PDF Attached

USDA

plantings and stocks reports are due out tomorrow. US agriculture futures ended higher pre-report day on renewed Black Sea concerns, rebound in WTI crude oil and lower USD. It’s too early to see if Russia will live up to their promise to de-escalate their

military “operation.” There

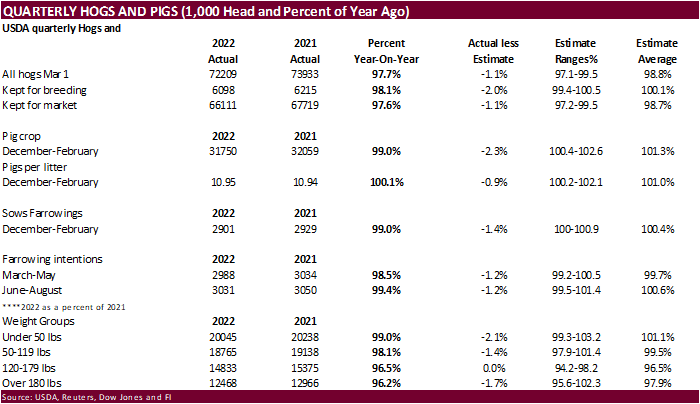

was a headline Russia actually intensified shelling in some areas outside the cities they were targeting. USDA’s hogs and pigs report was viewed bullish hogs and slightly negative for US corn futures.

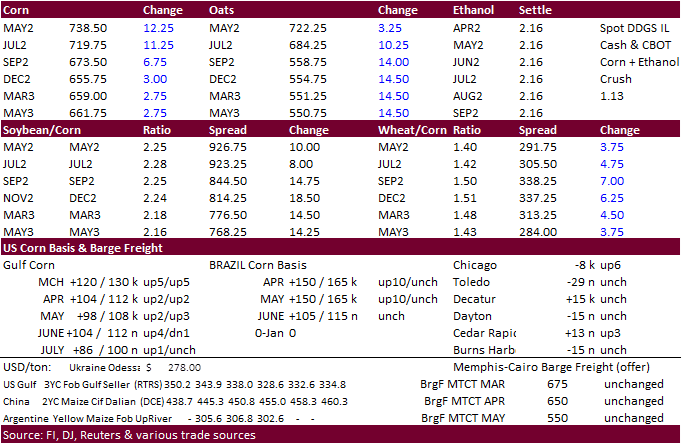

![]()

WEATHER

EVENTS AND FEATURES TO WATCH

- U.S.

Delta, Tennessee River Basin and lower Parts of the Midwest may experience planting delays this spring due to wet field conditions - Poor

drying rates are expected in this coming week between rain events and the ground is already saturated or nearly saturated - No

relief to dryness in West or South Texas is expected over the next ten days to two weeks - Dryland

crops in both regions will be vulnerable to production cuts this year, although there is plenty of time for rain to evolve in West Texas before planting begins in May - South

Texas crops, however, were planted previously and are not germinating, emerging or establishing well in unirrigated fields - U.S.

southeastern states will experience a mix of weather during the next two weeks that will be supportive of some spring fieldwork - U.S.

northwestern Plains and southwestern Canada’s Prairies are unlikely to see “significant” precipitation for a while, although a few sporadic periods of rain and snow will impact portions of the region infrequently. - California’s

rainfall in the southern coastal Plain this week was welcome, but precipitation in the Sierra Nevada was dismally poor and the outlook for the state is dry over the next ten days to two weeks.

