PDF Attached

Mato

Grosso will continue to see widespread rain delaying soybean harvesting and corn plantings. Mato Grosso soybean harvest reached 80 percent complete, 8 points below average. Argentina will see scattered showers, but the southern areas may miss out.

CBOT

agriculture markets saw a choppy trade again. China’s purchase of more than one million tons of corn announced this morning eased ideas ASF was severely hampering feed demand.

World

Weather Inc.

WORLD

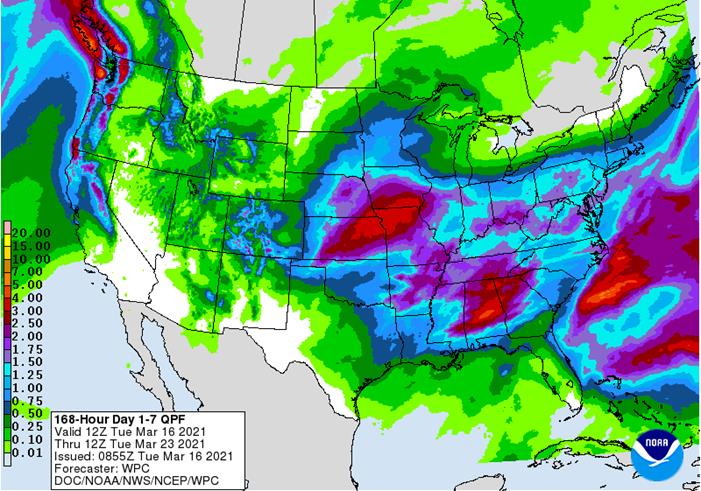

WEATHER TO WATCH

- Argentina’s

key summer crop areas from San Luis and Cordoba to western Entre Rios and northern Buenos Aires received significant rain overnight

o

Amounts of 0.35 to 1.00 inch was common with local totals of 1.00 to 2.00 inches and one spot south of Cordoba City, Cordoba getting 3.00 inches

o

Crop stress in Argentina peaked over the weekend. Monday and today’s rain event will bring relief to many areas and it will be followed by additional rain Sunday into Monday and possibly one more system late next week or into

the following weekend. Each of these events and less oppressive heat will support crop improvements

o

Summer crops are filling and maturing limiting the benefit from the moisture on production, but there may be some late season quality increases and most importantly the decline in crop conditions has ceased

- The

exception may be in the south where the wait for greater rain will continue for a while longer - Today’s

Brazil forecast keeps rain falling frequently in Mato Grosso, Goias and Tocantins through Saturday and then the frequency and more importantly the intensity of rain will lighten up helping to stop the decline in crop conditions in the wettest areas

o

Faster harvest progress and corn planting progress will also result after the greatest rain subsides, although several days of dry and warm weather are needed before aggressive fieldwork can occur

- Southern

and eastern Brazil will see a mix of rain and sunshine favoring late season crop development and supporting opportunities for additional fieldwork

o

Rio Grande do Sul will get some rain today and Wednesday with greater rainfall possible Sunday into Tuesday of next week

- Some

of this latter rainfall may be heavy, but it will help long term crop development in Rio Grande do Sul where the nation’s most immature soybeans are present - Paraguay

is dry and needs a general soaking of rain

o

Some showers will occur in the next two days with more possible late Sunday into early next week to help improve late season crop conditions

- U.S.

hard red winter wheat improvements are expected to be significant in the next two weeks especially with a couple of follow up rain events to that which occurred in the past few days

o

One storm is expected later today into Wednesday and another frontal system will bring another chance for rain early next week

- U.S

northwestern Plains and Canada’s Prairies will continue quite dry for the next ten days, despite a few brief showers of snow and rain

o

Better weather is expected in April and May that should prove helpful in getting crops planted this year

- West

and South Texas still need significant rain along with the Texas Coastal Bend

o

Some rain has fallen recently in parts of West Texas, but more significant rain and more generalized rain will be needed before planting begins in cotton, sorghum and corn areas in late April and May

- U.S.

Delta and southeastern states will experience a more active weather pattern over the next week slowing fieldwork after a nice start in some areas during the latter part of last week and into the weekend - U.S.

