PDF Attached

Grains and the soybean complex saw a two-sided trade today. After rallying yesterday, some profit taking in meal and corn occurred. Soybean oil rallied on product spreading and higher WTI crude oil. US wheat was higher led by fund buying for Chicago. Macros will be something to monitor this week. Traders are looking for a 25-point interest rate hike by the US Fed on Wednesday.

MOST IMPORTANT WEATHER FOR THE COMING WEEK

- Argentina’s first half of February outlook calls for below average precipitation in much of the nation with temperatures near to above normal

- Today’s soil moisture is rated favorably from northern La Pampa northward through Cordoba to Santiago del Estero while marginally adequate to short to the east

- The driest areas are in Entre Rio and areas north to Chaco where significant rain is needed now and over the next two weeks as well

- Argentina’s outlook for the second half of February will begin drier biased and may improve as the last week of the month arrives

- Brazil rainfall is expected to continue drier biased in the south while rain falls routinely across center west and center south crop areas through the next two weeks

- Sufficient rain and soil moisture will be present to support long term crops in Brazil

- Short term wet conditions, though, will present an ongoing challenge to early soybean and early corn producers as field conditions remain wetter biased keeping harvest progress slow

- Drying is needed for a little while to accelerate crop maturation and support soybean harvesting and Safrinha crop planting

- India winter crops need generalized rainfall in February to support reproduction

- Rain earlier this week in northern parts of the nation was good for wheat and other winter crops, but more is needed

- Central, western and far eastern parts of the nation need more moisture

- Eastern Australia rainfall will continue erratic over the next couple of weeks leaving some concern over unirrigated summer crop conditions in western Queensland where the precipitation will be lightest and least frequent

- Net drying is expected after today for several days

- The next best opportunity for rain will evolve next week

- Recent rain in eastern Australia was good for summer crop development especially in unirrigated production areas

- Rain Monday was greatest from central Queensland into central and northeastern New South Wales

- Extreme amounts reached up to 1.85 inches in south-central Queensland benefiting a few crops

- Other rain totals of 0.50 to 2.32 inches occurred in the Darling Downs region in northeastern New South Wales and southeastern Queensland

- Rain in most other areas varied up to 0.68 inch

- North Africa dryness is still a concern for interior Tunisia and southwestern Morocco where timely rain will be necessary this late winter and spring to support the best possible production potential

- Net drying occurred Monday after rain fell in northern Algeria during the weekend

- Not much precipitation is expected over the next week to ten days

- Western Europe will be drier biased for the next week to ten days

- Eastern Europe precipitation will occur periodically and erratically with some areas getting far more moisture than others

- Europe and Asia crop areas are not at risk of any crop damaging cold in the next two weeks

- Eastern China was dry Monday and the earliest that precipitation of significance will fall in rapeseed areas of the Yangtze River Basin will be late this week with precipitation expected most frequently during the weekend and through most of next week

- Some of this rain will reach southward to the southern coastal provinces

- Precipitation elsewhere in eastern China will be mostly sporadic and light having little impact on soil moisture or dormant winter crop conditions

- South Africa weather will include increasing frequency of rain and sufficient moisture to support summer crops as they move through the more sensitive reproductive stages of development in the next few weeks.

- Production potentials look very good

- U.S. hard red winter wheat production areas are not likely to see much significant moisture in the next two weeks, but crops are dormant and unlikely to change much

- West Texas will get a mix of precipitation types tonight and Wednesday ending Thursday

- Moisture totals will be light, but the moisture will be welcome for use in the spring

- Some follow up precipitation may occur for a little while next week

- U.S. Delta and southeastern states will be wet biased for much of the next two weeks

- Some areas are already a little too wet

- Freezing rain is expected the northern Delta and a part of the lower Tennessee River Basin over the next couple of days

- U.S. Midwest weather will include a wintry mix of precipitation types over the next couple of weeks, but moisture totals are expected to be lighter than usual