- The

state is likely facing some serious water shortages later this year and MUST experience a more favorable winter precipitation pattern next year to avoid a more serious water shortage

- Frost

and freezes may develop in the interior southeastern U.S. late next week, although it is too early to get specific about the outlook. - Southwestern

Argentina will be dry biased for the next week to ten days - Northeastern

Argentina, southern Brazil and southern Paraguay may get too wet this weekend and next week raising concern over rice and other crop conditions

- Delays

in harvesting is expected - Northeastern

Brazil will continue drier than usual over the next ten days to two weeks - The

region includes much of Bahia, away from the coast, and the northern and central parts of Minas Gerais - Crop

moisture stress is impacting corn, rice, sugarcane and coffee, although most of the production in these areas is limited - Rainfall

predicted in southern Mato Grosso and Mato Grosso do Sul in today’s forecast models has been reduced for the coming ten days, but this is not the end of seasonal rainfall for the region - The

drier bias might improve some Safrinha crops after recent excesses of moisture - Central

Europe to wet-central Russia will be wetter biased for a while during the coming week - Some

heavy snow is expected from southern Germany through northwestern Ukraine and southeastern Belarus to the Ural Mountains - The

snow might contribute to spring flooding since the moisture content will be high in the snow and the ground is suspected of being wet beneath the snow - Europe

and northwestern Russia temperatures will be cooler than usual over the coming week with some warming expected in western Europe during the second week of the outlook - Northwestern

Africa and southwestern parts of Europe will continue to receive periodic precipitation that will serve winter wheat, barley and some spring crops well - Additional

precipitation is predicted for the Russian New Lands and northern Kazakhstan during the weekend and especially next week - The

moisture will be ideal for spring planting - India’s

harvest weather will be very good over the next couple of weeks - Precipitation

will be limited to sporadic showers in the far south and more generalized rain in the Eastern States

- Southeastern

China will get additional rain today and Thursday and then be dry biased for much of the following week to ten days - The

break from rainy weather will be ideal for rapeseed development and early season corn and rice planting throughout the south - Improvements

to many crops and field working conditions are likely - Temperatures

will trend warmer, as well - Northern

wheat areas of China will experience some warmer weather next week that may stimulate some greater crop development potential - Mexico’s

dryness and drought have been expanding this winter due to poor precipitation resulting from persistent La Nina - The

region will continue lacking precipitation for an expected period of time - Eastern

and southern Mexico will remain seasonably dry this week and will only receive light rainfall next week - Southeast

Asia rainfall will continue frequent and abundant - No

area in the mainland areas, Philippines, Indonesia or Malaysia are expected to be too dry - Too

much rain may impact northeastern Philippines late this weekend into next week - Vietnam

may be impacted by a tropical disturbance during the next several days resulting in frequent rainfall along the lower coast with some rain reaching into coffee areas as well - The

moisture may be good for rain-fed coffee which normally flowers in April - East-central

Africa rainfall will continue greatest in Tanzania, although parts of Uganda and Kenya will get rain periodically as well.

- Ethiopia

rainfall should be most sporadic and light - West-central

Africa rainfall will continue periodically and sufficient to support coffee and cocoa development - Rainfall

so far this month has been a little sporadic, but no area has been seriously dry biased - Pockets

in Ivory Coast and western Ghana have received less than usual rain, but crop development has advanced well

- North

Africa rainfall will be greatest today and Thursday with some follow up showers early to mid-week next week in Morocco and northern Algeria - Crop

conditions will improve as a result of the rain - Western

Australia will continue to receive periods of rain through the weekend, although much of it be light and sporadic - The

additional moisture will further boaster topsoil moisture for use in the autumn wheat, barley and canola planting season that begins in late April - Eastern

Australia precipitation is expected to be limited the remainder of this week bringing on a better environment for cotton in the open boll stage of development - The

drier weather will also be good for early season planting which begins soon - Irrigated

late season sorghum and other crops will continue to develop favorably - Some

of the dryland crop that is still immature still needs greater moisture - Rain

is expected briefly during the weekend and early part of next week, but it should not seriously harm fiber quality, although any rain is not welcome at this time of year - South

Africa rainfall over the next couple of weeks will periodic and sufficient enough to support late season crop development while the impact on mature crops should be low outside of some brief harvest delays - Colombia,

Ecuador, western Venezuela and parts of Peru will remain plenty wet during the next ten days - Frequent

rain is expected - The

moisture will be great for coffee and cocoa flowering and well as support of all crops - Today’s

Southern Oscillation Index is +12.13 - The

index will move lower over the next seven days - Central

America precipitation will be greatest along the Caribbean Coast during the next seven to ten days and in both Panama and Costa Rica - Guatemala

will also get some showers periodically

Source:

World Weather Inc.

