export sales of 2.226 million tons were within expectations. China took 1.222 million tons and Egypt for 194,400 tons.

·

Soybean meal sales improved to 321,900 tons from 152,200 tons previous week. China took 20,000 tons.

·

Soybean oil sales were good at 37,000 tons from only 1,400 tons previous week. China took 11,000 tons.

·

USDA corn export sales were 1.832 million tons, well up from 655,200 tons from the previous week and above trade expectations. The corn sales included Japan (490,100 MT, including 162,800 MT switched

from unknown destinations and decreases of 10,000 MT), China (433,500 MT), and Mexico (377,400 MT, including decreases of 35,400 MT). There was also 125,000 MT optional origin corn for Ukraine and 127,000 MT for Argentina. We are looking into that.

·

Sorghum export sales of 280,000 tons included 195,800 tons for China.

·

Pork sales were 26,800 tons, unchanged from the previous week.

·

All-wheat export sales were 367,500 tons, within expectations. Mexico and Nigeria were the largest buyers.

Macros

US

Initial Jobless Claims Oct 17: 787K (est 870K; prevR 842k; prev 898K)

US

Continuing Claims Oct 10: 8373K (est 9625K; prevR 9397k; prev 10018K)

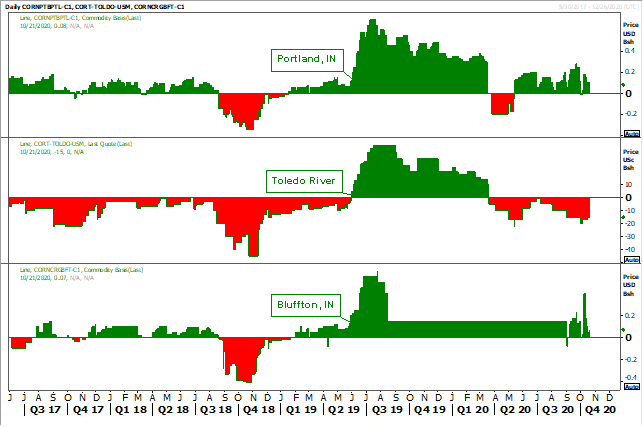

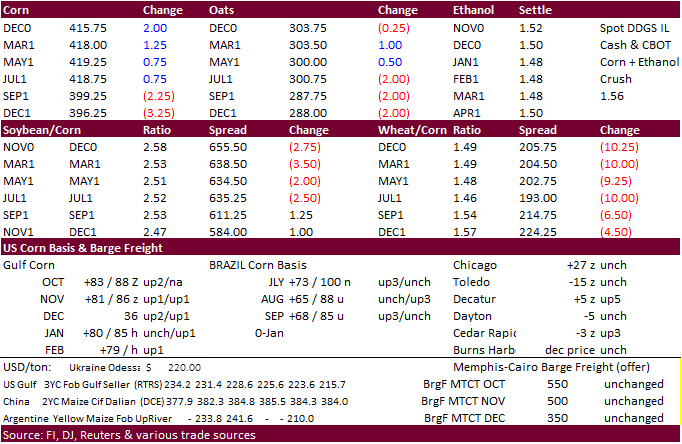

Corn.

-

Corn

futures traded at a 14-month high. December settled 2.50 cents higher. Snowy weather bias northern Great Plains and far northwestern Corn Belt delayed corn harvesting this week.

-

USD

was 34 higher as of 1:44 pm CT, and crude was $0.60 higher.

·

USDA corn export sales were 1.832 million tons, well up from 655,200 tons from the previous week and above trade expectations. The corn sales included Japan (490,100 MT, including 162,800 MT switched

from unknown destinations and decreases of 10,000 MT), China (433,500 MT), and Mexico (377,400 MT, including decreases of 35,400 MT). There was also 125,000 MT optional origin corn for Ukraine and 127,000 MT for Argentina. We are looking into that.

·

Sorghum export sales of 280,000 tons included 195,800 tons for China.

·

Pork sales were 26,800 tons, unchanged from the previous week.

