PDF Attached

USDA

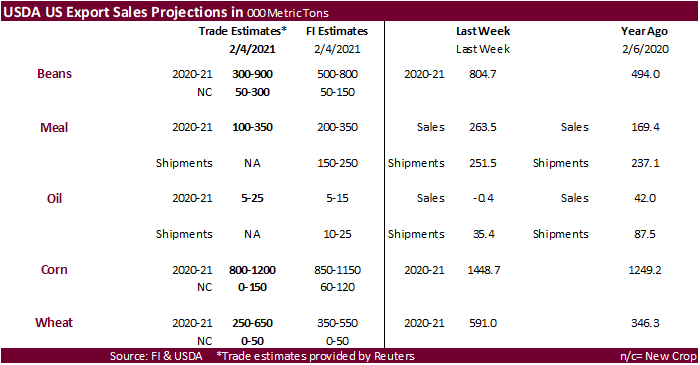

export sales will be out Friday.

![]()

USDA

Agriculture Outlook Forum

USDA

comments/speeches from the annual agriculture outlook forum will trickle out over the next week. Slides/speeches posted here

https://www.usda.gov/oce/ag-outlook-forum/aof-program

Or

follow it on Twitter

https://twitter.com/hashtag/AgOutlook?src=hashtag_click

NASS

is due out Friday with their initial 2021-22 US S&D statistical estimates. Those will be available to everyone early Friday.

https://www.usda.gov/oce/ag-outlook-forum

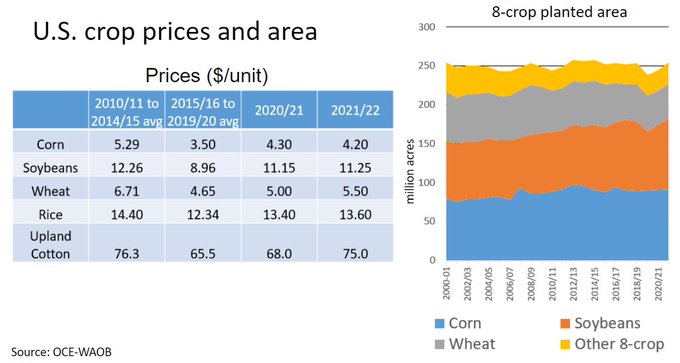

US

area:

Corn

92

Soybeans

90

Wheat

45

Cotton

12 (that is higher than National Cotton Council)

Average

$

Corn

$4.20

Soybeans

$11.25

Wheat

$5.50

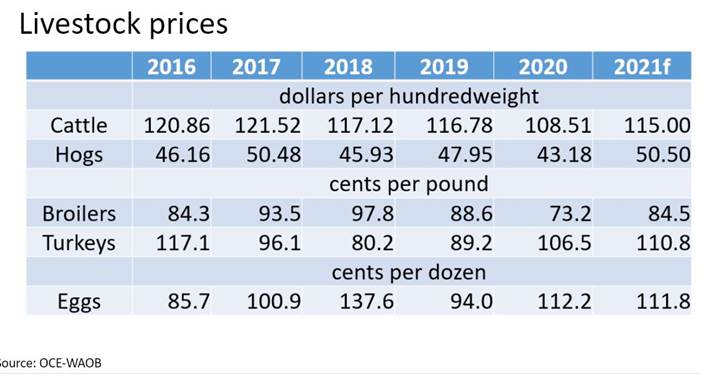

Cattle

115.00

Hogs

50.50

Chief

Economist Seth Meyer: drought impacted the size of the crop this year, but events such as the Derecho had a significant impact

