PDF Attached

Today

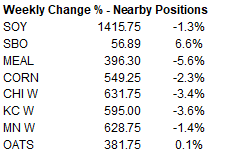

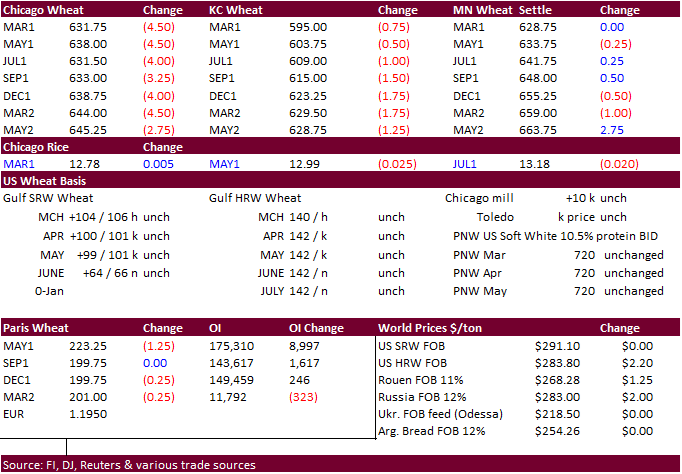

was last trade for CBOT March futures. (March settles below w/ weekly % change)

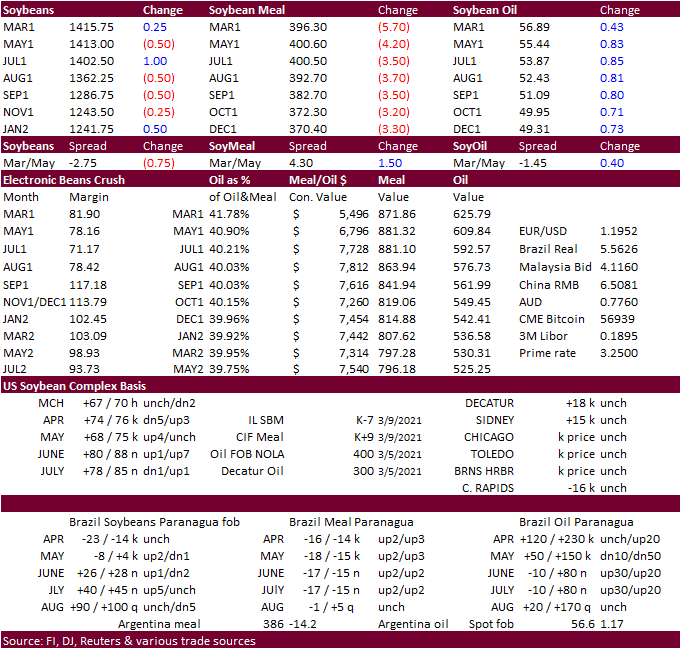

Soybean

oil was again the bread winner for the week. Futures traded choppy Friday on lack of direction and positioning. Most US wheat futures were under pressure from the current storm rolling across the heart of the US providing widespread soil moisture relief.

World

Weather Inc.

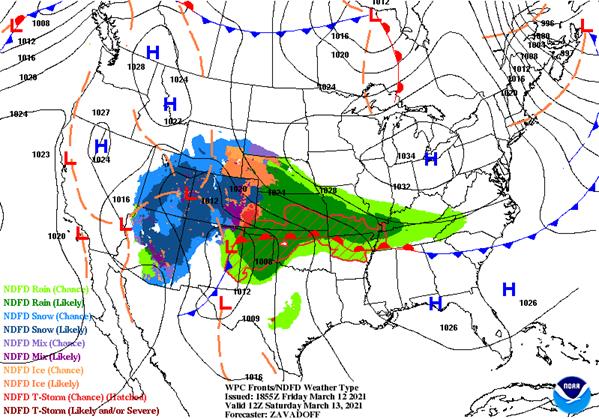

WORLD

WEATHER TO WATCH DURING THE WEEKEND

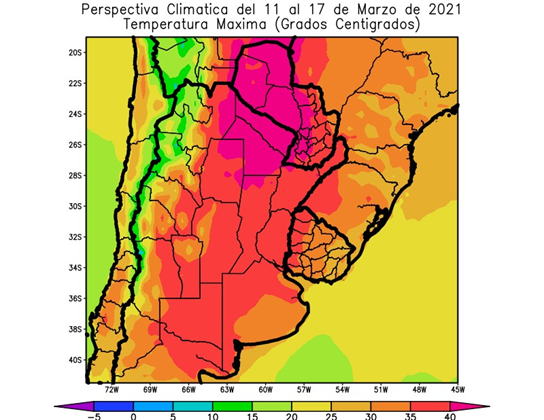

- Argentina

crop stress has continued to be punishing in some areas this week and that trend will prevail through the weekend and into Monday

o

Thunderstorms Monday night into Wednesday will bring relief to many areas with 0.50 to 1.50 inches of rain and locally more

