PDF Attached

Attached

are USDA export sales estimates that indicate a weekly record for corn, and USDA NASS soybean crush & corn for ethanol use charts.

USDA

report for Super Bowl 2021 – Feature Advertising by U.S. Supermarkets During Key Seasonal Marketing Events

https://www.ams.usda.gov/reports/super-bowl-2021

WASHINGTON,

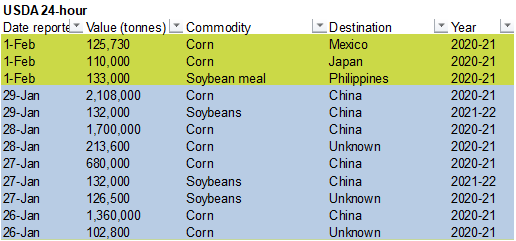

February 1, 2021–Private exporters reported to the U.S. Department of Agriculture the following activity:

–Export

sales of 125,730 metric tons of corn for delivery to Mexico during the 2020/2021 marketing year;

–Export

sales of 110,000 metric tons of corn for delivery to Japan during the 2020/2021 marketing year; and

–Export

sales of 133,000 metric tons of soybean meal for delivery to the Philippines during the 2020/2021 marketing year.

Weather

MOST

IMPORTANT WEATHER AROUND THE WORLD

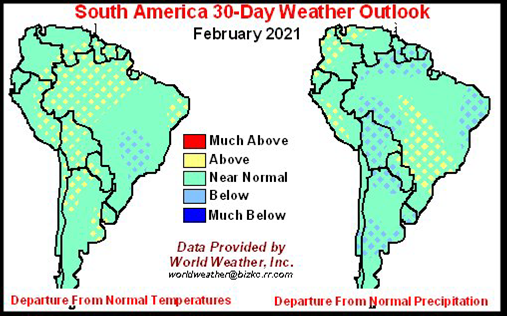

- Argentina

rainfall scattered from San Luis through Cordoba through southeastern Santiago del Estero and Santa Fe to Corrientes, Entre Rios and northeastern Buenos Aires early in the weekend and rain developed overnight from the north half of Buenos Aires northward into

Cordoba and Santa Fe once again - Rainfall

varied from 1.00 to 2.75 inches with local totals to 3.54 inches early in the weekend with another 0.05 to 0.50 inch with local totals to 1.87 inches occurring overnight - Other

areas of scattered showers occurred in the remainder of Argentina except in southeastern La Pampa and southern Buenos Aires where dry conditions prevailed - Chaco

was also dry through this morning - Temperatures

were very warm to hot in northwestern Argentina while close to normal elsewhere with highs in the 80s and lower 90s - Extreme

highs in the northwest reached the upper 90s to 102 degrees Fahrenheit - Lowest

morning temperatures were in the upper 40s and 50s in the south and in the 60s across the north - Argentina

weather will favor net drying conditions over the next ten days with a few exceptions - Totally

dry weather is not expected, but most of the precipitation that falls in key crop areas will not counter evaporation very well leading to net drying - The

only good news is that the showers that do evolve will likely slow down to decline in soil moisture - Crops

will continue to develop favorably especially in central and northeastern parts of the nation where soil conditions are favorably moist after recent rain

- Limited

rainfall in La Pampa and parts of southern Buenos Aires will keep some of those areas with moisture stress on the rise - Rain

is expected more routinely in northern Argentina for a while early this week - Net

drying will dominate the nation late this week through much of next week - Temperatures

will be seasonably mild to warm this week and warmer next week - Argentina’s

bottom line is very good after recent abundant rain in the heart of the nation. Drying in the far south will bring on some quick stress to corn, late season soybeans and other crops. Warmer temperatures and quick drying this weekend through next week will

raise the need for rain in the second week of February, but mostly in those areas that did not get much rain recent which includes southern and central La Pampa and some central and southwestern Buenos Aires locations. World Weather, Inc. believes rain will

return to Argentina during mid-February, but it is unclear how well that precipitation will be distributed. For now, the recent rain has improved crop development and production potentials in many areas and this trend could be sustained by some timely rainfall

during mid-month. - Brazil

weekend rainfall was concentrated from central and southern Paraguay into Rio Grande do Sul, southern Mato Grosso do Sul, western Parana and western Santa Catarina - Rain

totals varied from 1.00 to 2.25 inches most often; however, rainfall of 2.25 to 5.39 inches occurred in southeastern Paraguay, far southwestern Parana and Misiones, Argentina