Pacific Northwest has some moisture deficits that still need to be reduced, but mountain snowpack is good for adequate runoff to fuel irrigation systems this spring - California

snowpack and snow water equivalents are still below average with little change likely, despite some occasional precipitation events - Concern

over drought in the western U.S. remains, despite some precipitation recently and that which is still yet to come

o

Drought will prevail through the growing season this year

- India

will receive some brief periods of light rainfall Thursday through early next week

o

The moisture will slow crop maturation, but may benefit a few immature crops still filling

- Most

of the precipitation will be too brief and light to have a lasting impact - China’s

southern rapeseed crop would benefit from more sunshine and warmer temperatures, but the long term outlook is favorable - China’s

northern rapeseed and majority of key winter wheat production areas are poised for aggressive development this spring because of good establishment in the autumn and better than usual winter precipitation along with minimal winterkill - Eastern

Australia’s frequent precipitation pattern expected into late this month is likely to raise concern over open boll cotton fiber quality and some harvest delays

o

The moisture will be excellent for late maturing summer crops including sorghum and it will lift soil moisture and water supply for wheat, barley and canola planting that begins in late April

- Middle

East precipitation will continue greatest in Turkey and may increase in Afghanistan this week while Iraq, Iran and Syria continue in a net drying mode along with areas south into Israel and Jordan - Europe

precipitation in the coming ten days will be wettest in southern parts of the continent; including areas from Italy and eastern France into the Balkan Countries

o

Temperatures will be cooler than usual

o

Spain is drying down and will need some moisture soon to protect long term crop development

- Spain

and Portugal are drying out and will need a boost in precipitation later this month as seasonal warming becomes more aggressive and begins to accelerate net drying - Western

parts of the CIS will experience frequent bouts of light rain and snow during the coming ten days

o

The precipitation will continue to support abundant soil moisture across many areas

o

Temperatures will be near normal allowing some warming to occur in far southern crop areas in Ukraine, Moldova and Russia’s Southern Region where soil temperatures may rise enough to induce some greening of wheat and other winter

crops in early April.

- North

Africa weather will include a mix of rain and sunshine during the next two weeks

o

A boost in soil moisture is needed in northeastern Algeria, parts of Tunisia and southwestern Morocco

o

Some rain is expected periodically starting Thursday and lasting into next week

- Ivory

Coast, Ghana, Benin, Cameroon and southern Nigeria will receive waves of rain in the next ten days

o

New rain totals will vary from 0.50 to 3.00 inches and locally more will be supportive of coffee and cocoa flowering and help increase soil moisture for future rice, sugarcane and cotton production

- East-central

Africa rainfall will be erratic and light for a while

o

Crop conditions are best in Tanzania

o

Rain is needed most in Ethiopia, although this is the end of their dry season

- South

Africa will experience slowly increasing rainfall during the coming week to ten days with temperatures mostly near to above average

o

The recent drying trend encouraged early season crop maturation while subsoil moisture and irrigation supported late season crops

o

Summer crop conditions will remain favorably rated as long as the moisture boost occurs as advertised

- Mexico

drought conditions are still prevailing, although the impact on winter crops is low due to irrigation

o

Water supply is low in some areas and a notable improvement in rainfall is needed, but not very likely

o

Dryland winter crops are stressed and will yield poorly

o

Freeze damage is common in northern parts of the nation due to a couple of cold surges this winter

o

Rain in the coming week will be mostly confined to the east coast and temperatures will be seasonable with a slight warmer bias in the driest areas

- Central

America precipitation will continue greatest along the Caribbean Coast and in Guatemala while the Pacific Coast receives the lightest and most erratic rainfall, but some precipitation will fall especially in Costa Rica and Panama. - Southeast

Asia rainfall will occur relatively normally over the next two weeks

o

Mainland areas will experience increasing shower activity later this week

- The

resulting rainfall will be sporadic and light with net drying probably continuing in many areas for a while longer

o

Philippines rainfall will occur moderately periodically during the next ten days with some local flooding possible in the north

o

Indonesia and Malaysia weather will occur often enough to support most crop needs

- Peninsular

Malaysia needs rain most significantly - New

Zealand weather will be dry biased and a little cooler than usual in this coming week

o

The nation’s soil moisture is drifting farther below average

- Southern

Oscillation Index has been falling and was at +2.30 this morning. The index is expected to drift a little lower as time moves along.

