PDF Attached

The

U.S. Supreme Court ruled 6-3 in favor for small oil refineries seeking biofuel mandate exemptions. Weather was also a bearish factor for soybeans and corn. Dry weather for US spring wheat supported Minneapolis and KC & Chicago SRW wheat traded lower on weakness

in corn & soy.

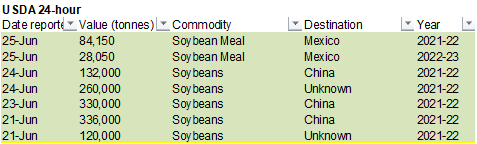

WASHINGTON,

June 25, 2021—Private exporters reported to the U.S. Department of Agriculture export sales of 112,200 metric tons (USDA posted 122,200) of soybean cake and meal for delivery to Mexico. Of the total, 84,150 metric tons is for delivery during the 2021/2022

marketing year and 28,050 metric tons is for delivery during the 2022/2023 marketing year.

1-7

DAY

WORLD

WEATHER INC.

MOST

IMPORTANT WEATHER OF THE DAY

- Kazakhstan

will experience five to seven days of dry and hot weather further stressing its spring wheat and sunseed crops

o

Similar conditions will occur north of the border in the southwestern portions of Russia’s eastern New Lands

o

Unirrigated yield potentials have already been drifting lower because of dryness this year

- Dryland

crops will be more seriously stressed over the coming week raising worry over greater production cuts

o

Some showers and cooling will occur in the July 2-8 period, although no general soaking is expected

- Russia’s

Southern Region will experience less oppressive heat in the coming week and a chance for “some” showers

o

The region has been very warm to hot and dry this week

o

Only partial relief is expected to unirrigated crops in the region

o

Subsoil moisture has carried most crops through the stressful period relatively well except in areas near the Caspian Sea and lower Volga River Valley where dryness was most significant

- Rain

will be returning to western Russia, Belarus, the Baltic States and parts of Ukraine in this coming week after a period of drier and warmer weather recently

o

Crops benefited from the drier and warmer weather and now that timely rain is returning the situation should prove quite favorable for production

- Western

portions of Europe’s Balkan Region have been drying out and heating up recently

o

Rain is needed and only a scattering of showers and thunderstorms will evolve in the coming week

- The

region impacted is small and unlikely to expand much in the coming week, but greater rain is needed - Other

areas in Europe are expecting a continuation of mostly favorable weather

o

Recent rain in the west and north-central parts of the continent have brought relief from recent drying and warm weather

- India’s

first week of weather is not likely to change much with below average precipitation in the interior west, far south and across most of the north

o

Week two weather will trend wetter in portions of the south and interior west while Rajasthan, Punjab and Haryana continue quite dry

o

Gujarat will experience a net drying bias after welcome rain fell this week

- Thailand,

Cambodia and Vietnam will continue drier biased in this first week of the outlook with Vietnam getting greater rain July 2-8

o

Thailand, corn, rice, sugarcane and other crops will need greater rainfall soon and the next two weeks will only generate light amounts of rain

- Australia

weather will be favorable during the next two weeks with periodic showers and mild temperatures supporting winter crop emergence and establishment as well as some additional late season planting - Argentina

temperatures will turn much colder this weekend into early next week

o

Freezes will occur in much of the nation, but winter crops are not likely to be damaged

o

Unharvested summer crops will also not be impacted by the cold

o

Some rain will fall erratically before the cold air settles in, but more is still desired for some western wheat areas

o

Wheat is in much better shape this year than last year at this time

- Southern

Brazil will also trend colder next week

o

Frost and freezes are expected from the grain areas of Parana into northeastern Rio Grande do Sul

- Most

crops are not likely to be impacted by frost or freezes, but some of the wheat is in the pre-reproductive stage of development and could be harmed if temperatures get too cold

o

No damaging frost or freeze is expected in sugarcane, coffee or citrus areas, although it will get cooler