- U.S. Northern Plains and upper Midwest will receive lighter than usual precipitation for a while over the next ten days and temperatures will trend warmer after being quite cool today and again Thursday into Friday morning of this week

- U.S. Pacific Northwest is not likely to see much precipitation east of the Cascade Mountains for a while and temperatures will trend warmer

- Some rain and snow will fall this weekend and periodically next week

- Temperatures will be cooler than usual in the central United States the remainder of this week and then slowly warm up from west to east across the region this weekend into next week

- California will receive some rain and mountain snow late this week and a couple of times next week

- Middle East weather is expected to gradually turn a little wetter during the coming week to ten days and the precipitation will help improve soil moisture for future wheat development and eventual cotton planting later in the year

- Turkey will be one of the wetter nations

- West-central Africa will receive some coastal showers in the coming week with some of the precipitation expected to drift northward into coffee, cocoa and sugarcane production areas

- Any rain that reaches into crop areas will be sporadic and light for a while

- Seasonal rains usually develop in February

- Southeast Asia rainfall will be most significant in Indonesia and Malaysia as well as eastern portions of central and southern Philippines over the next ten days

- The moisture will be good for ongoing crop development, although a few areas may become a little too wet

- Central Sumatra may be one of the drier areas

- East-central Africa rainfall will remain most significant in Tanzania and southern Uganda while more limited in areas north into Ethiopia which is not unusual for this time of year

- Today’s Southern Oscillation Index was +10.59 today and the index is expected to move erratically lower over the next week

Source: World Weather and FI

Bloomberg Ag calendar

Tuesday, Jan. 31:

- Malaysia’s January palm oil export data

- EU weekly grain, oilseed import and export data

- US cattle inventory, 3pm

- US agricultural prices paid, received, 3pm

Wednesday, Feb. 1:

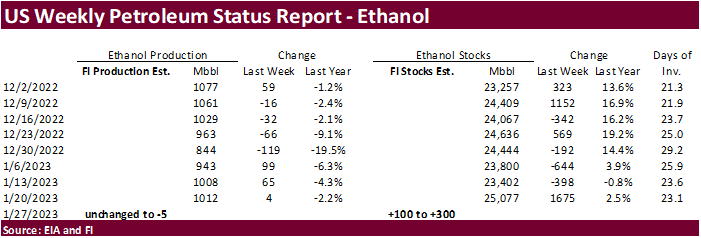

- EIA weekly US ethanol inventories, production, 10:30am

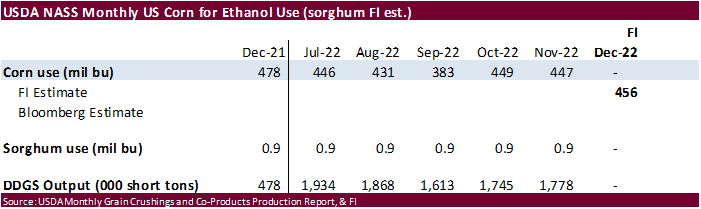

- USDA soybean crush, DDGS production, corn for ethanol, 3pm

- HOLIDAY: Malaysia

Thursday, Feb. 2:

- USDA weekly net-export sales for corn, soybeans, wheat, cotton, pork and beef, 8:30am

- Port of Rouen data on French grain exports

Friday, Feb. 3:

- FAO World Food Price Index

- FAO Cereal Supply and Demand Brief

- ICE Futures Europe weekly commitments of traders report

- CFTC commitments of traders weekly report on positions for various US futures and options

Source: Bloomberg and FI

Due out Feb 7 @ 7:30 am CT

Macros

OPEC: January Oil Output Falls By 50,000 BPD From December To 28.87 Million BPD, Led By Iraq – Reuters Survey

Bound Members Comply With 172% Of Pledged Cuts In January (Vs. 161% In December)

Bound Members Undershoot Jan Output Target By 920,000 Bpd (Vs. 780,000 Bpd Shortfall In Dec)

