PDF Attached

Very

impressive move in the US agriculture markets today. Ags were up sharply with some contracts establishing multi-year highs. Soybean open interest is at a record! Malaysian palm oil appreciated over 3.5 percent, up 97 MRY to 2818, in part to a report that

palm oil prices will be higher amid lower production from La Nina effects.

USDA

announced sales of 154,400 tons of soybeans to unknown for 2020-21 delivery.

US

soybeans hit a record high basis November today. With prices much higher than a year ago, they are still well off from what we saw in drought year 2012.

FEW

CHANGES OF SIGNIFICANCE OVERNIGHT

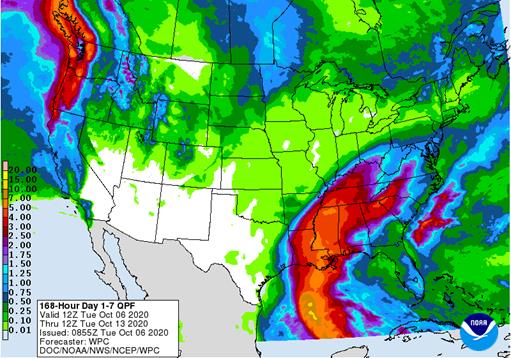

- Hurricane

Delta will have a greater impact on the lower U.S. Mississippi River Basin than previously expected. - Torrential

rainfall is expected from Louisiana to Tennessee from Thursday into Saturday resulting in some flooding, but more importantly causing some crop damage - Sugarcane

in Louisiana will be damaged by high wind speeds unless some aggressive harvesting can occur in the next few days - Cotton

damage is also possible with new crop losses possible because of high wind speeds and heavy rain either blowing or stringing cotton out of open bolls - Losses

will be greatest where boll rot has evolved - Cotton

quality declines are expected - Harvest

delays for all crops in the Delta are expected - Rain

from the storm will move through Kentucky and Tennessee before curving toward the middle Atlantic coastal states later in the weekend and Monday - Tropical

Storm Gamma dissipated over the Yucatan Peninsula overnight, but the storm’s remnants will continue to generate frequent rain and some flooding - Center

west and center south Brazil are advertised drier again at the end of next week and into the following weekend and if that verified it will be a great opportunity for aggressive fieldwork after showers scatter frequently Sunday through mid-week next week - Tropical

Storm Chan-Hom will threaten Japan Friday into the weekend with some heavy rain and potential flooding; the storm may become a weak typhoon as it approaches Japan - Tropical

disturbance near lower Vietnam coast will generate frequent rain through Wednesday as it moves inland through the Central Highlands coffee areas - This

disturbance may reach the Bay of Bengal during the weekend and will contribute to greater rain in India next week - Disturbed

tropical weather in the Philippines will generate greater rainfall over the next several days and a tropical cyclone “may” evolve near the country and move toward Vietnam early next week

BIGGEST

WEATHER ISSUES OF THE DAY

- Russia’s

Southern Region remains too dry with and no significant relief for at least ten days and probably two weeks - Kazakhstan

remains too dry and no relief is expected for two weeks - U.S.

west-central and southwestern hard red winter wheat areas in the Plains will be hot and dry this week and may cool down this weekend into next week - Northwestern

U.S. Plains remain quite dry and winter crops are not establishing well; there is a chance for “some” showers briefly this weekend, but they will be light - No

change in Argentina dryness is expected from central and northern Cordoba and parts of central Santa Fe to northwestern parts of the nation maintaining worry over winter and spring crops - Brazil

heat and dryness will last through Friday and then some relief is expected during the weekend and especially early to mid-week next week in center west and center south crop areas - Drying

may return to center west and center south crop areas at the end of next week and into the following weekend - Western

Australia is still too dry, although some showers will occur in the far south part of the state late Wednesday into Thursday - Queensland,

Australia still needs significant rain for summer crop planting; some rain is possible late next week and more likely in the following weekend - China

will experience a bitter mix of rain and sunshine this week and next week; including the water logged northeast - Central