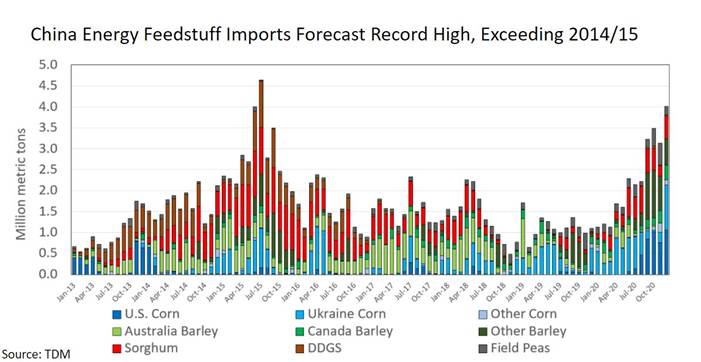

Chief

Economist Seth Meyer: China imports have been very corn focused

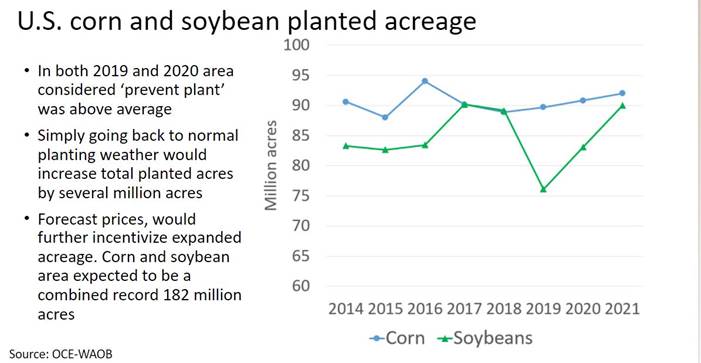

Chief

Economist Seth Meyer: if one assumes, we have normal planting weather, we will have an increase in total planted acres. But that’s entirely dependent on the weather

USDA

SEES FISCAL 2021 U.S. FARM EXPORTS AT $157 BLN

USDA

SEES U.S. FARM EXPORTS TO CHINA AT $31.5 BLN IN FY 2021

-

NWS

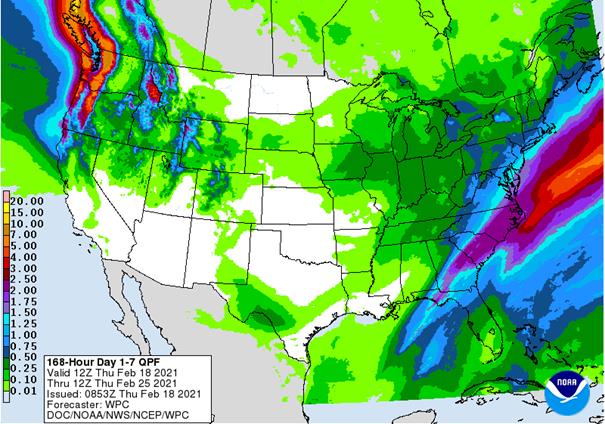

30-Day Outlook for U.S. – is classic La Nina -

March

was advertised to be wetter than usual in the Midwest (east of the Mississippi River) and northeast into New York and northwestern New England -

The

wet bias extends southward into Tennessee -

March

was also wetter biased in Montana, northwestern Wyoming and the mountains of Idaho -

Below

average precipitation was suggested for the central and southern Plains, Gulf of Mexico coastal areas, Florida, central and southern Georgia, South Carolina and southeastern North Carolina as well as in the southern Rocky Mountains, the southwestern desert

region and central and southern California -

Equal

chances for above, below and near normal precipitation was advertised elsewhere -

Temperatures

in March were advertised warmer than usual in the majority of the nation, but not in the Pacific Northwest where readings were advertised colder than usual. -

Equal

chances for above, below and near normal temperatures was suggested for central California, Nevada, northern Utah, the Dakotas, northern Nebraska, Minnesota, northern Iowa, and much of Wisconsin -

NWS

90-Day Outlook for U.S. – also follows traditional La Nina bias -

March

through May temperatures will be warmer than usual except in Washington state, far northern Idaho and far northwestern Montana where readings were advertised cooler than usual -

There

was an equal chance for above, below and near normal temperatures from far northern California and Oregon through the remainder of Montana and northwestern Wyoming to North Dakota, much of Minnesota, Upper Michigan and northern Wisconsin -

March

through May precipitation was advertised wetter than usual in the heart of the Midwest (mostly east of the Mississippi River) and extending northeast into western and northern New York and far northwestern New England -

Washington

state and areas east into northwestern Montana were also advertised to be wetter biased -

Below

average precipitation was suggested for the central and southern Plains, the southern Rocky Mountain region, much of California and the southwestern desert region along with Nevada.

