PDF Attached includes selected global STU graphs

US

Holiday Monday. Several other countries will also be on holiday. CBOT reopens Monday night.

WASHINGTON,

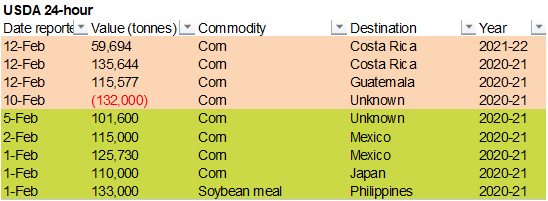

February 12, 2021—Private exporters reported to the U.S. Department of Agriculture the following activity:

Export

sales of 195,338 metric tons of corn for delivery to Costa Rica. Of the total, 135,644 metric tons is for delivery during the 2020/2021 marketing year and 59,694 metric tons is for delivery during the 2021/2022 marketing year; and

Export

sales of 115,577 metric tons of corn for delivery to Guatemala during the 2020/2021 marketing year.

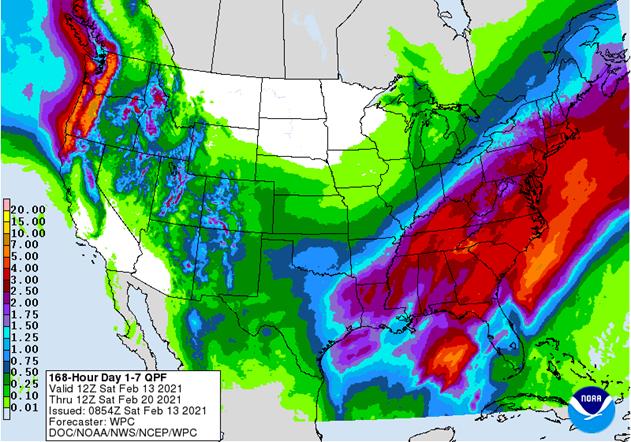

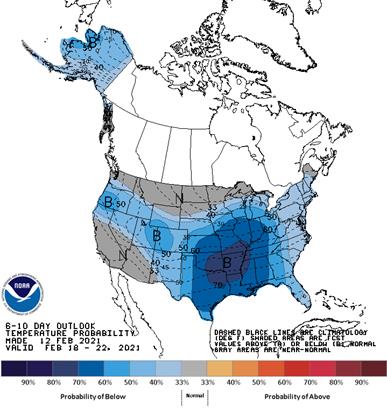

Source:

World Weather Inc. and FI

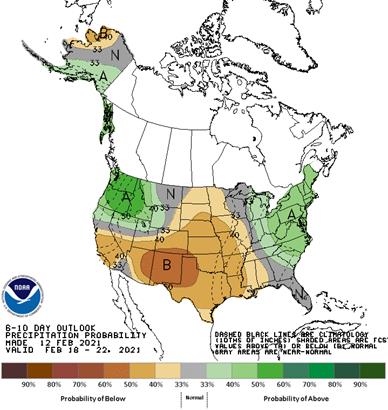

Source:

World Weather Inc. and FI

MARKET

WEATHER MENTALITY FOR CORN AND SOYBEANS:

Market

worry over Brazil harvest weather for soybeans and planting progress for Safrinha corn will continue, although the past week has been ideal in firming up the topsoil and supporting faster fieldwork. Expected rain over this coming week will disrupt fieldwork,

but it will not likely bring all field operations to a halt. Northern and eastern Mato Grosso may have the biggest problem with rain delays, although some will occur in other areas, as well.

In

Argentina, weather conditions are expected to be mixed with areas of drying from the southwest into central parts of the nation that may eventually raise a few flags, but there is still time for the outlook to change as crops thrive on favorable subsoil moisture

outside of southern La Pampa and southwestern Buenos Aires where conditions are already too dry.

South

Africa production remains good with little change likely. Recent rain in New South Wales has been good for summer crop development, But Queensland needs greater rain.

Weather

in rapeseed areas of China remains favorable and the same is true for India, although greater rain might be good for all of its winter crop areas this month.