- Southeast

Canada will experience below average precipitation and near average temperatures during the coming week to ten days - Canada

Prairies will continue drier and warmer than usual maintaining a great level of concern over drought since the region is already extremely short on moisture

Source:

World Weather inc.

Bloomberg

Ag Calendar

Tuesday,

March 16:

- New

Zealand global dairy trade auction

Wednesday,

March 17:

- EIA

weekly U.S. ethanol inventories, production - Brazil’s

Unica may release cane crush, sugar production data (tentative)

Thursday,

March 18:

- USDA

weekly crop net-export sales for corn, soybeans, wheat, cotton, pork, beef, 8:30am - Port

of Rouen data on French grain exports - China

customs to publish trade data, including import numbers for corn, wheat, sugar and pork - USDA

total milk production

Friday,

March 19:

- ICE

Futures Europe weekly commitments of traders report (6:30pm London) - CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm - FranceAgriMer

weekly update on crop conditions - U.S.

cattle on feed

Saturday,

March 20:

- China

3rd batch of Jan.-Feb. trade data, including country breakdowns for energy and commodities. No timing

Source:

Bloomberg and FI

US

Retail Sales Advance (M/M) Feb: -3.0% (exp -0.5%; R prev 7.6%)

–

Retail Sales Ex-Auto (M/M) Feb: -2.7% (exp 0.1%; R prev 8.3%)

US

Import Price Index (M/M) Feb: 1.3% (exp 1.0%; prev 1.4%)

–

Import Price Index Ex-Petroleum (M/M) Feb: 0.5% (exp 0.4%; R prev 1.0%)

–

Import Price Index (Y/Y) Feb: 3.0% (exp 2.6%; prev 0.9%)

–

Export Price Index (M/M) Feb: 1.6% (exp 1.0%; prev 2.5%)

–

Export Price Index (Y/Y) Feb: 5.2% (exp 4.4%; prev 2.3%)

Canadian

International Securities Transactions (CAD) Jan: 1.27B (prev 5.08B)