- The

precipitation will be welcome and should offer some relief to crop moisture stress, but follow up rain will be very important

o

Cooling accompanying next week’s rain will help temporarily slow evaporation and crop stress

o

Follow up rain will be very important and there is some expected in the March 20-26 period – that event will also be welcome, although many crops will move beyond their most moisture sensitive stage of development as the end of

the month rolls around.

- Brazil

rainfall will resume this weekend and occur frequently again next week in Mato Grosso, Goias, Tocantins and some immediate neighboring areas

o

This week’s break from the wettest conditions has allowed the topsoil to firm up in some areas, but the break has not likely allowed aggressive field progress because muddy conditions

o

Field progress will continue around the rain, but progress will be slow

- Southern

Brazil weather will be more supportive of crop development and farming activity including soybean harvesting and Safrinha corn planting

o

Rio Grande do Sul will have need for greater rain later this month, but crops in the state will remain in good shape through the next seven days

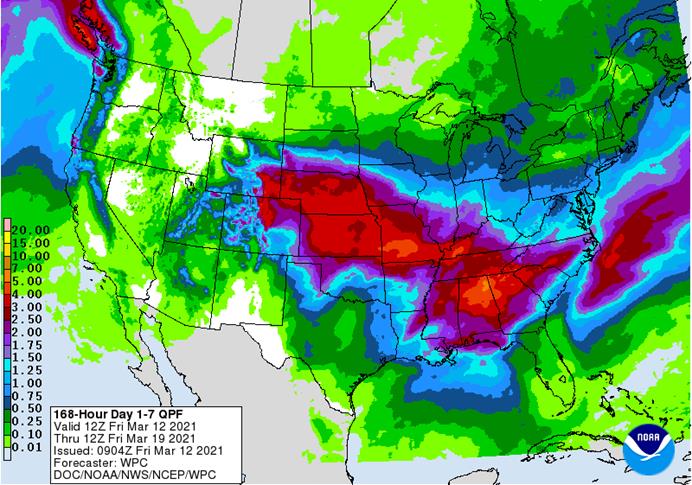

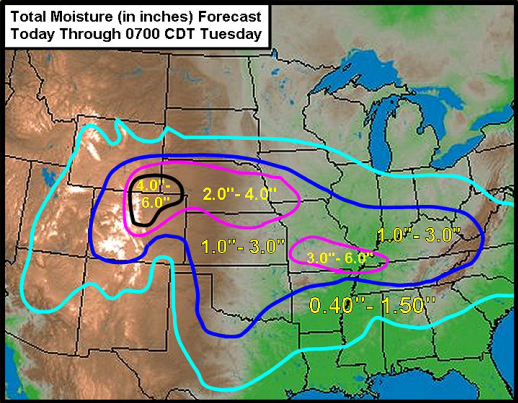

- Some

changes in the distribution of rain in the U.S. Plains has been subtly suggested today, but between this weekend’s precipitation event and the follow up system expected during mid-week a sufficient amount of relief will continue to the driest areas in Kansas,

Nebraska and northeastern Colorado.

o

Another storm system possible around March 22-23 could bring additional moisture to the region

o

Three storm systems in ten days across hard red winter wheat production areas could seriously improve root and tillering so that production can be raised later in the year barring no other weather adversities

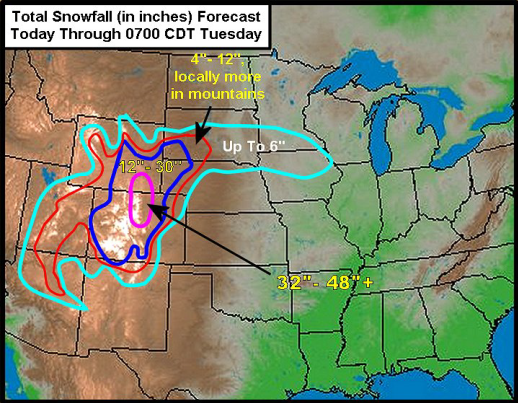

- Livestock

stress and possible losses may occur this weekend into early next week from southwestern South Dakota into eastern Wyoming and southward through the Front Range area of the Colorado mountains where 12 to 30 inches of snow will accumulate

o

Snowfall in the Mountains could range from 2 to 4 feet and locally much more

o

Travel issues are expected from Denver Colorado through Cheyenne Wyoming and areas north east into the Black Hills region

