PDF Attached

SBO was the feature again today but wheat and corn gained attention at the day session open from fund buying. Crude oil :: WTI fell 6% today on increased EU COVID lockdowns causing vegoils to give up earlier gains.

The US southern and central Great Plains (HRW) bias eastern areas will see additional rain this week. Northern Plains & Canadian Prairies will be in focus this week as it remains too dry and the two-week outlook does not suggest much precipitation. Rest of the US will be ok with exception of too much precipitation for the Delta that will slow fieldwork activity. Midwest will not start planting for a week or two so there is no concern there. Brazil will see a drier bias over the next seven to ten days. Monsoon rains are expected to withdraw later in April. Argentina will see additional rains Wednesday into Friday. Eastern Australia will dry down this week.

QPF 1-7 day total precipitation

World Weather Inc.

UNITED STATES

- Greater rainfall has been suggested for the Tennessee River Basin and a part of the lower Delta this weekend

- Some of the increase was overdone

- Less rain was suggested for West Texas, north-central Texas, Oklahoma, southeastern Kansas and southern Missouri late this weekend into early next week

- Some of the reduction was needed

- Rain was removed from the southern Plains during the middle part of next week

- Some of this reduction was needed

- Greater rain was advertised for the eastern Midwest during mid-week next week

- Some of this increase was needed

- GFS reduced rain in the lower and eastern Midwest, Delta and Tennessee River Basin April 2-4 which it was increased in Texas and Oklahoma

- Some of this was necessary

- GFS increased rain in the southern Plains and a part of the Delta April 3-5

- The boost may have been a little overdone

ARGENTINA

- No changes were noted in the first week of the outlook

- The second week of the outlook was drier

- Rain was removed from southeastern and some central parts of Argentina in the latter part of next week into the following weekend

- A little too much rain may have been removed, but this was a relatively weak event to begin with

- GFS was drier in the last days of the model run, April 5-6

- A little too much rain was removed

Overall, too much rain was removed from the second week outlook

BRAZIL

- No changes were noted relative to the previous model run in the first week of the outlook

- Rain was reduced April 2-4 in the interior southern parts of the nation

- Some of this reduction was needed

- Rain was also reduced from southern Brazil April 5-7

- Too much rain was removed, but the previous model run was too wet

Source: World Weather inc.

Bloomberg Ag Calendar

Wednesday, March 24:

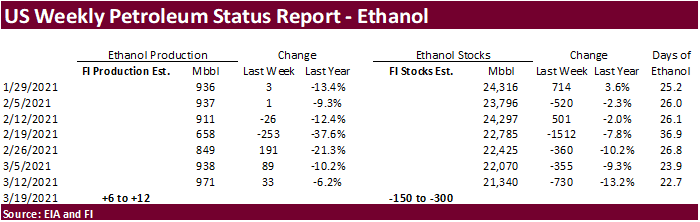

- EIA weekly U.S. ethanol inventories, production

- Bursa Malaysia Derivatives virtual palm oil conference 2021, day 2

- U.S. poultry slaughter

- EARNINGS: JBS

- HOLIDAY: Argentina

Thursday, March 25:

- USDA weekly crop net-export sales for corn, soybeans, wheat, cotton, pork, beef, 8:30am

- Seminar on sustainable palm oil in India by the Solvent Extractors’ Association and the MPOB

- International Grains Council monthly report

- Port of Rouen data on French grain exports

- Malaysia’s March 1-25 palm oil export data

- USDA hogs & pigs Inventory, red meat production

Friday, March 26:

- ICE Futures Europe weekly commitments of traders report (6:30pm London)

- CFTC commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm

- FranceAgriMer weekly update on crop conditions

Soybean and Corn Advisory:

2020/21 Brazil Soybean Estimate Unchanged at 132.0 Million Tons

2020/21 Argentina Soybean Estimate Unchanged at 46.0 Million Tons

2020/21 Brazil Corn Estimate Unchanged at 105.0 Million Tons

2020/21 Argentina Corn Estimate Unchanged at 45.5 Million Tons

Macro

US New Home Sales Feb: 775K (exp 870K; R prev 948K)

– New Home Sales (M/M) Feb: -18.2% (exp -5.7%; R prev 3.2%)

US Philadelphia Fed Non-Manufacturing Regional Business Activity Mar: 38.6 (prev 3.9)

Corn

- Corn rose today on fund buying and wet South American weather. The rains in Brazil are slowing planting of the Brazilian winter corn crop. While the rain in Argentina is well received and bearish, it may be too late for some of the corn crop which is why it did not outweigh the Brazilian delays.

