PDF Attached

CFTC

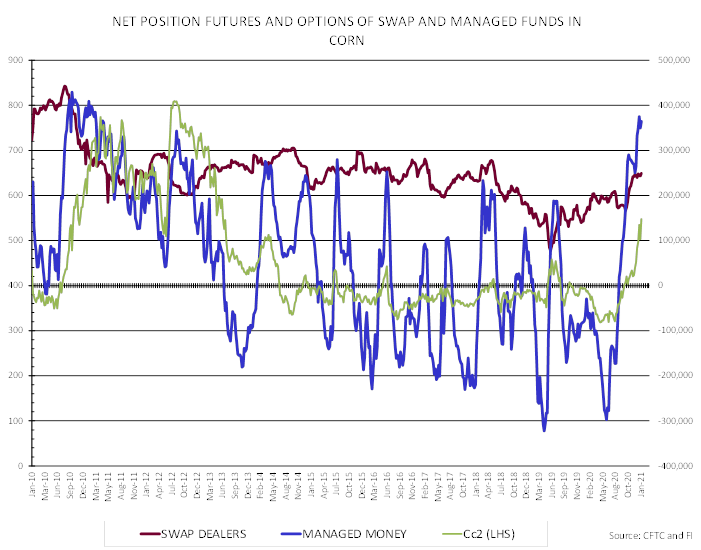

showed a record long position for CBOT traditional funds futures only corn of 547,677 contracts. Traditional funds futures and options combined maintains their 1/12 record long position of 557,581 contracts. Money manager positions are nearing highs for

net longs. They could have taken out the corn by Friday afternoon. Data by CFTC is as of Tuesday.

China

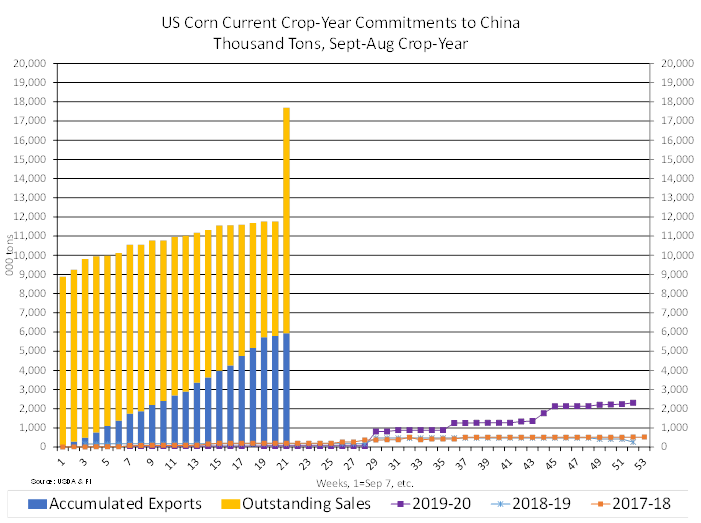

overtook Mexico as top US corn buyer.

