PDF Attached

May

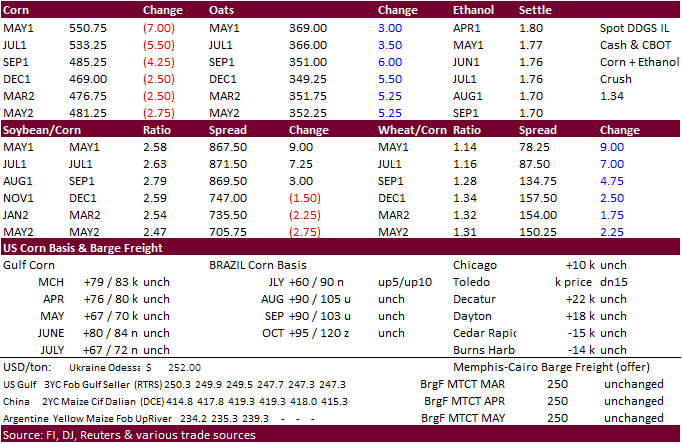

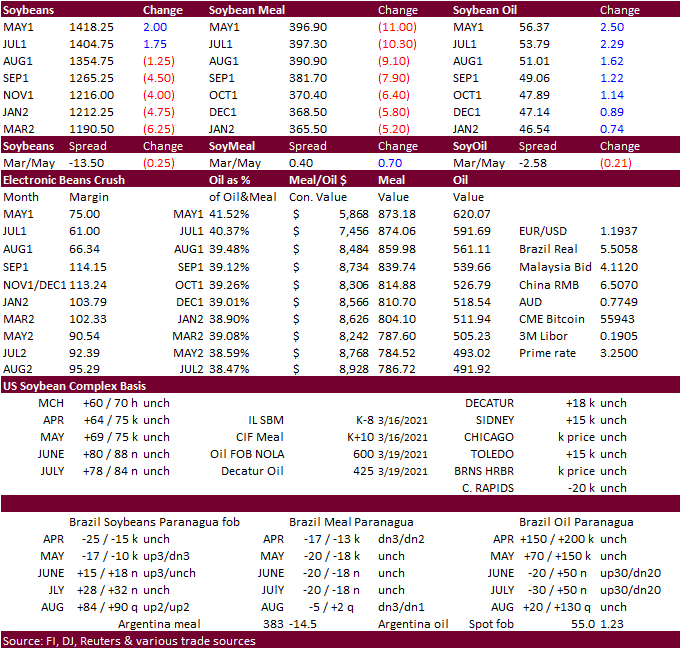

SBO ended limit up on talk of strong SBO use for renewable fuel tightening US stocks. We agree and look for a 100 million pound reduction to USDA’s balance sheet by at least the May USDA S&D update. We will issue stocks estimates for USDA March 1 on Tuesday.

The

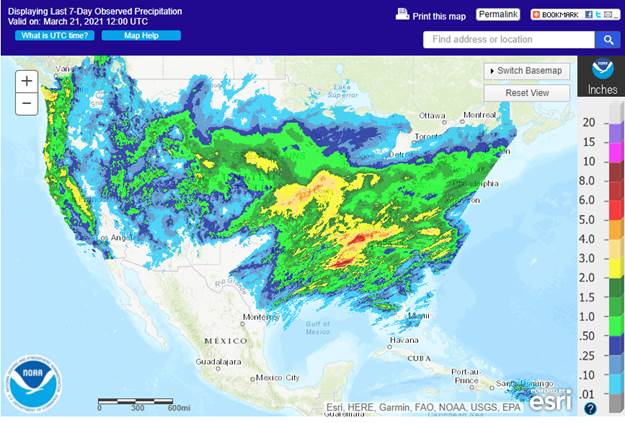

US southern and central Great Plains (HRW) bias eastern areas will see additional rain this week. Northern Plains & Canadian Prairies will be in focus this week as it remains too dry and the two week outlook does not suggest much precipitation. Rest of the

US will be ok with exception of too much precipitation for the Delta that will slow fieldwork activity. Midwest will not start planting for a week or two so there is no concern there. Brazil will see a drier bias over the next seven to ten days. Monsoon

rains are expected to withdraw later in April. Argentina will see additional rains Wednesday into Friday. Central Ukraine is a little wetter this week. Eastern Australia will dry down this week.

