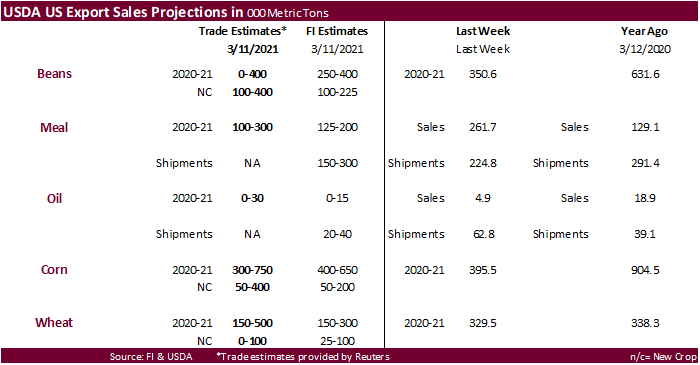

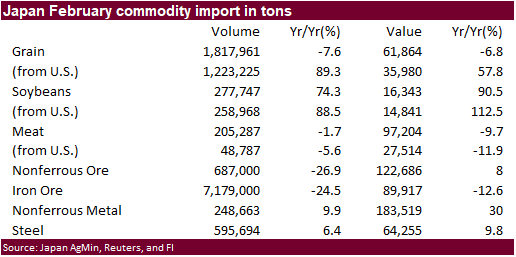

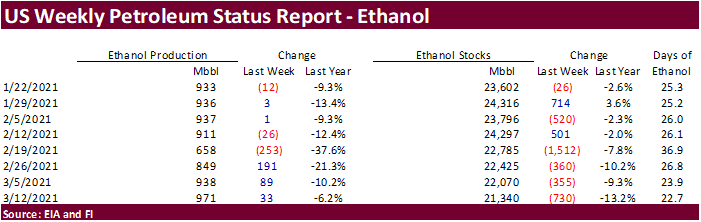

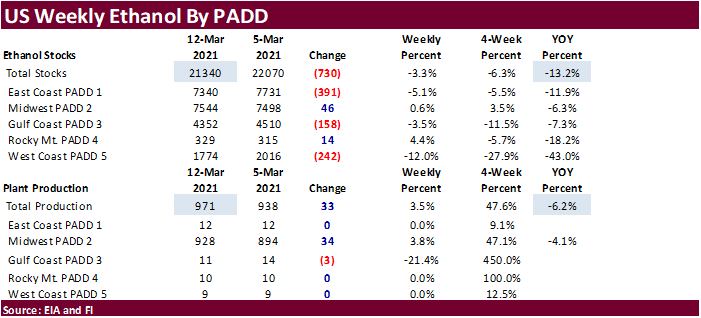

PDF attached includes US cash crush, Broiler Report, and US ethanol update.

US

FOMC Benchmark Interest Rate Unchanged; Target Range Stands At 0.00% – 0.25%. Lower trade in most CBOT agriculture commodity markets with exception of nearby corn and rice. By 2:30 PM CT, the USD fell by 36 points. US stocks traded mix until a late rally.

Gold was higher and energy markets remained lower.

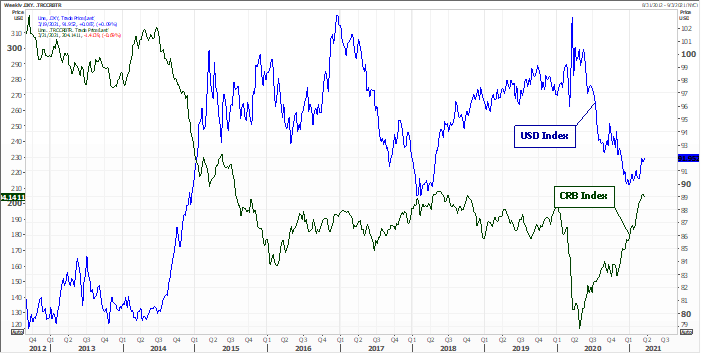

![]()

USD

versus CRB Index

Source:

Reuters and FI

World

Weather Inc.