- EIA

weekly U.S. ethanol inventories, production, 10:30am - USDA

hogs and pigs inventory, 3pm

Thursday,

March 31:

- U.S.

annual acreage prospective planting data for various farm commodities, including wheat, barley, corn, cotton, soybeans and sunflower, noon - USDA

quarterly stockpile data for wheat, barley, corn, oats, soybeans and sorghum, noon - USDA

weekly net-export sales for corn, soybeans, wheat, cotton, pork and beef, 8:30am - U.S.

agricultural prices paid, 3pm - Malaysia’s

March palm oil export data

Friday,

April 1:

- ICE

Futures Europe weekly commitments of traders report - CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm - Australia

Commodity Index - USDA

soybean crush, DDGS output, corn for ethanol, 3pm - FranceAgriMer

weekly update on crop conditions

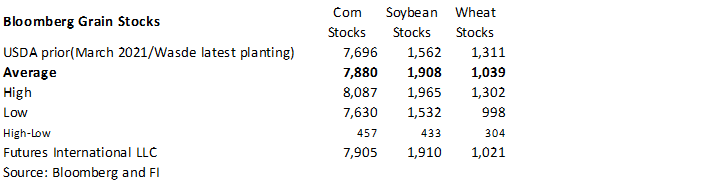

Source:

Bloomberg and FI

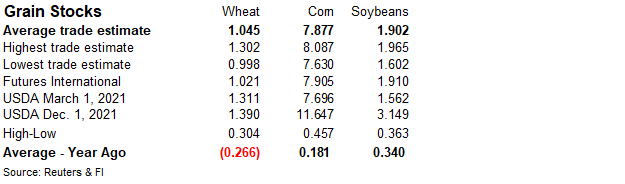

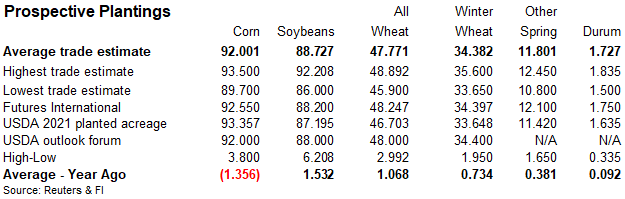

Reuters

trade estimates for USDA

US

GDP Annualized (Q/Q) Q4 T: 6.9% (est 7.0%; prev 7.0%)

US

GDP Price Index Q4 T: 7.1% (est 7.1%; prev 7.1%)

US

Core PCE (Q/Q) Q4 T: 5.0% (est 5.0%; prev 5.0%)

US

Personal Consumption Q4 T: 2.5% (est 3.1%; prev 3.1%)

US

ADP Employment Change Mar: 455K (est 450K; prev 475K)

US

DoE Crude Oil Inventories (W/W) 25-Mar: -3449K (est -2000K; prev -2508K)

–

Distillate Inventories: 1395K (est -1500K; prev -2071K)

–

Cushing OK Crude Inventories: -1009K (prev 1235k)

–

Gasoline Inventories: 785K (est -1600K; prev -2948K)

–

Refinery Utilization: 1.00% (est 0.40%; prev 0.70%)

86

Counterparties Take $1.786 Tln At Fed Reverse Repo Op (prev $1.719 Tln, 88 Bids)

·

US corn futures ended higher led by bull spreading mainly on a rebound in US WTI crude oil and lower USD. Post CBOT close, USDA’s Hogs and Pigs report appeared to be bullish for hog futures.

·

The AgMin in Brazil’s state of Parana reported 85% of the first corn crop had been harvested as of Sunday, above 82% year earlier. Conab showed all Brazil first corn crop 47% collected versus 43% year earlier.