- Some

parts of the Asuncion, Paraguay area reported 6.40 inches - Flooding

may have damaged a few crops in low-lying areas, but most of the crops have handled the wetter weather relatively well - Sporadic

showers occurred farther north from central Mato Grosso do Sul to Mato Grosso and Goias with rainfall to 0.72 inch - Rain

also developed in southern Minas Gerais and across Goias overnight with amounts to 0.75 inch and locally as great as 1.61 inches in southern Minas Gerais coffee areas - Drying

occurred in all other areas - A

highly favorable mix of rain and sunshine will occur in Brazil agricultural areas during the coming two weeks - The

moisture will be great for full season crops and for late maturing soybeans - Sufficient

drying time will occur between rain events to support soybean harvesting and Safrinha crop planting - Dryness

will be most significant in eastern Piaui and Bahia - Temperatures

will be seasonable during both forecast weeks - Brazil’s

bottom line continues favorable for corn and soybean development, although some early season corn production and a few soybean production areas suffered some loss. Most of the soybean region is expected to yield favorably, although perhaps not optimally. In

the meantime, this week’s weather and next week’s as well will be good for early soybean harvesting and for early Safrinha crop planting. Sugarcane, coffee and citrus will benefit from improved rainfall later this week as will crops in far northeastern parts

of the nation when rain finally reaches those areas later this week. - Paraguay

reported locally heavy rainfall over the past couple of days - Asuncion

reported 162 millimeters through this morning which is 6.38 inches most of which occurred since Saturday night into Sunday morning - Other

reports of rainfall in the range of 1.25 to 3.11 inches occurred across the interior southern parts of the nation with 5.39 inches occurring near the common borders of Parana and Misiones, Argentina - U.S.

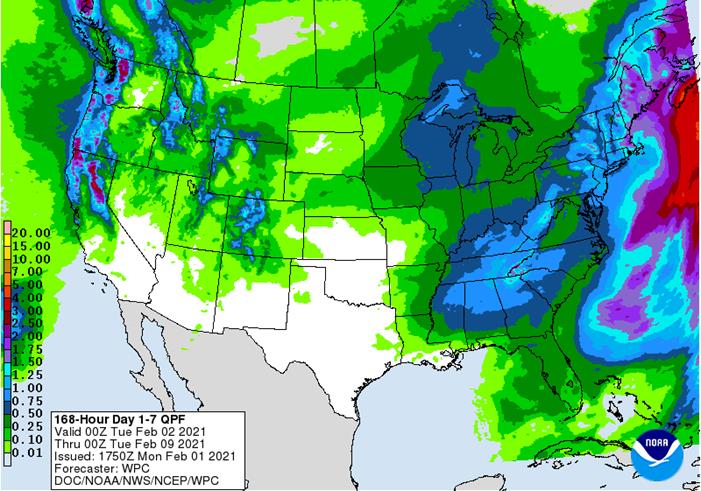

snowfall through the weekend varied from 2 to 10 inches from eastern Iowa to southern Wisconsin, northern Illinois, northern and eastern Indiana, southern Michigan and parts of Ohio

- 10-13

inches occurred near the west coast of Lake Michigan from Glendale through Racine to Kenosha, Wisconsin and southward into the greater Chicago area nearest to the lake - Snow

also fell in Pennsylvania, Virginia, in the Washington, D.C. area and areas southwest into the central Appalachian Mountains and northeast into southern New England - U.S.

rainfall during the weekend was widespread to the south of the snow areas - Amounts

ranged from 0.30 to 1.30 inches from the southeastern one-third of Kansas and extreme northeastern Oklahoma to southeastern Iowa, central and southern Illinois and areas east into southern Ohio, Kentucky and the southern Appalachian Mountains - Local

rain totals reached 1.50 inches in Missouri, Illinois, southern Ohio and from West Virginia into southwestern Pennsylvania, according to Doppler radar - Rain

also developed Sunday in the southeastern states where moisture totals varied from 0.30 to 1.24 inches - The

Delta reported less than 0.26 inch of moisture and much of the far southern and northern Plains were left dry - Snow

and rain also continued to impact the far western United States – especially in California, although the precipitation was much less than that reported last week - Huge

gains in snow water equivalencies and snowpack have occurred over the past ten days

- Big

improvements in runoff potential are occurring, but snow totals are still well below the norm for this time of year - Stormy

weather will continue through the first half of this week and then drier weather will evolve for a while.

- U.S.

weather forthcoming - Sunday’s

rain and snow event in the Midwest and middle Atlantic Coast states will diminish today except in the northeastern U.S. where snow will linger into Tuesday morning - Additional

snowfall will be greatest from northeastern West Virginia through eastern Pennsylvania and New Jersey to New England with 8-15 inches of new accumulations - A

new storm system will come across the northern Plains Wednesday and into the Midwest Thursday and Friday resulting in more rain and snow from the heart of the Midwest into the middle and northern Atlantic Coast States - Blizzard

or near-blizzard conditions are expected in the western Great Lakes region Thursday into Friday with snowfall of 3 to 8 inches and local totals to 10 inches and wind speeds of 20 to 35 mph and a few gusts to 40 - Northern

