PDF Attached

WASHINGTON,

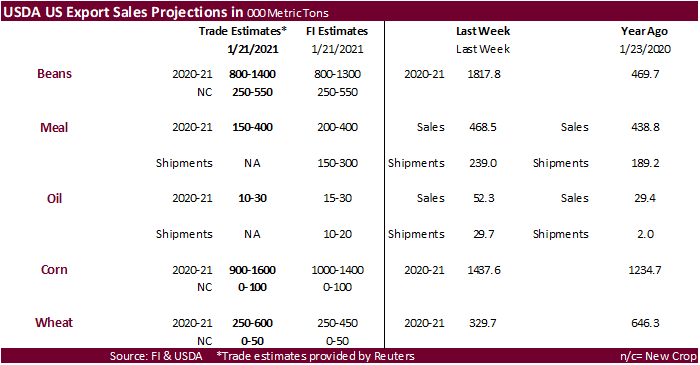

January 27, 2021–Private exporters reported to the U.S. Department of Agriculture the following activity:

–Export

sales of 680,000 metric tons of corn for delivery to China during the 2020/2021 marketing year;

–Export

sales of 132,000 metric tons of soybeans for delivery to China during the 2021/2022 marketing year; and

–Export

sales of 126,500 metric tons of soybeans for delivery to unknown destinations during the 2020/2021 marketing year.

MOST

IMPORTANT WEATHER AROUND THE WORLD

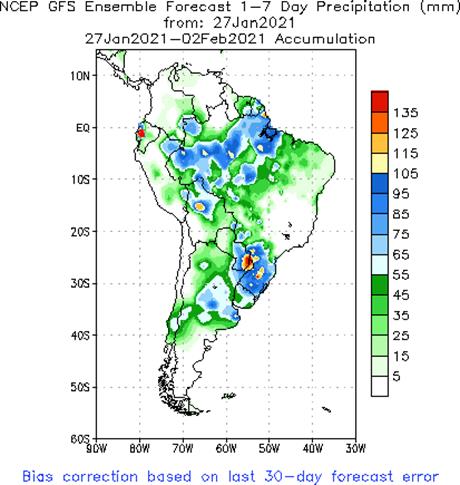

- Argentina

weather over the next ten days will be well mixed with opportunities for rain occurring in most of the nation supporting a relatively good environment for crop development - Brazil

crop weather will remain mostly good in the west and south with a favorable mix of rain and sunshine supporting ongoing crop development and some early harvesting of soybeans - Northeastern

Brazil will get some temporary relief from dryness during mid- to late week next week, but the bottom line will continue stressful until then and the amount of relief is likely to be a little disappointing - Flooding

rain expected from far northeastern Argentina and Paraguay into Rio Grande do Sul and some neighboring areas in Parana and Santa Catarina during the coming week to ten days is not likely to cause much damage - Crops

in low-lying areas will be impacted, but the production cuts are not likely to be very great - Some

loss cannot be ruled out, but much of the rain will be spread out over multiple days which should help localize the greatest flooding

- Paraguay

production should be most impacted from the excessive rainfall and ensuing floods - No

threatening cold temperatures are perceived for any winter crop production area in the northern Hemisphere that is not snow covered for at least the next week - Cooling

in February will raise the need for snow in the northwestern U.S. Plains and southwestern Canada’s Prairies - Snow

cover is expected to decrease across parts of southeastern Europe, including Ukraine and a part of Russia’s Southern Region, but no threatening cold is expected anytime soon - Flood

potentials are high in western Europe and the eastern Adriatic Sea nations where frequent rain of significance has been occurring over multiple weeks - Local

flooding has already been occurring - No

generalized major flood event is anticipated for now because of the absence of large storm systems, but the situation must be closely monitored for later this winter and spring – or at least until a period of dry weather evolves - North

Africa dryness is mostly confined to southwestern Morocco and areas from near the Morocco/Algeria border into northwestern Algeria - These

areas will remain dry biased for a while, but this is a time of year in which crops are semi-dormant which limits the need for moisture until seasonal warming begins.