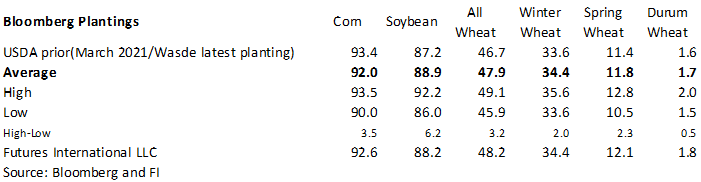

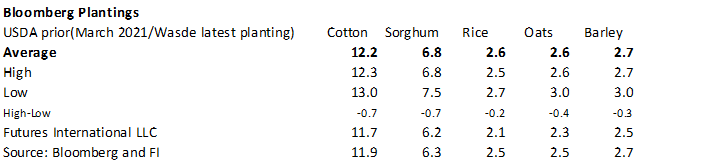

·

We heard a large ethanol company predicted acres at 88.6 million for corn and 89.2 million for soybeans. Combined this seems a little low, in our opinion. We are at 92.5 million acres, 500,000 above the trade average.

·

Looking past soybeans, the low corn area outlook from the ethanol company is a reminder record fertilizer prices and short supply of the product may force some producers to consider some switching from corn to soybeans and/or

other commodities. We are seeing this for producers residing in the fringe states. For example, some producers across the far SE are switching from corn to cotton and peanuts, due to high input costs for corn. And for the far western Great Plains we are hearing

wheat is favored over corn to plant for the same reason. If we had to call a position for the US acreage report, I would hold a small, long position in new-crop corn. But keep in mind we also get a stocks number. Bear spreading could be a play for those looking

for large old crop stocks and less than expected 2022 corn acres.

·

USDA’s Broiler Report showed eggs set in the US up 1 percent from a year ago and chicks placed up slightly. Cumulative placements from the week ending January 8, 2022, through March 26, 2022 for the United States were 2.23 billion.

Cumulative placements were down slightly from the same period a year earlier.

US

DoE Crude Oil Inventories (W/W) 25-Mar: -3449K (est -2000K; prev -2508K)

–

Distillate Inventories: 1395K (est -1500K; prev -2071K)

–

Cushing OK Crude Inventories: -1009K (prev 1235k)

–

Gasoline Inventories: 785K (est -1600K; prev -2948K)

–

Refinery Utilization: 1.00% (est 0.40%; prev 0.70%)

Export

developments.

- AgriCensus

noted South Korea’s MFG bought 137,000 tons of optional origin (South American and/or SAf) corn at $382.18 & $384.50/ton CFR for July delivery.

Updated

3/23/22

May

corn is seen in a $6.75 and $8.10 range

December

corn is seen in a wide $5.50-$7.50 range

·

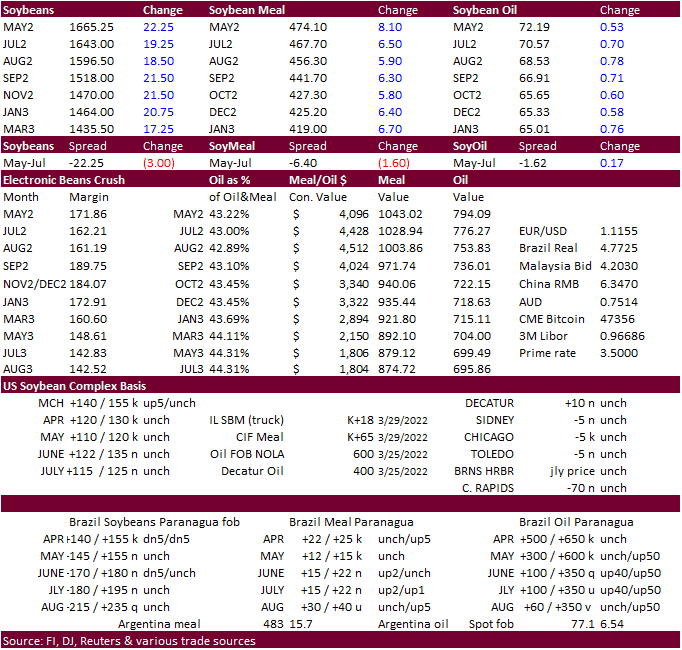

The CBOT soybean complex ended higher from strength in WTI crude oil, positioning ahead of the USDA reports, and a sharply lower USD.