- Far

northern U.S. Plains and Canada’s Prairies will be drier than usual over the next ten days due to frequent storms in the U.S. limiting northbound moisture from reaching the higher latitudes

o

World Weather, Inc. still believes better precipitation will reach these areas in April and May to east long term dryness.

o

A couple of weak weather systems will move through the Prairies late next week into the following weekend, but moisture totals will be light

- U.S.

West Texas weather will be mixed through next week

o

The High Plains region will get less than 0.50 inch of moisture

o

The Low Plains will receive 0.25 to 0.75 inch with a few totals to 1.50 inches

o

The Rolling Plains will receive 0.50 to 1.50 inches with a few locally greater amounts

- Severe

thunderstorms are likely in the southern Plains this weekend and some will reach the Delta late Sunday into Monday - U.S.

southeastern states will experience good planting weather through Sunday and Into Monday

o

Brief periods of precipitation will slow farming activity next week, but the mix of rain and sunshine should be good for early planted crops

- U.S.

Delta planting will advance in the south through the weekend and into next week, although rain will develop periodically to slow or stall fieldwork for short periods of time - Nebraska,

northeastern Kansas, Missouri and Kentucky will likely get too much rain in the next week resulting in some flooding

o

The greatest rain will occur through the weekend with follow up moisture during mid-week next week

- South

Texas will continue too dry along with some of the Coastal Bend region, despite a few brief showers

o

Irrigated corn, sorghum and some cotton are being planted

o

Dryland crops in the region need more moisture, but some planting is under way

- California

and the interior western U.S. will see some precipitation during the next two weeks, but most of the significant precipitation will fall in the mountains - Freezes

returning to the central and southern Plains late this weekend and next week will not cause any permanent damage to wheat that is greening

- Southeast

Canada will experience below average precipitation and near average temperatures during the coming week to ten days - North

Africa weather has trended drier once again

o

This week’s precipitation was welcome, but more will be needed to ensure the best yields later this spring

o

Northwestern Algeria, a few areas in northern Tunisia and southwestern Morocco are driest

- Ivory

Coast, Ghana, Benin and southern Nigeria will receive waves of rain in the next ten days

o

New rain totals will vary from 0.50 to 3.00 inches and locally more will be supportive of coffee and cocoa flowering and help increase soil moisture for future rice, sugarcane and cotton production

- East-central

Africa rainfall will be erratic and light for a while

o

Crop conditions are best in Tanzania

o

Rain is needed most in Ethiopia, although this is the end of their dry season

- South

Africa will experience an erratic rainfall pattern through the next week with temperatures mostly near to above average

o

The drying trend will encourage early season crop maturation, but subsoil moisture and irrigation will support late season crops

o

Summer crop conditions will remain favorably rated, although there will be a growing need for showers by mid-March

- Some

increase in precipitation is expected March 20-26 and that should prove timely for late season crops that dry out in this coming week - India

began receiving isolated showers in central parts of the nation Thursday and they will continue into Saturday morning

o

The moisture will be good for filling crops, but it will not likely to change soil conditions for very long

o

Some follow up precipitation may occur erratically in the March 20-26 period, but it will be lost to evaporation very quickly

- China

weather over the next ten days will continue dry in Yunnan while periodic rain and thunderstorms occur near and south of the Yangtze River

o

Rainfall will be greatest in southeastern Sichuan, Guizhou, Hunan Jiangxi and Zhejiang where 1.00 to 4.00 inches and locally more will result

o

Other showers and thunderstorms will occur in east-central China periodically during the next ten days, but periods of sunshine will also occur and rain totals will be mostly under 1.00 inch

o

Northeastern China and the Yellow River Basin will see alternating periods of light precipitation and sunshine through the next two weeks maintaining a very good outlook for winter crop development when seasonal warming begins

- Spring

planting prospects remain exceptionally good. but seasonal warming is needed in many areas

o

Temperatures will be above normal in most of the nation during the coming week to ten days

- Winter

crops will continue to come out of dormancy in the central and south. Spring planting will advance around periods of rain in the south