- US corn acre expectations are mostly coming in north of 93 million acres. The higher acres come at the expense to something, but unlikely soybeans. However, FBN has an 87.6 soybean acre estimate.

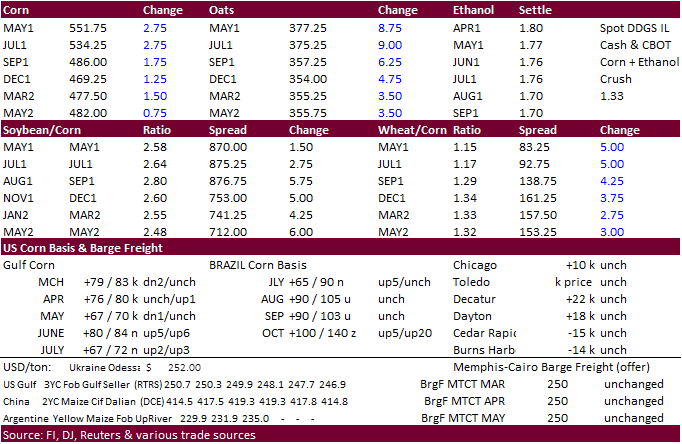

- May corn support is seen at $5.3950.

- Funds on Tuesday bought an estimated net 4,000 contracts.

- USDA hog and pig report estimates from Bloomberg: Hog inventory seen falling to 76.059 million head vs 76.179 last March. Breeding inventory seen down 1.3% y/y, and market hogs seen falling 0.1% y/y. The pig crop seen 0.5% higher y/y. March-May farrowing intentions seen down 0.8% y/y, and June-Aug. seen falling 0.5% y/y. Report due out March 25.

- April options expire this Friday.

Export developments.

- There were no USDA 24-hour sales.

- Global export developments have been slow so far this week.

Updated 3/16/21

May corn is seen in a $5.35 and $5.75 range.

July is seen in a $5.10 and $5.75 range.

December corn is seen in a $3.85-$5.50 range.

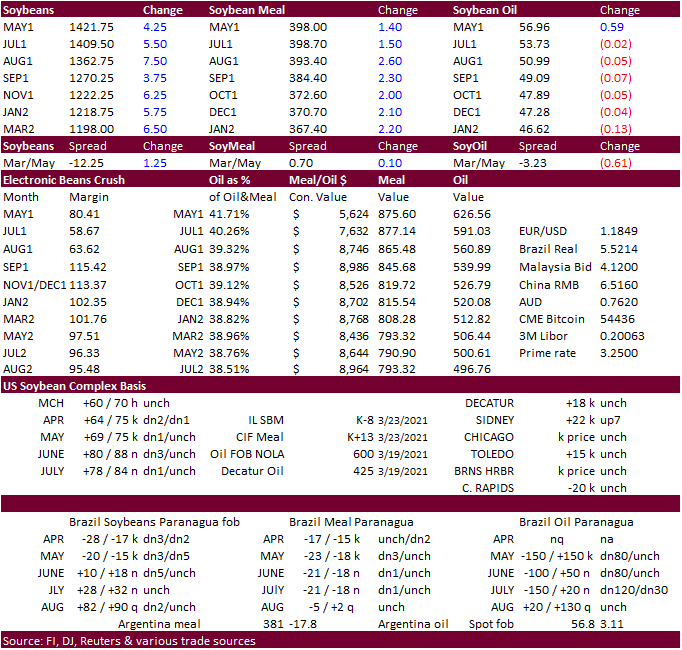

- Nearby soybeans traded higher today, but off the midday highs. Funds were buyers across the board in grains and oilseeds, but mid-session, the macro markets fell on increased EU COVID lockdowns. WTI was a big loser today on demand destruction which spilled over to vegoils causing the back of the BO futures curve to settle lower.

- Prompt month BOK1 futures settled up only 0.65 to 57.02 c/lb after making a contract high at 58.25.

- During the session we heard chatter on a couple Argentina refined soybean oil cargos traded to the US.

- Funds on Tuesday bought an estimated net 5,000 soybean contracts, bought 2,000 soybean meal, and bought 2,000 soybean oil.

- Argentina’s February crush hit an extremely large 2.85 million tons (for the month), up from 2.63 million tons a year earlier, down from 3.23 million tons during January 2021.

- Argentina will be on holiday Wednesday.

- Malaysian palm futures rallied more than 2% overnight (+87 MRY & cash up $12.50). China vegetable oil prices rallied while soybean meal in Dalian are trading near a year to date low and have dropped more than 15% from the 2014 highs in January, according to Bloomberg.