EXPORTERS

SELL 132,000 METRIC TONS OF SOYBEANS FOR DELIVERY TO CHINA DURING 2021/2022 MARKETING YEAR- USDA

EXPORTERS

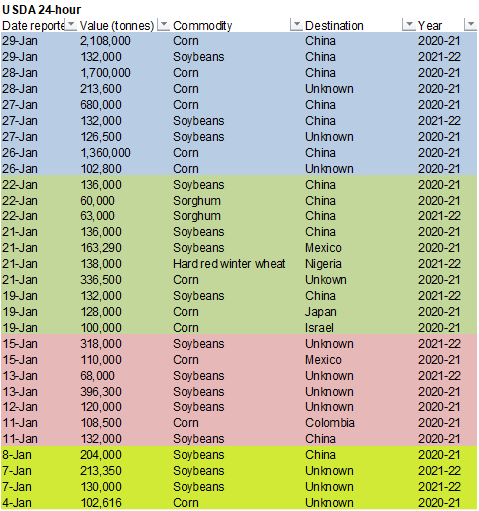

SELL 2,108,000 METRIC TONS OF CORN FOR DELIVERY TO CHINA DURING THE 2020/2021 MARKETING YEAR -USDA

Nearby

corn hit fresh contract highs

Weather

MOST

IMPORTANT WEATHER AROUND THE WORLD

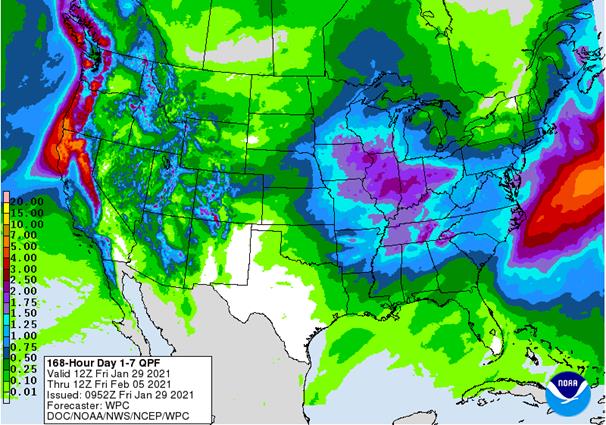

- Bitter

cold air will begin pooling in northern Canada this weekend and early next week and will surge southward across Canada’s Prairies and into the northern U.S. Plains during the second half of next week - This

cold surge will last for about ten days with varying degrees of intensity - Some

of the cold will briefly seep through the Rocky Mountains and into the far western United States - Some

of the cold air will eventually sweep into the Midwest and Atlantic Coast states, but not until the first weekend in February and on into the week of February 8

- U.S.

Midwest weekend storm will produce heavy snowfall briefly from far northeastern Illinois into southern Wisconsin, northern Indiana, southern Michigan and parts of northern and eastern Ohio

- Transportation

will be slowed - Chicago

and South Bend, Indiana and areas north into Milwaukee, and Madison, Wisconsin will be most impacted with air and land travel delays possible - Blizzard

conditions may evolve in the northeastern Plains and upper Midwest during mid-week next week as the arctic air pushes south into the those areas - The

details of this storm will be adjusted during the weekend, but preparations for the event should take place soon - Multiple

inches of snow and very strong wind speeds are expected - The

eastern Dakotas, Minnesota, a part of Nebraska Iowa could be impacted along with Wisconsin possibly - U.S.

and southwestern Canada wheat areas should become adequately protected against next week’s bitter cold by anticipated snowfall - Snow

will occur in Montana, Alberta and southwestern Saskatchewan during mid-week next week ahead of the arctic surge - However,

if the snow fails to evolve the potential for crop damage might rise higher than that of earlier this week because temperatures will ultimately fall lower than those of this week - U.S.

hard red winter wheat production areas will lose snow cover this weekend and early next week due to warmer temperatures and will need snow back again before the arctic outbreak begins - The

needed snow should fall before there is any serious concern over crop conditions - West

and South Texas crop areas will continue struggling for moisture and very little is expected over the next ten days - Soil

moisture remains excessive in parts of the U.S. southeastern states and weather in the next ten days will perpetuate the wet bias - U.S.

Delta precipitation will decrease during the coming week to ten days especially in the south - Far

western U.S. precipitation this week has been excellent for bolster soil moisture for crop areas in California’s central valleys - Snow

depth increases in the Sierra Nevada has been impressive this week - Less

frequent and less significant precipitation is expected over the next ten days, but additional precipitation will still occur in waves - Flooding

in coastal areas has been great enough to induce a few mud slides - Drought

in the western United States has not been seriously changed by this week’s precipitation, although California has seen enough moisture for improved topsoil conditions and has potential for better water supply in the spring as snow melts and runoff begins - Russia

will experience bitter cold weather later next week and on into the middle of February

- Early

indications suggest no winterkill will result because of new snow that precede the event and the deep snow that is already present in parts of the region to be coldest.

