(Resending)

PDF Attached

![]()

Monthly

USD

World

Weather Inc.

WEATHER

THAT MATTERS TODAY

- Argentina

is moving more deeply into a ten day period of net drying and warmth that promises to raise crop stress in many areas, but first in the driest areas from La Pampa and western Buenos Aires into southern Santa Fe and parts of southwestern Entre Rios - Potential

yield losses will be on the rise as time moves along and the most stressful period is expected late next week through the following weekend unless rain falls more significantly than advertised - Brazil

continues to struggle with its soybean harvest in the wetter areas of Mato Grosso and a few other areas - The

rain, even though not unusual at this time of year, will hinder field progress at times - This

matters more this year than in the past because the harvest is already notably late due to delayed seasonal rainfall in the spring which delayed the planting of soybeans - Weather

patterns are not likely to change much during the next ten days to two weeks

- Rio

Grande do Sul, Brazil and Paraguay will dry down along with Argentina over the next ten days - Crop

moisture stress will be on the rise and there is some potential for dryness to limit production in portions of both areas as time moves along - U.S.

weather is drier today than advertised Tuesday especially in the first ten days of the outlook in the Plains and northern Midwest - U.S.

northern Delta and Tennessee River Basin flood potentials will rise as waves of rain move across these areas late this week through Monday - The

ground is already saturated and rainfall of 2.00 to 6.00 inches will lead to significant runoff and small river and stream flooding - Flooding

of low-lying crop areas is also expected - U.S.

Midwest snowmelt will increase runoff over the coming week, but no flooding of major rivers is expected, but some low-lying areas will experience days of standing water for a while - River

ice on the Mississippi, Missouri and Illinois rivers will slowly decrease during the next week to ten days

- U.S.

hard red winter wheat is not likely to get much precipitation over the next ten days and net drying will result - Temperatures

will be warm enough at times to increase evaporation leading to net drying and rising need for greater precipitation

- Northern

U.S. Plains and parts of Canada’s Prairies will receive brief bouts of light precipitation in the coming week, but no change in drought status is expected - Significant

early spring precipitation is needed to recharge the soil with moisture to support planting - Southwestern

U.S. drought is not likely to change anytime soon - West

Texas dryness will prevail with some gradual loss in soil moisture expected due to warming temperatures - No

relief is expected through the next ten days - South

Texas crop areas are still too dry - 70-

and 80-degree Fahrenheit high temperatures in the coming week will accelerate the dryness while raising soil temperatures. Planting in irrigated areas will occur soon - Assessments

of freeze damage in South Texas and northeastern Mexico from earlier this month are ongoing, but damage to fruits and vegetables has been significant

- Portions

of North Africa are still too dry raising concern over spring crop development - Rain

will fall in Morocco Thursday into Monday improving soil conditions in some areas - Northwestern

Algeria and southwestern Morocco are driest, although Tunisia and northeastern Algeria have been drying down recently - India’s

winter crop areas are drying down and will continue to do so for the next ten days - Yield

potentials may slip a little during this period of time due to moisture stress, but production will still be favorable – just not as good as last year for some areas and some crops - Mexico

drought conditions are still prevailing, although the impact on winter crops is low due to irrigation - Water

supply is low in some areas and a notable improvement in rainfall is needed, but not very likely - Dryland

winter crops are stressed and will yield poorly - Freeze

damage is common in northern parts of the nation due to a couple of cold surges this winter - Eastern

Australia has received periodic showers and thunderstorms this summer supplementing irrigation and supporting good production in irrigated areas - Dryland

crop production may not be as good as expected this year especially in Queensland due to a somewhat restricted rainfall pattern in some areas at times

REST

OF THE WORLD

- China

has experienced no significant winterkill this year and soil moisture is favorably rated in most winter crop areas - A

little too much rain will fall in the coming ten days in the Yangtze River Basin where local flooding might evolve

- Southern

rapeseed may not benefit from the wet bias and will require some drier weather soon - Russia’s

winter crop areas have not been bothered by much winterkill this year - Bitter

cold has occurred periodically, but snow cover has been present in most cases preventing significant losses - Production

in Russia’s Southern Region is still expected to be down because of drought during the planting season - Long

term moisture deficits are continuing in many areas from Turkey to Kazakhstan, southern Russia and Ukraine, despite improved soil moisture in parts of the region - Winter

precipitation has been best in improving topsoil moisture in Ukraine, southeastern Europe and Turkey - Europe

weather has become drier biased and a little warmer than usual. - Winter

crops are still dormant or semi-dormant with little change likely into early March - Recent

drier weather has reduced runoff and thus lowering the potential for spring flooding - West