Plains’ snowfall will vary from a dusting to 3 inches with a couple of bands of greater snow in northwestern North Dakota and northeastern Montana and from northeastern Nebraska through southeastern South Dakota to central Nebraska where local totals to 6

inches will result. - Brief

waves of snow will then march across the northern and central Plains and Midwest during the weekend and next week as each successive shot of cold air moves through the region - Temperatures

will turn colder than usual late this week and next week in the northern and central Plains, Midwest, Delta and Atlantic Coast States - The

cold will retreat mostly to the northern and central Plains and upper Midwest during the latter part of next week into mid-month while the eastern states warm to a more seasonable range - Temperatures

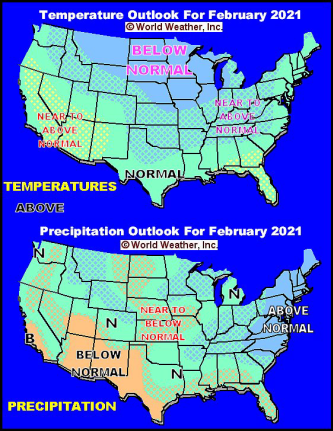

will be more seasonable elsewhere in the nation during these next two weeks - Western

U.S. stormy weather pattern is expected to diminish during mid- to late week this week through all of next week - Coastal

areas of the Pacific Northwest will continue wet during the first half of this week and then will begin to dry down thereafter - Restricted

precipitation will occur in hard red winter wheat production areas during the next two weeks, although totally dry weather is not likely - A

close watch on snow cover and extreme temperatures will be needed to ensure no risk of winterkill - West

and South Texas will not experience much rainfall for the next ten days - Cold

air will begin pooling in northern Canada early this week and will surge southward across Canada’s Prairies and into the northern U.S. Plains during the second half of the week - This

cold surge will last for about ten days with varying degrees of intensity - Some

of the cold will briefly seep through the Rocky Mountains and into the far western United States - Some

of the cold air will eventually sweep into the Midwest and Atlantic Coast states, but not this weekend and on into the week of February 8

- U.S.

and southwestern Canada wheat areas should get some snow to help protect against the late week cold surge, but a close watch on its distribution and significance is warranted since temperatures will fall below the damage threshold for unprotected winter wheat - U.S.

hard red winter wheat production areas will lose snow cover this week due to warmer temperatures and will need snow back again before the arctic outbreak begins - Some

of the needed snow should fall before there is any serious concern over crop conditions - Soil

moisture remains excessive in parts of the U.S. southeastern states and weather in the next ten days will perpetuate the wet bias in some areas - U.S.

Delta precipitation will occur often enough to keep soil moisture plentiful - Drought

in the western United States has not been seriously changed by recent precipitation, although California has seen enough moisture for improved topsoil conditions and has potential for better water supply in the spring as snow melts and runoff begins - Northern

Russia will experience bitter cold weather later this week and on into next week - Early

indications suggest no winterkill will result because of sufficient snow cover that will be present

- Southern

Russia and Ukraine will be closely monitored for snow cover if the cold reaches that far to the south - Snow

cover is expected to decrease across parts of southeastern Europe for a little while week, including Ukraine and a part of Russia’s Southern Region

- Cooling

during the weekend and next week allowing some snow cover to return prior to any bitter cold temperatures settling into these areas keeping the potential for winterkill minimal - Flood

potentials are high in parts of western Europe and the eastern Adriatic Sea nations where frequent rain of significance has been occurring over multiple weeks - Less

precipitation is expected over this coming week to help reduce some of the flood potential - France,

Germany, the U.K. and northern Spain are among the most vulnerable western nations for flooding – if a more significant storm system evolves before needed drying occurs - North

Africa dryness is mostly confined to southwestern Morocco and areas from near the Morocco/Algeria border into northwestern Algeria - These

areas will remain dry biased through Wednesday, but crops are semi-dormant which limits the need for moisture until seasonal warming begins.

- Some

rain will evolve late this week and into the weekend in all of Morocco resulting in a notable boost in soil moisture that may improve crop conditions - Northern

Tunisia and Algeria will receive limited rainfall until the middle part of next week - South

Africa will receive widespread rain during the next seven days further ensuring good production potentials for its summer crops - Northern

Cape, far western North West and Free State will experience the least amount of rain, but may experience some improved rainfall next week - Far

northern and central India may receive some welcome showers during the second half of this week and into the weekend

- Most

of India’s winter crops will reproduce over the next few weeks and timely rain is needed to induce the best yields - Rain

expected late this week will occur mostly from Punjab and Uttar Pradesh through southeastern Madhya Pradesh to West Bengal and Bangladesh and resulting rainfall will be light - The

precipitation will occur mostly in the north late this workweek and then advance to the southeast during the weekend - Very

little precipitation of significance occurred during the weekend, although one location in northern Odisha received 0.30 inch

- Queensland,

Australia’s sorghum and cotton areas need significant rain along with most of its livestock region, but precipitation will be restricted over the next week to ten days - Crop

conditions are better than they were last year at this time, but drought remains in Queensland’s central and south