- Argentina

has seen significant relief to dryness over the past two days and more is expected Friday into the weekend and again during the second half of next week

o

The three periods of rain will leave the nation favorably moist for late season summer crop development

- However,

production cuts did occur during the past couple of weeks in the driest areas and the speculation over that impact will continue for a while - Brazil’s

weather outlook is drier for next week and into the last week of this month in center south, interior southern and some center west locations

o

The drier bias comes along a little late, but soybean harvesting and Safrinha corn planting will conclude during that period of time

- Late

planted corn will not likely yield very well, but some crop is better than none – from the Brazilian farmer perspective with prices staying high

o

World Weather, Inc. still believes the monsoon season will end normally with no extended periods of rain this year to help the late crop

o

Previously planted Safrinha and late full season crops should benefit from the coming two weeks of weather

- An

active U.S. weather pattern will leave the Midwest and northern Delta too wet for early season fieldwork in early April

o

Some local flooding is expected periodically

- U.S.

temperatures will be warmer than usual in the northern Plains and upper Midwest as well as in neighboring Canada during the coming week - Paraguay

and northern Rio Grande do Sul, as well as western Parana and far southern Mato Grosso do Sul received rain overnight that helped to bolster soil moisture after recent drying

o

The precipitation reduced crop stress and will improve crop conditions

o

Additional rain will linger today in interior southern Brazil and southeastern Paraguay with more expected this weekend into early next week

- The

bottom line should be favorable for crops that have been stressed by dryness recently - U.S.

hard red winter wheat improvements are expected to be significant in the next two weeks especially with a couple of follow up rain events to the more significant early week precipitation event

o

Some rain and snow will occur today followed by some drier weather until early next week when the next opportunity for rain evolves

o

Southern portions of the Plains still have need for dryness easing rain

- This

includes Oklahoma and northern Texas as well as the western Texas Panhandle - U.S

northwestern Plains and Canada’s Prairies will continue quite dry for the next ten days, despite a few brief showers of snow and rain

o

Better weather is expected in April and May that should prove helpful in getting crops planted this year

- West

and South Texas still need significant rain along with the Texas Coastal Bend

o

Some rain has fallen recently in parts of West Texas, but more significant rain and more generalized rain will be needed before planting begins in cotton, sorghum and corn areas in late April and May

- A

few showers will occur in the Rolling Plains and Low Plains of West Texas Sunday into Monday with a few more possible during mid-week next week - Resulting

rainfall will be low

o

South Texas and the Texas Coastal Bend will struggle for moisture over the next couple of weeks

- U.S.

Delta and southeastern states will experience a more active weather pattern over the next week slowing fieldwork after a nice start in some areas during the latter part of last week and during the weekend

o

The southeastern states should see the best mix of rain and sunshine for fieldwork and early crop development

o

Portions of the Delta will receive a little too much rain too often and the same is true for the Tennessee River Basin

- U.S.

Pacific Northwest has some moisture deficits that still need to be reduced, but mountain snowpack is good for adequate runoff to fuel irrigation systems this spring - California

snowpack and snow water equivalents are still below average with little change likely, despite some occasional precipitation events - Concern

over drought in the western U.S. remains, despite some precipitation recently and that which is still yet to come

o

Drought will prevail through the growing season this year

- India

will receive some brief periods of light rainfall Thursday through early next week

o

The moisture will slow crop maturation, but may benefit a few immature crops still filling

- Most

of the precipitation will be too brief and light to have a lasting impact - China’s

southern rapeseed crop would benefit from more sunshine and warmer temperatures, but the long term outlook is favorable - China’s

northern rapeseed and majority of key winter wheat production areas are poised for aggressive development this spring because of good establishment in the autumn and better than usual winter precipitation along with minimal winterkill - Eastern