-

Florida

and areas from southern Georgia to Louisiana were also advertised to be drier than usual -

Equal

chances for above, below and near normal precipitation was suggested for most other areas.

-

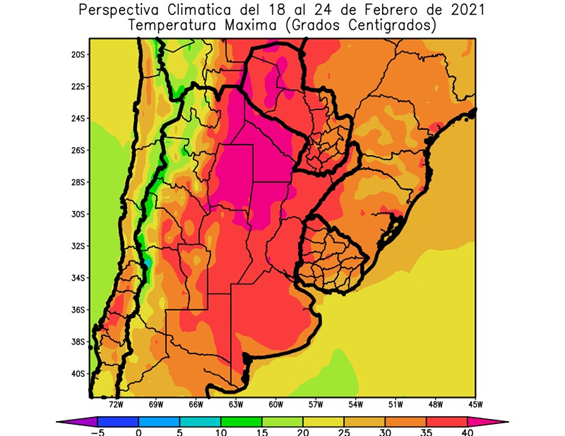

Argentina

weather will continue to dry down over the next ten days -

The

latest soil assessment shows most of the nation’s key crop areas still have good subsoil moisture -

Rapid

drying is expected in the coming week as temperatures turn seasonably warm and precipitation is limited to sporadic showers -

Greater

rain will be needed in the last days of February and early March to prevent moisture stress from becoming an issue for late season crops -

Today’s

GFS model suggested greater rain in the first week of March, but this was likely overdone -

Some

showers are expected, and they may offer some partial relief from previous drying -

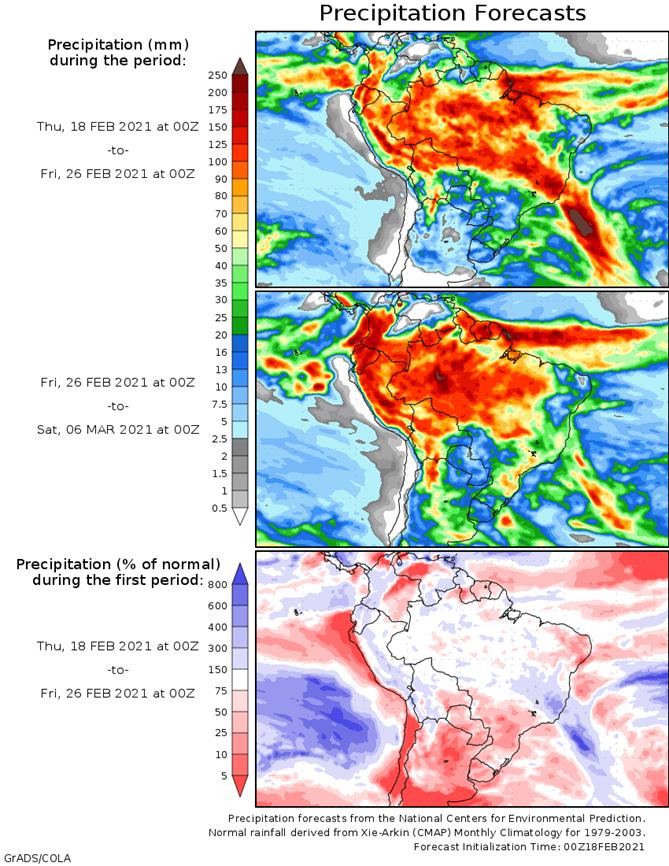

Brazil

crop weather will continue mixed -

Rain

frequency and intensity will remain a little greater than desired across Mato Grosso, Goias and Minas Gerais during the next couple of weeks -