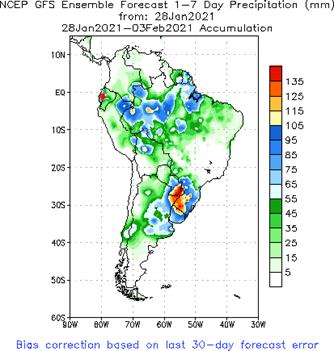

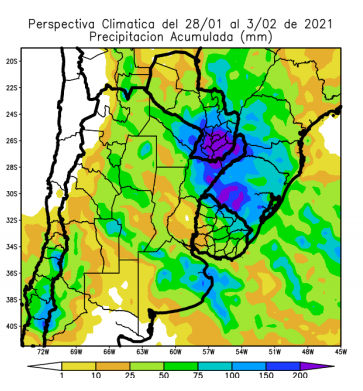

- Central

Argentina received some good solid rainfall overnight - Most

of Cordoba’s key crop areas reported 0.75 to 1.30 inches with local totals to 2.50 inches - Santa

Fe reported 1.00 to 3.25 inches in the interior south and some of this beneficial rain reached into northern Buenos Aires and western Entre Rios - Most

computer forecast models are still promoting more rain for Argentina periodically over the next ten days maintaining a favorable environment for crop development, despite some pockets of ongoing dry soil - Far

southwestern areas will not receive enough rain to counter evaporation, but crop development elsewhere should advance favorably, although not necessarily ideally - Brazil

weather continues wettest in the west and south parts of the country leaving areas from Minas Gerais and northeastern Sao Paulo northward into southern Piaui and Bahia in a net drying mode - Crop

stress is rising in these more northeastern locations and relief is needed - Showers

expected next week will be a little too brief and light to have a lasting impact, but any rain is better than none - Brazil

coffee areas in east-central Minas Gerais, southern Espirito Santo and Rio de Janeiro have been drying out for an extended period of time and there is not much irrigation available - Crop

stress is on the rise and little relief is expected for the next ten days - Flooding

rain expected from far northeastern Argentina and Paraguay into Rio Grande do Sul and some neighboring areas during the coming week is not likely to cause much damage - Crops

in low-lying areas will be impacted, but the production cuts are not likely to be very great - Some

loss cannot be ruled out, but much of the rain will be spread out over multiple days which should help localize the greatest flooding

- Paraguay

production should be most impacted from the excessive rainfall and ensuing floods, although some of the rice in Rio Grande do Sul could be negatively impacted as well. - Snow

cover is expected to decrease across parts of southeastern Europe, including Ukraine and a part of Russia’s Southern Region during the weekend and early part of next week - Cooling

later next week and into the second week of February will allow some snow cover to return prior any bitter cold temperatures settling into these areas keeping the potential for winterkill minimal - Flood

potentials are high in parts of western Europe and the eastern Adriatic Sea nations where frequent rain of significance has been occurring over multiple weeks - Local

flooding has already been occurring - No

generalized major flood event is anticipated for now because of the absence of large storm systems, but the situation must be closely monitored for later this winter and spring – or at least until a period of dry weather evolves - France,

Germany, the U.K. and northern Spain are among the most vulnerable western nations for flooding – if a more significant storm system evolves before needed drying occurs - North

Africa dryness is mostly confined to southwestern Morocco and areas from near the Morocco/Algeria border into northwestern Algeria - These

areas will remain dry biased for a while, but this is a time of year in which crops are semi-dormant which limits the need for moisture until seasonal warming begins.

- Some

rain may evolve in a part of this region at the end of next week - South

Africa will receive widespread rain during the next ten days further ensuring good production potentials for its summer crops - Far

northern and central India may receive some welcome showers over the next week to ten days - Most

of India’s winter crops will reproduce over the next few weeks and timely rain is needed to induce the best yields - Rain

expected late next week mostly from southern Uttar Pradesh and southeastern Madhya Pradesh to West Bengal, Bangladesh and northeastern Odisha and resulting rainfall will be light - Rain

is also expected this weekend into early next week in Punjab, Haryana, easternmost Rajasthan and northern Uttar Pradesh to benefit a few winter crops in that region - Most

of the rain will be a little too light to make a serious change to crop conditions, but any moisture is better than none.

- Queensland,

Australia’s sorghum and cotton areas need significant rain along with most of its livestock region, but precipitation will be restricted over the next week to ten days - Crop

conditions are better than they were last year at this time, but drought remains in Queensland’s central and south

- There

have been some beneficial rain events in southeastern Queensland this summer, but greater moisture is needed to induce the best possible cotton and sorghum production

- Sugarcane

areas along the upper coast are rated favorably - Rain

in New South Wales, Australia today and a few showers next week will be welcome and good for cotton and sorghum, but more moisture will be desired - China

wheat and rapeseed are favorably rated and expected to perform well in the spring.