- Australia

weather in the coming week is expected to include frequent showers and thunderstorms in northeastern New South Wales and southern Queensland

o

The precipitation will be good for late season crops and for improving topsoil moisture for autumn planting

o

Early maturing cotton might not welcome the precipitation and could become a little too wet

- Mexico

drought conditions are still prevailing, although the impact on winter crops is low due to irrigation

o

Water supply is low in some areas and a notable improvement in rainfall is needed, but not very likely

o

Dryland winter crops are stressed and will yield poorly

o

Freeze damage is common in northern parts of the nation due to a couple of cold surges this winter

o

Rain in the coming week will be mostly confined to the east coast and temperatures will be seasonable with a slight warmer bias in the driest areas

- Central

America precipitation will continue greatest along the Caribbean Coast and in Guatemala while the Pacific Coast receives the lightest and most erratic rainfall, but some precipitation will fall especially in Costa Rica and Panama. - Southeast

Asia rainfall will occur relatively normally over the next two weeks

o

Mainland areas will experience net drying over the coming week with rain possible in the March 19-25 period

- The

resulting rainfall will be sporadic and light with net drying probably continuing in many areas for a while longer

o

Philippines rainfall will increase in the coming week due to a tropical weather disturbance that will help induce some moderate to heavy rain at times

o

Indonesia and Malaysia weather during the next two weeks will bring rain to most crop areas maintaining a very good outlook for crop development

- A

boost in precipitation is expected and will be welcome - Peninsular

Malaysia is still driest and has the greatest need for rain - Rain

in peninsular Malaysia should fall during the middle to latter part of next week and into late month - New

Zealand weather will be drier and a little cooler than usual in this coming week

o

The nation’s soil moisture has drifted below average especially in the north

o

Additional drying is expected March 20-26

- Southern

Oscillation Index has been falling and was at +3.84 this morning. The index is expected to continue to fall for a little longer, but will soon start to level off somewhat. The index has fall since Feb. 23 when it was +15.24 - Europe

weather will be mixed over the next two weeks with periods of rain, mountain snow and sunshine occurring while temperatures are seasonable

o

The environment will be good in maintaining moisture abundance in much of the continent and seasonal warming will bring more winter crops out of dormancy in parts of the west and south

o

Net drying is expected in Spain and Portugal

- Western

CIS temperatures will be slightly cooler than usual in this coming week while waves of snow and rain prevail

o

The environment will be good for spring crop development, but for now there will not be much greening or crop development for a while longer due to coolness

o

Too much moisture is also present in the soil in western Russia and flooding may be an issue for a while this spring as a deep layer of snow melts while new precipitation falls

- Bitter

cold in Russia this week occurred in snow covered areas resulting in no crop damage.

Source:

World Weather inc.

Source:

World Weather inc.

Source:

World Weather inc.

Bloomberg

Ag Calendar

Monday,

March 15:

- USDA

Export Inspections – corn, soybeans, wheat, 11am - EU

weekly grain, oilseed import and export data - Malaysia

to announce crude palm oil export tax rate for April (tentative) - Monthly

MARS bulletin on EU crop conditions - Ivory

Coast cocoa arrivals - India

Feb. vegetable oil imports (tentative) - Malaysia’s

March 1-15 palm oil export data

Tuesday,

March 16:

- New

Zealand global dairy trade auction

Wednesday,

March 17:

- EIA

weekly U.S. ethanol inventories, production - Brazil’s

Unica may release cane crush, sugar production data (tentative)

Thursday,

March 18:

- USDA

weekly crop net-export sales for corn, soybeans, wheat, cotton, pork, beef, 8:30am - Port

of Rouen data on French grain exports - China

customs to publish trade data, including import numbers for corn, wheat, sugar and pork - USDA

total milk production

Friday,

March 19:

- ICE

Futures Europe weekly commitments of traders report (6:30pm London) - CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm - FranceAgriMer

weekly update on crop conditions - U.S.

cattle on feed

Saturday,

March 20:

- China

3rd batch of Jan.-Feb. trade data, including country breakdowns for energy and commodities. No timing

The

CME Group

intends to increase both spot-month and all-months-combined speculative position limits effective March 15.