Winter

crops in Europe are plenty wet and cold with little change likely for a while. No harm to crops in the continent will occur anytime soon. That is true for Ukraine crops as well. There is a rising potential for flooding in far western Europe, northwestern and

west-central Russia and in western and north-central Ukraine this spring because of wet soil and deep snow cover outside of Western Europe.

Overall,

weather today will continue to maintain a floor of support for the market’s bullishness, but caution is still warranted because the perception of what is happening in Brazil may be a little skewed from reality.

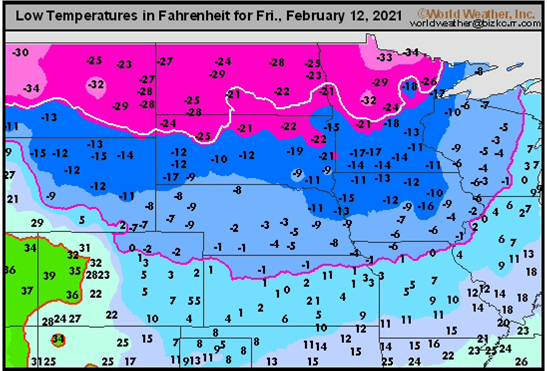

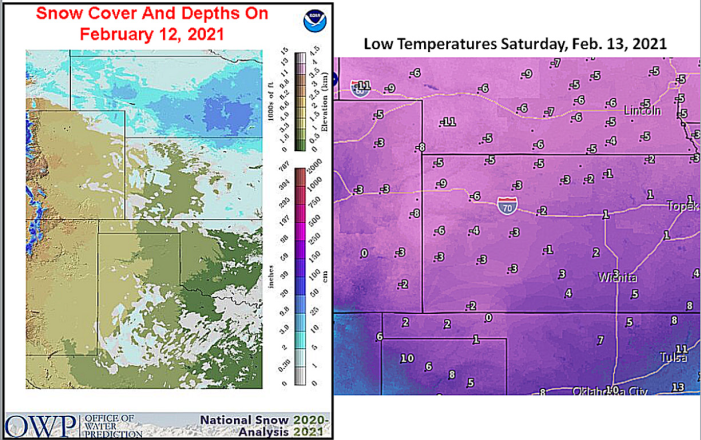

MARKET

WEATHER MENTALITY FOR WHEAT: Most of the wheat production losses in the northern U.S. Plains from recent bitter cold should be low from a national perspective, but locally farmers will not be pleased. Damage in Canada was even less of an impact on its winter

grain crop, but some loss is expected there as well.

There

is some potential for crop damage in a few Kansas and Colorado production areas Saturday as temperatures drop near and below zero Fahrenheit in snow free areas. Crops in the region have been adequately hardened against the cold which should help reduce the

risk of loss, but damage cannot be ruled out. After that, snow will fall across most wheat areas in Kansas to protect crops from the coldest weather expected late this weekend and early next week. That should prevent any potential for additional damage.

Mostly

of the U.S. Midwest will also receive snow before temperatures get cold enough for damage. Only a few locations in the region are snow free and the potential for loss is low.

No

crop damage has occurred in Europe or the western CIS so far this season and this week will likely maintain a mostly good environment for crops with snow cover to adequately protect wheat, barley and rye from permanent damage because of bitter cold temperatures.

Wheat conditions in China remain very good and that of India are fair to good. Rain is needed in most of India to induce better yield potentials, although the nation is still expecting a fair-sized crop. Some moisture will occur in central India next week.

North

Africa wheat is drying out except in north-central Morocco where conditions have been ideal. Drought has already cut into southwestern Morocco production and the same may occur in northwestern Algeria if spring rainfall is not very good.

Middle

East precipitation has been erratic and often light this winter and a boost in precipitation would be welcome especially from Iraq to Afghanistan. Turkey precipitation has been better distributed than in most other areas.

Overall, weather today will likely produce a mixed influence on market mentality.