Australia’s frequent precipitation pattern expected into late this month is likely to raise concern over open boll cotton fiber quality and some harvest delays

o

The moisture will be excellent for late maturing summer crops including sorghum and it will lift soil moisture and water supply for wheat, barley and canola planting that begins in late April

- Middle

East precipitation will continue greatest in Turkey and may increase in Afghanistan this week while Iraq, Iran and Syria continue in a net drying mode along with areas south into Israel and Jordan - Europe

precipitation in the coming ten days will be wettest in southern parts of the continent; including areas from Italy and eastern France into the Balkan Countries

o

Temperatures will be cooler than usual

o

Spain is drying down and will need some moisture soon to protect long term crop development

- Spain

and Portugal are drying out and will need a boost in precipitation later this month as seasonal warming becomes more aggressive and begins to accelerate net drying - Western

parts of the CIS will experience frequent bouts of light rain and snow during the coming ten days

o

The precipitation will continue to support abundant soil moisture across many areas

o

Temperatures will be near normal allowing some warming to occur in far southern crop areas in Ukraine, Moldova and Russia’s Southern Region where soil temperatures may rise enough to induce some greening of wheat and other winter

crops in early April.

- North

Africa weather will include a mix of rain and sunshine during the next two weeks

o

A boost in soil moisture is needed in northeastern Algeria, parts of Tunisia and southwestern Morocco

o

Some rain is expected periodically starting Thursday and lasting into next week with some of the drier areas in Algeria benefiting

- Ivory

Coast, Ghana, Benin, Cameroon and southern Nigeria will receive waves of rain in the next ten days

o

New rain totals will vary from 0.50 to 3.00 inches and locally more will be supportive of coffee and cocoa flowering and help increase soil moisture for future rice, sugarcane and cotton production

- East-central

Africa rainfall will be erratic and light for a while

o

Crop conditions are best in Tanzania

o

Rain is needed most in Ethiopia, although this is the end of their dry season

- South

Africa will experience slowly increasing rainfall during the coming week to ten days with temperatures mostly near to above average

o

The recent drying trend encouraged early season crop maturation while subsoil moisture and irrigation supported late season crops

o

Summer crop conditions will remain favorably rated as long as the moisture boost occurs as advertised

- Mexico

drought conditions are still prevailing, although the impact on winter crops is low due to irrigation

o

Water supply is low in some areas and a notable improvement in rainfall is needed, but not very likely

o

Dryland winter crops are stressed and will yield poorly

o

Freeze damage is common in northern parts of the nation due to a couple of cold surges this winter

o

Rain in the coming week will be mostly confined to the east coast and temperatures will be seasonable with a slight warmer bias in the driest areas

- Central

America precipitation will continue greatest along the Caribbean Coast and in Guatemala while the Pacific Coast receives the lightest and most erratic rainfall, but some precipitation will fall especially in Costa Rica and Panama. - Southeast

Asia rainfall will occur relatively normally over the next two weeks

o

Mainland areas will experience increasing shower activity later this week

- The

resulting rainfall will be sporadic and light with net drying probably continuing in many areas for a while longer

o

Philippines rainfall will occur moderately periodically during the next ten days with some local flooding possible in the north

o

Indonesia and Malaysia weather will occur often enough to support most crop needs

- Peninsular

Malaysia needs rain most significantly - New

Zealand weather will be dry with seasonable temperatures over the coming week

o

The nation’s soil moisture is drifting farther below average

o

Rain will return to some areas next week, but greater rain may be required to restore normal soil moisture

- Southern

Oscillation Index has been falling and was at +1.99 this morning. The index is expected to drift a little lower as time moves along.

- Southeast

Canada will experience below average precipitation and above normal temperatures during the coming week to ten days - Canada

Prairies will continue drier and warmer than usual maintaining a great level of concern over drought since the region is already extremely short on moisture

Source:

World Weather inc.