https://www.cmegroup.com/rulebook/files/cme-group-Rule-562-pending.pdf

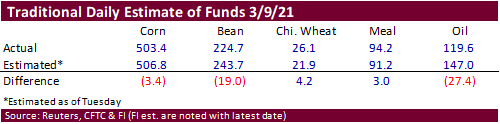

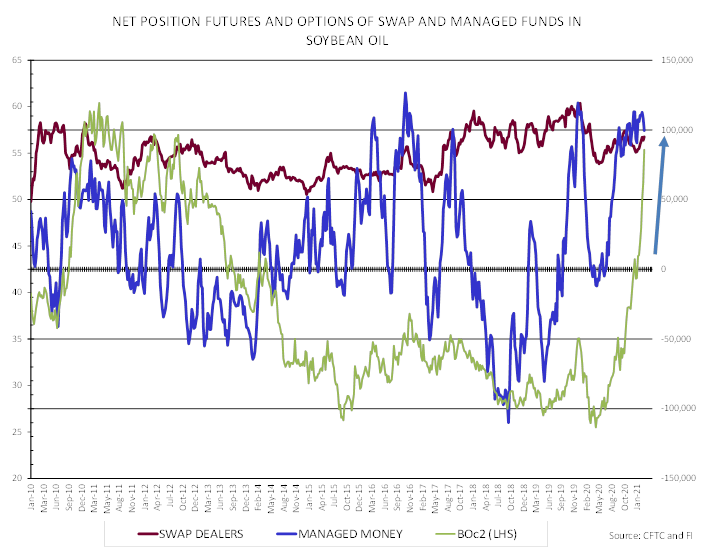

Traders

missed the net long positions in soybeans and soybean oil (less than expected). Lower trade Sunday night could be taken under consideration.

The

net longs for soybean oil managed money futures and options are down for the third consecutive week, while SBO futures traded higher.

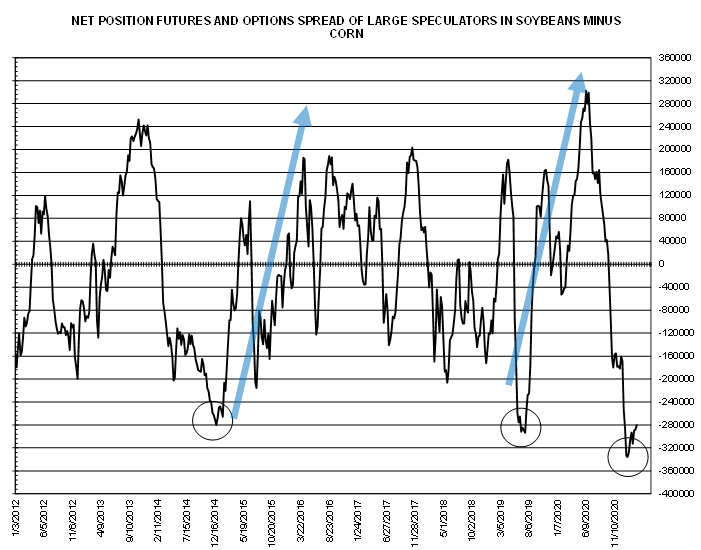

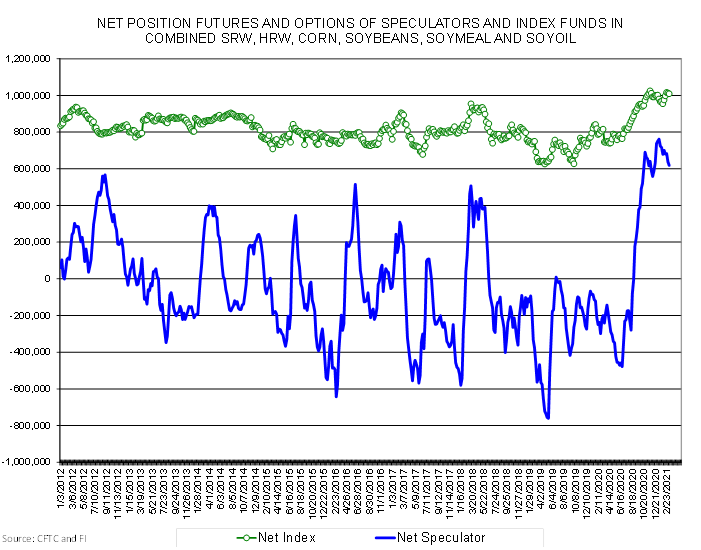

What

is next for the soybean/corn traditional funds futures & options relationship?