-

Brazil

domestic corn prices were up again, 16 consecutive days of appreciation. -

In

Brazil, shipments of a million tons of corn are stalled as a lack of rain left levels in the Madeira River, a major waterway, at the shallowest in decades. Ships that usually carry 20,000 tons in the high-water season and 13,000 tons during the drier period

are currently hauling 10,000 tons. (Bloomberg) -

USDA

Attaché seeks 2020-21 corn imports increasing 18 percent to 12 million tons from 10.2 million year earlier.

-

AGPM,

a French growing group, warned of disappointing French corn crop, at 13.6 million tons, below the AgMin estimate of 13.8 million tons.

-

Germany

ASF: 6 new cases; 86 cases since September 10

Corn

Export Developments

-

Results

awaited: Iran opened a new tender for 200,000 tons of barley, set to close October 21.

Selected

ECB corn basis

Source:

Reuters and FI

Updated

10/15/20

December

corn is seen in a $3.90-$4.20 range

China

could easily change the global balance sheet if they boost corn imports above 15 million tons in 2021.

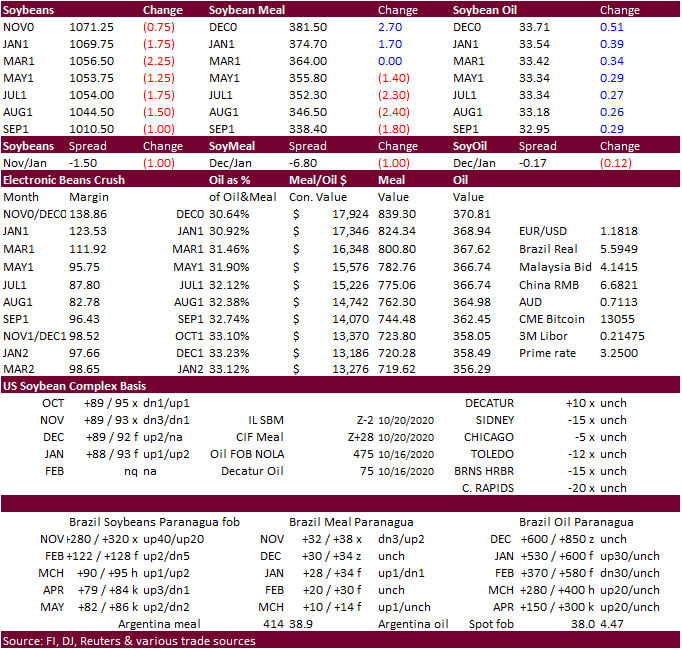

Soybeans

-

Before

settling 1.75 cents higher in November after a large break on the close, soybeans hit a four-year high bias bull spreading on spot US soybean export demand and sharply higher soybean meal. Jan soybeans were up 0.75 and back months all unchanged. December

soybean meal hit a high of $390.80 short ton. The explosion at an Argentina crushing facility firmed Argentina soybean meal basis and in turn supported CBOT soybean meal futures. Also, USDA export sales showed China bought 20,000 tons of US soybean meal.

But traders should not get too excited about the sales. Recall China resumed control over Hong Kong. Over the past five calendar years, US soybean meal exports for combined China and Hong Kong ranged from 23,000 short tons to 43,400 short tons (20,900-35,600

metric tons). If the meal was intended for Hong Kong and/or mainland China, this would not be unusual. Note historically China does not import a large amount of soybean meal, but for some months back in 2010 and 2012, China (only) monthly imports did exceed

40,000 tons and a couple months topped 50,000 tons. -

Traders

are also still trying to access the large China soybean meal physical trade rumored yesterday but no soybean meal sales showed up under the daily USDA sales announcement system.

-

The

soybean crush basis January was up sharply (high 1.2675 vs. 1.1400 yesterday close).

-

Good

soybean oil export sales, strong European vegetable oil markets and higher palm were leading soybean oil higher. December closed 49 points higher. Today we saw an outside day higher in soybeans and soybean oil. Soybean meal reach a new contract high but

settled up $3.60.

·

Soybean export sales of 2.226 million tons were within expectations. China took 1.222 million tons and Egypt for 194,400 tons.