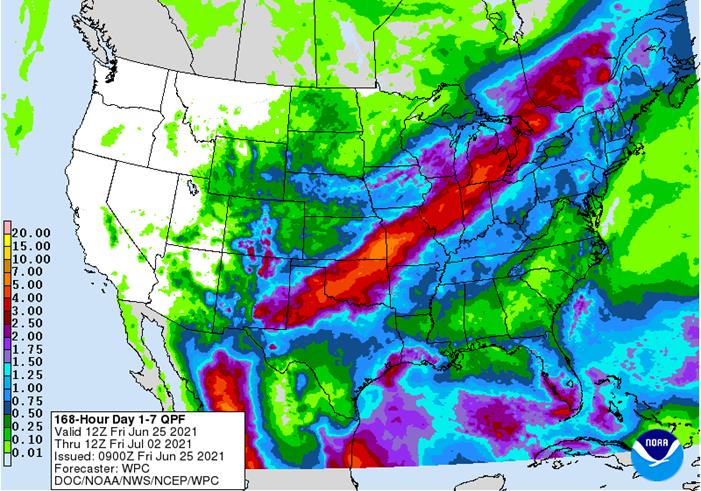

- U.S.

crop areas will be plenty wet from West Texas through Kansas and Missouri to Michigan; including Illinois, southeastern Iowa, Missouri and Indiana

o

Some flooding is expected in the coming week, although crop damage should be limited to small areas that are in low-lying regions

- West

Texas corn, cotton, sorghum and peanuts will benefit greatly from the rain and crop stress will be eased

o

Some excessive rain is possible – mostly in the Low Plains and Rolling Plains

- Northeastern

U.S. Plains, far northwestern U.S. Corn Belt and eastern Canada’s Prairies will continue drier than usual, but conditions should not deteriorate much in this coming week

- Excessive

heat from the U.S. Pacific Northwest and British Columbia east into Alberta, Saskatchewan and Montana in this coming week will have a negative impact on crops and livestock inducing some significant stress

o

Southern Alberta, Montana and the unirrigated crops in central Washington will be most impacted in a negative manner

o

Milk production will be cut

o

Livestock weight gains will be reduced

o

Irrigated crops will still be stressed by the excessive heat, but water will be applied to prevent serious crop distress

- A

good balance of weather is expected in the U.S. Delta and southeastern States during the next ten days to two weeks - Monsoonal

rainfall will begin to reach into the southwestern United States during the coming week to ten days and that moisture feed will prove to be very important for the Rocky Mountain region and Great Plains during July

- Southeastern

Canada corn, soybean and wheat conditions are rated mostly good, although a greater boost in rainfall might be welcome at some point into time over the next few weeks.

o

Some of that precipitation need is expected over the coming week as rain from the U.S. Midwest streams into the region

- China

drying is most likely from Jiangsu to Shaanxi and Shanxi during the next week and then relief is expected with scattered showers and thunderstorms

o

Subsoil moisture will carry on relatively normal crop development for a while

o

A good mix of rain and sunshine is likely elsewhere in east-central and northeastern China for the next couple of weeks

o

Far southern China may continue a little wetter than desired and some sunshine and warm weather is needed

- Western

Xinjiang, China weather has improved recently with warmer temperatures and less rain

o

Northeastern Xinjiang has turned much cooler than usual again and periods of showers and thunderstorms are expected through the weekend and into early next week keeping temperatures below average

o

Weather conditions will improve in northeastern Xinjiang later next week

o

Western Xinjiang weather is expected to be more favorable on a consistent basis, although temperatures may not be quite as warm as usual

- Southeast

Asia rainfall continues lighter and more sporadic than usual in the mainland crop areas and this week’s weather will not likely change much

o

Indonesia and Malaysia rainfall are expected to be sufficient to maintain or improve soil moisture for all crops

o

Philippines rainfall will be near to below average for at least the next ten days

- Some

areas may experience net drying

o

Western and southern Thailand (north of the Malay Peninsula) will be driest into next week along with some Vietnam locations

- West

Africa rainfall in Ivory Coast and Ghana will be near to above average during the coming ten days

o

Nigeria and Cameroon will see a mix of precipitation during the next ten days with most crops benefiting well from the pattern

- A

part of Nigeria will receive less than usual rainfall during this period, but timely rain is still expected - Erratic

rainfall has been and will continue to fall from Uganda and Kenya into parts of Ethiopia

o

A boost in precipitation is needed

- Ethiopia

rainfall is expected to gradually improve while a boost in precipitation will continue needed in other areas - South