- There

have been some beneficial rain events in southeastern Queensland this summer, but greater moisture is needed to induce the best possible cotton and sorghum production

- Sugarcane

areas along the upper coast are rated favorably - Rain

will evolve briefly tonight and Monday in both New South Wales and Queensland

- Another

chance for showers and thunderstorms will occur late this week and into the weekend - No

general soaking is expected, but the precipitation will be favorable eventually - New

South Wales, Australia summer crop areas have received some rain recently and a little more is expected - the

moisture will continue to supplement irrigation and support cotton and sorghum in the state, although greater rain might still be welcome - China

wheat and rapeseed are favorably rated and expected to perform well in the spring.

- There

is no threatening cold weather for the next two weeks and sufficient precipitation will fall to maintain status quo conditions - Bitter

cold is expected in the Northeast Provinces, but winter wheat is not produced significantly in that region - West

Africa rainfall will remain mostly confined to coastal areas while temperatures in the interior coffee, cocoa, sugarcane, rice and cotton areas are in a seasonably warm range for the next ten days - Some

rain will fall in a few coastal areas during the coming week, but most of the precipitation will stay far from coffee and cocoa production areas - There

is potential for a few of the showers to reach northward into coffee and cocoa production areas this weekend and early next week, but resulting rainfall should be light - East-central

Africa rainfall will continue limited in Ethiopia as it should be at this time of year while frequent showers and thunderstorms impact Tanzania. - Kenya

and Uganda will receive some infrequent rainfall over the next ten days - Southern

Oscillation Index weakened during the weekend and this trend will continue this week - Today’s

SOI was +15.40 today and the index will continue slowly declining this week - Southeast

Asia weather is not likely to change much over the coming week - Mainland

areas have been and will continue to be mostly dry - Philippines

rainfall will be erratic and mostly light, but it may increase somewhat during the next ten days - Indonesia

and Malaysia rainfall has been erratic, but sufficient in maintaining a very good crop development environment - No

excessive rain occurred recently, and little is anticipated for a while - Some

heavy rain fell in the Lesser Sunda Islands in southern Indonesia during the weekend - Southeastern

Mexico will get most of the rain periodically during the next ten days - The

precipitation will be erratic and mostly light, but still welcome wherever it occurs - Many

areas in Mexico are still dealing with long term drought - Central

America precipitation will continue greatest along the Caribbean Coast while the Pacific Coast is relatively dry - Canada

Prairies will be cooler than usual during the next two weeks and periodic precipitation is expected - The

greatest cool off is expected in the second half of this week through early next week when bitter cold conditions are expected

- Most

of the precipitation will be light - Southeast

Canada will experience near average temperatures this week with some brief periods of precipitation expected

Source:

World Weather Inc. and FI

Source:

World Weather Inc. and FI

Source:

World Weather Inc. and FI

Monday,

Feb 1:

- USDA

weekly corn, soybean, wheat export inspections, 11am - EU

weekly grain, oilseed import and export data - Malaysia

Jan 1-31 palm oil export data from AmSpec (tentative) - China

starts trading peanut futures on Zhengzhou Commodity Exchange - U.S.

DDGS production, soybean crush, 3pm - Australia

Commodity Index - Ivory

Coast cocoa arrivals - HOLIDAY:

Malaysia

Tuesday,

Feb 2:

- U.S.

Purdue Agriculture Sentiment - New

Zealand global dairy trade auction - U.S.

corn for ethanol, 3pm

Wednesday,

Feb 3:

- EIA

weekly U.S. ethanol inventories, production, 10:30am - New

Zealand Commodity Price

Thursday,

Feb 4:

- FAO

World Food Price Index; cereals supply/demand brief - USDA

weekly crop net-export sales for corn, soybeans, wheat, cotton, pork, beef, 8:30am - Port

of Rouen data on French grain exports

Friday,

Feb 5:

- ICE

Futures Europe weekly commitments of traders report, 1:30pm (6:30pm London) - CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm - China’s

CNGOIC to publish soybean and corn reports - Statcan

reports on wheat, soy, durum, canola and barley stockpiles in Canada

Source:

Bloomberg and FI

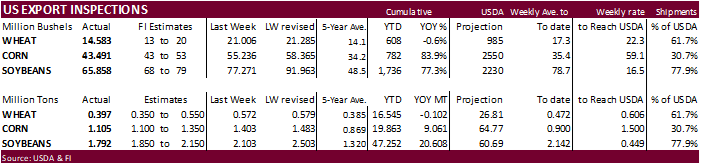

USDA

inspections versus Reuters trade range

Wheat

396,873 versus 350000-550000 range

Corn

1,104,721 versus 1000000-1350000 range

Soybeans

1,792,367 versus 1100000-2150000 range

US

University Of Michigan Sentiment Jan F: 79.0 (est 79.4; prev 79.2)