Source:

World Weather Inc. and FI

Friday,

Feb 12:

- ICE

Futures Europe weekly commitments of traders report, 1:30pm (6:30pm London) - CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm - Russian

consultant IKAR holds agricultural conference, day 2 - New

Zealand Food Prices - HOLIDAY:

China, Hong Kong, Indonesia, Malaysia, South Korea, Singapore, Vietnam, Thailand, Philippines

Monday,

Feb 15:

- Malaysia’s

Feb. 1-15 palm oil export data - Malaysia

CPO export tax for March (tentative) - EU

weekly grain, oilseed import and export data - Ivory

Coast cocoa arrivals - HOLIDAYS:

Chinese New Year, U.S., Canada, and Carnival holiday in much of South America including Brazil and Argentina

Tuesday,

Feb 16:

- USDA

Export Inspections, 11am - Abares

February Australian crop report - MPOB

and Universiti Kebangsaan Malaysia webinar on palm oil’s marketability to EU - Green

Coffee Association releases U.S. monthly green coffee stockpiles data - USDA

sugar and sweeteners outlook - New

Zealand dairy trade auction - Tereos

earnings - HOLIDAYS:

China, Carnival holiday throughout much of South America

Wednesday,

Feb 17:

- KL

Kepong earnings - HOLIDAY:

China

Thursday,

Feb 18:

- EIA

weekly U.S. ethanol inventories, production - USDA

Net Export Sales, 8:30am - USDA

Corn, Cotton, Soybean, Wheat Acreage Outlook, 8:30am - Sime

Darby Plantation earnings - Port

of Rouen data on French grain exports

Friday,

Feb 19:

- ICE

Futures Europe weekly commitments of traders report, 1:30pm (6:30pm London) - CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm - FranceAgiMer

crop conditions report - USDA

Corn, Cotton Soybean, Wheat End Stock Outlook, 7am - U.S.

Cattle on Feed, 3pm

Trade

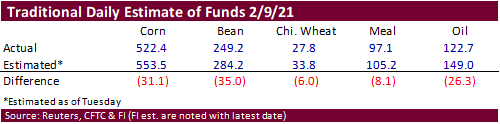

estimates for the traditional funds were nowhere near actual for the week ending February 9th, a testament that when you see volatile markets the trade tends to miss CFTC traditional and managed money positions. Key takeaway is there is price upside left

for managed money to reach multi month and/or multiyear record net long positions if we continue to see the uptrend in CBOT agriculture futures.

SUPPLEMENTAL

Non-Comm Indexes Comm

Net Chg Net Chg Net Chg

Corn

386,552 2,685 395,142 8,516 -771,378 -18,127

Soybeans

158,440 12,389 154,281 10,459 -316,822 -26,530

Soyoil

73,799 2,800 132,723 3,899 -229,111 -8,069

CBOT

wheat -7,613 -2,131 143,015 6 -124,841 -149

KCBT

wheat 34,922 3,143 66,682 -2,080 -103,861 -2,188

=================================================================================