Africa was dry Thursday except for a few random showers in the south

o

Showers will increase in the far southwest the remainder into the weekend

- The

moisture will be good for winter crops, but more moisture will be needed in Free State and other eastern wheat production areas

o

Summer crop harvesting has advanced well this year and the planting of winter grains has also gone well, but there is need for moisture in eastern winter crop areas

- North

Africa will experience net drying for the next ten days which will be ideal in supporting winter crop harvest and other late season farming activities - Mexico

rainfall will continue in southern parts of the nation over the coming week while some rain expands into the interior far west

o

Rain should increase and advance to the north during the June 27-July 4 period, but it will be erratic

- Nicaragua

and Honduras have received some welcome rain recently, but moisture deficits are continuing in some areas

o

Additional improvement is needed and may come slowly

- Southern

Oscillation Index is mostly neutral at -1.62 and the index is expected to trend higher over the coming week - New

Zealand rainfall during the coming week to ten days will be a little lighter than usual in eastern South Island and near to above normal in the west while a good mix of rain and sunshine occur in North Island

o

Temperatures will be near to above average

Source:

World Weather, Inc.

Bloomberg

Ag Calendar

Monday,

June 28:

- USDA

export inspections – corn, soybeans, wheat, 11am - U.S.

crop conditions — corn, cotton, soybeans, wheat, 4pm - EU

weekly grain, oilseed import and export data - Ivory

Coast cocoa arrivals

Tuesday,

June 29:

- Canada

Statcan data on seeded area for wheat, durum, canola, barley and soybeans - South

Africa updates corn production

Wednesday,

June 30:

- EIA

weekly U.S. ethanol inventories, production - U.S.

acreage data for corn, wheat, soybeans and cotton; quarterly grain stockpiles - Bloomberg

New Economy Catalyst; climate and agriculture - Malaysia

June 1-30 palm oil export data - U.S.

agricultural prices paid, received

Thursday,

July 1:

- USDA

weekly crop net-export sales for corn, soybeans, wheat, cotton, pork, beef, 8:30am - World

cotton outlook update from International Cotton Advisory Committee - Costa

Rica, Honduras monthly coffee exports - U.S.

corn for ethanol, DDGS production, 3pm - USDA

soybean crush, 3pm - Port

of Rouen data on French grain exports - Australia

Commodity Index - AB

Sugar trading update - HOLIDAY:

Canada, Hong Kong

Friday,

July 2:

- ICE

Futures Europe weekly commitments of traders report (6:30pm London) - CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm - FranceAgriMer

weekly update on crop conditions

Source:

Bloomberg and FI

CFTC

Commitment of Traders

Funds

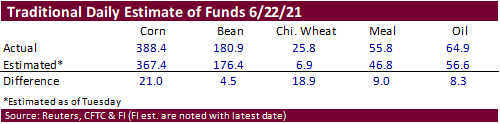

as of last Tuesday for the traditional positions were more net long than expected, especially for Chicago wheat. We don’t see any price influence from this week’s report. One thing did stock out, the net positions for managed money positions fir futures

only and futures and options combined were very close for all the major CBOT agriculture commodities we follow.

What

we think positions are as of Friday afternoon…

SUPPLEMENTAL

Non-Comm Indexes Comm

Net Chg Net Chg Net Chg

Corn

197,517 -15,497 426,987 -5,773 -570,503 35,513

Soybeans

29,702 -31,940 168,608 -15,473 -182,963 53,446

Soyoil

24,647 -15,782 120,152 -1,888 -151,725 25,944

CBOT

wheat -35,326 9,560 159,814 -749 -113,369 -5,934

KCBT

wheat 2,604 660 60,016 -2,211 -57,903 1,257

=================================================================================