Depends

in part on Index funds (they are near record long CBOT aggregated)

SUPPLEMENTAL

Non-Comm Indexes Comm

Net Chg Net Chg Net Chg

Corn

339,802 -8,812 408,098 1,159 -738,710 6,286

Soybeans

129,770 3,238 165,766 -1,870 -291,244 -3,127

Soyoil

74,589 -4,147 125,347 -793 -220,282 6,096

CBOT

wheat -4,234 -4,648 153,602 -2,685 -135,465 7,188

KCBT

wheat 28,252 -4,442 69,062 -130 -92,607 4,167

=================================================================================

FUTURES

+ OPTS Managed Swaps Producer

Net Chg Net Chg Net Chg

Corn

356,514 7,966 260,678 -2,931 -723,193 6,373

Soybeans

159,601 4,040 90,567 -533 -277,756 -4,388

Soymeal

64,244 -1,179 70,306 633 -185,297 -3,218

Soyoil

99,574 -8,508 95,122 2,584 -235,110 3,952

CBOT

wheat 27,576 -4,227 93,552 161 -116,891 4,683

KCBT

wheat 47,664 -4,060 41,748 -424 -84,710 4,265

MGEX

wheat 16,590 2,489 3,917 -275 -27,676 -2,166

———- ———- ———- ———- ———- ———-

Total

wheat 91,830 -5,798 139,217 -538 -229,277 6,782

Live

cattle 81,660 1,090 83,265 -1,012 -169,816 660

Feeder

cattle 379 -784 7,425 -268 -2,731 -743

Lean

hogs 74,287 155 55,368 337 -134,458 -5,942

Other NonReport Open

Net Chg Net Chg Interest Chg

Corn

115,193 -12,777 -9,190 1,368 2,374,719 16,167

Soybeans

31,882 -879 -4,293 1,759 1,193,643 37,019

Soymeal

17,922 408 32,824 3,357 471,502 10,492

Soyoil

20,067 3,127 20,347 -1,156 590,495 41,721

CBOT

wheat 9,663 -762 -13,902 145 503,536 -7,013

KCBT

wheat 5 -186 -4,707 404 233,235 -5,263

MGEX

wheat 1,858 -235 5,312 186 87,446 2,502

———- ———- ———- ———- ———- ———-

Total

wheat 11,526 -1,183 -13,297 735 824,217 -9,774

Live

cattle 19,796 -1,764 -14,905 1,026 381,857 -4,472

Feeder

cattle 3,992 1,283 -9,065 511 50,687 2,437

Lean

hogs 13,866 3,890 -9,065 1,561 319,949 5,761

Source:

Reuters, CFTC and FI

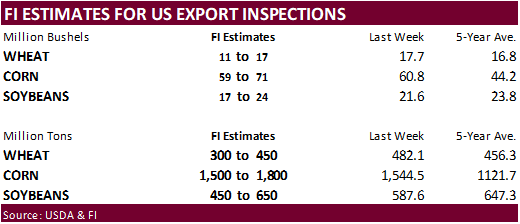

US

PPI Final Demand (M/M) Feb: 0.5% (est 0.5%; prev 1.3%)

US

PPI Ex-Food, Energy (M/M) Feb: 0.2% (est 0.2%; prev 1.2%)

US

PPI Ex-Food, Energy, Trade (M/M) Feb: 0.2% (est 0.3%; prev 1.2%)

US

PPI Final Demand (Y/Y) Feb: 2.8% (est 2.7%; prev 1.7%)

US

PPI Ex-Food, Energy (Y/Y) Feb: 2.5% (est 2.6%; prev 2.0%)

US

PPI Ex-Food, Energy, Trade (Y/Y) Feb: 2.2% (est 2.5%; prev 2.0%)

Canadian

Net Change In Employment Feb: 259.2K (est 75.0K; prev -212.8K)

Canadian

Unemployment Rate Feb: 8.2% (est 9.2%; prev 9.4%)

Brazil

Retail Sales (Y/Y) Jan: -0.3% (est 0.3%; prev 1.2%)

Brazil

Retail Sales (M/M) Jan: -0.2% (est 0.0%; prev -6.1%)

Brazil

Retail Sales Broad (Y/Y) Jan: -2.9% (est -0.5%; prev 2.6%

Corn

- Corn

futures ended

Friday mixed from contract positioning and a higher USD (+21 as of 3 pm CT).

- Funds

sold an estimated net 3,000 corn contracts. - News

for the corn market was extremely light. - China

corn futures traded lower for the last few days on ASF concerns. Feed demand is a head scratcher for China. They recently have been picking up US white wheat and using it for feed. Soybean meal stocks are highest since December and China has been a reserved

buyer of US corn over the past month. However, they have huge commitments on the books, and we expect shipments to increase.