·

Soybean meal sales improved to 321,900 tons from 152,200 tons previous week. China took 20,000 tons.

·

Soybean oil sales were good at 37,000 tons from only 1,400 tons previous week. China took 11,000 tons.

-

We

heard China bought 3-4 US soybean cargoes late Wednesday, with 2 booked out of the Gulf and 1-2 off the PNW. They were inquiring for Q1 Brail shipment.

-

Brazil’s

weather outlook remains unchanged with scattered to good rains occurring across much of the soybean production regions over the next two weeks. Some traders are concerned local areas will see a delay in soybean plantings.

-

StoneX

estimates up to 70 percent of Brazil’s soybean crop will be sold by the time harvest begins in January. They see a 132.6-million-ton crop, up 7 percent from last season.

-

Under

the 24-hour announcement system, private exporters sold the following: -

152,404

tons of soybeans for delivery to Mexico during the 2020/2021 marketing year -

132,000

tons of soybeans for delivery to unknown destinations during the 2020-21 marketing year

-

Syria

seeks 50,000 tons of soybean meal and 50,000 tons of corn on October 26 for delivery within four months of contract.

Updated

10/20/20

November

soybeans are seen in a $10.45-$10.90 range

December

soybean meal is seen in a $350-$3.90 range

December

soybean oil is seen in a 32.70-34.00 range

-

US

wheat

futures

traded lower in all three markets despite a large import tender by Algeria. Technical selling was noted.

-

A

Bloomberg story mentioned one of the reasons for many major high protein wheat importing countries are ramping up wheat imports is because they fear a second wave of a Covid-19 outbreak. We agree.

-

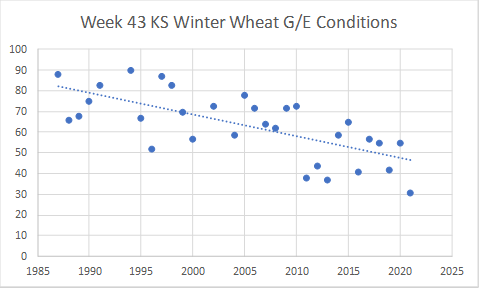

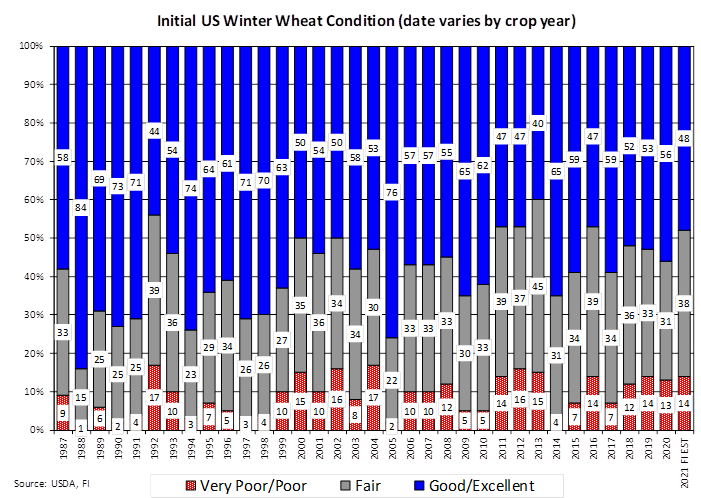

Earlier

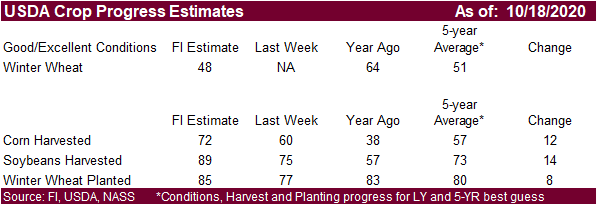

this week we noted the KS rating is at its lowest level since USDA began recording crop conditions for the state. A US rating will be issued on Monday.