- Indonesia set its crude palm oil price for April higher at $1,093.83 per ton, and export taxes for crude palm oil in April will be $116 per ton, up from $93 in March. The crude palm oil reference price for March was set at $1,036.22 per ton.

- Malaysia’s 2021 biodiesel exports are seen at lowest in four years due to European Union restrictions, to around 350,000 tons from 378,582 tons in 2020.

- SGS reported Malaysian palm March 1-20 shipments down 0.1 percent from the same period previous month.

Export Developments

- Results awaited: Iran seeks 30,000 tons of sunflower oil and 30,000 tons of soybean oil on March 18 for March and April shipment.

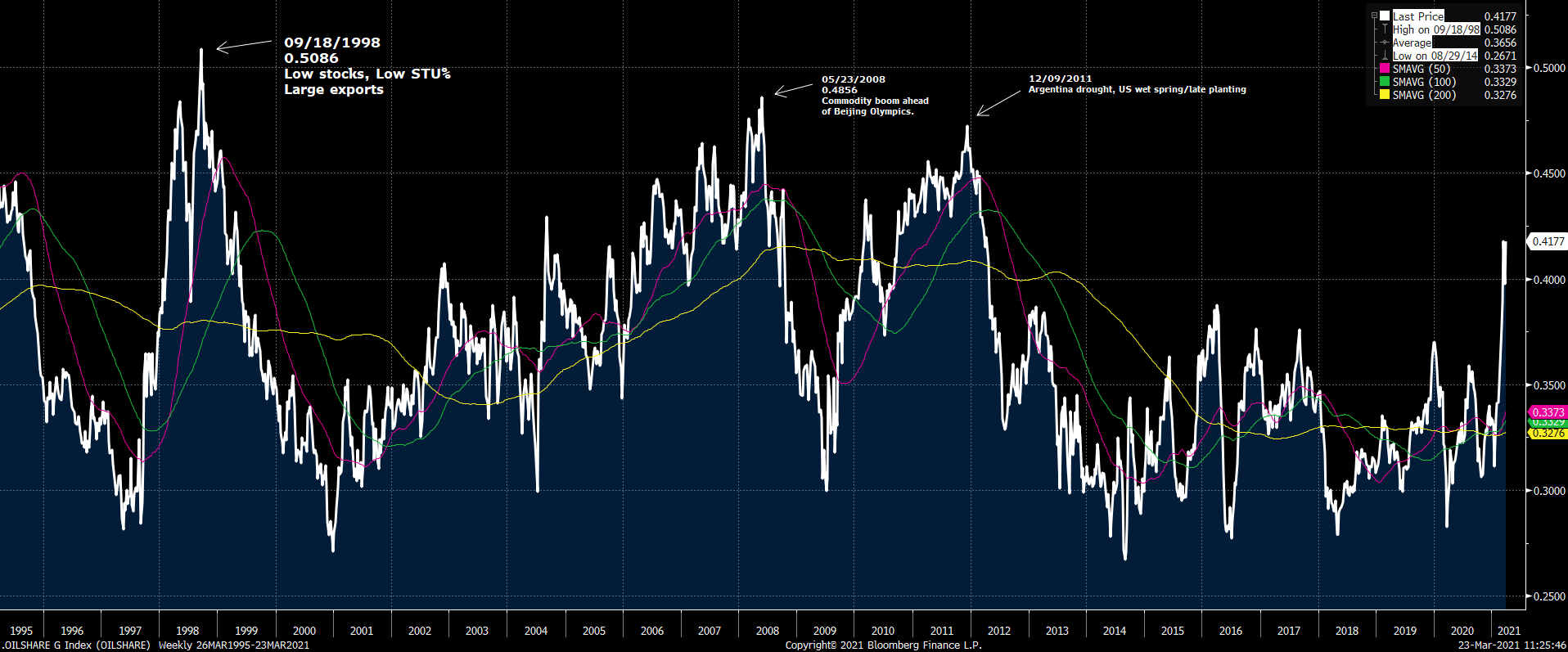

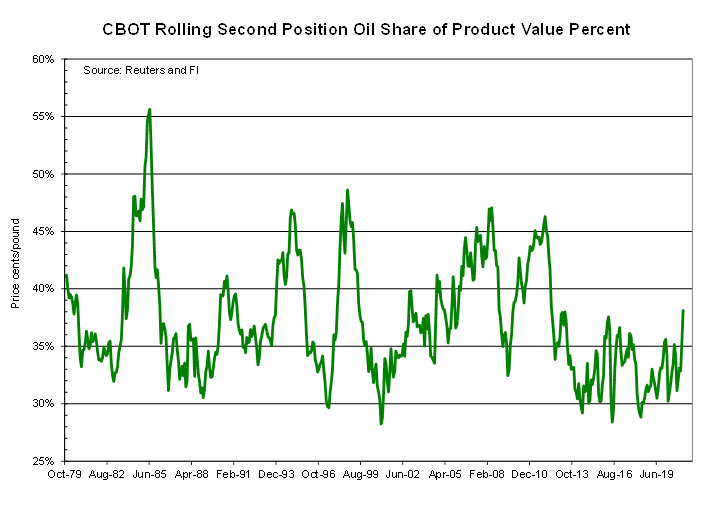

Soybean oil share, weekly back to 1995.