US Employment Cost Index Q4: 1.0% (exp 1.1%; prev 1.2%)

Canadian GDP (M/M) Nov: 0.1% (exp 0.1%; prev 0.1%)

Canadian GDP (Y/Y) Nov: 2.8% (exp 2.7%; 3.1%)

EIA: US Monthly Crude Oil Output Fell To 12.39M Bpd In November

US MNI Chicago PMI Jan: 44.3 (est 45.0; prev 45.1)

104 Counterparties Take $2.062 Tln At Fed Reverse Repo Op (Prev $2.049 Tln, 106 Bids)

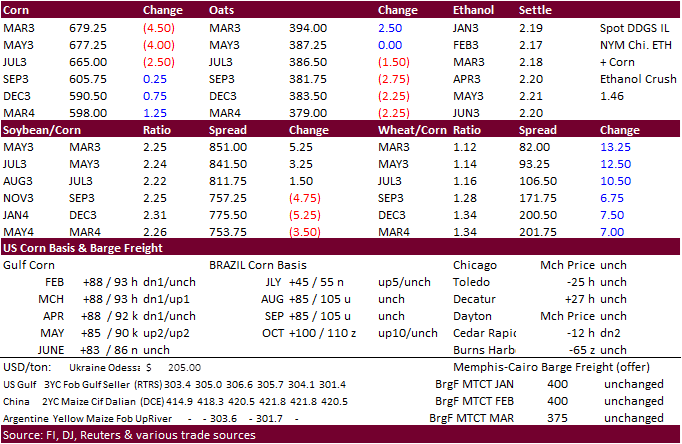

· CBOT corn traded two-sided, ending lower for the front three contracts and higher for the back months. Futures were lower earlier from weakness in US energy markets and widespread commodity selling. Many outside markets recovered by mid-morning, which spilled over into corn, but prices again sold off early afternoon. Brazil’s second corn crop plantings are underway but off to a slow start, but many still see a record crop this year.

· China saw some positive economic data on Tuesday. PMI increased to 54.0 in January from 39.4 in December and the manufacturing PMI improved to 54.4 from 41.6 in December, signaling growth.

· Anec sees Brazil corn exports reaching 4.991 million tons during January, down from 5.200 previous forecast.

· (Reuters) – China’s sow herd increased by 0.6% in December from November to 43.9 million sows, data published by the Ministry of Agriculture and Rural Affairs showed on Tuesday. The herd was also 1.4% larger than a year ago, the data showed. China’s pig herd increased by 1.9% in December from the month before to 452.6 million pigs, according to the data, and was 0.7% larger than the previous year.

· Bolivia reported two outbreaks of bird flu, one involving 35,000 birds and other 202 backyard birds.

· Romania reported a bird flu outbreak, H5N1, on a farm in the center of the country. 42,154 birds were infected.

· Some companies are exploring ethanol that could be used as SAF. One group called Blue Blade, a JV, was set up by Green Plains, Tallgrass and United Airlines. They look to build out a test pilot by 2024, then a larger plant by 2028. The SAF might be able to fly more than 50,000 flights.

· MARATHON PETROLEUM- MARTINEZ RENEWABLE FUELS FACILITY ON TRACK TO REACH PHASE I PRODUCTION CAPACITY OF 260 MLN GALLONS PER YR OF RENEWABLE FUELS BY Q1 2023 END – Reuters News