-

US

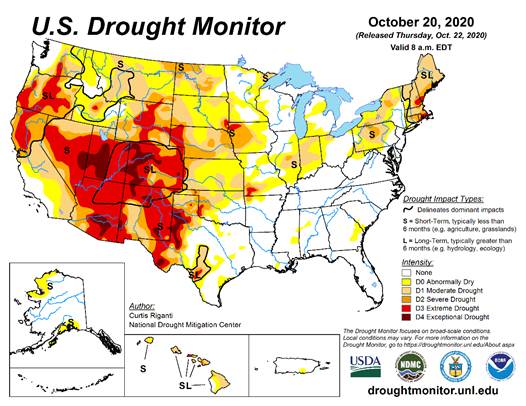

southern Great Plains see restricted precipitation through early November. US Drought Monitor showed 48 percent of the US winter wheat area exposed to drought conditions, up from 41 percent as of October 13 and 26 percent as of September 22.

-

We

look for the initial US winter wheat rating expected to be issued by USDA next week to end up near the lower end of 20-year range led by a multi decade lower combined good/excellent for Kansas at just 31 percent. In 2016 for the 2016-17 crop year, the KS

rating was 41 percent and 2013 (for 2013-14) was 37 percent.

We

estimate the initial US winter wheat rating at 48 percent for the combined good and excellent categories, compared to 64 percent last year and 51 percent average.

-

Argentina’s

BA Grains Exchange looks for wheat production at 16.8 million tons, down from 17.5 million tons last season.

-

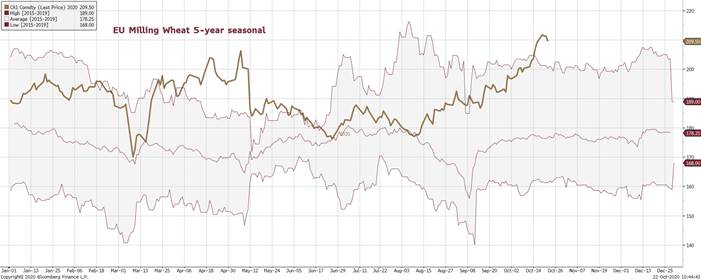

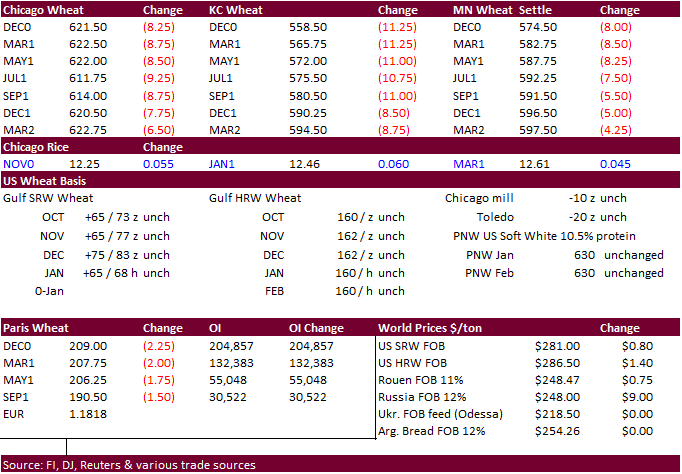

Paris

(Matif) December wheat was down 2.25 at 209.00 euros. -

Yesterday

Turkey removed duties on wheat, barley and corn imports and today they bought at least 50,000 tons of feed barley. Import taxes were 45% for wheat, 35% for barley and 25% for corn.

-

The

EU awarded 57,000 tons of Ukraine wheat import quotas under a tariff-free quota, bringing the season total to about 760,000 tons out of the 1 million tons available for the marketing year.

-

Ukraine

may get a second IMF loan tranche by the end of the year. -

Russia

asked Algeria to further relax on wheat tender specifications. Algeria recently increased its tolerance level for 12.5% protein wheat to 0.5% bug insect damage, but it’s hard for Black Sea shipments to meet the specification.

-

Algeria’s

OAIC bought around 720,000 tons of milling wheat between $275 and $276 a ton, c&f, for November and/or December shipment, depending on origin.

-

Tunisia

bought 50,000 tons of barley for late November through December 15 shipment. They also bought 50,000 tons of milling wheat.

-

Under

the 24-hour announcement system, private exporters sold the following: -

130,000

tons of white wheat for delivery to South Korea during the 2020/2021 marketing year.