Bloomberg

Ag Calendar

Wednesday,

March 17:

- EIA

weekly U.S. ethanol inventories, production - Brazil’s

Unica may release cane crush, sugar production data (tentative)

Thursday,

March 18:

- USDA

weekly crop net-export sales for corn, soybeans, wheat, cotton, pork, beef, 8:30am - Port

of Rouen data on French grain exports - China

customs to publish trade data, including import numbers for corn, wheat, sugar and pork - USDA

total milk production

Friday,

March 19:

- ICE

Futures Europe weekly commitments of traders report (6:30pm London) - CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm - FranceAgriMer

weekly update on crop conditions - U.S.

cattle on feed

Saturday,

March 20:

- China

3rd batch of Jan.-Feb. trade data, including country breakdowns for energy and commodities. No timing

FOMC

Benchmark Interest Rate Unchanged; Target Range Stands At 0.00% – 0.25%

–

Interest Rate On Excess Reserves Unchanged At 0.10%

US

IRS Plans To Delay Tax-Deadline From 15th April To Mid-May

US

Expected To Impose Additional Sanctions On Russia; May Sanction Individuals Close To Putin – CNN

US

Housing Starts Feb 1.421 Mln (est 1.560 Mln; prevR 1.584 Mln; prev 1.580 Mln)

–

US Building Permits Feb 1.682 Mln (est 1.750 Mln; prevR 1.886 Mln; prev 1.881 Mln)

Canadian

CPI (M/M) Feb 0.5% (est 0.7%; prev 0.6%)

–

Canadian CPI (Y/Y) Feb 1.1% (est 1.3%; prev 1.0%)

Canadian

Core CPI – Common (Y/Y) Feb 1.3% (est 1.4%; prev 1.3%)

–

Canadian Core CPI – Median (Y/Y) Feb 2.0% (est 2.0%; prev 2.0%)

–

Canadian Core CPI – Trim (Y/Y) Feb 1.9% (est 2.0%; prev 2.0%)

–

Canadian BoC Core CPI (M/M) Feb 0.3% (prev 0.5%)

–

Canadian BoC Core CPI (Y/Y) Feb 1.2% (prev 1.6%)

US

DoE Crude Oil Inventories (W/W) 12-Mar: 2396K (est 2700K; prev 13798K)

–

Distillate: 255K (est -2600K; prev -5504K)

–

Cushing: -624K (prev 526K)

–

Gasoline: 472K (est -3500K; prev -11869K)

–

Refinery Utilization: 7.10% (est 5.40%; prev 13.00%)

- Corn

futures traded

most of the day higher in the nearby contract(s) and lower in the back months. Lower energy markets, weakness in soybean & wheat, and expectations for a large US 2021 corn planted area weighted on the back months. Rising US/Russia geopolitical tensions also

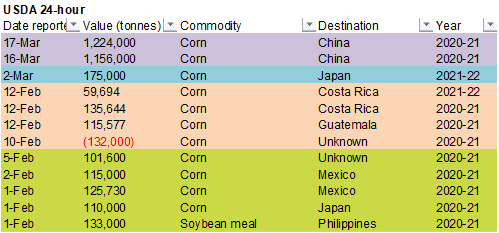

could have provided a negative sentiment. Talk of China needing additional corn for 2021 delivery was supportive pre day session open for the prompt month contract, then USDA dropped another bomb. Private exporters sold 1.224 million tons of corn to China,

bringing cumulative two-day sales to 2.380 million tons, 8.228 million tons since January 1. China committed to about 22.3 million tons of US corn after today’s sale. There is at least 14.9 million tons of US corn outstanding for China. USDA shows total

2020-21 China corn imports at 24 million tons. Bloomberg in an article overnight cited a senior analyst with a Chinese futures firm, estimating China could import 40 million tons of corn this year, up from 11 million in 2020.

- China

may have auctioned off corn yesterday from Jilin. An estimated 32 percent was talked about overnight at an average price of 2,880/yuan per ton ($11.25/bu or $443/ton). This price is higher than the average China northern cash price we show of $10.78/bu.