Soybean oil share, monthly

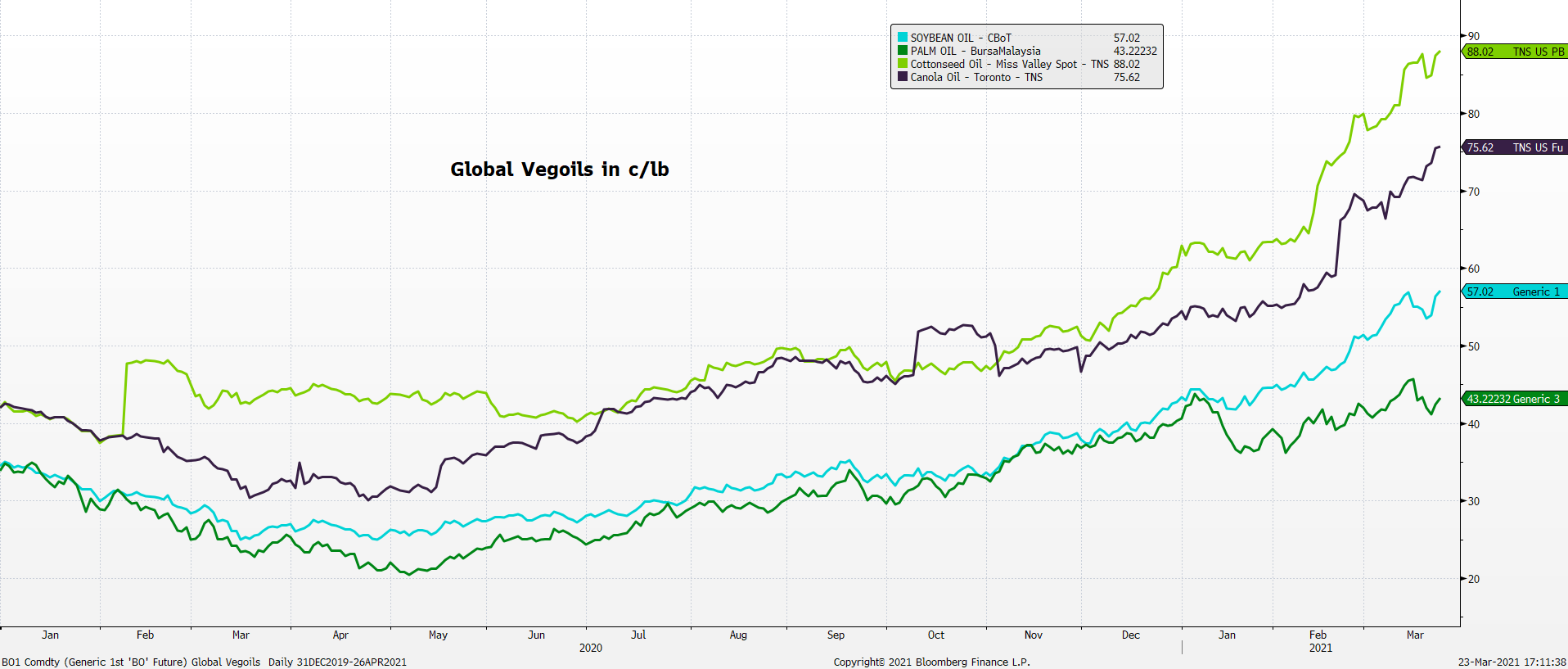

Global Vegoils in c/lb

Updated 3/22/21

May soybeans are seen in a $13.75 and $14.75 range.

May soymeal is seen in a $385 and $425 range.