FUTURES

+ OPTS Managed Swaps Producer

Net Chg Net Chg Net Chg

Corn

358,807 13,659 257,367 10,867 -761,374 -18,898

Soybeans

171,770 15,506 68,097 7,674 -293,187 -25,813

Soymeal

69,625 2,114 67,701 3,589 -192,042 -10,576

Soyoil

110,392 4,462 89,597 3,070 -235,512 -8,031

CBOT

wheat 19,306 -578 86,685 -1,689 -108,674 3,699

KCBT

wheat 60,092 3,691 42,088 -1,553 -98,508 -2,098

MGEX

wheat 12,933 -1,167 3,805 63 -21,813 2,648

———- ———- ———- ———- ———- ———-

Total

wheat 92,331 1,946 132,578 -3,179 -228,995 4,249

Live

cattle 86,610 11,439 82,640 3,900 -175,632 -12,931

Feeder

cattle 1,334 -126 7,752 -81 -2,034 105

Lean

hogs 56,176 4,823 52,783 2,012 -105,442 -7,898

Other NonReport Open

Net Chg Net Chg Interest Chg

Corn

155,515 -12,555 -10,315 6,926 2,693,387 53,588

Soybeans

49,220 -1,047 4,101 3,681 1,321,924 10,641

Soymeal

17,667 -718 37,050 5,590 497,713 13,722

Soyoil

12,933 -870 22,590 1,369 601,413 20,035

CBOT

wheat 13,243 -3,706 -10,561 2,275 557,908 -7,829

KCBT

wheat -5,928 -1,164 2,257 1,125 248,840 5,427

MGEX

wheat 1,781 -1,386 3,295 -160 94,819 178

———- ———- ———- ———- ———- ———-

Total

wheat 9,096 -6,256 -5,009 3,240 901,567 -2,224

Live

cattle 24,601 -89 -18,220 -2,319 372,822 -8,292

Feeder

cattle 2,562 567 -9,615 -465 45,962 833

Lean

hogs 7,568 39 -11,085 1,024 288,133 15,147

Source:

Reuters, CFTC and FI

Canada

Wholesale Trade Sales (M/M)) Dec: -1.3% (est -1.7%, prev 0.7%)

US

Univ. Of Michigan Sentiment Feb P: 76.2 (est 80.9; prev 79.0)

–

Current Conditions Feb P: 86.2 (est 89.0; prev 86.7)

–

Expectations Feb P: 69.8 (est 76.0; prev 74.0)

–

1-Year Inflation Feb P: 3.3% (prev 3.0%)

–

5-10 Year Inflation Feb P: 2.7% (prev 2.7%)

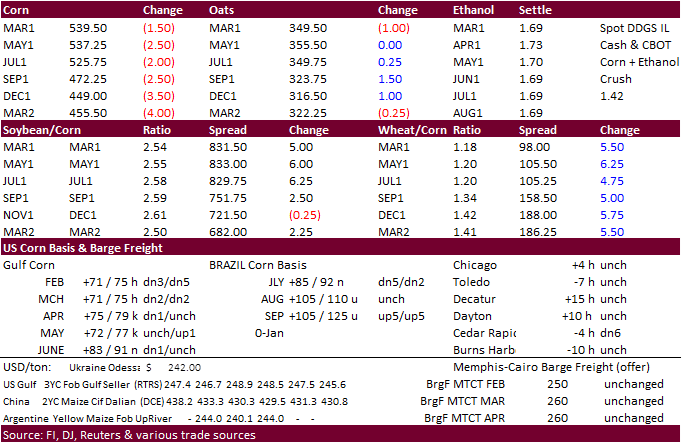

Corn.

-

Corn

futures traded mixed, closing lower, probably on soybean/corn spreading. USDA announced a combined 310,915 tons of corn sold to Central America, but since China was not involved, some traders may have been disappointed. News was light with many countries

on holiday. -

March

support over the short term is seen at $5.3650 and resistance at $5.5275.

-

Note

USDA is due out with commodity outlooks for the US 2021-22 supply and demand a week from Friday. There are some in the camp that USDA may unveil a 94 million US corn planted area. An area reported above 92.5 million could be negative for new-crop December

corn futures, based on our observations of selected estimates released in recent months.

-

USDA’s

annual Ag Outlook Forum: https://www.usda.gov/oce/ag-outlook-forum

Bloomberg

estimates below:

Corn

Export Developments

·

Under the USDA 24-hour reporting system, private exporters reported export sales of 195,338 tons of corn for delivery to Costa Rica. Of the total, 135,644 metric tons is for delivery during the

2020/2021 marketing year and 59,694 metric tons is for delivery during the 2021-22 marketing year.

·

Under the USDA 24-hour reporting system, private exporters reported export sales of 115,577 tons of corn for delivery to Guatemala during the 2020-21 marketing year.

Updated

2/10/21

March

corn is seen trading in a $5.20 and $6.00 range

May

corn is seen in a $5.15 and $6.00 range.

July

is seen in a $5.00 and $6.00 range.

December

corn is seen in a $3.75-$5.50 range.