–

Current Conditions Jan F: 86.7 (est 87.7; prev 87.7)

–

Expectations Jan F: 74.0 (est 74.1; prev 73.8)

–

1 Year Inflation Expectations Jan F: 3.0% (est 2.9%; prev 3.0%)

–

5-10 Year Inflation Expectations Jan F: 2.7% (prev 2.7%)

US

Pending Home Sales (M/M) Dec: -0.3% (est -0.5%; prev -2.5%)

–

Pending Home Sales NSA (Y/Y) Dec: 22.8% (est 20.3%; prev 16.1%)

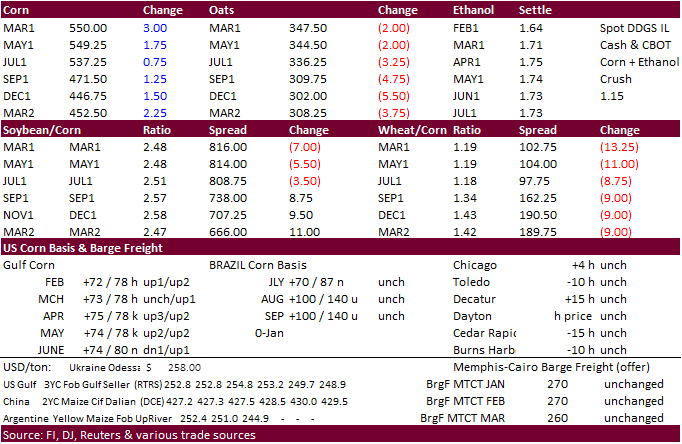

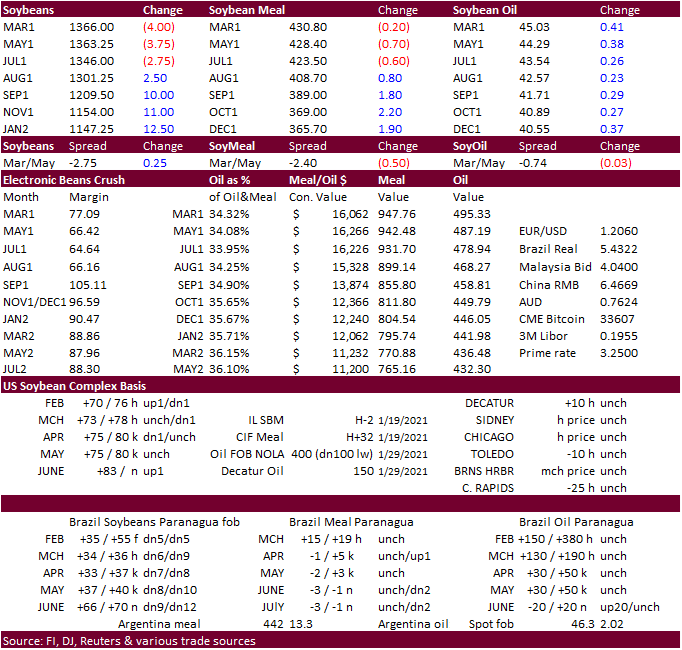

Corn.

-

Volatility

in corn futures kept traders on edge. March corn saw a low of 5.4925, making it a 6.50 cents range for the day.

$5.5575,

made in the overnight session, is the new March contract high. $5.60 is seen as the next resistance level.

-

Additional

USDA 24-hour sales announcements were posted, but they did note include China.

-

We

raised our US corn exports by 100 to 2.700 billion bushels, lowering the carryout by 100 to 1.406 million versus 1.552 billion for USDA. We may reduce US corn for feed for Q3 and Q4 for 2021-22.

-

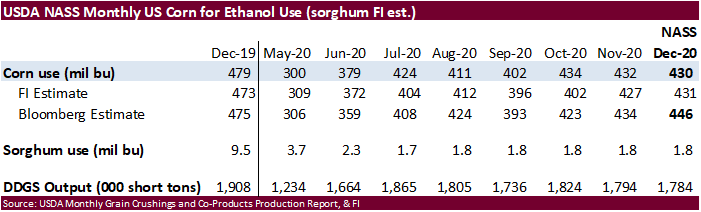

USDA

NASS reported Dec corn for ethanol use at 430 million bushels, near our expectations, but well down from a Bloomberg trade average of 446 million. It was slightly below November and well below 479 million in December 2019.

-

US

crop insurance pricing starts today, lasting through the end of the month.

