PDF Attached

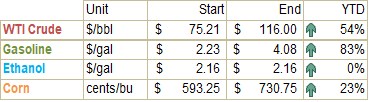

WTI

crude oil rallied after EIA reported a more than expected draw in crude oil supplies. The USD was down 70 points by noon CT. US agriculture futures rallied led by soybeans and soybean oil. Doubts are increasing over whether Ukraine grain exports will ship

over the near term. Drier weather is seen over the short-term for the northern US Great Plains. Argentina turns drier through Sunday. Brazil will see favorable corn harvest progress this week before slowing next week from rain.

USDA

will release its June Acreage report on Thursday, June 30th, the last business day of the month. Last year the USDA survey ran for 20 days during from Saturday, May 29 through Thursday, June 17, 2021. How USDA collects and assembles the data can

be explained on page 4 and 5 of this document. https://www.nass.usda.gov/Education_and_Outreach/Understanding_Statistics/pub1554.pdf

![]()

Weather

WEATHER

EVENTS AND FEATURES TO WATCH

- Relief

from dryness is expected in Europe over the next week to ten days with all areas impacted except Spain and Portugal - The

greatest relief is expected in France, Germany and the United Kingdom where moisture stress has evolved recently - Sufficient

moisture will fall to raise topsoil moisture and support ongoing crop development - Drying

is expected to continue in eastern parts of Canada’s Prairies and neighboring areas of North Dakota and northwestern Minnesota during the coming week to improve the potential for improved crop and field conditions - Temperatures

will be cooler than usual throughout the next week which will keep drying rates a little slow delaying the onset of more aggressive crop development - Eastern

Saskatchewan and much of Manitoba have the greatest need for dry and warm weather - Some

showers and drizzle will occur into Friday in Manitoba and a few immediate neighboring areas - Weather

conditions will improve greatly this weekend into early next week - Drought

relief is expected in central Montana, southern Alberta and a few far southwestern Saskatchewan, Canada locations during the weekend and early next week - Crop

conditions will improve where the rain falls, but only a small part of the drought region is expecting rain - West

Texas rainfall was missed overnight, but light showers will occur into Saturday with 0.20 to 0.80 inch of moisture resulting and locally more - The

precipitation will be welcome, but not nearly as great as advertised earlier this week - Warm

to hot temperatures and no rain will occur Sunday into Tuesday of next week before a new round of thunderstorms begins late next week through the following weekend - Some

locally strong thunderstorms will be possible late next weeks - Net

drying is expected in the lower U.S. Delta and southeastern states for a little while in this coming week - U.

S. Pacific Northwest will experience greater rain frequency and intensity over the coming week to ten days

- Some

of the moisture will help ease long term dryness - California

and the southwestern desert region will continue warm and dry biased for the next ten days - U.S.

Midwest weather will be favorably mixed over the next ten days keeping the ground adequately to abundantly wet

- Temperatures

will become cooler than usual resulting in slower drying rates and reduced degree day accumulations - Ontario

and Quebec weather will continue to be well balanced with periods of rain and sunshine - Southern

Florida citrus and sugarcane areas will be impacted by a tropical storm this weekend

- Heavy

rain and windy condition are expected, but very little, if any, damage is expected in agricultural areas - Local

flooding and a few strong wind gusts are expected, but the rain will be more welcome than detrimental - Recent

heavy rain from the remnants of Hurricane Agatha have produced some flooding in southern Mexico and northern parts of Central America

- Some

drying would now be welcome and should evolve - Western

Argentina wheat areas still need a boost in precipitation to induce the best planting, germination and emergence conditions - Argentina’s

main wheat production areas and areas all of the late season sorghum, soybeans, corn and peanuts produced in the nation are cool and moist enough to support crop needs through the harvest - Southern

Brazil has been and will continue to be a little too wet for a while - Drying

is needed to protect immature late season summer crops and to reduce flood potentials in wheat areas - Southeastern

Europe is getting enough rain to ease its recent dryness, but more is needed - Southwestern

Europe will have some ongoing needs for rain - Russia’s

Southern Region, southeastern Ukraine and western Kazakhstan will dry down through the weekend raising the need for timely rain later this month - Today’s

forecast model runs are offering rain to some of this region during the week next week

- Western

and northern Russia will continue in an active weather pattern bringing waves of rain and milder than usual weather periodically - Some

of the wetter and milder biased weather will also occur in Belarus, the Baltic States and northwestern Ukraine - Xinjiang,

China will experience some periodic rainfall in the northeast while most other areas away from the mountains are left mostly dry - Corn

and cotton planting are advancing well - North

China Plain dryness is not likely to go away anytime soon, despite the potential for a few showers in the coming week to ten days - Unirrigated

crop moisture stress has begun, although wheat has not been seriously impacted since it is largely irrigated - Three

wave of light rain will fall in the next ten days that may whittle back some of the dryness, but more rain will be necessary - Southern

China is bracing for additional excessive rainfall late this week and next week - Flooding

has already been a problem south of the Yangtze River recently and even though the rain is taking a short term break there is much more coming - Damage

to sugarcane and rice is possible - Southern

India monsoonal rainfall is expected to be lighter than usual over the next ten days - The

impact will be low for now, but greater rain will be needed in time - Australia

soil moisture is rated mostly well, but there will be need for rain in Western and South Australia this month especially in northern crop areas to restore favorable soil moisture

- New

South Wales and many areas in southeastern Queensland have favorable soil moisture for autumn planting and establishment of wheat, barley and canola - Rain

is expected in the dry areas of Western Australia next week - South

Africa weather is expected to be mostly dry for a while - Both

the harvest of summer crops and the planting of winter grains will advance well in the drier weather this week - Temperatures

will be near to above normal this week - All

of Southeast Asia will get rain at one time or another over the next couple of weeks. - The

precipitation will be good for most crop needs; however, it will be heavy along the Myanmar lower coast and in parts of both Laos and Vietnam into Cambodia - Northwestern