FUTURES

+ OPTS Managed Swaps Producer

Net Chg Net Chg Net Chg

Corn

243,465 -9,267 240,373 927 -536,530 31,156

Soybeans

80,304 -27,189 78,973 -7,777 -156,685 51,440

Soymeal

20,132 1,041 89,790 1,982 -155,403 -619

Soyoil

52,152 -15,075 117,290 -851 -177,146 23,933

CBOT

wheat 3,015 11,412 73,212 -3,550 -83,663 -5,826

KCBT

wheat 14,852 -2,635 43,086 2 -52,107 799

MGEX

wheat 10,867 -4,431 3,827 526 -27,723 185

———- ———- ———- ———- ———- ———-

Total

wheat 28,734 4,346 120,125 -3,022 -163,493 -4,842

Live

cattle 69,015 5,444 84,697 -1,508 -165,581 -4,543

Feeder

cattle 6,190 1,812 6,711 -45 -2,140 -891

Lean

hogs 75,716 -10,786 63,713 -55 -141,721 13,964

Other NonReport Open

Net Chg Net Chg Interest Chg

Corn

106,696 -8,573 -54,002 -14,243 2,414,293 -124,582

Soybeans

12,754 -10,442 -15,348 -6,032 1,145,008 -20,959

Soymeal

20,185 -1,136 25,295 -1,267 464,731 -4,015

Soyoil

778 267 6,925 -8,275 631,820 -30,566

CBOT

wheat 18,554 841 -11,119 -2,877 497,031 -35,482

KCBT

wheat -1,114 1,540 -4,717 293 218,576 -3,969

MGEX

wheat 1,396 267 11,634 3,453 86,698 -1,361

———- ———- ———- ———- ———- ———-

Total

wheat 18,836 2,648 -4,202 869 802,305 -40,812

Live

cattle 25,225 823 -13,356 -215 345,156 3,665

Feeder

cattle 2,679 655 -13,440 -1,531 50,496 1,051

Lean

hogs 13,282 -1,920 -10,990 -1,202 351,619 -38,132

=================================================================================

Macros

US

Univ. Of Michigan Sentiment Jun F: 85.5 (est 86.5; prev 86.4)

–

Current Conditions: 88.6 (est 92.0; prev 90.6)

–

Expectations: 83.5 (est 83.8; prev 83.8)

–

1-Year Inflation: 4.2% (est 4.1%; prev 4.0%)

–

5-10 Year Inflation: 2.8% (prev 2.8%)

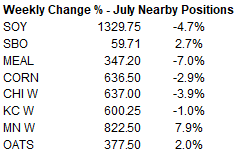

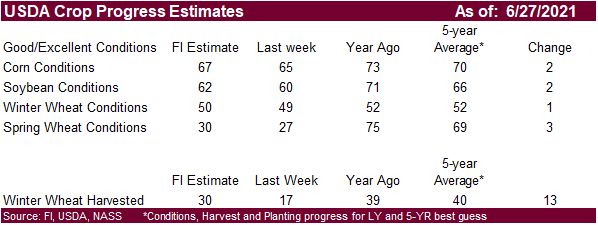

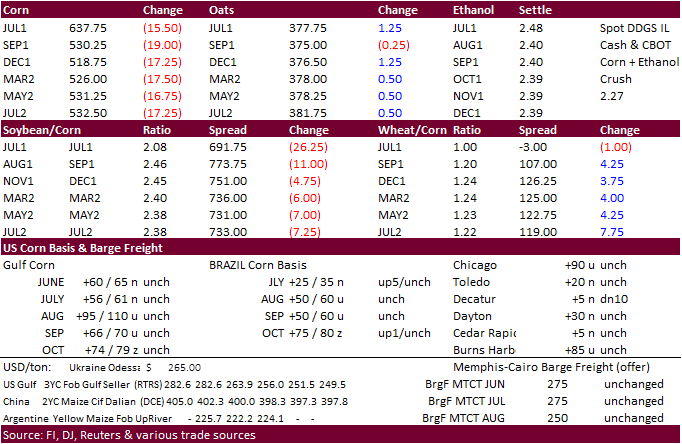

- US

corn futures traded 16.75-19.00 cents lower on lower RIN prices and improving US Midwest weather with rain encompassing much of the dry areas of the western Corn Belt. There is talk Missouri will get too much rain by the time this rain event ends. Meanwhile

CBOT losses could be limited after Brazil earlier this week saw frost conditions leading to private groups making further downward adjustments to the total corn crop. Yesterday Agroconsult lowered their Brazil second corn crop to 65.3 million tons versus

66.2 in May. - Ethanol

RINs fell as much as 27% to $1.25, which was last week’s low (RVO headline). But it rebounded to around $1.49 as of midday, about 16 cents off yesterday’s price.

