PDF Attached

WORLD

WEATHER OF GREATEST INTEREST

- Argentina

weather will continue to dry down over the next ten days to two weeks - The

latest soil assessment shows most of the nation’s key crop areas still have good subsoil moisture - Rapid

drying is expected in the coming week as temperatures turn seasonably warm and precipitation is limited to sporadic showers - Greater

rain will be needed in the last days of February and early March to prevent moisture stress from becoming an issue for late season crops - Brazil

crop weather will continue mixed - Rain

frequency and intensity will remain a little greater than desired across Mato Grosso, Goias and Minas Gerais during the next couple of weeks - However,

rain does not fall substantially every day and World Weather, Inc. believes enough drying will occur to support some slow field progress - Southern

Brazil will experience less frequent and less significant rain and many areas from Mato Grosso do Sul and southwestern Sao Paulo into Rio Grande do Sul and Paraguay will experience a good mix of weather - Enough

sunny and warm conditions will occur to promote soybean maturation and harvesting along with Safrinha corn planting - Soil

moisture will remain supportive of ongoing full season and late season crops and there will be some timely rainfall to maintain those conditions - Brazil

soybean harvest as of late last week was 9% harvested compared to 24% last year and 20% average, according to AgRural (data provided by Corn and Soybean Advisor) - Mato

Grosso was 22.2% harvested compared to 58.2 last year and 45.4% average - Harvest

was most advanced in the north where the greatest rainfall is forthcoming - Parana

soybeans were 13% flowering, 67% filling and 19% mature with 1% harvested as of late last week - Goias

soybeans were 10% harvested - Brazil

Safrinha corn planting was 11% done compared to 31% average, according to AgRural (data provided by Corn and Soybean Advisor)

- Optimal

planting window closes after Feb. 20 - 60%

or more of the crop will be planted after the optimal date is passed - Mato

Grosso planting was 20.9% done compared to 63% last year and 47% average - Parana

full season corn was 10% harvested and Safrinha planting was 3% done - Rio

Grande do Sul full season corn was 13% pollinating, 20% filling, 16% mature and 39% harvested as of late last week - South

Africa will experience net drying through the weekend, but timely rain will fall in many areas next week maintaining a very good production outlook - Recent

rain in eastern Australia cotton and sorghum production areas has been ideal for supporting crops

- Net

drying will occur for a while, but more rain is expected later in the forecast period - China

winter crop conditions are rated quite favorably - Wheat

is dormant in most of the nation, but was well established last autumn and soil moisture is favorable for this time of year - Rapeseed

is breaking dormancy in the south and has abundant soil moisture - Plant

development will be slow over the next couple of weeks - Soil

moisture will remain abundant - India

will receive scattered showers in central and southern parts of the nation the remainder of this week - The

moisture will be ideal for reproducing winter crops - Rain

is still needed in the north and west and more precipitation will still be desirable - The

nation’s winter crops should yield well this year - No

excessive heat is expected in the coming week, but warming is likely in the last week of this month - Snow

cover in eastern Europe and the western CIS is more than sufficient to protect winter crops from adverse weather - Very

little winterkill has occurred this year - Bitter

cold will remain over Russia’s New Lands in the coming ten days - No

snow free area in southern Russia or Europe will be subjected to any threatening weather - Europe

weather is expected to quiet for a while – at least in the heart of the continent - The

more limited precipitation bias will be great for runoff to continue which will eventually reduce the risk of more serious flooding - The

United Kingdom, western Norway and northwestern Spain will continue to see bouts of heavy rainfall resulting in some flooding in those areas - Winter

crops are still dormant in most of the continent and rated favorably - Morocco

and northwestern Algeria will receive some needed moisture this weekend into early next week - The

precipitation will help ease dryness in southwestern Morocco and northwestern Algeria while maintaining good crop and field conditions in north-central Morocco - Routinely

occurring rain is expected in the Middle East wheat and cotton production areas improving soil moisture for some of the drier areas in Iran and Afghanistan and maintaining good moisture in Turkey, Syria and Iraq - North