India will trend wetter again next week after this week’s rain is greatest in the south and far eastern states - South

Africa weather is slowly improving with rain in the south and east - Southeastern

Canada and the U.S. Great Lakes region will experience a better mix of weather over the next week to ten days after frequent precipitation - U.S.

harvest weather in the Midwest and Great Plains will be good through Saturday - Rain

is expected in the northern Plains and upper Midwest late this weekend into early next week - Some

rain from Hurricane Delta may reach into the lower eastern Midwest this weekend causing delays to fieldwork - U.S

Midwest and Great Plains weather next week will be mostly good with only a brief period in which rain is expected to occur in association with frontal systems - U.S.

southeastern states harvest will advance well through mid-week, but late week and weekend weather will deteriorate with rain and scattered thunderstorms expected

- U.S.

Delta faces torrential rain, flooding and strong wind speeds late Thursday through Saturday as Hurricane Delta impacts the region - Rain

totals of 3.00 to 8.00 inches will impact Louisiana, southeastern Arkansas and much of Mississippi with 2.00 to 5.00 inches and locally more in Kentucky and Tennessee - Local

rain totals over 10.00 inches will occur in Louisiana - Wind

speeds will be well over hurricane force in southeastern Louisiana Friday as Hurricane Delta arrives - Wind

speeds of 30 to 50 mph will occur into southwestern Mississippi and northeastern Louisiana while speeds of 20 to 40 mph occur northward into central Mississippi - Drier

weather will occur Sunday into early next week and then a frontal system is expected later next week that may generate additional rain - U.S.

temperatures will trend warmer this week until the late weekend frontal system arrives in the Plains and eventually moves through the Midwest next week - Highs

in the Midwest will rise to the 70s and lower 80s through the weekend with gradual cooling expected next week as a series of cool fronts move through the region - High

temperatures in the Plains will be in the upper 70s and 80s during much of this week with 90s in some southern locations - Cooling

will occur late this weekend and especially next week with a more seasonable range of temperatures expected over time - Cooling

is expected in the Pacific Northwest late this week and during the weekend after several more very warm days through Friday - No

threatening cold nighttime temperatures are expected in any part of the U.S. through the next ten days - Central

and western Ukraine and portions of southeastern Europe will receive waves of rain later this week through most of next week - Sufficient

rain will fall to relieve some of the driest areas from dryness - Rainfall

of 0.75 to 2.50 inches and local totals over 4.00 inches may occur by the end of next week - Temperatures

will be warmer than usual in much of the forecast period - Eastern

Ukraine, like Russia’s Southern Region and Kazakhstan, will get little to no rain for the next ten days and possibly two weeks - Europe

will continue to experience waves of rain over the next two weeks, but the intensity in western areas will be much less than that of this past weekend

- Spain

and Portugal will be driest in this first ten days of the outlook with some areas in the Iberian Peninsula getting rain after Oct. 18. - Temperatures

in western Europe will be near normal while those in the east are warmer than usual - Western

Australia and parts of Queensland will remain too dry - Rain

will fall from eastern South Australia through Victoria and western and southern portions of New South Wales over the next few days and the drier for a while - Temperatures

will be seasonable - India

will experience frequent rain in the east and south over the next week with central areas trending wetter again next week as well - Some

crop maturation and harvest disruption is expected - Northern

India will continue to be mostly dry favoring summer crop maturation and harvest progress and some winter crop planting - Brazil

weather will be dry biased in center west and center south crop areas through Saturday - Scattered

showers develop Sunday and continue daily through the middle part of next week - Daily

rainfall will vary from 0.20 to 0.75 inch with a few 1.00 to 2.00-inch totals - The

greatest rain is expected in Minas Gerais, southern Espirito Santo, Rio de Janeiro and areas south into northeastern Parana - A

few locations in Mato Grosso could also receive a few daily rain totals over 1.00 inch - Improved

soil moisture should support at least some improved topsoil moisture for better soybean and corn planting - Some

improved coffee flowering and pollinating conditions will also occur - Citrus

will flower additionally - Sugarcane

development will become more aggressive as topsoil moisture improves - Some

drier weather is now advertised to return to center west and center south Brazil for the end of next week and into the following weekend - Argentina

rainfall is expected to be limited over the coming week to ten days with rain most likely in Buenos Aires infrequently, but often enough to maintain favorable soil and crop conditions - Crop

moisture stress will continue in the driest areas of Cordoba, Santa Fe, Santiago del Estero, western Chaco and areas northwest to Salta - South