However,

rain does not fall substantially every day and World Weather, Inc. believes enough drying will occur to support some slow field progress -

Southern

Brazil will experience less frequent and less significant rain and many areas from Mato Grosso do Sul and southwestern Sao Paulo into Rio Grande do Sul and Paraguay will experience a good mix of weather -

Enough

sunny and warm conditions will occur to promote soybean maturation and harvesting along with Safrinha corn planting -

Soil

moisture will remain supportive of ongoing full season and late season crops and there will be some timely rainfall to maintain those conditions -

Argentina

early soybeans were 50% setting pods and 6% filling pods last week -

Late

planted soybeans were 40% flowering -

This

data was provided from “Soybeans and Corn Advisor” -

Argentina

early corn was 52% filling and 16% mature -

Harvesting

was expected to begin this week -

Late

planted corn was 50% pollinated -

Corn

was rated 9% poor, 69% average and 23% good to excellent that compares to 25% good to excellent last week and 62% average -

This

data was provided from “Soybeans and Corn Advisor” -

South

Africa will experience net drying through the weekend, but timely rain will fall in many areas next week maintaining a very good production outlook -

Recent

rain in eastern Australia cotton and sorghum production areas has been ideal for supporting crops

-

Alternating

periods of rain and sunshine will resume in the coming week and continue into early March -

China

winter crop conditions are rated quite favorably -

Wheat

is dormant in most of the nation, but was well established last autumn and soil moisture is favorable for this time of year -

Rapeseed

is breaking dormancy in the south and has abundant soil moisture -

Plant

development will be slow over the next couple of weeks -

Soil

moisture will remain abundant -

India

will began reporting light rainfall Wednesday and will receive additional scattered showers in central and southern parts of the nation the remainder of this week -

The

moisture will be ideal for reproducing winter crops, but probably a little too light for a lasting impact -

Rain

is still needed in the north and west and more precipitation will still be desirable -

The

nation’s winter crops should yield well this year -

No

excessive heat is expected in the coming week, but warming is likely in the last week of this month -

Snow

cover in eastern Europe and the western CIS is more than sufficient to protect winter crops from adverse weather -

Very

little winterkill has occurred this year -

Bitter

cold will remain over Russia’s New Lands in the coming ten days -

No

snow free area in southern Russia or Europe will be subjected to any threatening weather -

Europe

weather is expected to quiet for a while – at least in the heart of the continent -

The

more limited precipitation bias will be great for runoff to continue which will eventually reduce the risk of more serious flooding -

The

United Kingdom, western Norway and northwestern Spain will continue to see bouts of heavy rainfall resulting in some flooding in those areas -

Winter

crops are still dormant in most of the continent and rated favorably -

Morocco

and northwestern Algeria will receive some needed moisture this weekend into early next week and possibly again late next week -

The

precipitation will help ease dryness in southwestern Morocco and northwestern Algeria while maintaining good crop and field conditions in north-central Morocco -

Routinely

occurring rain is expected in the Middle East wheat and cotton production areas improving soil moisture for some of the drier areas in Iran and Afghanistan and maintaining good moisture in Turkey, Syria and Iraq -

North

America’s extreme cold is abating and will continue doing so into the weekend with temperatures near to above average possible in some areas for a little while next week -

The

warmup will last about ten days in the central and eastern U.S. while the western states start to cool down -

The

second week of March may bring cooling back to the eastern half of North America or at least central areas and the coolness will then drift to the east over time -

U.S.

