PDF Attached

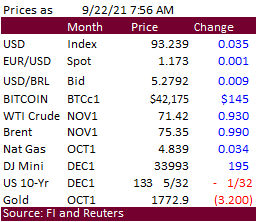

WTI crude oil is $0.97 higher, USD 4 points higher and Dow futures higher. FOMC meeting starts later today.

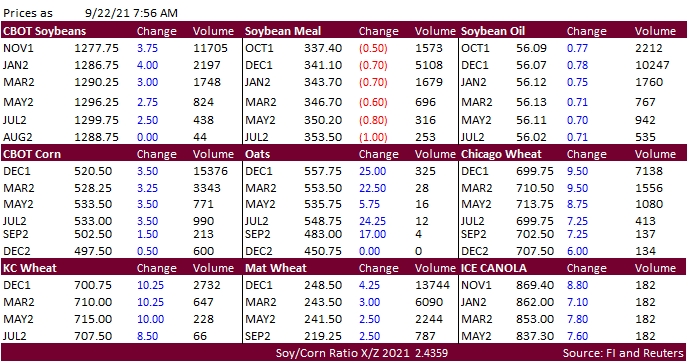

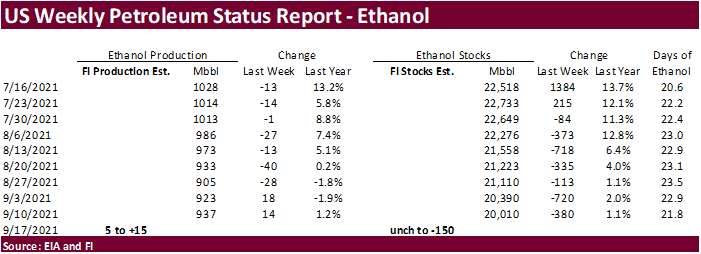

No 24-hour USDA sales. We are hearing US biofuel blending proposals will be out on Friday. Soybeans are higher after China returned from holiday and overnight there was talk of soybean interest. Soybean oil is higher after palm oil rallied. Corn and wheat are higher, looking to end a four-day losing streak. Outside markets are lending support. US weather looks favorable over the next two weeks. Weekly EIA ethanol production and stocks will be out later this morning.

7-day

WORLD WEATHER HIGHLIGHTS FOR SEPTEMBER 22, 2021

- U.S. hard red winter wheat areas were advertised to get significant rain during the middle and latter parts of next week in some of the model forecast runs Tuesday and early today, but this precipitation was overdone and future model runs will back off of the potential.

- The region will get some showers, but no big soaking.

- Eastern Australia reported some frost again today, but mostly in and near the Great Dividing Range in New South Wales resulting in no significant crop impact.

- There is still need for rain in much of the nation, but especially Queensland.

- South America’s forecast did not change much overnight maintaining a restricted rainfall pattern for Argentina and slowly increasing shower activity in parts of Brazil.

- Russia’s recent rain has proven beneficial for wheat areas that were too dry previously and some additional rain is still expected in the drier areas.

- China has taken a short term break from rain, but will get too much in the Yellow River Basin and North China Plain during the coming week raising some concern over field working delays.

- A tropical disturbance in the eastern part of the South China Sea will become better organized and will move through central Vietnam to Thailand producing widespread rain in both of those countries and both Laos and northeastern Cambodia possibly inducing local flooding

- Another tropical cyclone will evolve near Guam over the next few days, but it will turn away from the eastern Asian Nations while intensifying during the coming week

- Dryness and warmer than usual conditions will continue in Canada’s Prairies and the northern U.S. Plains as well as much of the interior western U.S.

- Europe weather will be favorably mixed

- Northern Algeria received some significant rain Tuesday and early today, but that comes too early in the season to be of much use to planting of winter crops

- India’s monsoon continues to show little sign of withdrawing, although the far north will see more sporadic rainfall for a while

Source: World Weather Inc.

Wednesday, Sept. 22:

- EIA weekly U.S. ethanol inventories, production

- U.S. cold storage data – pork, beef, poultry, 3pm

- HOLIDAY: Hong Kong, Korea

Thursday, Sept. 23:

- USDA weekly crop net-export sales for corn, soybeans, wheat, cotton, pork, beef, 8:30am

- Globoil India – international vegetable oil conference, day 1

- The UN Food Systems Summit

- USDA red meat production, 3pm

- Port of Rouen data on French grain exports

- HOLIDAY: Japan

Friday, Sept. 24:

- ICE Futures Europe weekly commitments of traders report (6:30pm London)

- CFTC commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm

- Globoil India – international vegetable oil conference, day 2

- FranceAgriMer weekly update on crop conditions

- U.S. cattle on feed, hogs and pigs inventory, poultry slaughter, 3pm

Saturday, Sept. 25:

- Globoil India – international vegetable oil conference, day 3

Source: Bloomberg and FI

Macros

US MBA Mortgage Applications Sep 17: 4.9% (prev 0.3%)

· Corn is higher on commercial and fund buying after the December contract hit a one-week low. Outside markets are lending support. Oats are limit up. https://www.cmegroup.com/trading/price-limits.html

· There is already talk of US acreage decisions for 2022 and latest word was producers plan to slightly scale back on corn plantings due to high fertilizer prices. Meanwhile spot fertilizer is expensive and, in some areas, hard to find for winter wheat producers after imports of the key ingredients dropped amid hurricane Ida logistical problems.