America temperatures will be very warm to hot in center west and center south Brazil this week and then cooler next week - Argentina

temperatures will be seasonable during both weeks - Southeast

Asia rainfall over the next ten days will be erratic, but most areas will be impacted multiple times in the next two weeks supporting most crop needs - Mexico

precipitation will be most significant in the far south of the nation over the coming week to ten days - Central

America will be wetter biased over the next ten days to two weeks further easing long term dryness and possibly delaying early season crop maturation.

- South

Africa will experience erratic rainfall over the next couple of weeks - The

precipitation will begin to improve topsoil moisture for spring planting and winter crop reproduction, but greater rain will still be needed

·

West-central Africa will experience waves of rain through the next ten days favoring coffee, cocoa, sugarcane, rice and other crops

·

East-central Africa rain will be erratic and light over the next couple of weeks, but most of Uganda, southwestern Kenya and portions of Ethiopia will be impacted while Tanzania is mostly dry

·

Philippines rain will be widespread over the next ten days to two weeks maintaining a favorable outlook for crops

·

New Zealand temperatures will be near to below average over the next seven days while precipitation is lighter than usual with the greatest amounts likely along the lower west coast of South Island

-

Southern

Oscillation Index was +9.92 today and it will stay significantly positive through the coming week

TUESDAY,

Oct. 6:

- Purdue

Agriculture Sentiment - New

Zealand global dairy trade auction - HOLIDAY:

China

WEDNESDAY,

Oct. 7:

- EIA

U.S. weekly ethanol inventories, production, 10:30am - HOLIDAY:

China

THURSDAY,

Oct. 8:

- USDA

weekly crop net-export sales for corn, soybeans, wheat, cotton, pork, beef, 8:30am - UN

FAO World Food Price Index - India

SEA-Globoil webinar with Dorab Mistry, Thomas Mielke and James Fry - Brazil’s

Conab releases first report on 2020-21 planted area, output and yield of soy and corn - Port

of Rouen data on French grain exports - EARNINGS:

Suedzucker, Agrana - HOLIDAY:

China

FRIDAY,

Oct. 9:

- USDA’s

WASDE report with world supply/demand crops update, stockpiles noon - ICE

Futures Europe weekly commitments of traders report, 1:30pm (6:30pm London) - CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm - China’s

CNGOIC to publish monthly soy and corn reports - China

agriculture ministry (CASDE) to release its monthly data on supply and demand - FranceAgriMer

weekly update on crop conditions - Brazil

Unica cane crush, sugar production (tentative) - HOLIDAY:

Korea

Macros

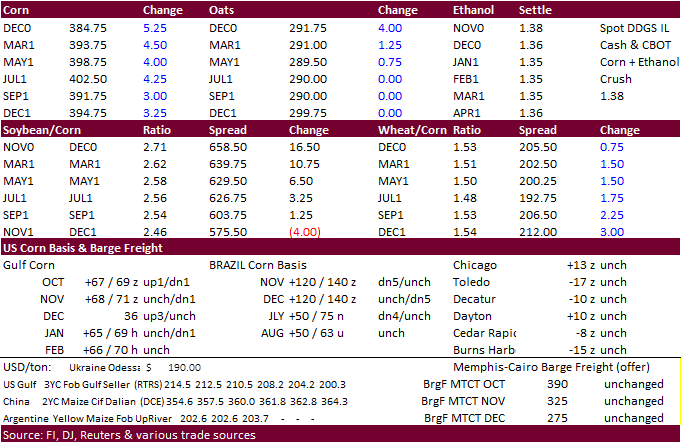

Corn.