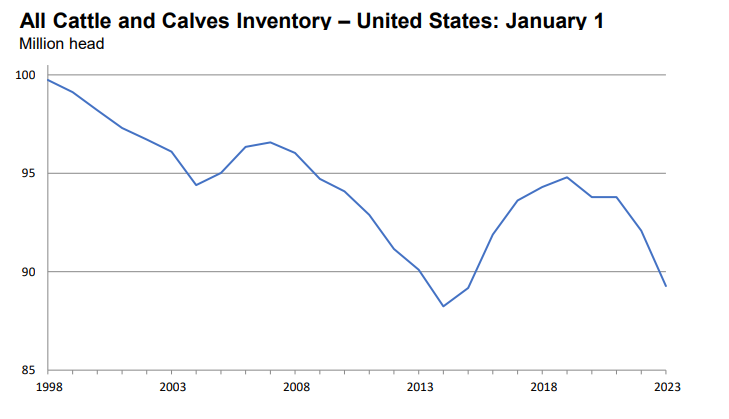

· USDA reported January cattle inventory down 3 percent from year ago to 89.3 million head. The US beef cow herd in January was lowest level since 1962. We think this is slightly bearish for corn futures. https://release.nass.usda.gov/reports/catl0123.pdf

Export developments.

· Egypt seeks yellow corn on Feb 1 for Feb 20-Mar 10 shipment.

Updated 01/31/23

March corn $6.60-$7.00 range. May $6.25-$7.00

· Soybeans and products were lower before a two-sided trade set in. Soybeans were mixed, soybean meal lower and soybean oil higher. Losses were limited for nearby soybeans from the slow start to Brazil’s soybean harvest. 5 percent had been collected as of last Thursday, half the pace at this time last year. Soybean meal is seeing some light technical correction after prices traded near an 8-year high yesterday. Argentina crushers are still having problems with securing soybeans, and Oil World looks for February and March crush to fall below expectations. Argentina soybean meal cash increased 7 percent during January to around $580/ton.

· Argentina’s AgMin reported 2021-22 soybean sales were 80.8% of the 44 million ton crop last week, slightly below 83% from same time year ago. 56,200 tons were sold during the Jan. 19 and 25 period. 77.4% of the corn crop had been sold out of 59 million tons, 79.4% year ago.

· US soybean meal stocks are tight. Good export demand and slowing crush rates for some plants that are seeing cold temperatures this week underpinned values in the truck and rail markets.

· Egypt bought 35,000 tons of vegetable oils.

· Argentina will see limited precipitation over the next two weeks. Recent rains were welcome but not enough rain occurred to end the drought.

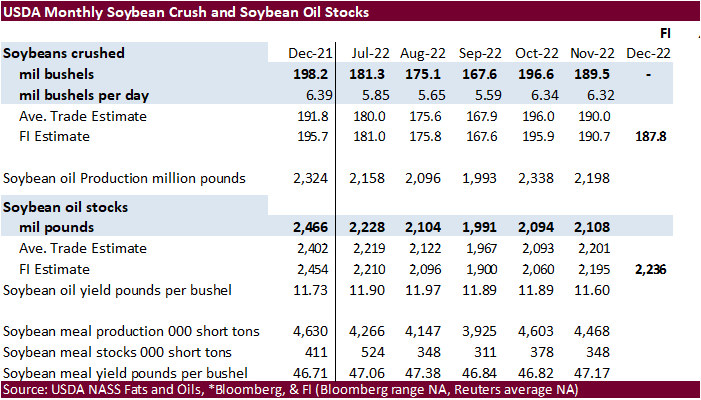

· A Reuters poll looks for the NASS crush to come in at 188.0 million bushels, down from 189.4 million bushels in November, and well below the December 2021 crush of 198.2 million bushels. U.S. soyoil stocks as of Dec. 31 were estimated at 2.249 billion lbs., up from 2.108 billion at the end of November and the highest since end of June, and below stocks totaling 2.466 billion lbs. at the end of December 2021.

· Anec sees Brazil soybean exports reaching 1.222 million tons during January, down from 1.356 previous forecast. Soybean meal is seen at 1.437 million versus 1.521 previous.

· Indonesia looks to start its B35 mandate on Feb 1.

· AmSpec reported January Malaysian palm oil exports at 1.066 million tons, down from 1.457 million in December, a 26.8 percent decrease. ITS reported a 27 percent decline to 1.134 million tons. SGS reported 1.113 million tons, down 26.4 percent.