Weather in the next week -

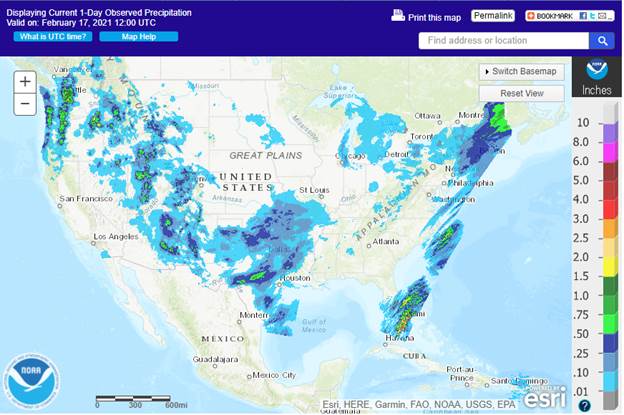

A

serious ice storm will impact Virginia, North Carolina, Maryland and neighboring areas today -

Snow

will pile up today from the Appalachian Mountains and parts of central and western North Carolina into New York and New England -

Snowfall

will vary from 3 to 10 inches and local amounts over 12 inches with the mountains of Pennsylvania, West Virginia and Virginia being most impacted -

One

more shot of cold air will push through the eastern U.S. following this week’s storm system -

Weather

systems this weekend and next week will move in quick succession across parts of the Plains and into the Midwest maintaining moisture abundance -

Melting

snow is also expected in the Plains late this week into next week -

No

more threatening cold is expected after Thursday morning -

Another

relatively large storm may impact the lower Midwest and middle Atlantic Coast states late next week -

Snow

fell significantly from the Delta into the Tennessee River Basin, southwestern Pennsylvania and a part of the lower Midwest Wednesday -

Accumulations

of 2 to 6 inches were common with a few totals of 7 inches or more -

Temperatures

were still bitterly cold across the Plains and parts of the Midwest Wednesday, but readings will slowly moderate over the next few days -

Southern

Ghana and Ivory Coast received additional Wednesday -

Some

flowering might have occurred since some of this region reported rain Tuesday as well -

Greater

and more uniform rain is needed to induce a more generalized bout of flowering in coffee and cocoa areas, but the showers occurring now are not unusual for February and should increase next month -

Other

areas in west-central Africa will see most of this week’s rain occurring near the coast -

Southeast

Asia weather is not likely to change much in the coming week, although some additional heavy rain will overtake much of the Philippines this weekend into early next week causing some local flooding -

A

tropical cyclone is possible this weekend in southern and central Philippines -

East-central

Africa precipitation over the next ten days will be most significant in Tanzania and lightest in Ethiopia -

All

of the rain will be welcome and beneficial -

Southern

Oscillation Index weakened during the weekend and this trend will continue this week -

Today’s

SOI was +12.74 today and the index will move erratically over the next week -

Mexico

precipitation in the coming week will be mostly confined to the east coast. although a few showers may occur briefly in the far north too -

Central

America precipitation will continue greatest along the Caribbean Coast and in Guatemala while the Pacific Coast is relatively dry -

Canada

Prairies will experience warmer temperatures over the next several days week with readings becoming much closer to normal -

Precipitation

will continue limited -

Southeast

Canada will experience near normal amounts of precipitation in the coming week while temperatures are seasonable.

Source:

World Weather Inc. and FI

Thursday,

Feb 18:

- EIA

weekly U.S. ethanol inventories, production - USDA

Net Export Sales, 8:30am - USDA

Corn, Cotton, Soybean, Wheat Acreage Outlook, 8:30am - Sime

Darby Plantation earnings - Port

of Rouen data on French grain exports

Friday,

Feb 19:

- ICE

Futures Europe weekly commitments of traders report, 1:30pm (6:30pm London) - CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm - FranceAgiMer

crop conditions report - USDA

Corn, Cotton Soybean, Wheat End Stock Outlook, 7am - U.S.

Cattle on Feed, 3pm

Monday,

Feb 22:

- USDA

Export Inspections – corn, soybeans, wheat, 11am - EU

weekly grain, oilseed import and export data - MARS

crop bulletin - Ivory

Coast cocoa arrivals - EARNINGS:

Wilmar - HOLIDAY:

Russia

Tuesday,

Feb 23:

- USDA

Milk production, 3pm - U.S.

pork, beef, poultry cold storage data, 3pm - U.K.