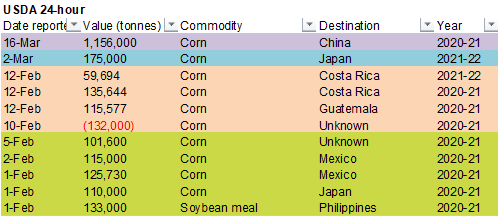

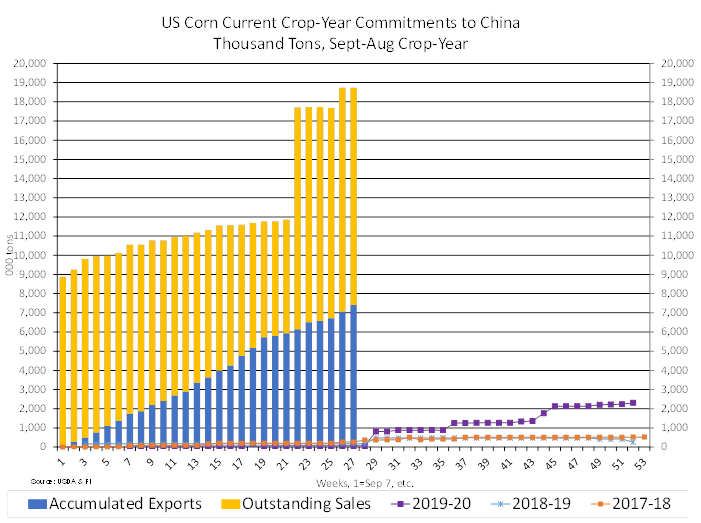

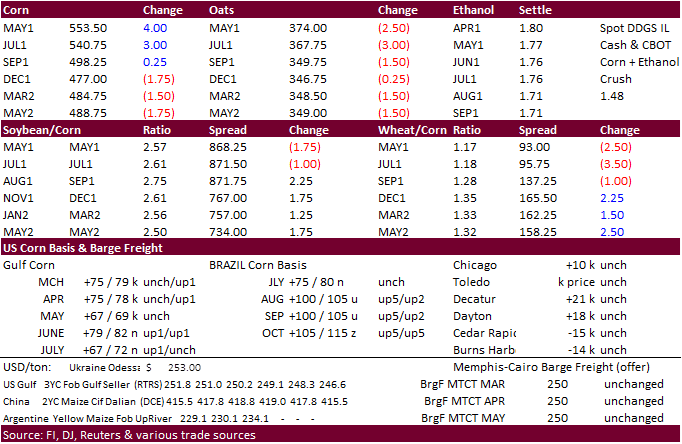

- Nearby

corn futures hit

a one week high (May up 4 consecutive days). May was up 4.75 cents, July up 4.00 and Sep up 1.25 cents. December was lower by 1.0 cent. The strength was in part to follow through buying after export inspections topped 2.2 million tons on Monday and ongoing

planting delays in Brazil. Then it was announced China bought 1.156 million tons of corn under the 24-hour system for the current marketing year. Last time we saw China show up under the 24-hour reporting system was January 29. they picked up a combined

7 million tons under the 24-H since Jan 1. China committed to nearly 20 million tons of US corn after today’s sale. There are at least 12.5 million tons outstanding. USDA shows total 2020-21 China corn imports at 24 million tons.

- USDA

estimates 2020-21 US corn exports at 2.6 billion bushels, or 66 million tons. Some are now thinking that could be as high as 70 million tons. We expect US corn inspections to remain robust over the next several weeks. It’s going to take some time for US

corn shipments to reach USDA’s 2.6 billion projection. As of March 11, 1.179 billion bushels had been shipped, or 45 percent of USDA’s export estimates.

- The

corn back months are lower from a private group calling for the US corn area to end up higher that USDA’s working estimate. Allendale estimated the corn area at 92.8 million acres, above USDA’s 92 million.

- RBOB

and WTI traded lower. USD was up slightly. - Today

was day two of CBOT expanded position limits. Some traders are looking for an eventual small increase in volatility, yet to be seen.

- China

plans to auction off corn this week and its should give the trade a glimpse of demand. African swine fever has raised feed demand alarms in recent weeks. With China buying more US corn this week, we think this may have put some minds at ease.

- Renewable

fuel (D6) credits for 2021 traded at $1.43 each on Monday, highest since at least 2013, according to Refinitiv. Biomass-based (D4) credits traded at $1.50 each, highest since at least 2014. They were both slightly lower on Tuesday. (Reuters) - A

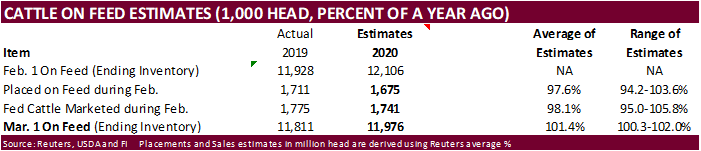

Bloomberg survey calls for USDA Cattle on Feed up 1.5% from the previous year to 11.988 million. February placements are projected down 1.9%.

- A

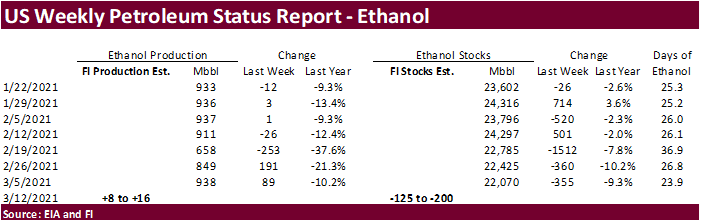

Bloomberg poll looks for weekly US ethanol production to be up 8,000 barrels (930-960 range) from the previous week and stocks up to 86,000 barrels to 22.156 million.

Export

developments.

- Under

the 24-hour reporting system, private exporters sold 1.156 million tons of corn to China for the current marketing year.

- Taiwan’s

MFIG seeks up to 65,000 tons of corn, optional origin (NA or SA) on March 17 for May 27-June 15 shipment.

China

corn sales as of March 4.

Updated

3/16/21

May

corn is seen in a $5.35 and $5.75 range. (up 15, unch)

July

is seen in a $5.10 and $5.75 range. (up 10, dn 25)

December

corn is seen in a $3.85-$5.50 range.