Last

7 days

World

Weather Inc.

MOST

IMPORTANT WEATHER IN THE WORLD

- Central

and eastern Ukraine into Kazakhstan will get some rain during mid-week this week

o

Moisture totals of 0.20 to 0.75 inch and local amount over 1.00 inch will be possible

o

The moisture will help improve field conditions ahead of spring crop development in Russia’s Southern region and especially in the lower Volga River Basin where it has been driest

- Market

talk has been increasing over dryness concerns in Canada’s Prairies and the northern U.S. Plains since the planting season often begins in April

o

Drought is very serious in the region and not likely to change much for the next ten days to two weeks

- U.S.

hard red winter wheat areas will receive waves of rain and a little snow again this week further ensuring a favorable environment for crop recovery from drought and extreme cold during the winter and autumn

o

Today and early Tuesday will be wettest with lighter showers occurring erratically the remainder of this week

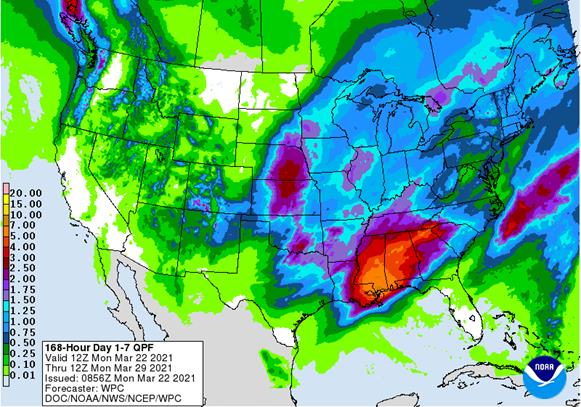

- U.S.

Delta, Midwest and southeastern states will experience waves of rain in the coming week to ten days

o

Sufficient drying time is expected between events for “some” fieldwork, but warming is needed to accelerate evaporation so that drying and planting can occur faster

- No

planting is expected in the Midwest until next month - Some

fieldwork has occurred well recently in the lower Delta and southeastern states, but in order for that process to continue favorably warm temperatures and infrequent rain would be best for the region

- Farmers

will continue to advance around the precipitation - West

and South Texas and the Texas Coastal Bend will not be seeing much precipitation during the next couple of weeks, despite a few showers

o

Dryness in each of these areas will remain a concern for long term farming activity

- Another

dry region in the U.S. is in the Yakima Valley of central Washington and from there southward into the heart of Oregon where dryness remains notable, despite some periodic precipitation events during the winter - U.S.

Midwest weather will be active enough this week to maintain a wet field bias, but that is not unusual for this time of year.

o

Drier and warmer weather will be needed in April to get fieldwork to evolve normally

- U.S.

weather during the weekend was drier biased and that was welcome after recent moisture abundance

o

No precipitation fell in the Great Plains, Midwest, Delta or interior parts of the southeastern states

o

Some rain fell from northeastern Florida to southern South Carolina with a few 1.00- to 2.28-inch amounts resulting

- Some

rain also fell in eastern North Carolina and southern Virginia

o

Rain was reported in the northwestern U.S., but not in the Yakima Valley or areas southward into central and eastern Oregon

o

Dry conditions also occurred in the southwestern United States

- Temperatures

were unusually warm in the northern Plains and parts of Canada’s Prairies during the weekend with highs in the 60s and lower 70s Fahrenheit

o

Drought in these areas continues to be a great concern

o

Some relief is expected later this spring, but dryness will likely return later this summer

o

Rain was noted briefly from eastern North Dakota and northwestern Minnesota into southeastern Manitoba Sunday, but resulting rainfall through mid-afternoon Sunday had not been more than 0.20 inch leaving the region drier biased