On December 22, China sold 103,455 tons of corn out of auction at an average price of 2,491 yuan per tons.

- Funds

bought an estimated net 3,000 corn contracts. CBOT corn volume for May and July composed of about 81 percent of today’s volume.

- Ukraine

will be able to resume poultry exports to the EU on March 20. 2020 exports were 4% higher in 2020 to 431,000 tons. - The

USDA weekly Broiler Hatchery report showed eggs set down slightly and chicks placed down 3 percent. Cumulative placements from the week ending January 9, 2021 through March 13, 2021 for the United States were 1.86 billion. Cumulative placements were down

2 percent from the same period a year earlier.

Export

developments.

- USDA

announced 1.224 million tons of 2020-21 corn sold to China.

- Taiwan’s

MFIG bought about 65,000 tons of corn, optional origin (likely Argentina) for May 27-June 15 shipment

at

an estimated premium of 264.12 cents a bushel c&f over the Chicago September contract.

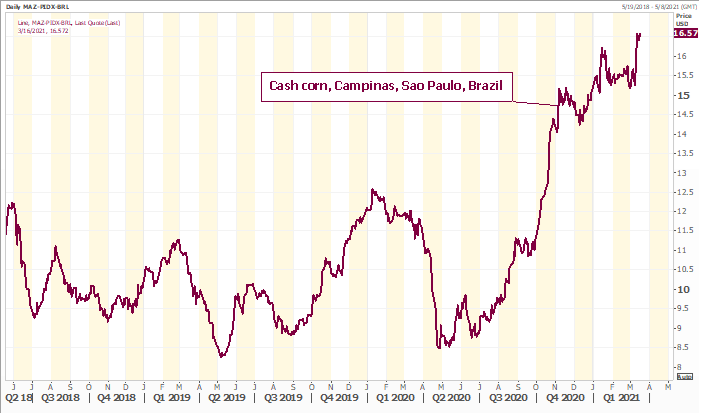

Brazil

cash corn – Campinas, Sao Paulo

Source:

Reuters and FI

Updated

3/16/21

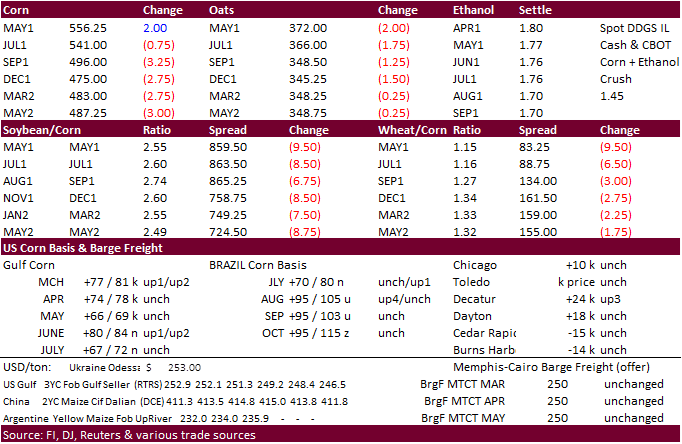

May

corn is seen in a $5.35 and $5.75 range.

July

is seen in a $5.10 and $5.75 range.

December

corn is seen in a $3.85-$5.50 range.