-

We

look for a record weekly USDA corn net export figure this Thursday. Weekly USDA net export sales have averaged little over 1.5 million tons over the previous three weeks. Of the three week combined USDA corn export sales of 4.726 million tons, China accounted

for 769,000 tons (16 percent of the total reported), or on average 256,000 ton per week. With last week’s 24 hour data, we estimate USDA’s weekly export sales report will account for up to 6.16 million tons that was reported last week under the 24-hour reporting

system. This considers Friday’s announcement. China accounted for 5.85 million tons of that. If we assume traditional buyers committed up at least 1 million tons of corn last week, we look for a record 7.1 to 7.8 million tons to be reported. The previous

record week* was 4.726 million tons for the week ending January 9, 1991, that included the record 3.720 million ton 24-hour US corn sale reported 1/9/91 for USSR.

*Omits

weeks reported with crop-year rollover and government root boots after fiscal shutdowns.

-

The

European Union granted imports licenses for 188,000 tons of corn imports, bringing cumulative 2020-21 imports to 9.661 MMT, 27 percent below same period year ago

-

StoneX

sees the Brazil corn crop at 110.2 million tons versus 109.34 million tons previously. -

Conab

has been much lower than selected trade estimates for the Brazilian corn crop. Recent rains should have been beneficial to see an increase in the yield. We think Conab will raise their Brazilian corn crop estimate later this month to 103.03 million tons

from 102.31 million tons in January. -

Soybean

and Corn Advisory: -

2020/21

Brazil Corn Estimate Unchanged at 105.0 Million Tons -

2020/21

Argentina Corn Estimate Unchanged at 44.5 Million Tons

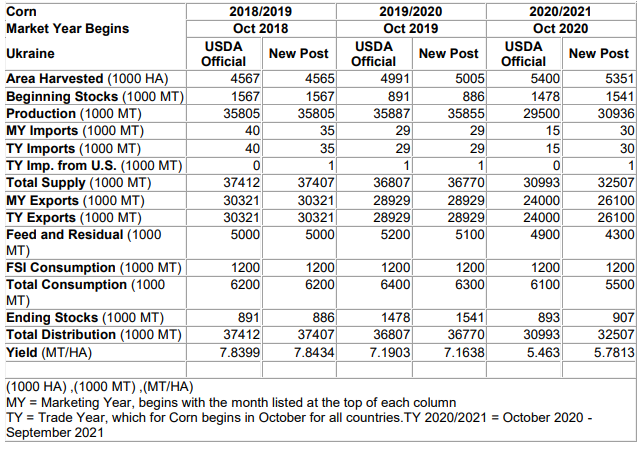

Ukraine

grain and feed update – USDA Attaché

Corn

Export Developments

·

WASHINGTON, January 29, 2021–Private exporters reported to the U.S. Department of Agriculture the follow activity:

–Export

sales of 125,730 metric tons of corn for delivery to Mexico during the 2020/2021 marketing year

–Export

sales of 110,000 metric tons of corn for delivery to Japan during the 2020/2021 marketing year;

Updated

1/29/21

March

corn is seen trading in a $5.15 and $6.00 range.

May

corn is seen in a $5.00 and $6.00 range.

July

is seen in a $4.90 and $5.75 range.

December

is seen in a $3.75-$5.50 range.

-

Today

the soybean complex saw a choppy trade. Wide swings in soybean oil and soybeans left questions on the table. We saw 24-hour sales reported this morning for soybean meal that could limit downside risk at the open. Then soybean oil rallied on bottom picking

and interpretation over India’s changes to its CPO import duty percent and “cess” rule. Rest of the day prices in the complex remained choppy. We are hearing corn and soybeans are getting harder to find across the US Delta and there is rising speculation

rationing will hit the domestic use categories before exports. For soybeans, we look for US export shipments to gradually decline when Brazil ramps up their export program.

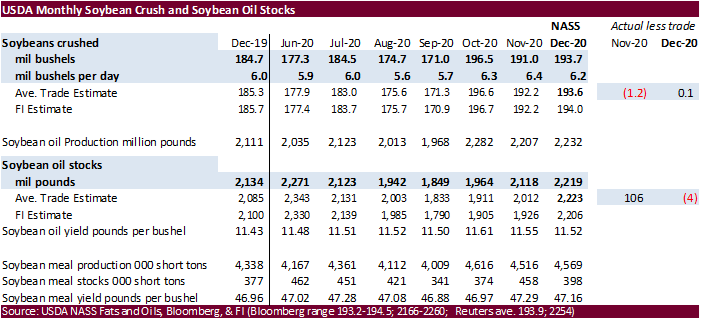

-

After

the close NASS reported the December crush near expectations at 193.7 million bushels and stocks also near expectations at 2.219 billion pounds. See out table below.

-

ICE

canola futures spiked near the end of the session. Reuters noted Canada is running short of canola six months before the next harvest, driven by strong export demand. Canadian farmers may expand plantings by 6% this spring.