· US ethanol margins look good. Weekly EIA ethanol production and stocks will be out later this morning. A Bloomberg poll looks for weekly US ethanol production to be up 4,000 barrels (923-955 range) from the previous week and stocks up 4,000 barrels to 20.014 million.

· Vietnam plans to reduce tariffs on US ethanol and corn. They will meet with the US Grains Council today to discuss.

· Haiti reported an outbreak of African swine fever. Dominican Republic reported an outbreak last July, which borders Haiti.

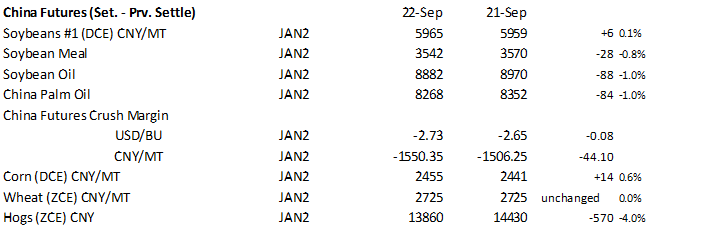

· China hog futures made new contract lows today. Jan settlements below.

· Cattle on feed and the hogs & pigs reports will be released after the close on Friday.

Export developments.

- None reported

· Soybeans are higher after China returned from holiday and overnight there was talk of soybean interest. However, no 24-hour sales were reported.

· We are hearing US biofuel blending proposals will be out on Friday.

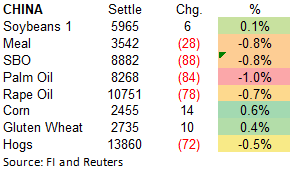

· Meal is on the defensive. Soybean oil is higher after palm oil rallied. China soybean futures were moderately higher, meal down 0.8% and soybean oil and palm slipped 1%.

· Argentine producers sold 30 million tons of soybeans from the 2020-21 crop through mid-September, up 650,200 tons from the previous week. Last year they were 31.6 million tons through Sept. 15.BA Grans Exchange is using a 43.1-million-ton production, compared with 49 million tons in 2019-20 (40.4MMT sold). They look for new-crop 2021-22 production to be around 44 million tons.

· Germany plans to phase out palm oil as a feedstock for biodiesel production from 2023. They are a minor player when it comes to this feedstock (about 4% palm, rapeseed is 60%).

· Globoil India edible oil conference will run from Thursday to Saturday. Look for direction for price projections for various vegetable oil.

· The Malaysian Palm Oil Association estimated palm production during Sept. 1-20 fell 0.55% from the same week in August.

· Malaysian palm oil futures were up 138 ringgit at 4,330. Cash palm was up $22.50/ton to $1,122.50/ton.

· Offshore values are leading soybean oil 47 points higher and meal $2.70/short ton lower.

· China cash crush margins were last positive 161 cents on our analysis (162 previous) versus 162 cents late last week and 92 cents around a year ago.

· Malaysia:

Export Developments

- Egypt’s GASC is seeing offers for 30,000 tons of soyoil and 10,000 tons of sunflower oil for arrival Nov. 15-30 and/or Dec. 1-15. Lowest offer for soyoil was $1,340 a ton c&f. Lowest offer for sunflower oil was $1,289 a ton c&f.

· Wheat futures are on track to snap a four-day losing streak.

· US weather looks favorable over the next two weeks.

· December Paris wheat was down 0.25 at 245 euros.

· The USD was 17 points lower as of 7:50 am CT.

Export Developments.

· The Philippines bought an estimated 112,000 tons of feed wheat. Two 56,000-ton consignments for shipment in December 2021 and January 2022 were bought near $350/ton c&f and thought to originate from Australia.

· Pakistan seeks 640,000 tons of wheat on Sep. 29 for shipment between January and February 2022.

· Pakistan’s lowest offer for 500,000 tons of wheat was $383.50/ton c&f.

· Jordan passed on 120,000 tons of wheat for LH December through FH February shipment.

· Yesterday Morocco received no offers for 363,000 tons of US wheat for arrival by the end of the year.

· Results awaited: Algeria seeks 50,000 tons of durum wheat on September 22 for November shipment.

· Results awaited: Mauritius seeks 47,000 tons of wheat flour, optional origin, on Sept. 21 for various 2022 shipment.

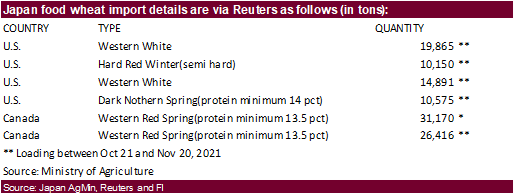

· Japan seeks 113,067 tons of food wheat from the US and Canada, this week for October 21-November 20 loading.

· Jordan seeks 120,000 tons of feed barley on September 23 for Dec. 16-31, Jan. 1-15, Jan. 16-31, and Feb. 1-14.

- Taiwan seeks 49,580 tons of US wheat on September 23 between November 6 and November 20.

Rice/Other

· Bangladesh seeks 50,000 tons of rice on September 23.

· Bangladesh seeks 50,000 tons of rice on October 4.

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International

One Lincoln Center

18 W 140 Butterfield Rd.

Oakbrook Terrace, Il. 60181

W: 312.604.1366

ICE IM: treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.