-

Macro

trade today supported overall US agriculture futures. WTI was very strong for the second day in a row. The short term energy outlook calls for WTI prices to increase in 2021.

https://www.eia.gov/outlooks/steo/?src=email

-

CBOT

corn traded sharply higher on strength in soybeans and concerns SA plantings (soybeans) are running behind normal for this time of year. December corn was up 5.50 cents and March up 5.00 cents.

-

Nearby

corn hit its highest level since January 2020. -

Funds

bought an estimated net 25,000 contracts. -

Midday

weather outlook showed the GFS model making a slight westward shift to Hurricane Delta and the storm moves from south-central Louisiana early Saturday into northern Mississippi by Saturday night with a larger part of the northern Delta to western and central

Kentucky seeing heavy rain. -

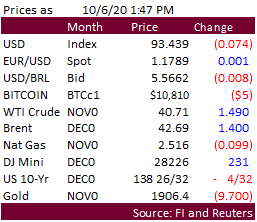

USD

was 5 lower as of 1: 30 pm CT. -

Germany

ASF: 49 cases since September 10 -

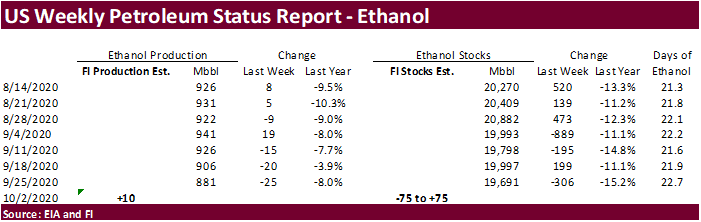

RFA:

U.S. ethanol exports in August increased 35% to 100.7 million gallons, largest volume since March. Canada remained the largest customer. India slowed imports and Brazil returned to pick up a small amount. US DDGS exports in August fell 6 percent to 1.02

million tons. -

US

corn exports during August were 4.539 million tons vs, 2.793MMT year earlier. Mexico and China were the largest takers.

Corn

Export Developments

-

Syria

seeks 50,000 tons of soybean meal and 50,000 tons of corn on October 26 for delivery within four months of contract.

DJ

U.S. August Grain Exports-Oct 6

In

kilograms (top) and in bushels (bottom), except flour in cwt and malt

in

pounds. /1 denotes includes commercial and donated. Source: U.S. Department

of

Commerce.

——-

In Kilograms ——-

Aug

20 Jul 20 Jun 20 Aug 19

Barley

788,000 6,180,000 2,047,000 3,755,000

Corn

/1 4,539,144,000 4,343,711,000 5,035,249,000 2,825,045,000

Sorghum

525,291,000 361,560,000 576,822,000 312,340,000

Oats

3,054,087 3,309,254 1,926,717 1,437,887

Rye

507,707 1,543,800 885,579 1,220,900

Wheat

/1 2,576,550,118 2,367,853,459 2,283,170,928 2,571,064,128

wheat

flour /1 24,621,402 22,946,849 23,776,786 25,214,831

Malt

28,205,171 22,830,290 18,055,175 29,265,120

——-

In Bushels, CWT or Pounds ——-

Aug

20 Jul 20 Jun 20 Aug 19

Barley

36,192 283,842 94,017 172,464

Corn

/1 178,696,372 171,002,593 198,226,963 111,215,968

Sorghum

20,679,581 14,233,842 22,708,246 12,296,156

Oats

210,408 227,987 132,739 99,061

Rye

19,987 60,776 34,863 48,064

Wheat

/1 94,671,039 87,002,828 83,891,310 94,469,465

wheat

flour /1 542,809 505,891 524,188 555,892

Malt

62,181,769 50,332,182 39,804,854 64,518,557

1/Includes

commercial and donated.

Updated

9/30/20

-

December

corn is seen in a $3.60-$4.00 range. 2020-21 to average $3.75 for corn and $2.85 for oats.