- We

look for US export inspections for corn to increase over the next several weeks as imports shift away from soybeans.

- Note

at least five of the corn cargoes SK bought this week were out of the PNW.

Export

developments.

- None

reported

Updated

3/1/21

May

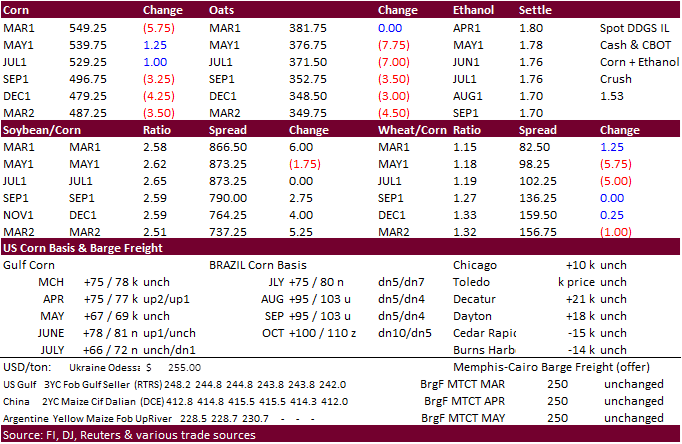

corn is seen in a $5.20 and $5.75 range.

July

is seen in a $5.00 and $6.00 range.

December

corn is seen in a $3.85-$5.50 range.

- The

soybean complex was very choppy today in part to a higher USD, rally in soybean oil after briefly turning lower, and sharply lower soybean meal futures. We are getting a lot of questions on SBO these days. When will it break? The hundred thousand dollar

question. But with renewable diesel production coming online, long term we remain bullish. We do think a short term correction is due for soybean oil, but long traders may want to see a decline in South American cash prices and pause in the upward momentum

in Malaysian palm futures before taking profits. We also caution a product spread reversal when US soybean rationing hits the crush industry this summer, limiting available supplies of soybean meal for domestic feed. Global vegetable oil prices were up this

week and exports are lucrative. Note vegetable oil accounted for 40% of Ukraine’s farm exports so far in 2020-21 in USD terms (4.4 USD billion). And some countries may need to play catchup for imports as their economic situation improves. India vegetable

oil imports slowed last month. SEA reported India February palm oil imports at 394,495 tons, down 27% year earlier and lowest level in nine months. Soybean imports were 285,973 tons from 322,448 tons, and sunflower oil dropped to 116,110 tons from 226,743

tons. - Funds

were net even in soybeans, sold 4,000 soybean meal and bought 6,000 soybean oil.

- Lack

of export developments since Thursday afternoon and light news kept CBOT soybeans choppy, eventually ending mixed.

There

again were no major changes to the SA weather forecast although Argentina was slightly wetter for early next week. Argentina will see 1-1.5 inches of rain Tuesday and Wednesday. Northern and central Brazil will remain active for at least the next week.

- After

the Friday close, the

Association of Mato Grosso Soy and Corn Producers (Aprosoja) estimated the Brazil soybean crop at 128.57 million tons vs. 129-130 million tons previously. Note this group represents producers. For Brazil we are using 133 million tons, around other trade

expectations. - ICE

canola basis May position fell 40 cents to 801.10/ton. - Coceral

lowered their EU rapeseed crop to 17.7 million tons from 17.8 million tons in December, above 17.1 million harvested in 2020. - Offshore

values this morning were leading CBOT SBO 49 points lower (69 lower for the week) and meal $0.90 short ton higher ($4.10 lower for the week).

- China

cash crush margins on our analysis were 178 cents (175 previous), up from 113 cents late last week and compares to 128 cents year earlier.

- Malaysian

palm oil for the week was up 10 percent this week to nearly 5-1/2 year high.

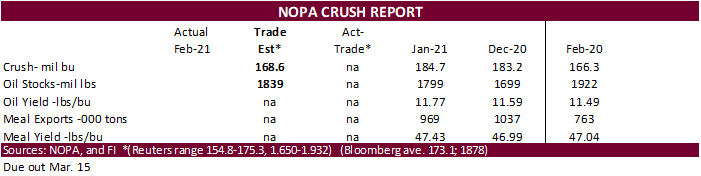

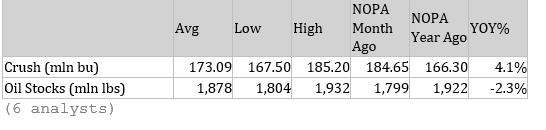

- Monday

we will see NOPA release February US crush figures and the trade can’t seem to get a handle on what was crushed for the month. Bloomberg and Reuters reported a very large range for the US February soybean crush, and it appears some

people may have forgot the US saw a large storm last month temporarily knocking some crush plants offline, and that there are only 28 days for the month of Feb.