- There

is no threatening cold weather for the next two weeks and sufficient precipitation will fall to maintain status quo conditions - Bitter

cold is expected in the Northeast Provinces, but winter wheat is not produced significantly in that region - West

Africa rainfall will remain mostly confined to coastal areas while temperatures in the interior coffee, cocoa, sugarcane, rice and cotton areas are in a seasonably warm range for the next ten days - Some

rain will fall in a few coastal areas during the coming week, but most of the precipitation will stay far from coffee and cocoa production areas.

- East-central

Africa rainfall will continue limited in Ethiopia as it should be at this time of year while frequent showers and thunderstorms impact Tanzania. - Kenya

and Uganda will receive some infrequent rainfall over the next ten days - Southern

Oscillation Index remained very strong during the weekend and was at +17.02 today and the index will remain strongly positive over the coming week - Southeast

Asia weather is not likely to change much over the coming week - Mainland

areas have been will continue to be mostly dry - Philippines

rainfall will be erratic and mostly light, but it may increase somewhat during the next ten days - Indonesia

and Malaysia rainfall has been, but sufficient in maintaining a very good crop development environment - No

excessive rain occurred recently and little is anticipated for a while - Southeastern

Mexico will get most of the rain periodically during the next ten days - The

precipitation will be erratic and mostly light, but still welcome wherever it occurs - Many

areas in Mexico are still dealing with long term drought - Central

America precipitation will continue greatest along the Caribbean Coast while the Pacific Coast is relatively dry - Canada

Prairies will briefly warm this weekend and early next week and then a new period of bitter cold is expected as time moves along late next week and into the following weekend - Precipitation

will be periodic and mostly light - Southeast

Canada will experience restricted precipitation and seasonably cool temperatures over the coming week

Source:

World Weather Inc. and FI

Friday,

Jan. 29:

- ICE

Futures Europe weekly commitments of traders report, 1:30pm (6:30pm London) - CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm - U.S.

agricultural prices paid, received - U.S.

cattle inventory

Sunday,

Jan. 31:

- Malaysia

Jan 1-31 palm oil export data from Intertek

Monday,

Feb 1:

- USDA

weekly corn, soybean, wheat export inspections, 11am - EU

weekly grain, oilseed import and export data - Malaysia

Jan 1-31 palm oil export data from AmSpec (tentative) - China

starts trading peanut futures on Zhengzhou Commodity Exchange - U.S.

DDGS production, soybean crush, 3pm - Australia

Commodity Index - Ivory

Coast cocoa arrivals - HOLIDAY:

Malaysia

Tuesday,

Feb 2:

- U.S.

Purdue Agriculture Sentiment - New

Zealand global dairy trade auction - U.S.

corn for ethanol, 3pm

Wednesday,

Feb 3:

- EIA

weekly U.S. ethanol inventories, production, 10:30am - New

Zealand Commodity Price

Thursday,

Feb 4:

- FAO

World Food Price Index; cereals supply/demand brief - USDA

weekly crop net-export sales for corn, soybeans, wheat, cotton, pork, beef, 8:30am - Port

of Rouen data on French grain exports

Friday,

Feb 5:

- ICE

Futures Europe weekly commitments of traders report, 1:30pm (6:30pm London) - CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm - China’s

CNGOIC to publish soybean and corn reports - Statcan

reports on wheat, soy, durum, canola and barley stockpiles in Canada

Source:

Bloomberg and FI

CFTC

COT showed

a record long position for CBOT traditional funds futures only corn of 547,677 contracts. Traditional funds futures and options combined maintains their 1/12 record long position of 557,581 contracts. Money manager positions are nearing highs for net longs.

They could have taken out the corn by Friday afternoon. Data by CFTC is as of Tuesday. Keep an eye on the changes in weekly positions for traditional funds and money managers, for futures only versus futures and options combined. The divergence over the

last couple of reports may indicate option volume is up.