- Funds

sold an estimated net 20,000 corn. - We

heard this morning China was in for corn late this week, but there were no flash announcements on Friday. USDA export sales may improve next week reflecting the break in the market last week.

- US

corn conditions could be up 2 points when reported Monday afternoon. - On

June 29, South Africa’s CEC will update their corn production and a Reuters trade average for the 2020-21 crop is estimated at 16.352 million tons, up from 16.180 million previous and compares to 15.300 million tons last season. That consists of around 9.110

million tons of white and 7.247 million tons of yellow. - China

hog futures traded over 5 percent higher on Friday on tighter spot supplies for slaughter. Live hog futures prices were up 5.3% at 18,925 yuan ($2,932.84) per ton at the close.

- French

corn ratings dropped 1 point to 89% as of June 21. - A

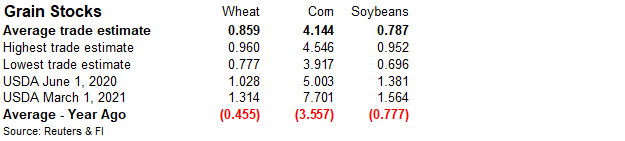

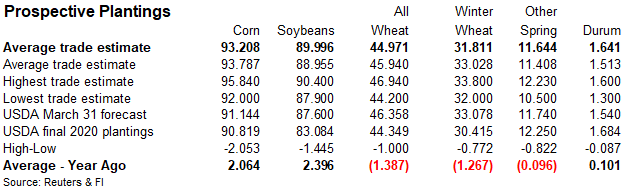

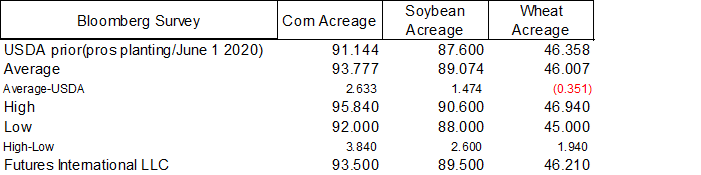

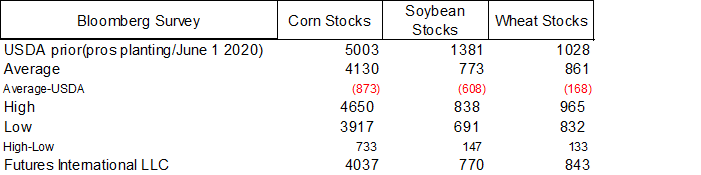

Bloomberg survey calls for the corn area to increase 2.6 million acres to 93.8 million. Stocks as of June 1 were estimated 4.130 billion bushels, below 5.003 billion a year ago.

Export

developments.

Cattle

on Feed

showed June 1 inventories slightly below expectations and placements below an average trade guess.

Export

developments.

- China’s

Sinograin plans to auction off 18,207 tons of imported Ukraine corn on June 25.

Updated

6/25/21

September

$4.50 and $6.00 (lowered 50 & 75 from previous)

December

corn is seen in a $4.25-$6.00 range. (lowered 50 cents)

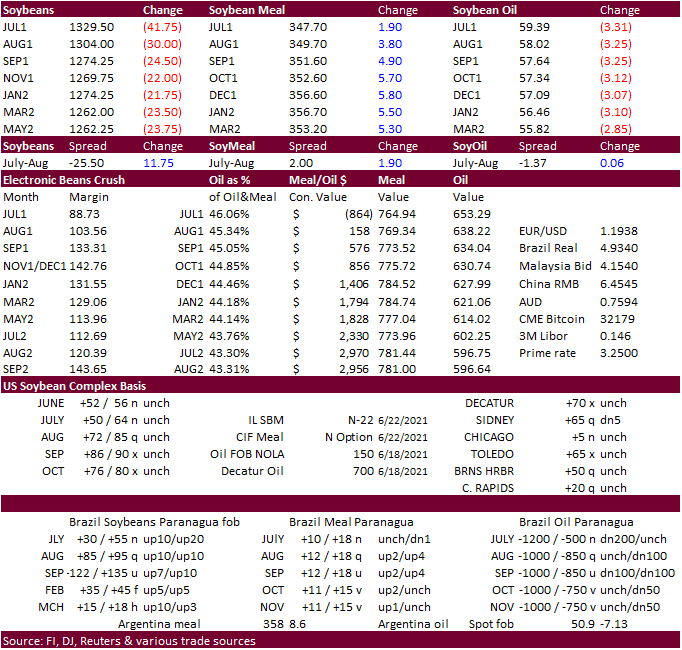

Soybeans

-

The

soybean complex was mixed to start. Soybean oil was higher early, lifting soybeans higher, but with favorable US weather in play and sharply lower SBO, soybean prices fell. Meal reversed to trade higher on unwinding of oil/meal spreads. July soybeans dropped