- CBOT

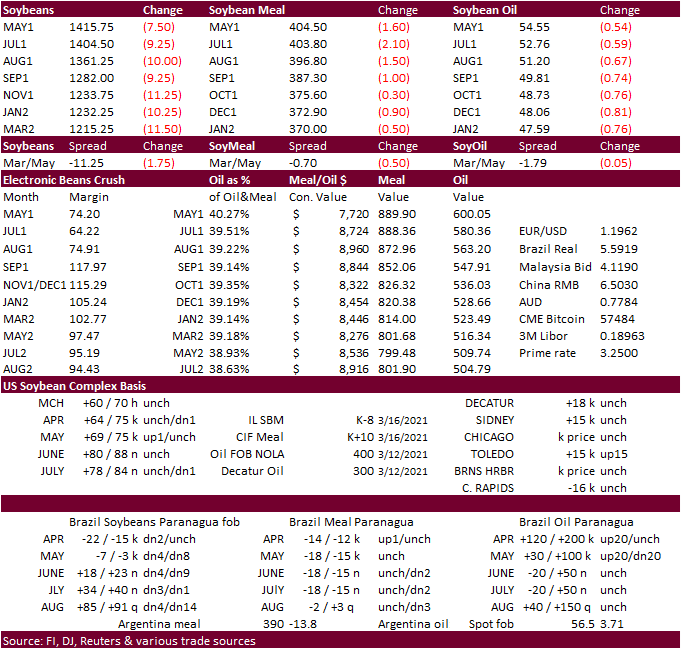

soybean complex drifted lower in part to a negative undertone in the energy market and slow US soybean exports.

- SA

weather will improve over the next week and second week of the outlook is wetter. Argentina’s Pampas long due rain event over the past few days may stabilize the soybean crop, but yields are thought to not improve, according to a meteorologist covered in

a Reuters story. - Funds

sold an estimated net 6,000 soybean contracts, sold 2,000 soybean meal and sold 4,000 soybean oil.

- China

and the US meet this week in Alaska and some think this could generate Chinese buying of US agriculture products. We may have already seen this for corn.

- Malaysia

kept its April export tax for crude palm oil at 8%, and at current values, is profitable for India to import the vegetable oil. The Southern Peninsula Palm Oil Millers’ Association forecast a large increase in March 1-15 production in Malaysia while Indonesia’s

output is also expected to rise, a Kuala Lumpur-based trader said. - Indonesia

Palm Oil Association (GAPKI) reported January palm exports was up about 20% from the previous year to 2.86 million tons but down 18% from the previous month from slowing demand from China.

Export

Developments

- Iran

seeks 30,000 tons of sunflower oil and 30,000 tons of soybean oil on March 18 for March and April shipment.

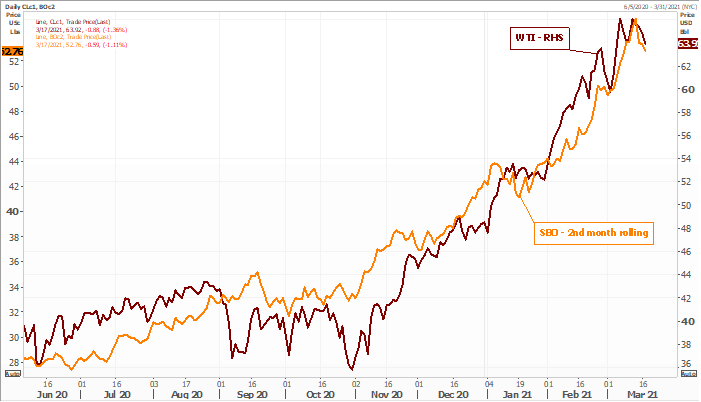

Nearby

rolling WTI vs. second month rolling soybean oil

Source:

Reuters and FI

Updated

3/16/21

May

soybeans are seen in a $13.75 and $14.75 range.

May

soymeal is seen in a $385 and $425 range.

May

soybean oil is seen in a 53.50 and 56.00 cent range.