Luzon Island, Philippines and Taiwan will also be wet - Thailand

may not be included in the heavier rainfall that other Southeast Asia nations will experience for a while, but scattered showers and thunderstorms are still expected - West-central

Africa rainfall during the next ten days will be favorable for coffee, cocoa, sugarcane, rice and cotton

- East-central

Africa rainfall will be most significant in Ethiopia, southwestern Kenya and Uganda during the next ten days while Tanzania’s Pare region dries down seasonably - North

Africa rainfall will be limited in the next two weeks, although some rain is expected very lightly - Most

wheat and barley in the region is maturing and being harvested keeping the need for rain very low - Most

of the rain expected will be limited and should not adversely impact crop conditions or field progress - Turkey

crop areas will be the only ones in the Middle East to get significant rainfall during the next week to ten days - A

boost in rain is needed in many areas, but this is the beginning of the dry season

- These

areas may have experienced a decline in wheat, rice and cotton production this year – at least in unirrigated areas - Mexico

rainfall is expected to slowly increase in central and southern parts of the nation during the next ten days to two weeks with next week wettest - The

moisture will be welcome and should be a part of the developing monsoon season - Central

America will see periodic rain in the coming ten days with some of it to become heavy this weekend and next week from Costa Rica into Panama.

- Today’s

Southern Oscillation Index was +17.94 and it will steadily decline over the next few weeks - New

Zealand rainfall will be trending wetter over the next week

Source:

World Weather Inc.

Macros

97

Counterparties Take $1.985 Tln At Fed Reverse Repo Op (prev $1.965 Tln, 93 Bids)

US

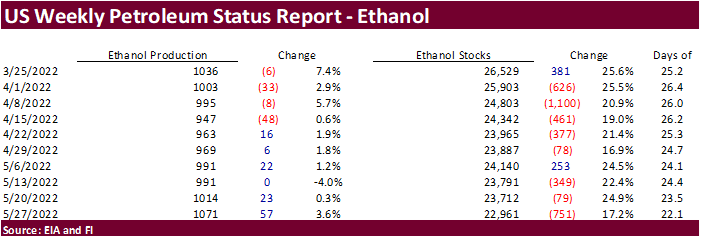

DoE Crude Oil Inventories (W/W) 27-May: -5068K

–

Distillate Inventories: -529K

–

Cushing OK Crude Inventories: 256K

–

Gasoline Inventories: -711K

–

Refinery Utilization: -0.60%

US

EIA Natural Gas Storage Change (BCF) 27-May: +90 (est +88; prev +80)

–

Salt Dome Cavern NatGas Stocks (BCF): -3 (prev 0)

US

ADP Employment Change May: 128K (est 300K; prev 247K)

US

Initial Jobless Claims May 28: 200K (est 210K ; prev 210K; prevR 211K)

–

US Continuing Claims May 21: 1.309M (est 1.325M; prev 1.346M; prevR 1.343M)

US

Nonfarm Productivity (Q1 F): -7.3% (est -7.5%; prev -7.5%)

–

US Unit Labor Costs (Q1 F): 12.6% (est 11.6%; prev 11.6%)

Canadian

Building Permits (M/M) Apr: -0.6% (est 0.8%; prev -9.3%)

·

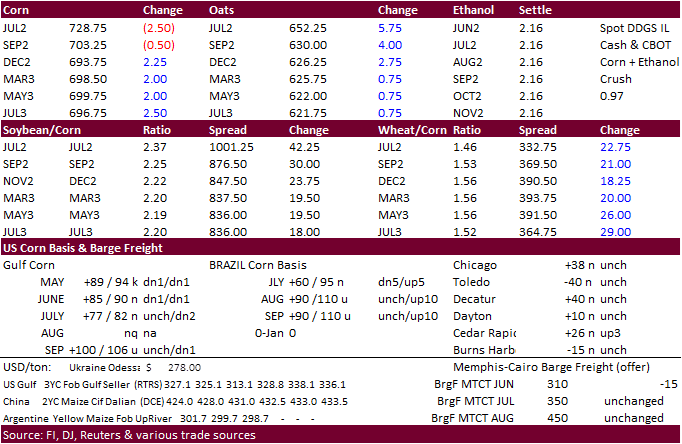

US corn futures ended lower in July and higher back months. They were much higher earlier on technical buying and Black Sea export uncertainty.

EIA numbers were supportive WTI crude oil and corn futures. Futures were pressured during afternoon trade from soy/corn and wheat/corn spreading coupled with lack of US export interest.

·

Funds were even today.

·

The USD was 74 points lower as of 1:20 pm CT.

·

Doubts are increasing over whether Ukraine grain exports will ship over the near term. Russia is looking for some sanctions to be lifted, including food, but there are no deals on the table. Russia did remove some quotas (set

for July-December period) on some fertilizers.

·

Today China planned to buy 40,000 tons of frozen pork for reserves, tenth round of procurement.

US

DoE Crude Oil Inventories (W/W) 27-May: -5068K

–

Distillate Inventories: -529K

–

Cushing OK Crude Inventories: 256K

–

Gasoline Inventories: -711K

–

Refinery Utilization: -0.60%

·

South Korea’s KFA bought 66,000 tons of corn from South America at $391.95/ton c&f for LH July through early August shipment. Early May they paid $382/ton.

Updated

6/1/22

July

corn is seen in a $6.75 and $8.00 range

December

corn is seen in a wide $5.50-$8.00 range