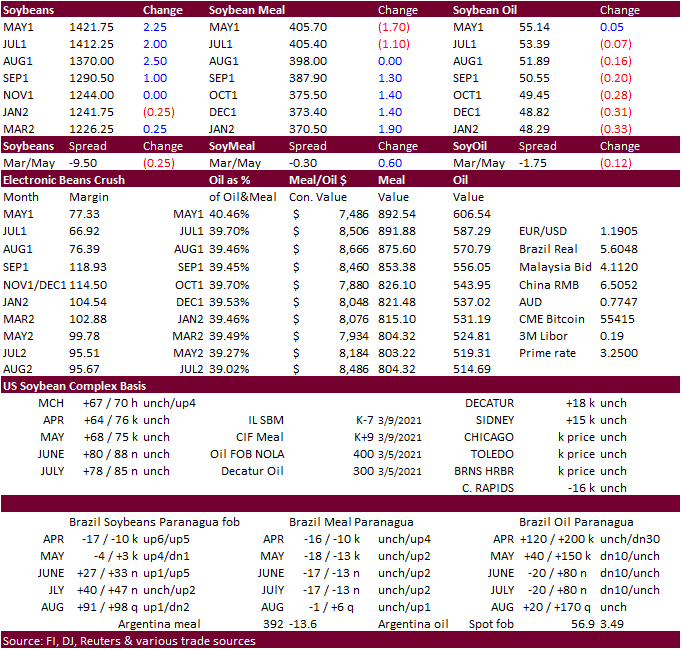

- Choppy

trade today in the CBOT soybean complex. Bull spreading supported nearby soybeans. Soybean meal was mixed with the front two months lower. Soybean oil saw a two-sided trade, ending mostly lower in the back months. May SBO managed to close unchanged.

- Soybeans

were initially lower on follow through selling after the poor NOPA crush (17-month low) and expectations for the 2021 US soybean and corn area to end up above USDA’s agriculture outlook forum.

- Based

on NOPA’s latest report, implied end of month NASS crush is expected to come in near 164.3 million bushels, down from 196.5 million in January, and lowest monthly crush since September 2019. We lowered our September-August crush from 2.195 billion bushels

to 2.190 billion, and October-September from 2.199 billion to 2.194 billion.

- Malaysian

palm futures were down 3 percent overnight after hitting a 13-year high on Monday. Reuters noted Rotterdam SBO fell about 15 euros a ton on Tuesday. Reuters: The price of crude palm oil (CPO) peaked at RM4,247.50 per ton yesterday, an all-time high in the

country’s palm oil industry history, compared to RM4,193 per ton on Thursday, which was the highest in 13 years.

- Argentina

rains has been beneficial for late planted corn and second crop soybeans. We thought we would see additional downgrades to the Argentina soybean crop in coming days, but some traders think the rain will stabilize the crop. Some people were noting the weakness

in soybeans today was related to increasing soybean shipments out of Brazil. China arrivals of Brazilian soybeans high over 2.3 million tons last week (through March 11), up about double from the same week in February.

- Brazil

exported 5.1 million tons of soybeans during first half March. AgriCensus noted another 11.5 million tons is on the books to be exported during LH March, which would put March at a record. March last year was 11.6 million tons alone.

- Brazil’s

Abiove sees 2021 soybean exports at a record 84 million tons and production at 134.8 million tons.

- AgRural

estimated Brazil soybean harvest at 46% complete as of March 11, up from 35% previous week, and 59% a year earlier. They have the crop at 133 million tons. Brazil corn plantings were 74% complete, compared to 54% week earlier and 89% a year earlier. - We

are using 133 million tons for Brazil soybeans and 46.5 million tons for Argentina (USDA @ 134 and 47.5MMT, respectively).

- SGS:

Malaysian palm shipments down 1 percent for the March 1-15 period to 549,273 tons.

Export

Developments

- Iran

seeks 30,000 tons of sunflower oil and 30,000 tons of soybean oil on March 18 for March and April shipment.

- Today

the USDA CCC seeks 2,030 tons of packaged oil on March 16 for shipment Apr 16 – May 15.

Updated

3/16/21

May

soybeans are seen in a $13.75 and $14.75 range.