Macros

Canada

Q4 GDP Up c.1.9% Vs. Q3 – StatsCan Flash Estimate

2020

GDP Down 5.1% Versus 2019

US

Employment Cost Index Q4: 0.7% (est 0.5%; prev 0.5%)

US

Personal Income Dec: 0.6% (est 0.1%; prev -1.1%)

US

Personal Spending Dec: -0.2% (est -0.4%; prev -0.4%)

US

Real Personal Spending Dec: -0.6% (est -0.6%; prev -0.4%)

US

Core PCE Deflator (M/M) Dec: 0.3% (est 0.1%; prev 0.0%)

US

Core PCE Deflator (Y/Y) Dec: 1.5% (est 1.3%; prev 1.4%)

US

PCE Deflator (M/M) Dec: -0.4% (est 0.3%; prev 0.0%)

US

PCE Deflator (Y/Y) Dec: 1.3% (est 1.2%; prev 1.1%)

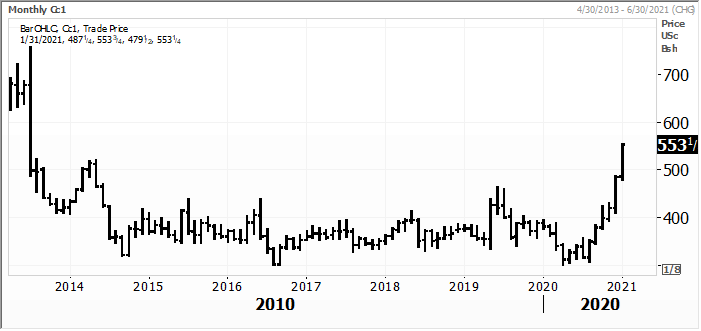

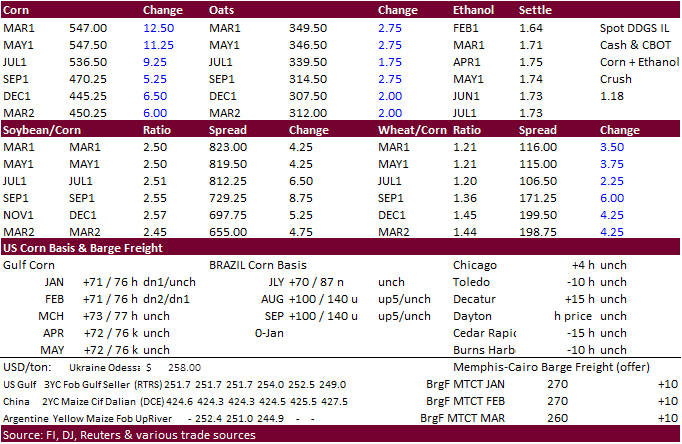

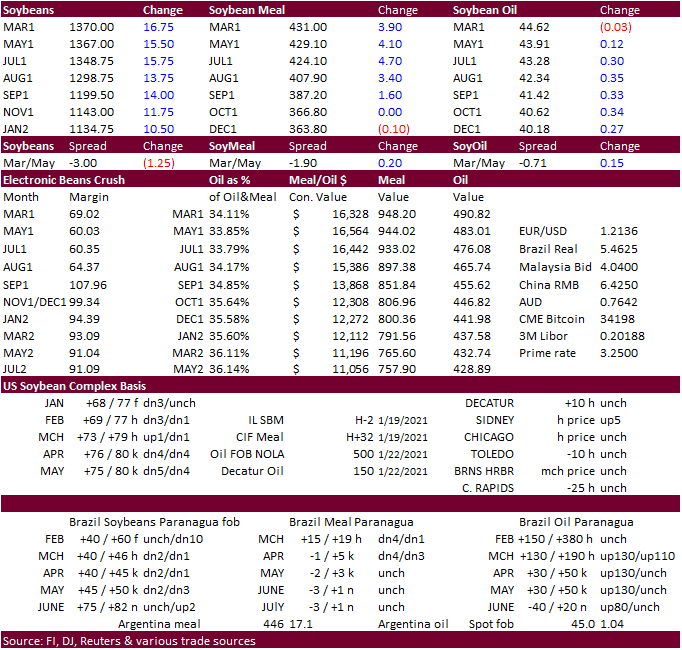

Corn.

-

March

corn charged higher from China buying more than 6 million tons of corn for the balance of the week. Nearby rolling corn is at a 7-1/2 year high.

-

$5.5375

is the new contract high. -

$5.60

is seen as the next resistance level. -

China

may easily import more corn that their current TRQ in 2021. All the corn reported this week is for 2020-21 delivery. We think China will be pushing back some of those commitments to 2021-22.