National Farmers Union virtual annual conference to discuss the future of agriculture, horticulture - EARNINGS:

IOI Corp. - HOLIDAYS:

Japan, Russia

Wednesday,

Feb 24:

- EIA

weekly U.S. ethanol inventories, production - Amsterdam

sustainable cocoa conference (Feb 24-26) - U.S.

poultry slaughter, 3pm - MPOB

palm oil prices seminar

Thursday,

Feb 25:

- USDA

weekly crop net-export sales for corn, soybeans, wheat, cotton, pork, beef, 8:30am - Port

of Rouen data on French grain exports - International

Grains Council monthly report - Malaysia’s

Feb. 1-25 palm oil export data - USDA

red meat production, 3pm - EARNINGS:

Minerva, BRF, FGV (tentative), Golden Agri

Friday,

Feb 26:

- ICE

Futures Europe weekly commitments of traders report, 1:30pm (6:30pm London) - CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm - U.S.

agricultural prices paid, received, 3pm - Earnings:

Olam - HOLIDAY:

Thailand

RINS

The

following is a table of the credit generation for the month of January by credit type.

RINs Volume (Gal.)

D3

4,442,298 4,442,298

D4

300,219,091 190,219,039

D5

19,415,774 12,580,794

D6

1,077,475,275 1,075,130,541

Source

Reuters and FI

US

Initial Jobless Claims Feb 13 861K (est 765K; prevR 848K; prev 793K)

–

US Continuing Claims Feb 6 4.494 Mln (est 4.413 Mln; prevR 4.558 Mln; prev 4.545 Mln)

US

Housing Starts Jan 1.580 Mln (est 1.658 Mln; prevR 1.680 Mln; prev 1.669 Mln)

–

US Building Permits Jan 1.881 Mln (est 1.678 Mln; prevR 1.704 Mln; prev 1.709 Mln)

US

Import Price Index (M/M) Jan 1.4% (est 1.0%; prev 0.9%)

–

US Import Price Index Ex. Petroleum (M/M) Jan 0.9% (est 0.4%; prev 0.4%)

–

US Import Price Index (Y/Y) Jan 0.9% (est 0.4%; prev -0.3%)

–

US Export Price Index (M/M) Jan 2.5% (est 0.8%; prev 1.1%)

–

US Export Price Index (Y/Y) Jan 2.3% ( prev 0.2%)

Canada

ADP Employment Change Jan -231.2K (prevR 338.0K; prev -28.8K)

US

DoE Crude Oil Inventories (W/W) 12-Feb: -7257K (est -2150K; prev -6645K)

–

Distillate Inventories: -3422K (est -1549K; prev -1732K)

–

Cushing OK Crude Inventories: -3028K (prev -658K)

–

Gasoline Inventories: 372K (est 1477K; prev 4259K)

–

Refinery Utilization: 0.1% (est -0.3%; prev 0.7%)

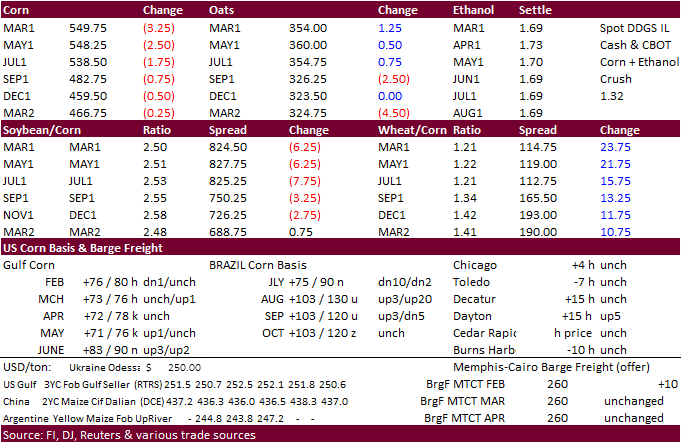

Corn.