-

Malaysian

was on holiday for Federal Territory Day. AmSpec reported a 36 percent decline in Malaysian palm oil exports for the month of January from December at 1.090 million tons. ITS reported a 37 percent decline in January palm shipments from December. SGS reported

a 32 percent decline at 1.104 MMT. -

India

lowered their import duty on soybean oil and sunflower oil to 15% from 35%, and CPO palm oil to 15 percent from 27.5 percent. But they imposed a 17.5% “cess” – a separate tax – on the imports. The cess would provide resources for “an immediate need to improve

agricultural infrastructure. Some think imports of CPO could slow into India if they use cess. Effective import duty on soy and sunflower oil will remain unchanged at 38.5%. -

Note

the Brazilian trucker strike started today, amplifying what is already a slow start to the export season. Brazil’s 2020-21 soybean crop harvest stood at 1.9% through Jan. 28, slowest pace in ten years-AgRural. 2.5 million tons were collected versus 11.7

million tons at the same time last year. -

Brazil

reported Jan soybean exports were 49,498 tons in January versus 1.4 million tons a year earlier and corn exports were 2.55 million tons versus 2.1 million tons year earlier.

-

StoneX

sees the Brazil soybean crop at 132.77 million tons versus 132.6 million tons previously.

-

We

think Conab will raise their Brazilian crop estimate later this month to 134.5 million tons from 133.7 million tons in January.

-

Soybean

and Corn Advisory: -

2020/21

Brazil Soybean Estimate Increased 1.0 mt to 130 Million -

2020/21

Argentina Soybean Estimate Unchanged at 46.0 Million Tons -

Argentina

will see good weather over the next week. Northeastern Brazil will continue to see dry conditions.

-

Argentina’s

farm exports rose 32.63% year-on-year in January-CIARA-CEC chamber of crushers and exporters. -

Strategie

Grains raised their forecast for rapeseed imports into the European Union and Britain by 800,000 tons to a record 6.7 million tons. EU rapeseed stocks at the end of the 2020/21 season on June 30 were expected to be very low.

-

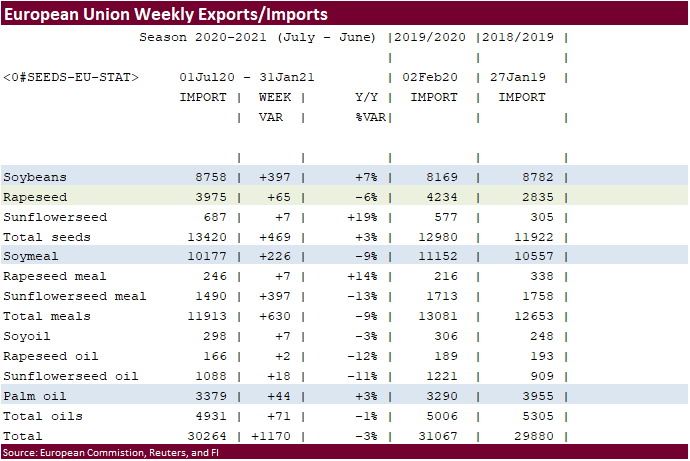

The

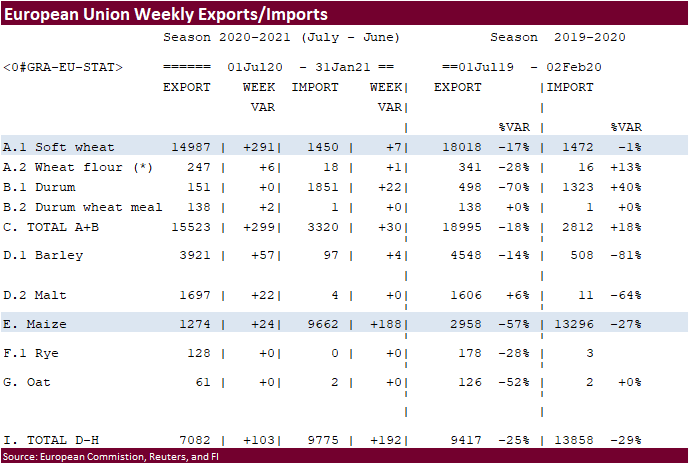

European Union reported soybean import licenses since July 1 at 8.758 million tons, above 8.169 million tons a year ago. European Union soybean meal import licenses are running at 10.177 million tons so far for 2020-21, below 10.557 million tons a year ago.

EU palm oil import licenses are running at 3.379 million tons for 2020-21, above 3.290 million tons a year ago, or up 3 percent. -

European

Union rapeseed import licenses since July 1 were 3.975 million tons, down 6 percent from 4.234 million tons from the same period a year ago.

Oilseeds

Export Developments

·

South Korea’s KFA bought 60,000 tons of soybean meal at $503.95 a ton c&f for shipment from South America between June 1 and July 1. On Friday

South

Korea’s MFG bought about 60,000 tons of soybean meal at $501.95/ton c&f for arrival around Aug.

·

Egypt’s GASC seeks at least 30k soybean oil and 10k sunflower oil on Feb 2 for March 10-30 arrival.