-

Spread

traders should monitor March corn versus July and new-crop December. During the session the CH21/CZ21 traded above $1.00, first time since 2013.

-

Ukraine

grain exports are running 20% lower since the start of the marketing year to 28.7 million tons. Traders sold 12.99 million tons of wheat, 10.37 million tons of corn and 3.9 million tons of barley. The government has said exports could decline to 45.4 million

tons in 2020/21 because of a weaker harvest. (Reuters)

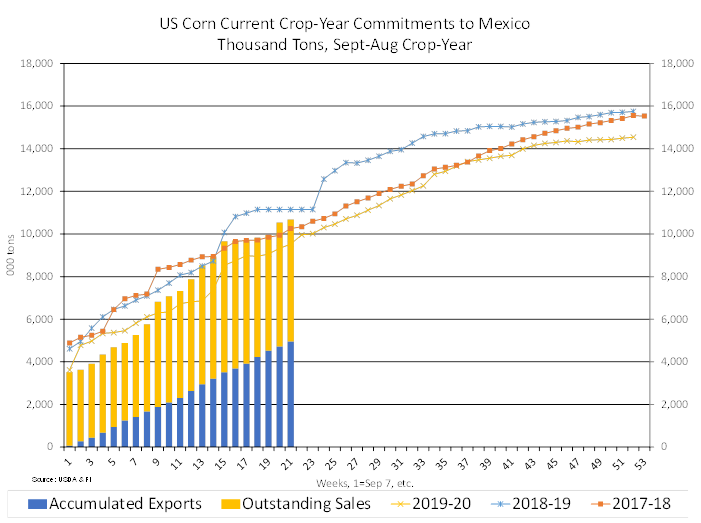

China

overtook Mexico as to US corn buyer. Below are some stats.

China

as of 1/21 USDA export sales report:

2020-21

crop year:

5.909

MMT outstanding

5.936

MMT accumulated exports

11.845

MMT total commitments

2021-22

crop year – nothing on books

Unknown

7.878 million tons outstanding / nothing for new crop

That

puts China commitments at least 17.7 million tons for 2020-21; nothing for new crop. Unknown destinations at least 8.2 million tons.

Mexico:

2020-21

outstanding sales totaled 5.727 million tons and accumulated exports at 4.953 million tons (10.681 million tons total commitments).

Below

is what the China sales chart could look like next week versus Mexico (below China)

Corn

Export Developments

·

WASHINGTON, January 29, 2021–Private exporters reported to the U.S. Department of Agriculture the follow activity:

–Export

sales of 2,108,000 metric tons of corn for delivery to China during the 2020/2021 marketing year

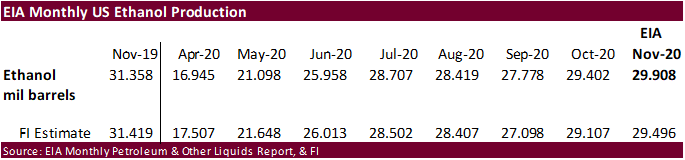

November

ethanol output near expectations. No

change to our 5.000 bil bu corn crush. USDA @ 4.950 billion versus 4.852 billion 2019-20.

Updated

1/29/21

March

corn is seen trading in a $5.15 and $6.00 range.

May

corn is seen in a $5.00 and $6.00 range.

July

is seen in a $4.90 and $5.75 range.

December

is seen in a $3.75-$5.50 range.

-

CBOT

soybeans

traded higher in large part to strength in the corn market. The slow soybean harvest progress in Brazil added to the positive undertone. March soybeans settled up 16-3/4 cents at $13.70 per bushel. For the month they are up 4.5%, or nearly 60 cents. Soybean

meal saw a two-sided trade but a strong finish pulled the March contract up $3.90 at $431 per short ton. March soybean oil dropped slightly and settled at 44.62 cents, still an impressive level after global vegetable oils rallied this week. Palm oil hit

a 2-week high. USDA announced 132,000 tons of soybeans were sold to China, but that news was overshadowed by the massive corn sale.

-

Safras

& Mercado raised its estimate of Brazil’s 2020-21 soybean crop to 133.1 million tons, from 132.5 million previously.