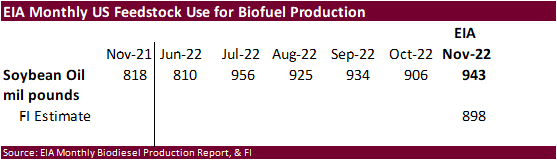

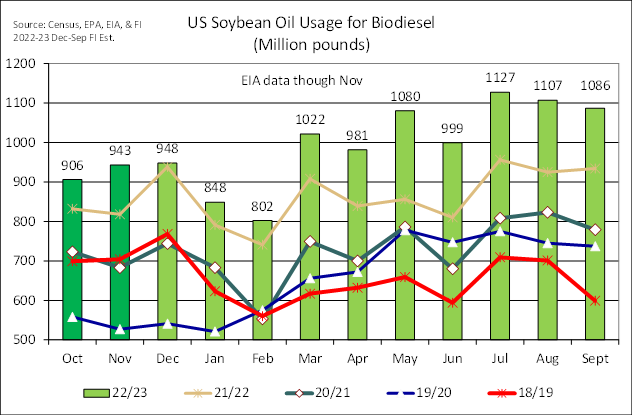

November SBO use for biofuel beat expectations

We are using 11.850 billion pounds for SBO for biofuel use, above USDA’s 11.600 billion estimate.

Reuters estimates above…

· Egypt bought 35,000 tons of vegetable oils for Feb 25-Mar 3 shipment, 19,000 tons of soybean oil ($1,330) in the international market, 6,000 tons of soybean oil ($1,499.50) in the local market and 10,000 tons of sunflower oil ($1,236.40) in the international market.

· The CCC seeks 3,770 tons of vegetable oils on February 1 for last half March shipment.

· The CCC seeks a total of 100,320 tons of bulk hi-pro soybean meal for shipment to Ghana, Ivory Coast and Senegal. One half will be shipped Mar 21-31, with the balance for Apr 1-10 shipment. All offers are due by Feb 2 at 2 PM CT.

Updated 01/31/23

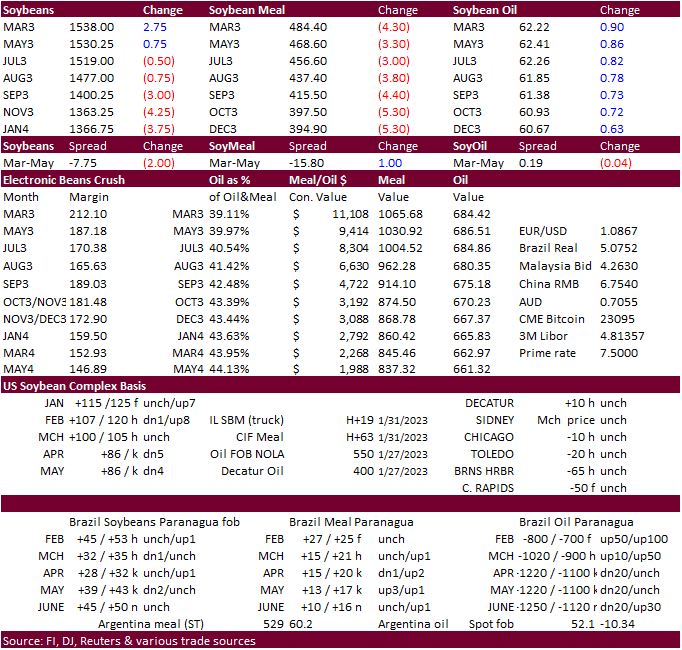

Soybeans – March $15.00-$15.80, May $14.75-$16.00

Soybean meal – March $450-$520, May $425-$550

Soybean oil – March 60.00-67.00, May 58-70

· Chicago wheat opened lower on widespread commodity selling but rebounded to close higher on fund buying. KC was mostly higher, and MN closed mixed despite Algeria’s durum wheat import tender where some of it could originate from Canada.