- Argentina

will receive some additional rain Wednesday into Friday with a few lingering showers in the far northeast Friday

o

Amounts will be lightest from southern Cordoba into northwestern Santa Fe where less than 0.60 inch will result

o

Amounts will be greatest in the central and northeast where 0.70 to 2.00 inches are expected with local totals of 2.00 to 5.00 inches

o

Additional showers are expected late next week into the following weekend, but this event will be more erratic and light with 0.10 to 0.75 inch and locally more is expected

o

Net drying is expected from this weekend into mid-week next week

o

Temperatures will be seasonable this week and a little cooler next week

- Argentina

rainfall was restricted in the west and south Friday through Sunday, but temperatures were mild which kept drying rates slow

o

Highest afternoon temperatures were in the 70s Fahrenheit followed by lows in the upper 40s and 50s

o

Rainfall ranged from 0.05 to 0.30 inch

- Northeastern

Argentina reported greater rainfall during the weekend with 0.68 to 2.40 inches which was sufficient to bolster topsoil moisture especially in Chaco where the greatest amounts occurred and helped to further improve late season crop conditions - Argentina’s

bottom line remains favorable for late season crop development, although there will be a few pockets of moisture stress most likely in the southwest part of the nation. Soil moisture will carry crops through the drier days and the lack of excessive heat will

keep evaporation rates low enough to conserve that soil moisture. The worst of this year’s crop stress and greatest pressure to reduce production in 2021 has passed and crops will finish the growing season without much further decline in potential yield.

- Brazil

rainfall during the weekend was a little more restrictive compared to last week which was perfect for promoting a drier environment for the maturation and harvest of soybeans and the planting of late season Safrinha corn

o

Rainfall was not more than 0.72 inch in key crop areas except in western and northern Sao Paulo and northern Parana where 1.50 inches resulted

- Rio

Grande do Sul, Brazil was another exception where western and southern crop areas received 1.00 to 2.28 inches rain and that helped bolster topsoil moisture for better field and crop conditions after recent drying - Brazil’s

center south, center west and interior southern crop areas will experience a week’s worth of additional drying before showers and thunderstorms return next week; some computer forecast models suggest ten days will pass without significant rain

o

The exception will be northwestern Mato Grosso where rain is expected to continue periodically

o

Temperatures will be seasonable

o

Some longer range forecast models have suggested below average rainfall might continue for six weeks even when rainfall returns next week

- Remember

below average rainfall in Brazil does not mean drought

o

Concern will rise about long term soil moisture in Brazil especially if monsoonal rain withdraws normally in late April

- The

below average precipitation and normal end to the rainy season could raise the potential for crop moisture stress for Safrinha corn, cotton and other late season crops - South

Africa’s greatest rainfall over the next two weeks will occur Tuesday through Thursday of this week when 0.20 to 0.80 inch and local totals to 1.50 inches results

o

Sporadic showers will occur most other days through April 5 will not likely produce enough precipitation to counter evaporative moisture

- South

Africa showers scattered through 45% of the nation Friday through Sunday with rainfall varying up to 0.75 inch

o

Much of the rain was not great enough to counter evaporative moisture losses

o

Temperatures were seasonable

- India

showers that occurred Friday through Sunday will continue into Tuesday in central and northern parts of the nation

o

Resulting rainfall was no more than 0.50 inch during the weekend and another 0.05 to 0.40 inch of moisture is expected by Wednesday

o

The moisture has been good for filling crops and for holding down temperatures and restricting crop stress

o

Dry and warm weather will evolve later this week into early April promoting faster drying rates, crop maturation and eventual early harvesting

- China

soil conditions remain favorably moist and weekend precipitation will help to ensure that the moisture situation remains good into April

o

Soil temperatures are rising sufficiently to bring wheat and northern rapeseed out of dormancy, although new crop development will be restricted until greater warming evolves

o

Weekend rain was greatest in southern Inner Mongolia and northern most parts of the Yellow River Basin and North China Plain where 0.25 to 1.18 inches

- Local

totals reached up to 1.57 inches

o

Rain also fell in the Northeast Provinces where moisture totals of 0.10 to 0.72 inch resulted with local totals to 1.58 inches

o

Rain fell in the Yangtze River Basin, as well, with 0.40 to 1.18 inches resulted with a few amounts of 1.20 to 3.46 inches

o

Net drying occurred in Guangdong, southern Jiangxi, western and southern Fujian, western Guangxi, most of Guizhou and all of Yunnan

o

Temperatures were mild to cool except in the southern most provinces from Yunnan to Fujian where 80- and lower 90-degree highs were noted

o

Yunnan is still too dry and needs significant rain to ease long term dryness and to support spring planting and crop development. Other provinces near the coast in far southern China are also drying out and will need timely rain

soon

- China

will be drier than usual early this week and then two waves of rain will overspread the nation from late this week through next week maintaining a very good moisture profile in the majority of the nation

o

Temperatures will be warmer than usual

o

Rain totals in this coming week will vary from 0.10 to 0.75 inch with local totals of 1.00 to 2.00 inches

o

Additional drying is likely from Yunnan through Guangdong to southern Fujian during the coming week with “some” increase in rainfall to come in the following week. Other areas will stay favorably moist, although the Yangtze River