-

Argentina

will see good weather over the next week. Northeastern Brazil will continue to see dry conditions.

SBO

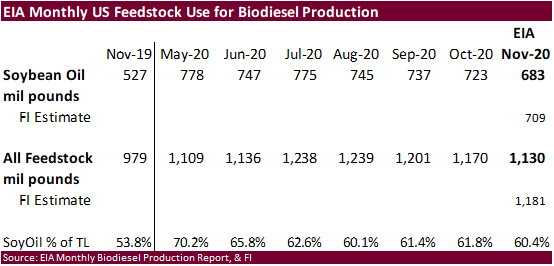

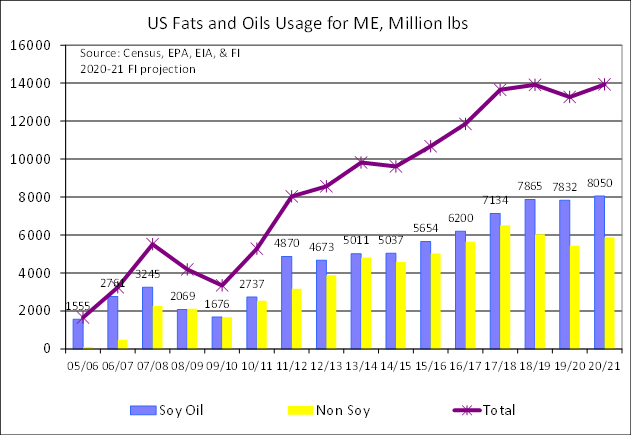

for biodiesel. USDA

may have been a little premature in upward revising their soybean oil for biodiesel use earlier this month (8.100 billion pounds to 8.200 billion) as November soybean oil use fell below expectations at 683 million pounds, but that is up from 527 million year

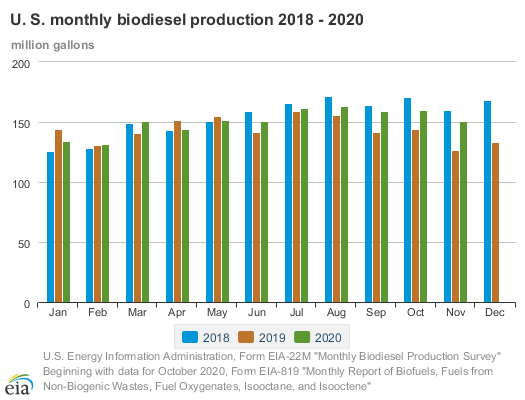

earlier. We were looking for 709 million pounds. U.S. production of biodiesel was 151 million gallons in November 2020. 9 million gallons lower than production in October 2020. There was a total of 1,130 million pounds of feedstocks (FI est. 1181) used to

produce biodiesel in November 2020, up from 979 million pounds November 2019. We are going to maintain our 8.050 billion pound soybean oil use for biodiesel estimate, below USDA’s 8.200 estimate and above 7.858 billion used in 2019-20.

Oilseeds

Export Developments

·

Egypt’s GASC seeks at least 30k soybean oil and 10k sunflower oil on Feb 2 for March 10-30 arrival.

·

South Korea’s MFG bought about 60,000 tons of soybean meal at $501.95/ton c&f for arrival around Aug.

·

WASHINGTON, January 29, 2021–Private exporters reported to the U.S. Department of Agriculture the follow activity:

–Export

sales of 132,000 metric tons of soybeans for delivery to China during the 2021/2022 marketing year.

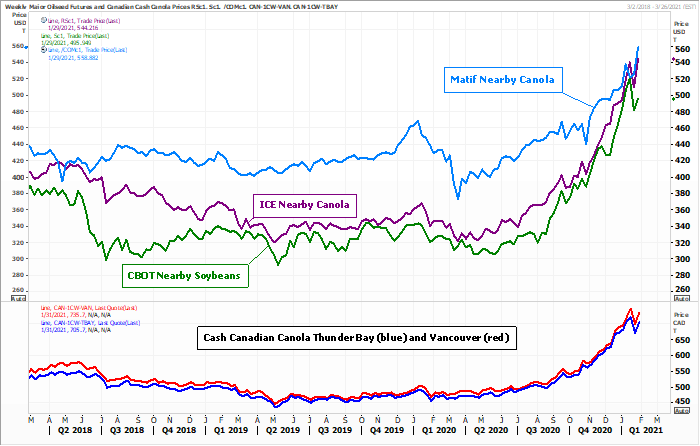

Canadian

canola exports

off the PNW was so robust over the past few weeks it limited Canadian wheat exports. Some estimates for Canada canola 2021 plantings are suggesting a 6 percent increase.