-

Corn

futures ended mostly lower in part to bear spreading in soybeans. Less than expected 92 million area US corn planting outlook for 2021 (92.9 Reuters guess) did little to stop overall selling but in the end may have influenced late bear spreading. News was

light. Some traders were waiting out to see what the extent of the damage had from the recent US cold temperatures and heavy snow prompting reports of forces majeures for exports. We are hearing US logistic problems started easing yesterday. USDA export

inspections on Monday will be the first indication if the cold weather had a significant impact on exports. Texas ranchers, home to about 13 million cattle, are still working around the clock to save animals from the cold weather and lack of fresh water.

-

March

support over the short term is seen at $5.47. -

Euronext

suspended trading in its corn futures and options contracts for January 2023 pending a review of technical specifications. -

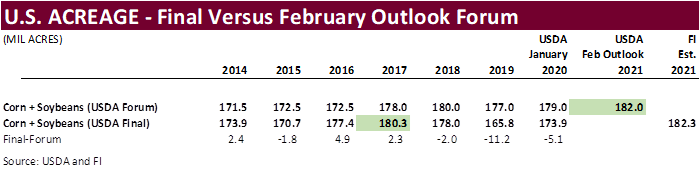

The

92 million acres USDA projected for the US corn crop was the only figure that initially stood out this morning in USDA’s “2021 Agricultural Economic & Foreign Trade Outlook” speech, as it came in below trade expectations. But combining soybeans (90.0), the

182.0 million acre outlook would be a record for any year if realized. Historically the final planted area varies from USDA’s initial outlook.

Weekly

US ethanol production

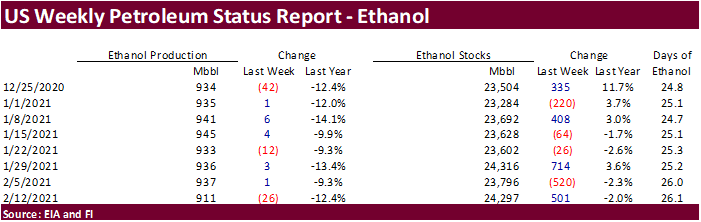

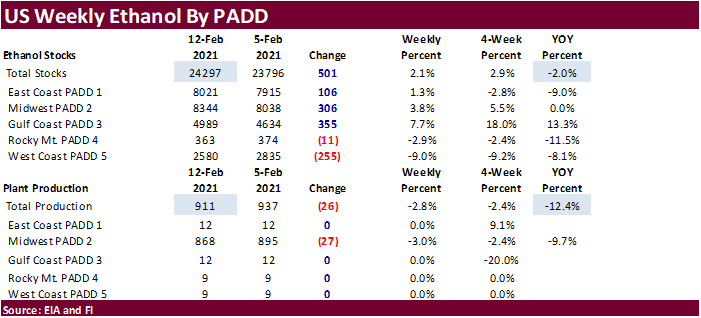

last week was off 26,000 barrels to 911,000 barrels (trade was looking down 17,000) and stocks were up 501,000 barrels to 24. (trade 48,000 increase) from the previous week. Ethanol production was lowest since September 25. Stocks are at a three-week high.

Early September to date ethanol production is running 8.5 percent below the same period a year ago. Based on weekly ethanol production, implied corn use using September to date average weekly ethanol production suggests 5.162 billion bushels, but if ethanol

production from now until the end of the year remained unchanged, implied use would stand at 5.067 billion bushels. However, several ethanol plants went offline earlier this week, or slowed, and we it is nearly impossible to predict when US ethanol production

will return to a pre-pandemic level, so those figures can’t be taken seriously. USDA is using 4.950 billion. US gasoline stocks increased 672,000 barrels to 257.1 million. US gasoline demand was up from the previous week but overall running 5.7 percent

below a year ago. US crude oil stocks fell to lowest since March.

Corn

Export Developments

·

None reported

Updated

2/10/21

March

corn is seen trading in a $5.20 and $6.00 range

May

corn is seen in a $5.15 and $6.00 range.

July

is seen in a $5.00 and $6.00 range.

December

corn is seen in a $3.75-$5.50 range.