Basin and some areas in the interior south will become a little too wet next week as heavy rain evolves

- Eastern

Australia will receive additional rain today resulting in a notable increase in soil moisture for New South Wales and southern Queensland

o

The moisture will be good for future winter crop planting and for a few of the latest maturing summer crops, but concern will continue moderately high over the quality of early maturing cotton quality

o

Drier weather the remainder of this week into next week will be good for summer crop maturation and cotton quality

- New

South Wales, Australia coastal areas received excessive weekend rainfall with amounts through this morning varying from 2.75 to 14.60 inches resulting in some significant coastal flooding

o

One location reported 22.83 inches of rain

o

Flooding was widespread along the coast and may have damaged personal property and infrastructure

o

Crop areas did not receive nearly as much rain and net drying occurred in the majority of production areas until Sunday afternoon and early today when rainfall varied up to 1.18 inches in northern and central New South Wales and

up to 1.07 inches in southern Queensland

o

Net drying occurred elsewhere in the nation

- North

Africa received some additional rain of significance during the weekend improving topsoil moisture for use this spring as more aggressive crop development begins

o

Rain totals of 0.57 to 1.30 inches occurred in northeastern Morocco with a local amount of 2.87 inches

o

Northern Tunisia also reported 1.00 to more than 3.00 inches while rainfall of 0.08 to 0.75 inch occurred in northern Algeria with a local total to 1.30 inches.

- Southwestern

Morocco was dry

o

Dryness remains a concern for northwestern Algeria and especially southwestern Morocco where significant rain is needed to improve crop and soil conditions

- North

Africa rainfall will be limited to Tunisia and northeastern Algeria today followed by dry weather through the end of this week

o

Scattered showers will return to Morocco this weekend into next week, although the daily precipitation will be erratic and light

- Ivory

Coast, Ghana, Benin, Cameroon and southern Nigeria will receive waves of rain in the next ten days

o

New rain totals will vary from 0.50 to 3.00 inches and locally more will be supportive of coffee and cocoa flowering and help increase soil moisture for future rice, sugarcane and cotton production

o

Cameroon may receive excessive rainfall late this week into next week

- East-central

Africa rainfall will be erratic and light for a while

o

Crop conditions are best in Tanzania

o

Rain is needed most in Ethiopia, although this is the end of their dry season

- Southeast

Asia rainfall will occur relatively normally over the next two weeks

o

Mainland areas will experience increasing shower activity, although greater rainfall would be welcome

- The

resulting rainfall will be sporadic and light with net drying probably continuing in many areas for a while longer

o

Philippines rainfall will occur routinely during the next ten days with some local flooding possible in the north

o

Indonesia and Malaysia weather will occur often enough to support most crop needs

- Northern

parts of Peninsular Malaysia still need rain most significantly - New

Zealand weather will be dry with seasonable temperatures early this week and then scattered showers will begin to evolve later this week into next week

o

The nation’s soil moisture is drifting farther below average

- Middle

East precipitation will continue greatest in Turkey while Iraq, Iran and Syria continue in a net drying mode along with areas south into Israel and Jordan - Europe

precipitation in the coming week will be lighter and less frequent than usual while temperatures are seasonable

o

Some net drying is expected, but timely rain may return next week

o

Spain is drying down most significant and will need some moisture soon to protect long term crop development

o

Soil moisture in most of the continent is rated favorably and will continue rated that way over the next two weeks

o

Warming is needed to bring a larger portion of winter crops out of dormancy

- Spain,

western France and a few areas in Italy and Greece are warm enough for some crop development, but other areas need to warm up - Frost

and freezes were noted in much of the continent during the weekend, although no damage to crops resulted - Mexico

drought conditions are still prevailing, although the impact on winter crops is low due to irrigation

o

Water supply is low in some areas and a notable improvement in rainfall is needed, but not very likely this week

- Some

increase in precipitation is possible in the east and south next week, although confidence is low

o

Dryland winter crops are stressed and will yield poorly

o

Freeze damage is common in northern parts of the nation due to a couple of cold surges this winter

o

Rain in the coming week will be mostly confined to the east coast and temperatures will be seasonable with a slight warmer bias in the driest areas

- Central

America precipitation will continue greatest along the Caribbean Coast and in Guatemala while the Pacific Coast receives the lightest and most erratic rainfall, but some precipitation will fall especially in Costa Rica and Panama. - Southern

Oscillation Index has been falling and was at -1.33 this morning. The index is expected to level off for a while this week with some rise in the index possible.