When eyeing the estimates below, keep in mind the median estimate for Reuters was 167.9 million bushels and Bloomberg medium at 171.

Bloomberg

estimates below

Export

Developments

- Results

awaited: South Korea’s NOFI group seeks 12,000 tons of soybean meal for March 11-March 29 shipment (US), or up through April 15 if sourced from China.

- The

USDA CCC seeks 2,030 tons of packaged oil on March 16 for shipment Apr 16 – May 15.

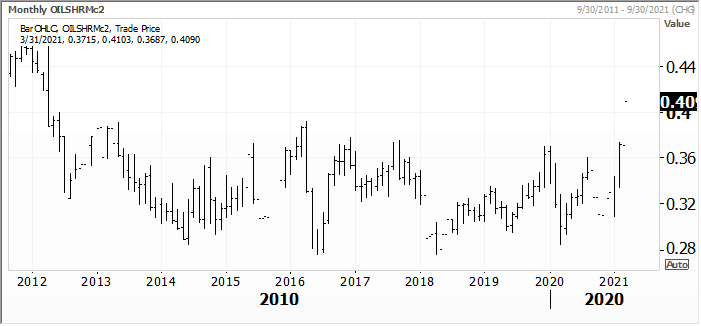

Monthly

oil share – rolling second month

Source:

Reuters and FI

12ZSAT

Updated

3/11/21

May

soybeans are seen in a $13.75 and $14.75 range.

May

soymeal is seen in a $400 and $450 range.

May

soybean oil is seen in a 52.00 and 56.00 cent range. –

do not discount volatility to increase.

- US

wheat futures ended mostly lower after trading tow-sided. A large US wintery precipitation event is expected to bring soil moisture relief to many parts of the central and southern Great Plains. The Kansas (ratings declined one point last week to 36% G/E)

wheat areas badly need precipitation. US global export developments slowed by late workweek.

- Funds

sold an estimated net 4,000 wheat contracts. - French

soft wheat conditions were 88% as of March 8, unchanged from the week prior and above 63% a year ago. Durum was rated 88% as well, and winter barley at 85%, according to FranceAgriMer. Egypt said they have enough strategic reserves for 5 months.

- Coceral

lowered their EU soft wheat production to 141.5 million tons from 143.0 million but above last year’s 128.2 million. - EU

May milling wheat was down 1.25 at 223.25 euros. - Egypt

said they have enough strategic reserves for 5 months. - APK-Inform:

(Barley now more than expensive than milling wheat - Milling

wheat $218-$227 a ton Black Sea June-July delivery - Barley

$220-$230 a ton CPT (carriage paid to) Black Sea June-July delivery - 80%

of Russia’s winter crop is in good condition-Russian Ag Ministry.

Export

Developments.

- Japan

bought 94,925 tons of milling wheat this week. - Results

awaited: Algeria seeks around 50,000 tons of feed barley on March 11 for shipment by April 25.

- Jordan

seeks 120,000 tons of animal feed barley, on March 16 for shipment between October 1 and November 15.

- Pakistan

seeks 300,000 tons of wheat on March 16 for April-August shipment.

Rice/Other

·

South Korea’s Agro-Fisheries & Food Trade Corp. seeks 208,217 tons of rice, on March 25 for arrival in South Korea in 2021 between May 1 and Oct. 31. 64,444 tons of non-glutinous brown rice is sought

from the United States. Rest from Thailand, China, Australia and Vietnam.

·

Bangladesh seeks 50,000 tons of rice on March 18.

·

Syria seeks 25,000 tons of white rice on March 29, from China or Egypt.

Updated

3/9/21

May

Chicago wheat is seen in a $6.25‐$6.90 range

May

KC wheat is seen in a $5.75‐$6.75 range

May

MN wheat is seen in a $6.20‐$6.65 range

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International

One Lincoln Center

18 W 140 Butterfield Rd.

Oakbrook Terrace, Il. 60181

W: 312.604.1366

ICE IM:

treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered

only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making

your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors

should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or

sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy

of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.