Africa rainfall will remain mostly confined to coastal areas for a while, but may drift to the north into some coffee and cocoa production areas early next week - East-central

Africa precipitation will be scattered over the coming week - The

lightest and most infrequent rain occurring in Ethiopia and parts of Uganda while the most significant rain occurs in Tanzania where all crop areas will get moisture - Southeast

Asia rainfall will occur relatively normally over the next two weeks - Mainland

areas will be mostly dry, although a few showers could pop up across the region next week - All

of the precipitation will be sporadic and light having little to no impact on crops or soil conditions - Philippines

rainfall will become more scattered and light after recent flooding rainfall from Tropical Depression Dujuan - Indonesia

and Malaysia weather during the next two weeks will bring rain to most crop areas maintaining a very good outlook for crop development - Sumatra,

Peninsular Malaysia and eastern Borneo have been drying out recently and greater rain is needed - New

Zealand weather over the next ten days will include light rainfall and slightly warmer biased temperatures - Mexico

precipitation in the coming ten days will be mostly confined to the east coast - Central

America precipitation will continue greatest along the Caribbean Coast and in Guatemala while the Pacific Coast is relatively dry - Southern

Oscillation Index is beginning to fall once again and was at +14.79 this morning. The index is expected to continue to fall over the next several days - Canada

Prairies will experience seasonable temperatures over the next ten days with precipitation mostly near to below average - Some

occasional precipitation will occur along the front range of mountains in Alberta and across the southwestern Prairies as well as in a few northeastern crop areas - Southeast

Canada will experience near to above normal amounts of precipitation in the coming week while temperatures are seasonable.

Source:

World Weather Inc. and FI

Thursday,

Feb 25:

- USDA

weekly crop net-export sales for corn, soybeans, wheat, cotton, pork, beef, 8:30am - Port

of Rouen data on French grain exports - International

Grains Council monthly report - Malaysia’s

Feb. 1-25 palm oil export data - USDA

red meat production, 3pm - EARNINGS:

Minerva, BRF, FGV (tentative), Golden Agri

Friday,

Feb 26:

- ICE

Futures Europe weekly commitments of traders report, 1:30pm (6:30pm London) - CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm - U.S.

agricultural prices paid, received, 3pm - Earnings:

Olam - HOLIDAY:

Thailand

US

10 Year Yield Rises To 1.40% The Highest Since Feb 2020

US

New Home Sales Change Jan: 923K (est 856K; prev 842K)

–

New Home Sales (M/M) Jan: 4.3% (est 1.6%; prev 1.6%)

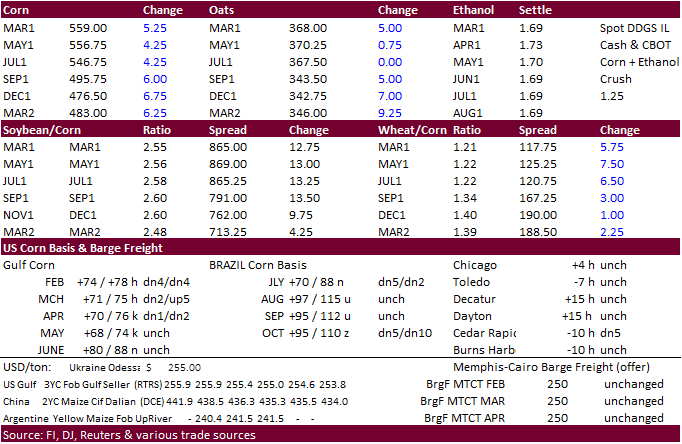

Corn.

-

Corn

futures ended higher despite poor US ethanol production. Prices were likely led by higher soybeans and wheat. Our outlook for US corn for ethanol use dropped 40 million bushels for 2020-21 because EIA reported the largest weekly drop in ethanol production

since data began mid-2010, due to industrial production halts from the US deed freeze. -

Funds

bought an estimated net 13,000 contracts. -

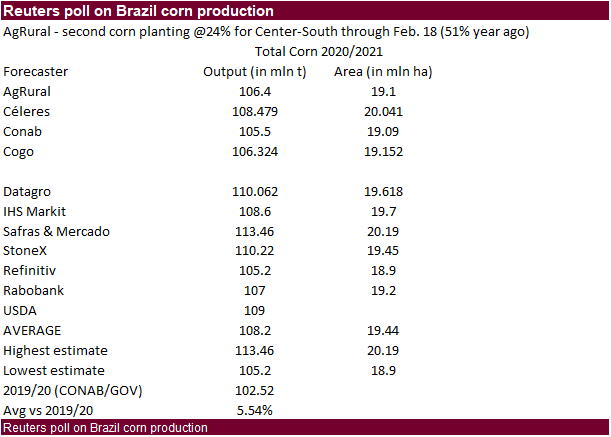

A

Reuters poll calls for South Africa’s CEC to initially report their 2020-21 corn production at 16.872 million tons, up from the 15.300 million tons last season. The first survey of the season is expected to show 8.929 million tons of white maize and 7.943

million tons of yellow maize. They will release the report on Thursday.