around 10 cents late in the session to end 41.50 cents lower. November was off 22 cents. August soybeans dropped 21.25 cents, August meal up $3.00 and August soybean oil down 307 points.

-

Several

opinions and questions emerged throughout the day on the Supreme Court decision. Did the best I can to try to summarize the issue/opinions below.

-

The

limit lower move in soybean oil this morning was likely overdone. It traded sharply lower after the U.S. Supreme Court at 9:10 am CT ruled 6-3 in favor for small oil refineries seeking biofuel mandate exemptions. It means less RIN’s required for the small

refiners and thus less feedstock needed to produce the fuel. The decision should not apply to all small refiners, and we are uncertain what constitutes a small refiner (hearing around 75-million-gallon capacity). Remember the law allows the EPA Administrator

to decide on individual waivers on recommendations from the DOE. Going forward, we look for the EPA to continue granting waivers, perhaps amounting less than what were granted during the Trump administration. So, in our view not much has changed, and if the

product is economical, it will be produced and blended. The next biofuel major announcement may come from the pro green energy Biden Administration. We made no changes to our US soybean oil balance sheet. In the end look for soybean oil price direction to

eventually revert to tracking mineral oil prices. https://www.supremecourt.gov/opinions/20pdf/20-472_0pm1.pdf

-

Bearish

long term? Some think the court ruling overturning the 10th circuit was 1) a surprise as the market was leaning towards the Supreme Court siding with the 10th, 2) about ½ billion RINs, at least, that were thought to be replaced going

all the way back to 2016 (may have already, we don’t know), 3) it now becomes difficult for Biden Administration to legally argue for fewer SRE’s per year (2020 SRE’s awarded waivers were absorbed by large refiners), and 4) some now believe the soon to be

released proposed RVO could be unchanged for 2021 & 2022. If the latter is realized, then we may see 1 to 1.5 billion of RIN generation (new plants) coming online over the next one to two years with no change in blend rates. Think of current gasoline demand-down

roughly 10 percent from 2019 level. We will not know the degree of bearishness until the proposals are released. Look for a volatile RIN market over the short term. Going forward, we will keep in mind looking at the RVO as a percentage for blend, not as

a flat number such as the 15 billion gallon ethanol mandate. -

Funds

sold an estimated net 16,000 soybean contracts, bought 2,000 soybean meal and sold 15,000 soybean oil contracts.

-

Note

CBOT SBO registrations declined 50 to only 718 (Emmetsburg, IA). Traders will be monitoring Supreme Court opinions later this morning, looking for arguments over biofuel waivers. Expect RIN prices to remain influential on soybean oil prices.

https://www.supremecourt.gov/opinions/slipopinion/20

-

USDA

announced Friday morning sales of 122,200 tons of soybean meal to Mexico, 84,150 tons for 2021-22 and 28,050 tons for 2022-23.

-

ICE

Canola fell 2.10. -

A

Bloomberg survey calls for the US soybean area to increase 1.5 million acres to 89.1 million. Stocks as of June 1 were estimated 0.773 billion bushels, below 1.381 billion a year ago.

-

Cargo

surveyor SGS reported month to date June 25 Malaysian palm exports at 1,167,989 tons, 81,313 tons above the same period a month ago or up 7.5%, and 248,762 tons below the same period a year ago or down 17.6%. ITS reported a 2.4 percent increase to 1,142,480

tons. AmSpec reported a 6 percent increase to 1,174,350 tons.

- WASHINGTON,

June 25, 2021—Private exporters reported to the U.S. Department of Agriculture export sales of 112,200 metric tons of soybean cake and meal for delivery to Mexico. Of the total, 84,150 metric tons is for delivery during the 2021/2022 marketing year and 28,050

metric tons is for delivery during the 2022/2023 marketing year.