· Colorado winter wheat condition declined, with 38 percent of the crop rated good to excellent, compared to 50 percent good to excellent from the previous report, and 20 percent good to excellent last year. As of January 30, 2023, snowpack in Colorado was 133 percent measured as percent of median snowfall. (USDA) Kansas winter wheat condition rated 20% very poor, 27% poor, 32% fair, 19% good, 2% excellent. Nebraska wheat condition rated 14% very poor, 26% poor, 38% fair, 20% good, and 2% excellent.

· US storms this week are seen replenishing soil moisture levels bias the southern Great Plains and Midwest soft wheat area. Not all winter wheat areas will see rain over the next week.

· Paris March wheat was 1.25 euros higher at 288.75 per ton.

· Last week China sold 140,066 tons of wheat from reserves at 2,961 yuan per ton.

Export Developments.

· Algeria started buying durum wheat today, open until Wed, for three periods between Feb. 16-28, March 1-15 and March 16-31. Prices were thought to be $448 to $459 percent ton, depending on ship size. 250,000 to 300,000 tons was cited and traders think some of the durum could originate from Canada.

· Egypt seeks wheat on Feb 2 for late Feb through March 20 shipment. They seek the wheat within the framework of the Food Security and Resilience Support Program funded by the World Bank under Loan No. EG -9399 with at sight financing. The tender is for a quantity of 30,000, 40,000, 50,000, 55,000 or 60,000 tons, +/- 5% should the seller choose, from the last crop for supply C&F (cost and freight). (Reuters)

· Jordan bought 60,000 tons of wheat for LH June shipment at $336.50 c&f.

· Jordan seeks 120,000 tons of feed barley on Feb 1 for May and June shipment.

Rice/Other

· (Reuters) – Thailand exported 7.69 million tons of rice in 2022, up 22.1% from a year earlier, the commerce ministry said on Tuesday. The exports exceeded a target of 7.5 million tons with top markets being Iraq, South Africa, China and the United States, it said in a statement.

· (Reuters) The state purchasing agency in Mauritius has issued an international tender to buy 6,000 tons of long grain white rice sourced from optional origins, European traders said on Tuesday. The rice was sought for delivery between March 15 and June 15. The deadline for submission of price offers in the tender is Feb. 10.

Updated 01/31/23

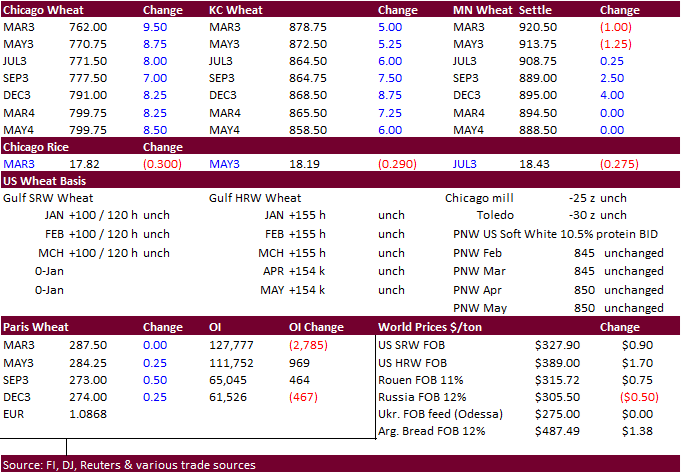

Chicago – March $7.25 to $8.00, May $7.00-$8.25

KC – March $8.40-$9.00, $7.50-$9.25

MN – March $8.90 to $9.75, $8.00-$10.00

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International

One Lincoln Center

18W140 Butterfield Rd.

Suite 1450

Oakbrook Terrace, Il. 60181

Work: 312.604.1366

ICE IM: treilly1

Skype IM: fi.treilly

DISCLAIMER:

The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy of such information or opinions. This communication may contain links to third party websites which are not under the control of FI and FI is not responsible for their content.

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors should obtain advice based on their unique situation before making any investment decision. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.

#non-promo