- Southeastern

Canada’s corn, soybean and wheat production areas are favorably moist and will stay that way for a while

o

Additional rain is expected this week with temperatures above average

- Canada’s

Prairies will get some shower activity in the next ten days, but resulting rainfall will often be less than usual and temperatures will continue warm biased

Source:

World Weather inc.

Bloomberg

Ag Calendar

Monday,

March 22:

- USDA

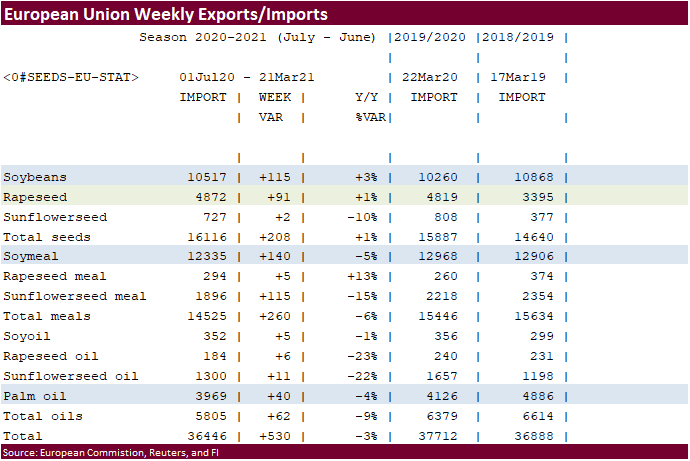

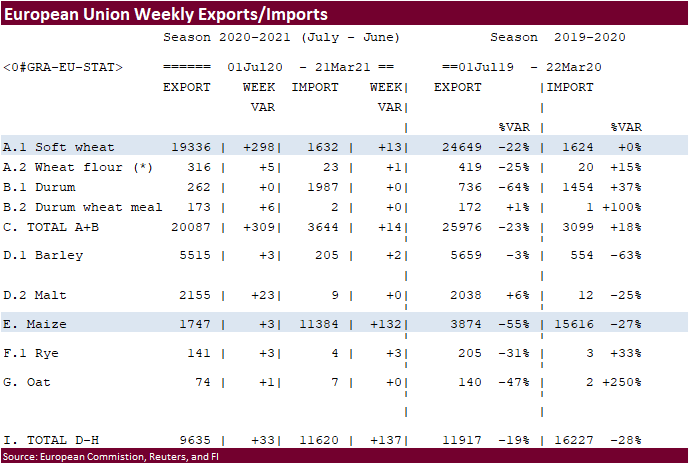

Export Inspections – corn, soybeans, wheat, 11am - EU

weekly grain, oilseed import and export data - U.S.

cold storage data — pork, beef, poultry - Ivory

Coast cocoa arrivals

Tuesday,

March 23:

- Bursa

Malaysia Derivatives virtual palm oil conference 2021, day 1 - HOLIDAY:

Pakistan

Wednesday,

March 24:

- EIA

weekly U.S. ethanol inventories, production - Bursa

Malaysia Derivatives virtual palm oil conference 2021, day 2 - U.S.

poultry slaughter - EARNINGS:

JBS - HOLIDAY:

Argentina

Thursday,

March 25:

- USDA

weekly crop net-export sales for corn, soybeans, wheat, cotton, pork, beef, 8:30am - Seminar

on sustainable palm oil in India by the Solvent Extractors’ Association and the Malaysian Palm Oil Board - International

Grains Council monthly report - Port

of Rouen data on French grain exports - Malaysia’s

March 1-25 palm oil export data - USDA

hogs & pigs Inventory, red meat production

Friday,

March 26:

- ICE

Futures Europe weekly commitments of traders report (6:30pm London) - CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm - FranceAgriMer

weekly update on crop conditions

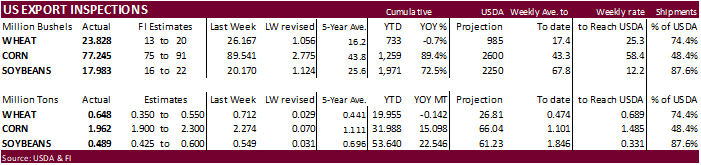

USDA

inspections versus Reuters trade range

Wheat

648,485 versus 325000-575000 range

Corn

1,962,118 versus 1600000-2200000 range

Soybeans

489,405 versus 300000-600000 range

China

took only 7,663 tons of soybeans while shipments of corn were 418,000 tons.

GRAINS INSPECTED AND/OR WEIGHED FOR EXPORT

REPORTED IN WEEK ENDING MAR 18, 2021

— METRIC TONS —

————————————————————————-

CURRENT PREVIOUS

———–

WEEK ENDING ———- MARKET YEAR MARKET YEAR

GRAIN 03/18/2021 03/11/2021 03/19/2020 TO DATE TO DATE

BARLEY

0 0 49 31,023 30,377

CORN

1,962,118 2,274,441 868,864 31,988,525 16,890,464

FLAXSEED

0 0 0 509 520

MIXED

0 0 0 0 0

OATS

699 0 0 3,192 3,243

RYE

0 0 0 0 0

SORGHUM

71,199 284,744 101,077 4,130,791 1,638,736

SOYBEANS

489,405 548,951 587,398 53,639,990 31,094,062

SUNFLOWER

0 0 0 0 0

WHEAT

648,485 712,158 354,466 19,954,937 20,097,386

Total

3,171,906 3,820,294 1,911,854 109,748,967 69,754,788

————————————————————————

CROP

MARKETING YEARS BEGIN JUNE 1 FOR WHEAT, RYE, OATS, BARLEY AND

FLAXSEED;

SEPTEMBER 1 FOR CORN, SORGHUM, SOYBEANS AND SUNFLOWER SEEDS.

INCLUDES

WATERWAY SHIPMENTS TO CANADA.

Canada

Feb Wholesale Trade Most Likely Fell 0.4% – StatsCan Flash Estimate

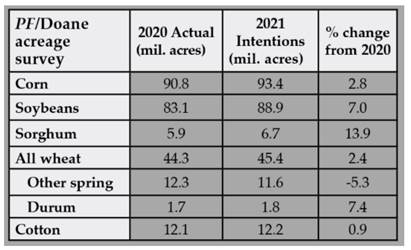

US

area: IHS

Markit forecast U.S. 2021 corn plantings at 94.294 million acres, up 3.8% from the 90.819 million corn acres in 2020. Soybean plantings for 2021 was estimated at 89.730 million acres, 8% higher from 83.084 million acres in 2020.

ProFarmer

crop results via internet article

- Corn

ended 8.75 cents lower basis May after seeing a late rally last week and lack of news. Soybean/corn spreading should be noted. Good precipitation across the US Midwest is beneficial for upcoming plantings. North Carolina (US east coast) will see a cargo

of Turkish corn hit the shores this week. There were no USDA 24-hour sales. Two private groups expect the US corn area to end up above 93 million acres (93.4 and 94.3 million). Brazil winter corn is about 90% planted. Crop conditions for SA’s corn crops

improved over the past week. - USDA

export inspections for soybeans were within expectations. China took only 7,663 tons of soybeans while shipments of corn were 418,000 tons.

- May

corn support is now seen at $5.3950. - April

options expire this Friday. - USDA

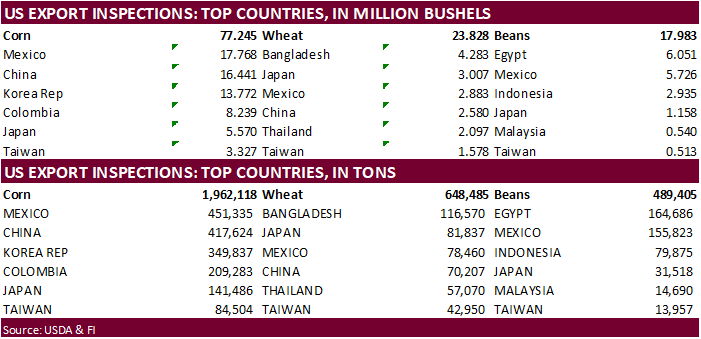

US corn export inspections as of March 18, 2021 were 1,962,118 tons, within a range of trade expectations, below 2,274,441 tons previous week and compares to 868,864 tons year ago. Major countries included Mexico for 451,335 tons, China for 417,624 tons, and