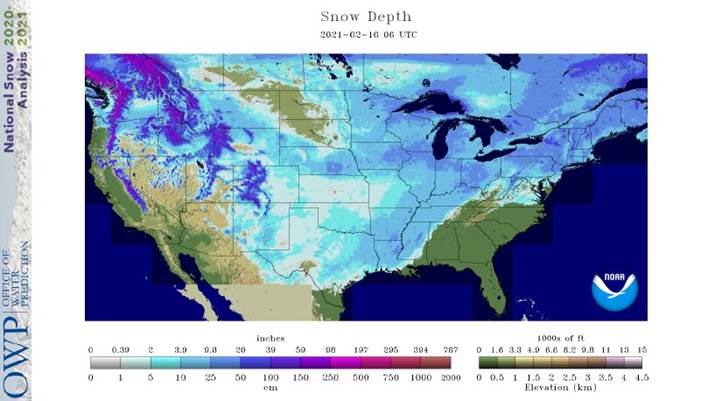

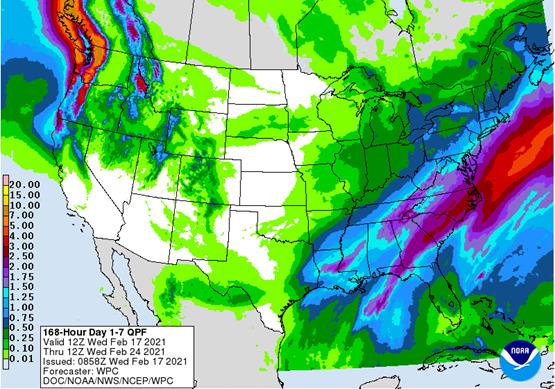

America’s extreme cold will be abating later this week and into the weekend with temperatures near to above average possible next week - U.S.

Weather in the next week - A

serious ice storm will impact Virginia, North Carolina, Maryland and neighboring areas Thursday - Snow

will pile up again today in the Delta and will shift through the lower eastern Midwest to the northeastern United States Thursday and early Friday - One

more shot of cold air will push through the eastern U.S. following this week’s storm system - Weather

systems this weekend and next week will move in quick succession across parts of the Plains and into the Midwest maintaining moisture abundance - Melting

snow is also expected in the Plains late this week into next week - No

more threatening cold is expected after Thursday morning - Snow

fell significantly in the central Texas Panhandle overnight with up to 9 inches resulting east of Amarillo - Other

areas received 2 to 7 inches - Oklahoma

snowfall overnight ranged from 2 to 6 inches and some of that extended into Arkansas, Missouri and southeastern Kansas - Temperatures

were still bitterly cold across the Plains and parts of the Midwest Tuesday, but readings will slowly moderate over the next few days - Eastern

Ghana and Ivory Coast received some rain during Sunday and Monday - Erratic

flowering might have occurred especially when that moisture was combined with rain that fell in a few areas last week - Greater

and more uniform rain is needed to induce a more generalized bout of flowering in coffee and cocoa areas, but the showers occurring now are not unusual for February and should increase next month - Other

areas in west-central Africa will see most of this week’s rain occurring near the coast - Southeast

Asia weather is not likely to change much in the coming week, although some additional heavy rain will overtake much of the Philippines this weekend into early next week causing some local flooding - A

tropical cyclone is possible this weekend in southern and central Philippines - East-central

Africa precipitation over the next ten days will be most significant in Tanzania and lightest in Ethiopia - All

of the rain will be welcome and beneficial - Southern

Oscillation Index weakened during the weekend and this trend will continue this week - Today’s

SOI was +12.53 today and the index will move erratically over the next week - Mexico

precipitation in the coming week will be mostly confined to the east coast. although a few showers may occur briefly in the far north too - Central

America precipitation will continue greatest along the Caribbean Coast and in Guatemala while the Pacific Coast is relatively dry - Canada

Prairies will experience warmer temperatures this week with readings becoming much closer to normal - Precipitation

will continue limited - Southeast

Canada will experience greater than usual precipitation this week and seasonably cool temperatures

Source:

World Weather Inc. and FI

Wednesday,

Feb 17:

- KL

Kepong earnings - HOLIDAY:

China

Thursday,

Feb 18:

- EIA

weekly U.S. ethanol inventories, production - USDA

Net Export Sales, 8:30am - USDA

Corn, Cotton, Soybean, Wheat Acreage Outlook, 8:30am - Sime

Darby Plantation earnings - Port

of Rouen data on French grain exports

Friday,

Feb 19:

- ICE

Futures Europe weekly commitments of traders report, 1:30pm (6:30pm London) - CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm - FranceAgiMer

crop conditions report - USDA

Corn, Cotton Soybean, Wheat End Stock Outlook, 7am - U.S.

Cattle on Feed, 3pm

U.S.

Oil Production Has Plunged by a Third Amid Deep Freeze

Houston

Power Outages Could Last Several Days, CenterPoint Says

US

Retail Sales Advance Jan: 5.3% (exp 1.1%; R prev -1.0%)

–

Retail Sales Ex-Auto (M/M) Jan: 5.9% (exp 1.0%; R prev -1.8%)

–

Retail Sales Ex-Auto And Gas Jan: 6.1% (exp 0.9%; R prev -2.5%)

–

Retail Sales Control Group Jan: 6.0% (exp 1.0%; R prev -2.4%)

US

PPI Final Demand (M/M) Jan: 1.3% (exp 0.4%; prev 0.3%)