Under

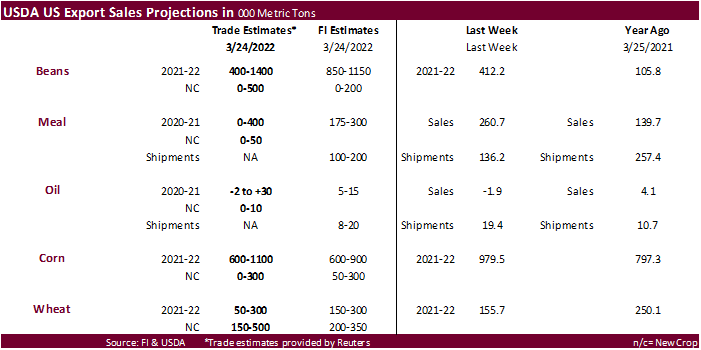

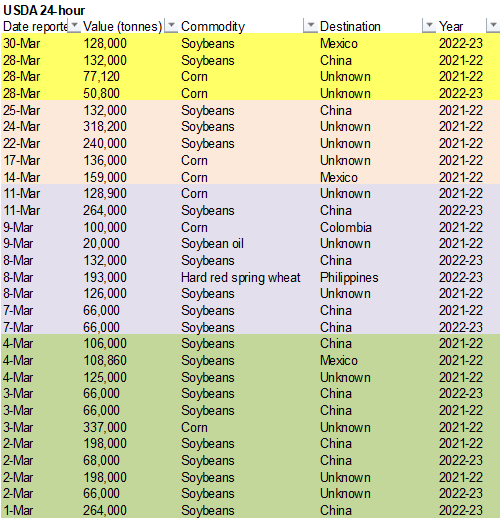

the 24-hour announcement system, private exporters sold 128,000 tons of soybeans to Mexico for 2022-23 delivery.

·

Our bias is to see a neutral to bearish soybean planting number for USDA’s report based on the possibility for US producers to scale back on corn plantings. We are near the higher end for US corn plantings but recent reports

from producers do hint they are scaling back on corn intentions due to high input costs and uncertainty they will secure fertilizer. Trade estimate widely vary which tells up the trade has great uncertainty for acreage.

·

The AgMin in Brazil’s state of Parana reported 83% of the soybean crop had been harvested as of Sunday, down from 88% year earlier. Conab showed all Brazil soybean crop 76% collected versus 70% year earlier.

·

Brazil consultancy Datagro sees 2022 Brazil soybean exports at 99.1 million tons, down nearly 6 percent from a year ago.

·

Reuters – Indonesia’s palm oil export levy collection in 2022 is estimated at 68.18 trillion rupiah ($4.76 billion), down from last year’s 71.6 trillion rupiah, said Eddy Abdurrachman, head of the palm oil fund agency.

·

Under the 24-hour announcement system, private exporters sold 128,000 tons of soybeans to Mexico for 2022-23 delivery.

·

Turkey seeks 18,000 tons of sunflower oil on Thursday.

·

China plans to sell about 500,000 tons of soybeans on April 1.

- USDA

seeks 2,710 tons of packaged oil on April 7 for May shipment (May 23-June 13 for plants at posts).

- Qatar

seeks to buy 960k cartons of corn oil in a tender closing April 4.