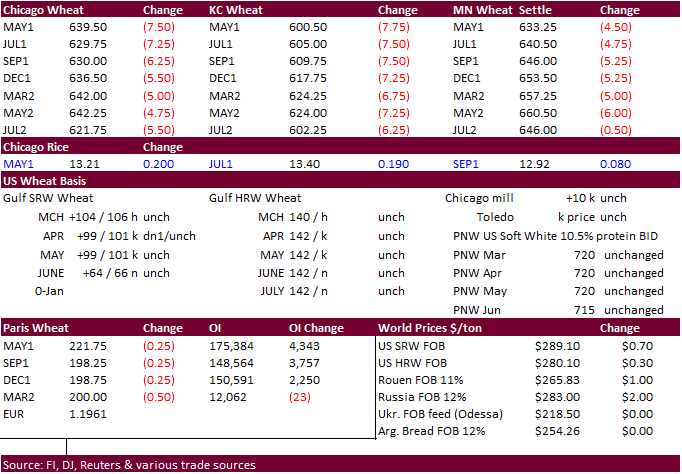

- US

wheat futures are lower on technical selling, precipitation for US HRW wheat area, and easing Black Sea cash prices earlier this week after Russia said they might be open to stepping back on export restrictions. US weather looks good for the wheat emerging

from dormancy and we look for improved crop conditions in coming weeks.

- Funds

sold an estimated net 5,000 SRW wheat contracts. - EU

May milling wheat traded 0.50 lower at 221.50 euros. - CME

Group announced they will list cash settled Ukrainian wheat futures and options contracts next month via Platts. Sunday April 11 is the launch date.

- APK-Inform

estimated Ukraine grain exports at 45.9 million tons, down from 54.98 million in 2019-20.

- SovEcon

raised its Russian forecast for 2021 wheat crop to 79.3 million tons from 76.2 million tons previously. Crop conditions are good for the Black Sea region.

- Lebanon’s

current economic situation is deteriorating rapidly, threatening the current food supply. We are hearing many grocery shops are temporarily closed and some bread makers may have to stop production. This is because the pound fell to 15,000/USD, down a third

from the previous week. It is down 90 percent since Q4 2019. Lebanon imports almost all its wheat and supplies should be good for at least two months, according to Reuters.

Export

Developments.

- Tunisia’s

state grains agency seeks 42,000 tons of optional origin durum wheat, 117,000 tons of soft wheat and 75,000 tons of animal feed barley on March 18. The durum is sought in one consignment of 25,000 tons and one of 17,000 tons for shipment between April 15 and

May 5. The soft wheat is sought in four 25,000 ton consignments and one of 17,000 tons for shipment between April 10 and May 25. The barley is sought in three 25,000 ton consignments for shipment between April 15 and May 25. (Reuters) - Algeria’s

ONAB seeks 40,000 tons of animal feed barley on March 18 for April 15-30 shipment. - Jordan

is back in for feed barley on March 23. Possible shipment combinations are Oct. 1-15, Oct. 16-31, Nov. 1-15 and Nov. 16-30.

- Japan

seeks 135,603 tons of food wheat from the US, Canada and Australia.

- Awaited:

Pakistan seeks 300,000 tons of wheat for April-August shipment and lowest offer was $285.97/ton c&f for August shipment. April was thought to be $323.97/ton.

Rice/Other

·

(new 3/16) Syria seeks 39,400 tons of white rice on April 19. Origin and type might be White Chinese rice or Egyptian short grain rice.

·

Bangladesh seeks 50,000 tons of rice on March 18.

·

South Korea’s Agro-Fisheries & Food Trade Corp. seeks 208,217 tons of rice, on March 25 for arrival in South Korea in 2021 between May 1 and Oct. 31. 64,444 tons of non-glutinous brown rice is sought

from the United States. Rest from Thailand, China, Australia and Vietnam.

·

Bangladesh also seeks 50,000 tons of rice on March 28.

·

Syria seeks 25,000 tons of white rice on March 29, from China or Egypt.

Updated

3/9/21

May

Chicago wheat is seen in a $6.25‐$6.90 range

May

KC wheat is seen in a $5.75‐$6.75 range

May

MN wheat is seen in a $6.20‐$6.65 range

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International

One Lincoln Center

18 W 140 Butterfield Rd.

Oakbrook Terrace, Il. 60181

W: 312.604.1366

ICE IM:

treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered

only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making

your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors

should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or

sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy

of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.