Korea Rep for 349,837 tons. - USDA

hog and pig report estimates from Bloomberg: Hog inventory seen falling to 76.059 million head vs 76.179 last March. Breeding inventory seen down 1.3% y/y, and market hogs seen falling 0.1% y/y. The pig crop seen 0.5% higher y/y. March-May farrowing intentions

seen down 0.8% y/y, and June-Aug. seen falling 0.5% y/y. Report due out March 25.

Export

developments.

- There

were no USDA 24-hour sales.

Updated

3/16/21

May

corn is seen in a $5.35 and $5.75 range.

July

is seen in a $5.10 and $5.75 range.

December

corn is seen in a $3.85-$5.50 range.

- Nearby

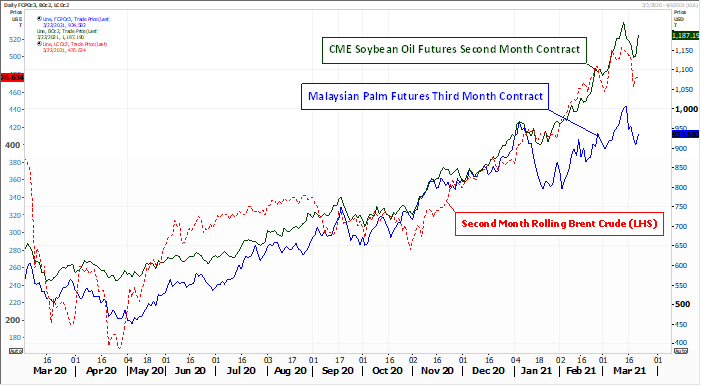

soybeans were supported limit up May soybean oil. Synthetic just before the close was 57.25. May SBO hit its highest level since September 2012. Talk of tight US soybean oil stocks and rising SBO interior US and US Gulf basis firmed up prices overnight

into the day session. The funds ran it higher during afternoon trading. In coming weeks look for traders to increase chatter over RVO requirements and surge in SBO use for renewable fuel production. Some think USDA is underestimating 2020-21 US SBO stocks

by at least 200 million pounds. We think it could easily be downward adjusted by the May USDA S&D by 100 million pounds. USDA may add renewable SBO use to its balance sheet in May, but keep in mind it will come out of the food category. Offshore values

were leading CBOT SBO 36 points higher and meal $4.30 short ton lower. Malaysian palm futures rallied about 1% overnight (+113 MRY & cash up $22.50) after falling around 10% last week. USDA export inspections for soybeans were within expectations. China

took only 7,663 tons of soybeans while shipments of corn were 418,000 tons.

- May

soybeans ended 1.25 cents higher, May soybean oil 250 points higher and May soybean meal $11.30 short ton lower. Spreads were active (see attached after text).

- U.S.

green energy push sets global edible oils alight, raises food inflation fears – Reuters

https://www.reuters.com/article/uk-global-vegoils-prices-idUSKBN2BB06M

- News

was slow over the weekend. - USDA

US soybean export inspections as of March 18, 2021 were 489,405 tons, within a range of trade expectations, below 548,951 tons previous week and compares to 587,398 tons year ago. Major countries included Egypt for 164,686 tons, Mexico for 155,823 tons, and

Indonesia for 79,875 tons. - AmSpec

reported Malaysian palm exports for the March 1 – 20 period rose 6.8 percent to 745,260 tons from 697,794 tons month earlier. ITS reported 734,463 tons, up 5.2%.

- AgRural

reported 59% of Brazil’s soybean crop had been harvested vs. 46% previous week and 66% year ago. 90% of Brazil’s corn crop (winter) had been planted).

- Safras:

Brazil soybean production 112.8MMT, down from 113.5 previous. - Malaysian

palm futures rallied about 1% overnight (+113 MRY & cash up $22.50) after falling around 10% last week.