-

Turkey

bought 175,000 tons of wheat of various classes for November shipment.

-

Japan

bought 80,526 tons of food wheat later this week including 29,217 tons from the US and 51,309 tons from Canada.

-

Jordan

seeks 120,000 tons of wheat on October 28. -

Jordan

seeks 120,000 tons of feed barley on October 27, optional origin, for LH December through FH March shipment.

-

Taiwan

seeks 88,635 tons of US wheat on October 23 for Dec/Jan shipment.

-

Sudan

seeks 1 million tons of wheat through US assistance.

-

China

plans to buy 500,000 tons of cotton for state reserves.

·

Results awaited: Mauritius seeks 5,500 tons of white rice on October 20 for Dec 15-Mar 15, 2021 delivery.

Updated

10/20/20

December Chicago wheat is seen in a $6.10-6.60 range

December KC wheat is seen in a $5.50-$6.10 range

December MN wheat is seen in a $5.55-$6.20 range

U.S. EXPORT SALES FOR WEEK ENDING 10/15/2020

|

|

CURRENT MARKETING YEAR |

NEXT MARKETING YEAR |

||||||

|

COMMODITY |

NET SALES |

OUTSTANDING SALES |

WEEKLY EXPORTS |

ACCUMULATED EXPORTS |

NET SALES |

OUTSTANDING SALES |

||

|

CURRENT YEAR |

YEAR |

CURRENT YEAR |

YEAR |

|||||

|

|

THOUSAND METRIC TONS |

|||||||

|

WHEAT |

|

|

|

|

|

|

|

|

|

HRW |

157.5 |

1,643.2 |

1,240.1 |

47.6 |

4,144.4 |

4,049.3 |

0.0 |

22.0 |

|

SRW |

89.0 |

403.9 |

616.8 |

3.0 |

879.4 |

1,162.9 |

0.0 |

100.0 |

|

HRS |

55.9 |

1,507.0 |

1,171.8 |

78.9 |

2,904.7 |

2,643.9 |

0.0 |

5.0 |

|

WHITE |

64.8 |

1,452.2 |

916.0 |

62.6 |

1,939.5 |

1,765.8 |

0.0 |

0.0 |

|

DURUM |

0.3 |

220.9 |

204.5 |

0.0 |

321.6 |

312.9 |

0.0 |

0.0 |

|

TOTAL |

367.5 |

5,227.2 |

4,149.2 |

192.1 |

10,189.5 |

9,934.8 |

0.0 |

127.0 |

|

BARLEY |

0.0 |

32.9 |

38.6 |

0.2 |

9.1 |

18.9 |

0.0 |

0.0 |

|

CORN |

1,831.6 |

22,943.7 |

7,729.2 |

898.0 |

5,390.9 |

3,126.8 |

0.0 |

206.0 |

|

SORGHUM |

280.8 |

2,752.5 |

220.2 |

70.1 |

463.5 |

45.9 |

0.0 |

136.0 |

|

SOYBEANS |

2,225.5 |

33,926.3 |

12,096.4 |

2,516.5 |

11,423.2 |

6,164.8 |

0.0 |

60.0 |

|

SOY MEAL |

321.9 |

3,593.0 |

3,084.2 |

90.8 |

348.1 |

642.3 |

0.0 |

18.1 |

|

SOY OIL |

37.0 |

193.7 |

126.9 |

3.1 |

21.5 |

76.3 |

-0.2 |

0.0 |

|

RICE |

|

|

|

|

|

|

|

|

|

L G RGH |

28.4 |

525.2 |

429.3 |

46.8 |

125.6 |

317.2 |

0.0 |

0.0 |

|

M S RGH |

0.0 |

21.3 |

18.8 |

5.2 |

7.6 |

12.0 |

0.0 |

0.0 |

|

L G BRN |

1.1 |

12.0 |

23.2 |

0.4 |

9.4 |

4.5 |

0.0 |

0.0 |

|

M&S BR |

0.1 |

20.6 |

11.5 |

2.5 |

29.0 |

0.9 |

0.0 |

0.0 |

|

L G MLD |

8.4 |

47.8 |

136.7 |

21.9 |

88.5 |

268.5 |

0.0 |

0.0 |

|

M S MLD |

22.9 |

113.5 |

117.9 |

7.8 |

80.0 |

129.9 |

0.0 |

0.0 |

|

TOTAL |

60.9 |

740.4 |

737.5 |

84.6 |

340.1 |

733.1 |

0.0 |

0.0 |

|

COTTON |

|

THOUSAND RUNNING BALES |

||||||

|

UPLAND |

227.8 |

5,761.9 |

7,070.7 |

194.1 |

2,699.1 |

2,205.4 |