May

soymeal is seen in a $385 and $425 range. (dn 15 & 25)

May

soybean oil is seen in a 53.50 and 56.00 cent range. (up

150, unch)

May/July

soybean meal spread has tightened over the past month and half

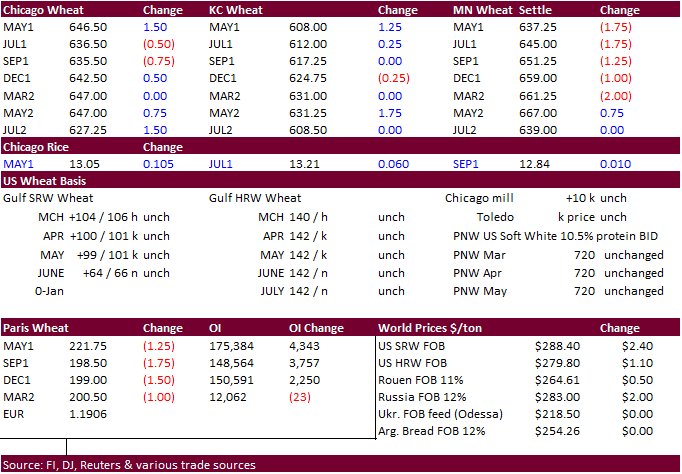

- US

wheat futures traded two-sided, ending unchanged to slightly higher in Chicago & KC and mostly lower in MN. KS and OK winter wheat conditions saw an improvement from the previous week after the US saw a great rain event late last week. EU wheat hit a one

month low. Chicago May wheat help above its 100-day MA, ending well above the 6.31 level.

- Black

Sea wheat prices have declined, as much as $10/ton according to AgriCensus due to lack of buyers and recent Egypt GASC import tender.

- Egypt’s

Minister mentioned they expect 3.5 million tons of wheat production during the harvest season in mid-April.

- Germany’s

association of farm cooperatives estimated the 2021 wheat crop up 0.9% on the year to 22.34 million tons. They put the 2021 winter rapeseed crop down 0.7% to 3.48 million tons. Winter barley was expected to increase 2.7% to 9.07 million tons while spring

barley was projected to decrease 5.7% to 1.89 million tons from a smaller planted area. - Russia

said they will stop intervening in regulation of grain exports if the situation stabilizes.

- EU

May milling wheat (down 6 sessions) was down 1.00 at 222 euros. - Selected

US state crop ratings:

Texas

27 percent G/E, unchanged previous week.

Oklahoma

57 percent, up from 53 percent previous week.

May

Paris wheat

Source:

Reuters and FI

Export

Developments.

- Pakistan

seeks 300,000 tons of wheat for April-August shipment and lowest offer was $285.97/ton c&f for August shipment. April was thought to be $323.97/ton.

- Jordan

passed on 120,000 tons of animal feed barley, for shipment between October 1 and November 15. Reuters noted only one trading house participated.

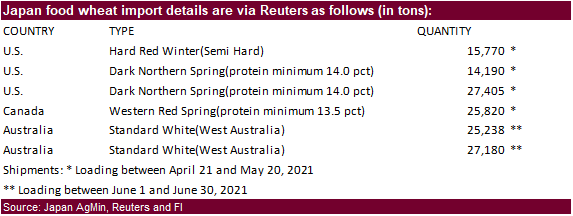

- Japan

seeks 135,603 tons of food wheat from the US, Canada and Australia.

Rice/Other

·

(new 3/16) Syria seeks 39,400 tons of white rice on April 19. Origin and type might be White Chinese rice or Egyptian short grain rice.

·

Bangladesh seeks 50,000 tons of rice on March 18.

·

South Korea’s Agro-Fisheries & Food Trade Corp. seeks 208,217 tons of rice, on March 25 for arrival in South Korea in 2021 between May 1 and Oct. 31. 64,444 tons of non-glutinous brown rice is sought

from the United States. Rest from Thailand, China, Australia and Vietnam.

·

Bangladesh also seeks 50,000 tons of rice on March 28.

·

Syria seeks 25,000 tons of white rice on March 29, from China or Egypt.

Updated

3/9/21

May

Chicago wheat is seen in a $6.25‐$6.90 range

May

KC wheat is seen in a $5.75‐$6.75 range

May

MN wheat is seen in a $6.20‐$6.65 range

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International

One Lincoln Center

18 W 140 Butterfield Rd.

Oakbrook Terrace, Il. 60181

W: 312.604.1366

ICE IM:

treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered

only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making

your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors

should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or

sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy

of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.