- There

were no changes to CBOT registrations. - Richardson

International plans to double its canola crushing capacity at Yorkton, Saskatchewan, to 2.2 million tons annually, according to Reuters.

USDA

Attaché: Indonesia: Oilseeds and Products Annual

Export

Developments

- Results

awaited: Iran seeks 30,000 tons of sunflower oil and 30,000 tons of soybean oil on March 18 for March and April shipment.

Updated

3/22/21

May

soybeans are seen in a $13.75 and $14.75 range.

May

soymeal is seen in a $385 and $425 range.

May

soybean oil is seen in a 54 and 58.00 cent range (up 150 & 200).

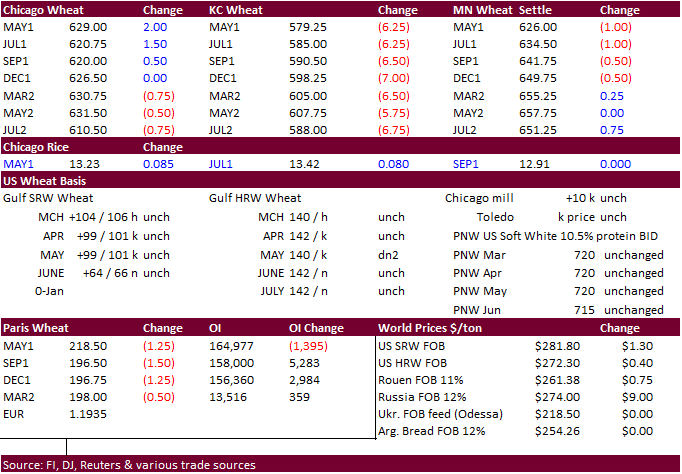

- CBOT

Chicago wheat approached a three month low, but the May contract closed 0.25 cent higher and July unchanged, in part to good weather for the US and Black Sea region. Both Ukraine (wheat down $7/ton) and Russian (12.5% protein wheat off $7/ton) cash export

prices for wheat and barley trended lower last week. Egypt might be in for wheat this week. Paris wheat hit a 5-week low.

- Chicago

May wheat futures remain below its 100-day MA. Next support level for May Chicago is now seen at $616. KC May ended 7.25 cents lower and MN May finished 1.0 cent lower.

- USDA

US all-wheat export inspections as of March 18, 2021 were 648,485 tons, above a range of trade expectations, below 712,158 tons previous week and compares to 354,466 tons year ago. Major countries included Bangladesh for 116,570 tons, Japan for 81,837 tons,

and Mexico for 78,460 tons. - China

sold 1.6 million tons of wheat at auction from 4.020 million tons offered (41%) at an average price of 2,356 yuan per ton ($362.04/ton). 43 million tons of wheat had been sold from auction since June 22, 2021.

- Egypt

said they have sufficient wheat reserves to last until the end of June. - EU

May milling wheat was 1.00 lower at 218.25 euros. Support is seen at 215.00.

Export

Developments.

- Results

awaited: Algeria’s ONAB seeks 40,000 tons of animal feed barley on March 18 for April 15-30 shipment. - Jordan

is back in for feed barley on March 23. Possible shipment combinations are Oct. 1-15, Oct. 16-31, Nov. 1-15 and Nov. 16-30.

Rice/Other

·

South Korea’s Agro-Fisheries & Food Trade Corp. seeks 208,217 tons of rice, on March 25 for arrival in South Korea in 2021 between May 1 and Oct. 31. 64,444 tons of non-glutinous brown rice is sought

from the United States. Rest from Thailand, China, Australia and Vietnam.

·

Bangladesh also seeks 50,000 tons of rice on March 28.

·

Syria seeks 25,000 tons of white rice on March 29, from China or Egypt.

·

Syria seeks 39,400 tons of white rice on April 19. Origin and type might be White Chinese rice or Egyptian short grain rice.

Updated

3/18/21

May

Chicago wheat is seen in a $6.15‐$6.75 range

May

KC wheat is seen in a $5.65‐$6.60 range

May

MN wheat is seen in a $6.15‐$6.50 range

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International

One Lincoln Center

18 W 140 Butterfield Rd.

Oakbrook Terrace, Il. 60181

W: 312.604.1366

ICE IM:

treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered

only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making

your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors

should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or

sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy

of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.