May soybean oil is seen in a 54 and 58 cent range

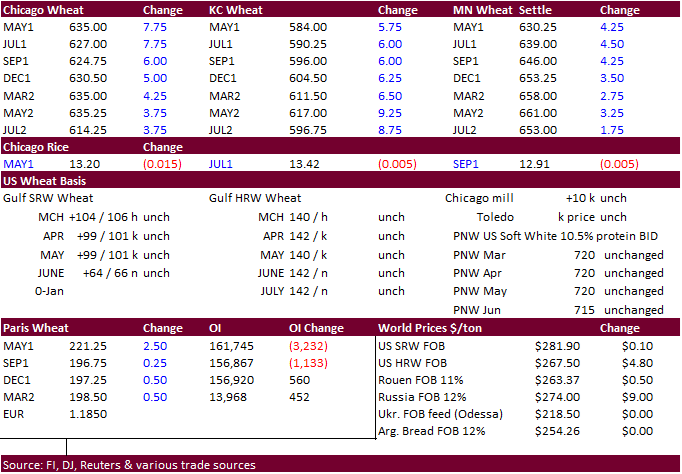

- CBOT Chicago wheat climbed today on the fund buying, but the rains on the Plains and yesterday’s improved WW crop conditions helped limit gains.

- Global tender activity has picked up with the drop in prices, but nothing yet from the large MENA players.

- Funds on Tuesday were net buyers of 5,000 SRW wheat contracts.

- EU May milling wheat was 2.25 higher at 221.00 euros, ending an 11-session skid.

- USDA Attaché on Egypt grain update: https://apps.fas.usda.gov/newgainapi/api/Report/DownloadReportByFileName?fileName=Grain%20and%20Feed%20Annual_Cairo_Egypt_03-15-2021

Reuters recap on US winter wheat ratings and corn plantings:

- Kansas was rated 45% G/E for the winter wheat crop, up from 38% a week earlier.

- Soil moisture readings were improving in Kansas, the top U.S. winter wheat producer. The USDA reported that Kansas topsoil moisture as of Sunday was short to very short in 17% of the state, a drop from 24% the previous week and 47% two weeks ago.

- For Oklahoma, another major wheat state, the USDA rated 62% of the winter wheat crop in good to excellent condition, up from 57% a week earlier.

- The USDA said 36% of Oklahoma’s wheat had reached the “jointing” stage of growth, ahead of the five-year average of 31%.

- For Texas, the No. 2 winter wheat state by planted area, the USDA rated 29% of the crop as good to excellent, up from 27% the previous week.

- The Texas corn crop was 38% planted, up from 26% a week ago and ahead of the state’s five-year average of 34%.

- For Colorado, the USDA rated 33% of the winter wheat as good to excellent, up from 25% the previous week.

- Farmers in the Plains states grow hard red winter wheat, the largest U.S. wheat class, which is milled into flour for bread.

- In Arkansas, where farmers grow soft red winter wheat used to make cookies and snack foods, the USDA rated 57% of the state’s wheat as good to excellent, up from 53% a week ago.

- The USDA rated 45% of the Louisiana winter wheat crop and 49% of Mississippi’s wheat as good to excellent.

- Corn planting was 52% complete in Louisiana and 11% complete in Mississippi.

- Over the winter and early spring, the USDA’s National Agricultural Statistics Service releases crop progress reports for select states. The government is scheduled to resume regular weekly U.S. crop progress reports on April 5.

Export Developments.

- Thailand seeks up to 430,000 tons of animal feed wheat on Wednesday, March 24 for shipment during May and December.

- Cancelled. 2 participants: Jordan is in for feed barley.

- Jordan will be back in for feed barley on March 30 for Oct/Nov shipment.

- South Korean group SPC seeks 35,000 tons of milling wheat from the United States and Canada on March 23. for arrival in July.

- The Philippines seek 155,000 tons of milling wheat and animal feed wheat on March 24 for shipment between April and July.

- Results awaited: Algeria’s ONAB seeks 40,000 tons of animal feed barley on March 18 for April 15-30 shipment.

Rice/Other

· South Korea’s Agro-Fisheries & Food Trade Corp. seeks 208,217 tons of rice, on March 25 for arrival in South Korea in 2021 between May 1 and Oct. 31. 64,444 tons of non-glutinous brown rice is sought from the United States. Rest from Thailand, China, Australia, and Vietnam.

· Bangladesh also seeks 50,000 tons of rice on March 28.

· Syria seeks 25,000 tons of white rice on March 29, from China or Egypt.

· Syria seeks 39,400 tons of white rice on April 19. Origin and type might be White Chinese rice or Egyptian short grain rice.

Updated 3/18/21

May Chicago wheat is seen in a $6.15‐$6.75 range

May KC wheat is seen in a $5.65‐$6.60 range

May MN wheat is seen in a $6.15‐$6.50 range

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International

One Lincoln Center

18 W 140 Butterfield Rd.

Oakbrook Terrace, Il. 60181

W: 312.604.1366

ICE IM: treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.