21.3 |

520.2 |

|

PIMA |

29.6 |

254.6 |

117.2 |

7.4 |

123.2 |

92.3 |

0.0 |

0.7 |

This

summary is based on reports from exporters for the period October 9-15, 2020.

Wheat: Net

sales of 367,500 metric tons (MT) for 2020/2021 were down 31 percent from the previous week and 23 percent from the prior 4-week average. Increases primarily for Mexico (192,800 MT), Nigeria (60,600 MT), the Philippines (60,000 MT), Guatemala (38,700 MT,

switched from unknown destinations), and Japan (34,600 MT, including decreases of 300 MT), were offset by reductions primarily for unknown destinations (95,500 MT). Exports of 192,100 MT were down 62 percent from the previous week and 67 percent from the

prior 4-week average. The destinations were primarily to Indonesia (55,300 MT), Malaysia (40,800 MT), Japan (33,000 MT), Venezuela (25,100 MT), and Mexico (22,900 MT). Optional Origin Sales: For 2020/2021, the current outstanding balance of 10,000 MT, all

Spain.

Corn:

Net sales of 1,831,600 MT for 2020/2021 were up noticeably from the previous week and up 21 percent from the prior 4-week average. Increases primarily for Japan (490,100 MT, including 162,800 MT switched from unknown destinations and decreases of 10,000 MT),

China (433,500 MT), Mexico (377,400 MT, including decreases of 35,400 MT), Taiwan (179,800 MT), and Israel (157,500 MT), were offset by reductions for unknown destinations (55,500 MT). Exports of 898,000 MT were up 10 percent from the previous week and 7

percent from the prior 4-week average. The destinations were primarily to China (364,000 MT), Mexico (168,300 MT), Japan (165,900 MT), Saudi Arabia (70,200 MT), and Colombia (55,000 MT). Optional Origin Sales: For 2020/2021, new optional origin sales of

30,000 MT were reported for Ukraine. The current outstanding balance of 834,800 MT is for Vietnam (260,000 MT), Taiwan (204,200 MT), Argentina (127,000 MT), Ukraine (125,000 MT), South Korea (65,000 MT), and unknown destinations (53,600 MT). Late Reporting:

For 2020/2021, exports totaling 7,100 MT were reported late. The destination was Jamaica.

Barley:

No net sales were reported for the week. Exports of 200 MT were to South Korea.

Sorghum:

Net sales of 280,800 MT for 2020/2021 resulted in increases for China (195,800 MT) and unknown destinations (85,000 MT). Exports of 70,100 MT were to China.

Rice:

Net

sales of 60,900 MT for 2020/2021 were up noticeably from the previous week, but down 45 percent from the prior 4-week average. Increases primarily for Colombia (21,900 MT), Japan (13,000 MT), Guatemala (10,000 MT), Jordan (4,000 MT), and Saudi Arabia (3,700

MT), were offset by reductions for New Zealand (800 MT). Exports

of 84,600 MT–a marketing-year high–were up noticeably from the previous week and from the prior 4-week average. The destinations were primarily to Mexico (52,300 MT), Haiti (15,200 MT), Saudi Arabia (5,400 MT), Canada (4,900 MT), and South Korea (2,500

MT).