·

WASHINGTON, January 29, 2021–Private exporters reported to the U.S. Department of Agriculture the follow activity:

–Export

sales of 133,000 metric tons of soybean meal for delivery to the Philippines during the 2020/2021 marketing year.

Updated

1/26/21

March

soybeans are seen in a $13.25 and $14.75 range

March

soymeal is seen in a $410 and $480 range

March

soybean oil is seen in a 42.50 and 45.00 cent range

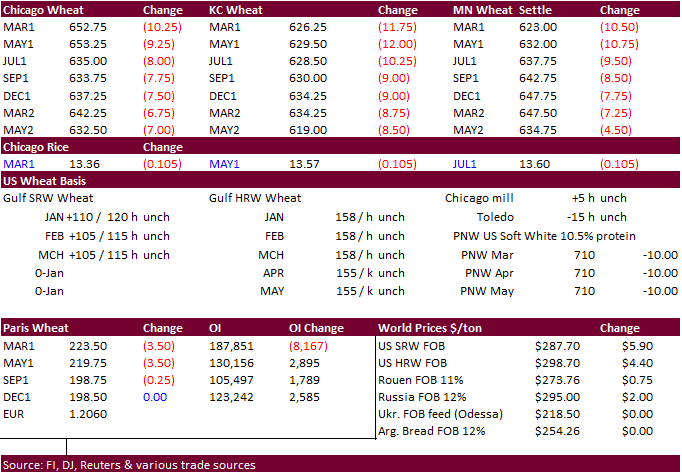

- US

wheat ended more than ten cents lower led by the front month contracts. A higher USD, up 40 points by 2 pm CT, was a big influence, followed by lack of import tenders announced over the weekend. However, after the close Egypt announced an import tender for

wheat for March 15-30 shipment. We will know soon if exporters are comfortable in making offers know that traders know details of Russia’s export duty plan. Recall Egypt passed on wheat January 12.

- China

sold 2.187 million tons of wheat out of auction making January sales totaled 12.253 million tons versus 3.024 million tons during December (nearly 30 million since June). The 2,187,297 tons of wheat represented 54.34% of total offered. It was done at an

average price at 2,373 yuan ($367.46) per ton. - Russia

exported 32.422 million tons of grain from July 1, 2020, to January 25, 2021, which was 20.4% more than the 26.92 million tons the previous year – Center for Agro-analytics. During the period, wheat exports totaled 27.3 million tons, a rise of 20.8%; barley

was 3.6 million tons, an increase of 41%; corn was 1.2 million tons, a decline of 20.7%; and other grain crops were 300,000 million tons, growth of 47.6%. (Reuters) - (Reuters)

– Russian wheat export prices fell for the second consecutive week. 12.5% protein Black Sea for Feb. 15 and Feb. 28 was at $293 a ton free on board (FOB) at the end of last week, down $3 from the previous week – IKAR.

- On

Saturday there was a news article talking about Russia could impose a formula based wheat export tax from June 1. We thought this might be in the works as they tame domestic food inflation. What this could lead to is higher North America wheat exports during

the summer months, if global prices continue to rise into new-crop. Previously Russia set a 25 euros ($30) per ton tax for Feb. 15 to 28, rising to 50 euros per ton from March 1 to June 30.

- Ukrainian

Black Sea ports have restricted grain loading operations due to poor weather.

- Ukraine

used 74.3% of its 17.5 million ton wheat exports quota for the 2020-21 season, with wheat exports amounting to 13 million tons as of Feb. 1, down almost 2.9 million tons from the same date a season ago. - EU

March milling wheat was down 3.5 at 223.50 euros. - Parts

of the river Rhine in south Germany were closed to shipping on Monday from high water levels.

- The

European Union granted export licenses for 291,000 tons of soft wheat exports, bringing cumulative 2020-21 soft wheat export commitments to 14.987 MMT, well down from 18.018 million tons committed at this time last year, a 17 percent decrease. Imports are

down slightly from year ago at 1.472 million tons.

- Egypt

seeks wheat for March 15-30 shipment. We will know soon if exporters are comfortable in making offers know that traders know details of Russia’s export duty plan. Recall Egypt passed on wheat January 12.

- Jordan

is in for another 120k wheat on Feb 3 and 120k barley on Feb 2.

·

CME Raises COMEX Silver Futures Margins By 18%

·

Iraq seeks 30,000 tons of rice on Feb 3, valid until Feb 10, optional origin.

·

Syria is in for 25,000 tons of rice on February 9.

Updated

1/26/21

March

Chicago wheat is seen in a $6.35‐$7.15 range

March

KC wheat is seen in a $6.25‐$6.70 range (up 10 & 15)

March

MN wheat is seen in a $6.00‐$6.55 range

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International

One Lincoln Center

18 W 140 Butterfield Rd.

Oakbrook Terrace, Il. 60181

W: 312.604.1366

ICE IM:

treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered

only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making

your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors

should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or

sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy

of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.