Updated

1/26/21

March

soybeans are seen in a $13.25 and $14.75 range

March

soymeal is seen in a $410 and $480 range

March

soybean oil is seen in a 42.50 and 45.00 cent range

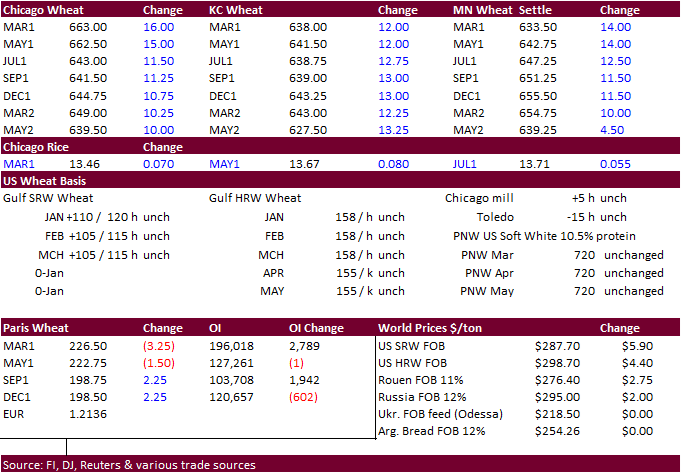

- US

wheat futures saw a higher trade on Friday on technical buying following higher corn and soybeans. US wheat might be the next headliner if China decides to stockpile the commodity, but for now, expectations for Black Sea shipments to slow and fund investing

into commodities should keep a positive undertone on the three US markets.

- On

Saturday there was a news article talking about Russia could impose a formula based wheat export tax from June 1. We thought this might be in the works as they tame domestic food inflation. What this could lead to is higher North America wheat exports during

the summer months, if global prices continue to rise into new-crop. Previously Russia set a 25 euros ($30) per ton tax for Feb. 15 to 28, rising to 50 euros per ton from March 1 to June 30.

- EU

March milling wheat was down 3.25 at 226.50 euros. - SovEcon

raised its forecast for Russia’s 2020-21 wheat exports by 1.6 million tons to 37.9 million tons. This could be in part to a last min attempt to get wheat out before higher taxes kick in. They said Russia’s January wheat exports may reach 3.3 million tons,

up 57% year on year.

-

Taiwan

Flour Millers’ Association bought 85,340 tons of milling wheat to be sourced from the United States. First consignment for shipment between March 22 and April 5 involved 21,645 tons of U.S. dark northern spring wheat of 14.5% protein content bought at $291.36

a ton FOB U.S. Pacific Northwest coast. It involved 13,675 tons of hard red winter wheat of 12.5% protein bought at $291.10 a ton FOB and 7,070 tons of soft white wheat of 9% protein bought at $300.18 a ton FOB. Second consignment for shipment between April

8 and April 22 involved 23,260 tons of dark northern spring wheat of 14.5% protein content bought at $287.68 a ton FOB U.S. Pacific Northwest coast and included 14,075 tons of hard red winter wheat of 12.5% protein content bought at $291.10 a ton FOB and 5,615

tons of soft white wheat of 9% protein bought at $290.97 a ton FOB. -

Jordan

is in for another 120k wheat on Feb 3 and 120k barley on Feb 2.

·

Iraq seeks 30,000 tons of rice on Feb 3, valid until Feb 10, optional origin.

·

Syria is in for 25,000 tons of rice on February 9.

Updated

1/26/21

March

Chicago wheat is seen in a $6.35‐$7.15 range

March

KC wheat is seen in a $6.25‐$6.70 range (up 10 & 15)

March

MN wheat is seen in a $6.00‐$6.55 range

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International

One Lincoln Center

18 W 140 Butterfield Rd.

Oakbrook Terrace, Il. 60181

W: 312.604.1366

ICE IM:

treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered

only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making

your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors

should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or

sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy

of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.