Updated

6/25/21

August

soybeans are seen in a $12.15-$14.50 range; November $11.50-$14.75

August

soybean meal – $320-$390; December $320-$400

August

soybean oil – 48.50-65; December 46-65 cent range

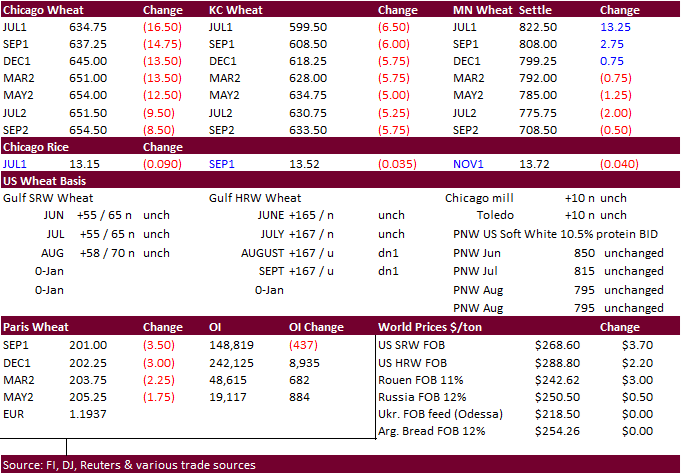

- US

wheat futures traded choppy, ending lower for Chicago (8.75-14.25 cents) and KC (5.0-5.75). Those markets followed corn and soybeans. Minneapolis wheat ended higher in the front three contracts (bull spreading) and lower in the back months. Heavy rains

across the Midwest will impact crop conditions and/or harvest progress. But for this week, harvesting advanced nicely across the southwest. US Wheat Associates noted favorable weather increased harvest progress in Texas, Oklahoma and Kansas while “an early

harvest of the drought-stressed SW crop is expected to begin this weekend.”

- Funds

sold an estimated net 8,000 Chicago wheat contracts. - While

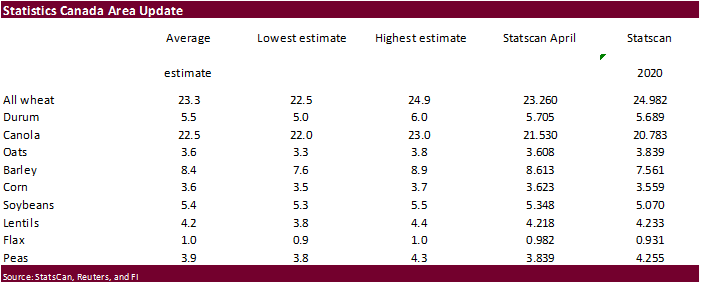

the Midwest benefits from rain this week through the weekend, the far northern Great Plains and parts of the Canadian Prairies will dry out, accompanied with hot temperatures. On Tuesday we will get StatsCan plantings and consensus should show Canada’s wheat

area could be down from April. - French

wheat ratings dropped 2 points to 79% as of June 21. - Bloomberg

reported Russia’s wheat export customs duty will rise to $41.30/ton from $38.10/ton – AgMin. Duty on barley will be unchanged at $39.60.

- Egypt’s

Minister said they have enough wheat for reserves to last 6.3 months. - September

Paris milling wheat settled down 3.00 euros, or 1.5%, at 201.50 euros ($240.47) a ton.

- Results

awaited: Taiwan seeks 55,000 tons of US million wheat on June 24 for Aug 12-26 shipment from the PNW.

- Jordan

retendered for 120,000 tons of wheat set to close July 6 for Jan/Feb 2022 shipment.

- Ethiopia

seeks 400,000 tons of wheat on July 19.

Rice/Other

- None

reported

Updated

6/25/21

September

Chicago wheat is seen in a $5.90-$7.00 range

September

KC wheat is seen in a $5.60-$6.70

September

MN wheat is seen in a $7.00-$8.50

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International

One Lincoln Center

18 W 140 Butterfield Rd.

Oakbrook Terrace, Il. 60181

W: 312.604.1366

ICE IM:

treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered

only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making

your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors

should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or

sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy

of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.