Soybeans:

Net sales of 2,225,500 MT for 2020/2021 were down 14 percent from the previous week and 18 percent from the prior 4-week average. Increases primarily for China (1,222,000 MT, including 395,000 MT switched from unknown destinations and decreases of 6,600 MT),

Egypt (194,400 MT, including 55,000 MT switched from China), unknown destinations (185,100 MT), Germany (111,300 MT), and Mexico (105,700 MT, including decreases of 2,400 MT), were offset by reductions primarily for the Netherlands (20,000 MT). Exports of

2,516,500 MT were up 8 percent from the previous week and 49 percent from the prior 4-week average. The destinations were primarily to China (1,960,200 MT, including 71,400 MT late – see below), Egypt (126,400 MT), Germany (111,300 MT), Mexico (59,700 MT),

and Saudi Arabia (53,800 MT). Optional Origin Sales: For 2020/2021, the current outstanding balance of 126,000 MT, all China.

Exports for Own Account: For 2020/2021, the current exports for own account outstanding balance is 7,300 MT, all Canada. Export Adjustments: Accumulated export of soybeans to the Netherland were adjusted down 56,666 MT for week ending October 1st

and 54,630 MT for week ending October 8th. The correct destination for these shipments is Germany and is included in this week’s report. Late Reporting: For 2020/2021, exports totaling 71,400 MT were reported late. The destination was China.

Soybean

Cake and Meal:

Net sales of 321,900 MT for 2020/2021 primarily for Mexico (127,800 MT, including decreases of 500 MT), the Dominican Republic (36,700 MT, including decreases 200 MT), unknown destinations (32,000 MT), Colombia (31,300 MT), and China (20,000 MT), were offset

by reductions for Belgium (600 MT), Nepal (500 MT), Nicaragua (300 MT), and South Korea (100 MT). Exports of 90,800 MT were primarily to Mexico (35,500 MT), Canada (18,700 MT), Morocco (7,700 MT), Jamaica (6,600 MT), and Costa Rica (5,700 MT).

Soybean

Oil: Net

sales of 37,000 MT for 2020/2021 were primarily for China (11,000 MT), the Dominican Republic (8,600 MT), Venezuela (8,000 MT), South Korea (4,000 MT), and Nicaragua (2,000 MT). For 2021/2022, total net sales reductions of 200 MT were for Canada. Exports

of 3,100 MT were primarily to Mexico (1,600 MT) and Canada (1,500 MT).

Cotton:

Net sales of 227,800 RB for 2020/2021 were up noticeably from the previous week and up 51 percent from the prior 4-week average. Increases primarily for Pakistan (93,300 RB, including 800 RB switched from Indonesia), China (47,500 RB, including decreases

of 10,600 RB), Mexico (33,800 RB), Vietnam (30,100 RB, including 1,100 RB switched from China and decreases of 100 RB), and Bangladesh (9,000 RB), were offset by reductions primarily for Japan (1,000 RB) and Indonesia (800 RB). For 2021/2022, net sales of

21,300 RB were for China (17,200 RB) and Mexico (4,100 RB). Exports of 194,100 RB were up 1 percent from the previous week, but down 7 percent from the prior 4-week average. Exports were primarily to China (95,500 RB), Pakistan (29,100 RB), Vietnam (16,200

RB), Indonesia (12,600 RB), and Bangladesh (12,000 RB). Net sales of Pima totaling 29,600 RB–a marketing-year high–were up 66 percent from the previous week and 53 percent from the prior 4-week average. Increases were primarily for China (9,800 RB), India

(5,700 RB, including decreases of 100 RB), Pakistan (3,900 RB), Bangladesh (3,800 RB), and Turkey (1,300 RB). Exports of 7,400 RB were down 41 percent from the previous week and 43 percent from the prior 4-week average. The destinations were primarily to

India (3,400 RB), Peru (1,800 RB), China (1,100 RB), Bangladesh (600 RB), and Germany (200 RB).

Exports for Own Account: For 2020/2021, new exports for own account totaling 7,400 RB were to China. Decreases were reported for China (300 RB). The current exports for own account outstanding balance of 20,100 RB is for China (15,200 RB), Indonesia

(3,900 RB), and Bangladesh (1,000 RB).