–

PPI Ex-Food And Energy (M/M) Jan: 1.2% (exp 0.2%; prev 0.1%)

–

PPI Ex-Food, Energy, Trade (M/M) Jan: 1.2% (exp 0.2%; prev 0.1%)

–

PPI Final Demand (Y/Y) Jan: 1.7% (exp 0.9%; prev 0.8%)

–

PPI Ex-Food And Energy (Y/Y) Jan: 2.0% (exp 1.1%; prev 1.2%)

–

PPI Ex-Food, Energy, Trade (Y/Y) Jan: 2.0% (exp 1.0%; prev 1.1%)

Canadian

CPI (Y/Y) Jan: 1.0% (exp 0.9%; prev 0.7%)

–

CPI NSA (M/M) Jan: 0.6% (exp 0.5%; prev -0.2%)

–

CPI Core Median (Y/Y) Jan: 1.4% (exp 1.8%; prev 1.8%)

–

CPI Core Common (Y/Y) Jan: 1.3% (exp 1.4%; prev 1.3%)

–

CPI Core Trim (Y/Y) Jan: 1.8% (exp 1.6%; prev 1.6%)

US

Industrial Production (M/M) Jan: 0.9% (exp 0.5%; prev 1.6%)

–

Capacity Utilisation Jan: 75.6% (exp 74.9%; prev 74.5%)

–

Manufacturing (SIC) Production Jan: 1.0% (exp 0.7%; prev 0.9%)

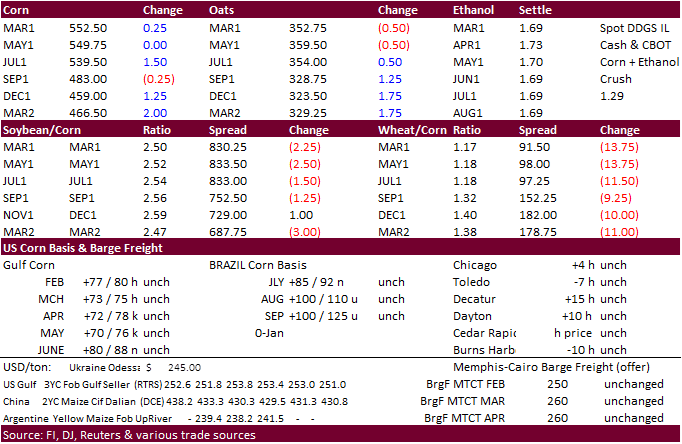

Corn.

-

March

corn ended 0.75 cent higher after trading two-sided. -

Corn

futures started lower following a higher USD and weakness in wheat but rallied late to close higher. South Korea bought US corn, but the amount was about half of what they were seeking. Slowing grain crush at ethanol and other industrial plants across the

US should results in a dent in the February US domestic use. Icy rivers are slowing grain flow to ports for export. By early morning basis along rivers were mostly steady.

-

March

support over the short term is seen at $5.47, then $5.38. -

Lunar

New Year holiday wrapped up in China and traders are looking for them to soon return to import market.

-

We

heard IHS Markit raised their Argentina corn production estimate by 0.5 million tons to 47 and decreased Brazil production by 0.4 million tons to 108.6 million.

-

A

Reuters poll sees USDA NASS on Friday reporting a 92.9 million US area, 178.4 yield and 15.160 billion production with a 1.665 billion carryout for 2021-22 crop year.

-

Some

meat plants in Texas are down from the cold weather and power outages. It may take at last a week to find out the extend of the damage this event had on the US.

-

The

USDA Broiler Report showed eggs set in the United States down 1 percent and chicks placed down 2 percent. Cumulative placements from the week ending January 9, 2021 through February 13, 2021 for the United States were 1.12 billion. Cumulative placements were

down 2 percent from the same period a year earlier. -

Bloomberg

– Feb. 1 herd seen rising y/y to 12.038m, seventh straight y/y expansion since June of last year. January placements seen down 0.2% . -

BADI

Baltic Dry Index increased 17.5 percent to 1,756 points. It was up 131 points yesterday or 9.6%. Yesterday Alibra Shipping via Hellenic Shipping News Worldwide said it is the “FFA (Forward Freight Agreement) sentiment that is pushing up the capesize index,

which could be coming from hopes of further vaccine roll outs boosting demand.”

https://www.hellenicshippingnews.com/buoyant-rates-lift-baltic-index-to-near-three-week-high/

Corn

Export Developments

·

South Korea’s MFG bought about 69,000 tons of corn, thought to be from the US, at an estimated $295.40 a ton c&f for June 21 arrival.

Updated

2/10/21

March

corn is seen trading in a $5.20 and $6.00 range

May

corn is seen in a $5.15 and $6.00 range.

July

is seen in a $5.00 and $6.00 range.

December

corn is seen in a $3.75-$5.50 range.