Updated

3/29/22

Soybeans

– May $15.50-$17.50 (down 50, down 50)

Soybeans

– November is seen in a wide $12.50-$16.00 range

Soybean

meal – May $430-$500 (unch, down $20)

Soybean

oil – May 68.50-74.00

(sharply

lower range)

·

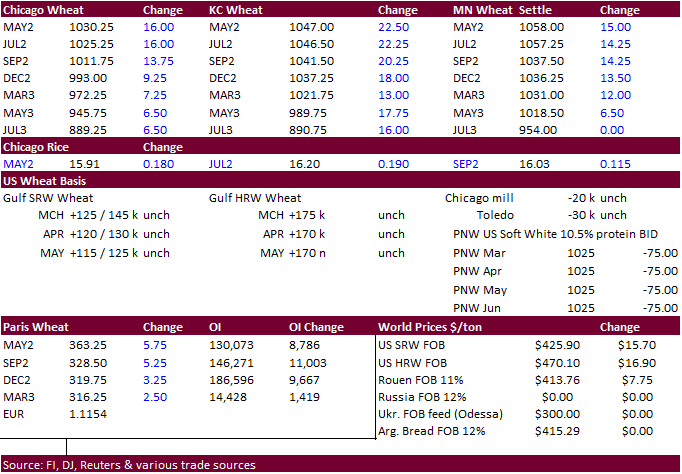

US wheat futures traded tow-sided before the day session, traded higher throughout the day, and settled 12-20 cents higher led by KC type wheat. Renewed Black Sea concerns, rebound in WTI crude oil and lower USD underpinned prices.

It’s too early to see if Russia will live up to their promise to de-escalate their military “operation.” But the trade believes nothing drastically will change over the short-term.

·

Our bias for the USDA report is to see more than expected US spring wheat acres plantings. Stocks should have little impact unless we see a 40 plus million bushel deviation, which is unlikely.

·

Russia is looking at expanding their list of commodities requiring importers to pay in rubles, including grain and metals.

·

Taiwan bought 40,000 ton of US wheat while results are awaited on Tunisia and Algeria.

·

Ukraine is in talks with Romania to ship wheat out of the Constanta Black Sea port.

·

Russian wheat exports are expected to end up around 1 million tons for the month of March, a much larger number than what the trade thought at the beginning of the month.

·

May Paris wheat futures were up 9 euros (2.5%) to 366.50 euros.

Wheat

in 2023?

Schnitkey,

G., C. Zulauf, N. Paulson and K. Swanson. “Wheat in 2023?.” farmdoc

daily

(12):40, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign, March 29, 2022.

https://farmdocdaily.illinois.edu/2022/03/wheat-in-2023.html

·

Algeria started buying milling wheat with prices around 448/ton C&F for May and/or June shipment.

·

Tunisia bought about 125,000 tons of soft wheat and 100,000 tons of feed barley. The wheat was bought between $418.68 and $455.75 per ton and barley $442.68 and $457.96 per ton. The wheat was sought for shipment between April

20 and June 25, depending on origin supplied. The barley is sought for shipment between April 25 and June 25.

·

Taiwan bought 40,000 tons of US wheat for shipment off the PNW during the May 14 and May 28 period. 14.5 percent dark northern spring wheat was bought at $439.82 a ton FOB PNW, 12.5 percent hard red winter wheat bought at $462.94

a ton FOB and 10.5% protein soft white wheat bought at $415.47 a ton FOB.

·

Jordan bought about 60,000 tons of feed barley at an estimated $395.00 a ton c&f for shipment in the second half of July.

·

Bangladesh seeks 50,000 tons of wheat on April 11 for shipment within 40 days after contract signing.

·

Jordan issued an import tender for 120,000 tons of milling wheat for shipment during May, June, or July on March 31.

·

Results awaited: Qatar seeks 105,000 tons of optional origin animal feed barley on March 27 shipment in April, May and June.

·

Bangladesh is in for 50,000 tons of wheat with a deadline of April 4.

Rice/Other

·

(Bloomberg) — Qatar is seeking to buy 1.2m bags of rice in a tender that closes April 4, according to the Ministry of Commerce and Industry’s website. Qatar also seeks to buy 960k cartons of corn oil in a tender closing April

4

Updated

3/29/22

Chicago

May $9.00 to $12.00 range

KC

May $9.00 to $12.00 range

MN

May $9.75‐$12.00

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International

One Lincoln Center

18 W 140 Butterfield Rd.

Oakbrook Terrace, Il. 60181

W: 312.604.1366

ICE IM:

treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered

only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making

your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors

should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or

sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy

of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.