Hides

and Skins:

Net sales of 480,700 pieces for 2020 were up 27 percent from the previous week and 30 percent from the prior 4-week average. Increases primarily for China (407,400 whole cattle hides, including decreases of 10,500 pieces), South Korea (51,000 whole cattle

hides, including decreases of 1,600 pieces), Mexico (48,300 whole cattle hides, including decreases of 500 pieces), Cambodia (5,300 whole cattle hides), and Thailand (3,400 whole cattle hides), were offset by reductions for Taiwan (400 pieces) and Indonesia

(200 pieces). Additionally, total net sales of 2,100 calf skins were reported for Italy. Net sales reductions of 40,100 kip skins were reported for Italy (39,900 kip skins) and Belgium (200 kip skins). Exports of 397,700 pieces reported for 2020 were down

11 percent from the previous week and 13 percent from the prior 4-week average. Whole cattle hides exports were primarily to China (314,300 pieces), South Korea (30,200 pieces), Mexico (30,000 pieces), Brazil (8,000 pieces), and Taiwan (3,500 pieces). In

addition, exports of 2,600 kip skins were to Belgium.

Net

sales of 173,100 wet blues

for 2020 were up 61 percent from the previous week and 15 percent from the prior 4-week average. Increases were primarily for Vietnam (92,800 unsplit, including decreases of 200 unsplit), Italy (53,800 unsplit and 100 grain splits, including decreases of

200 unsplit), China (21,300 unsplit, including decreases of 200 unsplit), Mexico (3,300 unsplit, including decreases of 100 unsplit and grain splits), and India (1,200 unsplit). For 2021, total net sales of 4,000 wet blues unsplit were reported for Vietnam.

Exports of 127,000 wet blues for 2020 were down 1 percent from the previous week and 25 percent from the prior 4-week average. The destinations were primarily to Italy (31,600 unsplit and 4,500 grain splits), China (34,400 unsplit), Vietnam (32,600 unsplit),

Thailand (8,400 unsplit), and Taiwan (7,400 unsplit). Net sales of 1,353,800 splits were for Vietnam (1,302,000 pounds, including decreases of 12,200 pounds) and China (51,800 pounds). For 2021, total net sales of 167,500 splits were for China. Exports

of 492,100 pounds were to Vietnam (449,600 pounds) and China (42,500 pounds).

Beef:

Net sales of 21,700 MT reported for 2020 were up 62 percent from the previous week and 13 percent from the prior 4-week average. Increases primarily for South Korea (5,400 MT, including decreases of 400 MT), China (3,700 MT), Japan (3,600 MT, including decreases

of 600 MT), Mexico (2,800 MT), and Hong Kong (2,600 MT, including decreases of 200 MT), were offset by reductions for Chile (100 MT). For 2021, net sales of 2,600 MT resulting in increases for Japan (1,400 MT) and South Korea (1,300 MT), were offset by reductions

for Hong Kong (200 MT). Exports of 17,800 MT were up 10 percent from the previous week and 6 percent from the prior 4-week average. The destinations were primarily to Japan (4,500 MT), South Korea (4,200 MT), China (2,000 MT), Mexico (1,600 MT), and Hong

Kong (1,500 MT).

Pork:

Net sales of 26,800 MT reported for 2020 were unchanged from the previous week, but down 35 percent from the prior 4-week average. Increases primarily for Mexico (13,800 MT, including decreases of 800 MT), Japan (4,900 MT, including decreases of 200 MT),

China (1,800 MT, including decreases of 1,500 MT), South Korea (1,500 MT, including decreases of 500 MT), and Colombia (1,000 MT), were offset by reductions for Vietnam (100 MT). For 2021, net sales of 800 MT were primarily for New Zealand (400 MT), Australia

(300 MT), and Mexico (100 MT). Exports of 36,600 MT were up 2 percent from the previous week and 4 percent from the prior 4-week average. The destinations were primarily to China (12,500 MT), Mexico (11,100 MT), Japan (4,300 MT), Canada (2,500 MT), and South

Korea (1,500 MT).

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International

One Lincoln Center

18 W 140 Butterfield Rd.

Oakbrook Terrace, Il. 60181

W: 312.604.1366

ICE IM:

treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered

only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making

your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors

should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or

sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy

of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.