-

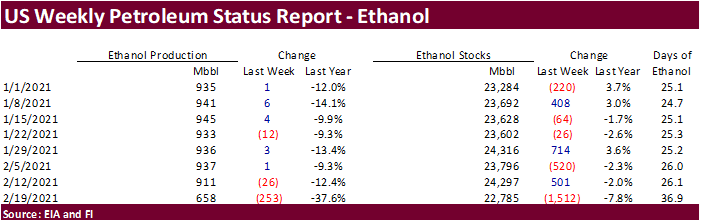

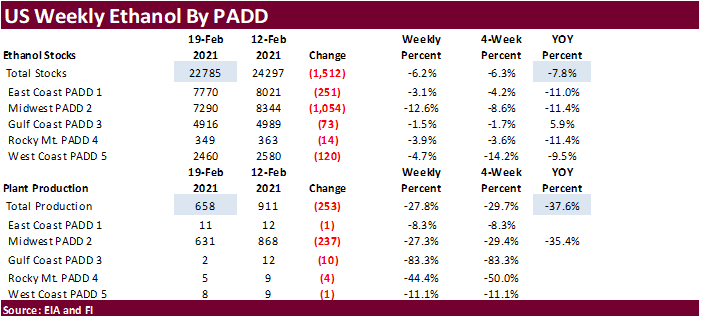

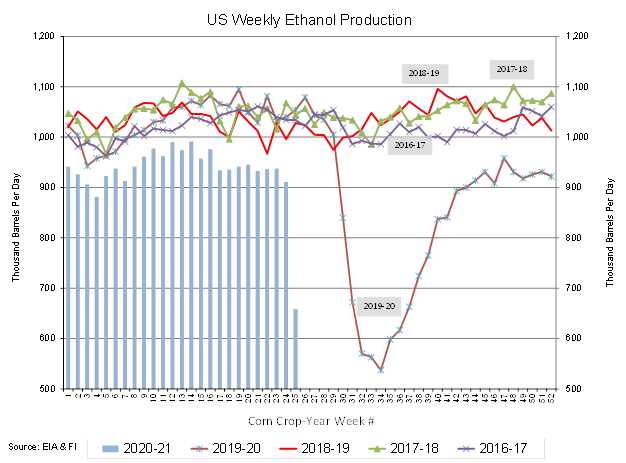

The

US deep freeze had a very large impact on US weekly ethanol production and time will tell if the industry can recover back above 900,000 barrels per day by the end of this month. Ethanol production fell 6.2 percent or 253,000 barrels per day to 658,000, lowest

level since the height of the world pandemic shutdowns nearly a year earlier, and down about 38 percent from this time a month ago. This was the largest weekly drop for any week since weekly data began in 2010. (Estimates ranged from 727-910 thousand barrels

for production, down 92k average, and stocks to be down 207k). Our bias is for US corn for ethanol use to end up below USDA’s 4.950 billion bushel outlook if ethanol blend rates fail to recover by the summer driving months to its respected linear three year

trend. Looking at early September through February 19th ethanol production, implied corn use to make ethanol is down 9.7 percent from the same period a year earlier. Gasoline stocks increased 12,000 barrels to 257.1 million. Refinery and blender

net input of oxygenates fuel ethanol was only 725,000 barrels per day for the week ending February 19, down nearly 20 percent from a year ago. Gasoline demand had a large impact on ethanol use as the ethanol blend rate remained above 89 percent (90.6% for

the week). -

Our

February projection for US ethanol production was revised lower to 23.191 million barrels from 25.109 million barrels previously. US corn for ethanol use is now seen at 4.960 billion bushels, down from 5.000 billion previously and compares to 4.950 billion

bushels by USDA and 4.852 billion year ago. The 40 million bushel decrease in industrial demand will likely get absorbed into exports when modifying our US balance sheet, taking int account delayed Brazilian Q4 (Oct-Sep) corn shipments (soybean export season

extended) and strong Asian demand for US corn.

Corn

Export Developments

·

South Korea’s KOCOPIA bought about 60,000 tons of corn from the United States at about $309 a ton c&f for arrival in South Korea around May 20.

Updated

2/22/21

March

corn is seen trading in a $5.25 and $5.75 range.

May

corn is seen in a $5.15 and $6.00 range.

July

is seen in a $5.00 and $6.00 range.

December

corn is seen in a $3.75-$6.00 range.