- South

Africa will receive widespread rain during the next ten days further ensuring good production potentials for its summer crops - Central

India may receive some needed showers in the second half of next week, but will be dry until then - Most

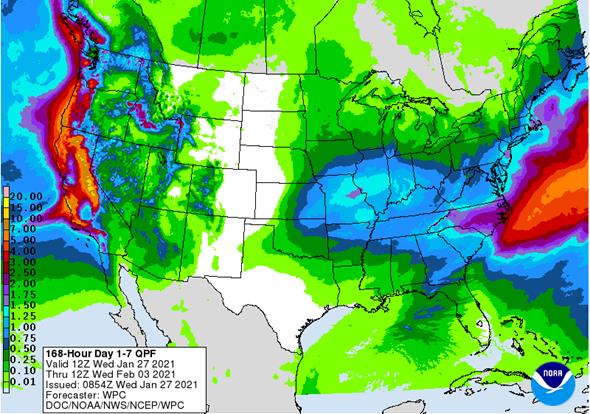

of India’s winter crops will reproduce over the next few weeks and timely rain is needed to induce the best yields - U.S.

hard red winter wheat areas benefited from this week’s snowstorm, but there will still be an ongoing need for greater moisture in the soil across many areas - La

Nina conditions will prevail into early spring and that will likely keep precipitation events a little more meager than usual - The

need for rain will rise as seasonal warming begins in the spring - U.S.

snowstorm this week slowed transportation and was a little stressful for livestock from the central Plains to the Great Lakes region, but there was not much serious impact - Western

U.S. storminess is expected to improve topsoil moisture, but more precipitation will be needed to more seriously impact drought conditions - California’s

Sierra Nevada is experiencing rising snow depths that will improve runoff for the state’s reservoirs - Early

season precipitation in California and most of the western U.S. was well below average - Only

parts of the Pacific Northwest have been reporting routinely occurring precipitation and much of that has been on the coast

- U.S.

Midwest, Delta and southeastern states are still plenty moist which is not unusual for this time of year - The

moisture abundance in parts of the Delta and southeastern states, however, is unusual for a La Nina year - Some

drying will occur in these areas later this season - Drought

in the U.S. northwestern Plains and southwestern Canada’s Prairies is still significant an must change in the spring to support normal planting conditions - New

South Wales, Australia will receive some needed rain over the coming week improving both dryland and irrigated crop conditions - Queensland,

Australia’s sorghum and cotton areas need significant rain along with most of its livestock region, but precipitation will be restricted over the next week to ten days - Crop

conditions are better than they were last year at this time, but drought remains in Queensland’s central and south

- Sugarcane

areas along the upper coast are rated favorably - China

wheat and rapeseed are favorably rated and expected to perform well in the spring.

- There

is no threatening cold weather for the next two weeks and sufficient precipitation will fall to maintain status quo conditions - West

Africa rainfall will remain mostly confined to coastal areas while temperatures in the interior coffee, cocoa, sugarcane, rice and cotton areas are in a seasonable range for the next ten days - Some

rain fell in coastal areas of Ivory Coast and Ghana during the weekend, but key crop areas were dry - East-central

Africa rainfall will continue limited in Ethiopia as it should be at this time of year while frequent showers and thunderstorms impact Tanzania. - Kenya

and Uganda will receive some infrequent rainfall over the next ten days - Southern

Oscillation Index remained very strong during the weekend and was at +17.55 today and the index will remain strongly positive over the coming week - Southeast

Asia weather is not likely to change much over the coming week - Mainland

areas have been will continue to be mostly dry - Philippines

rainfall will be erratic and mostly light, but it may increase somewhat during the next ten days - Indonesia

and Malaysia rainfall has been, but sufficient in maintaining a very good crop development environment - No

excessive rain occurred recently and little is anticipated for a while - Northern

and far southeastern Mexico will get most of the rain periodically during the next ten days - The

precipitation will be erratic and mostly light, but still welcome wherever it occurs - Many

areas in Mexico are still dealing with long term drought - Central

America precipitation will continue greatest along the Caribbean Coast while the Pacific Coast is relatively dry - Canada

Prairies will continue cold for another day or two, but some warming is expected - Precipitation

will be periodic and mostly light - Southeast

Canada will experience restricted precipitation and seasonable temperatures over the coming ten days

Source:

World Weather Inc. and FI

Wednesday,

Jan. 27:

- EIA

weekly U.S. ethanol inventories, production, 10:30am - National

Coffee Association’s webinar on U.S. coffee outlook in 2021 - Paris

Grain Day virtual conference, day 1 - EARNINGS:

Barry Callebaut

Thursday,

Jan. 28:

- USDA

weekly crop net-export sales for corn, soybeans, wheat, cotton, pork, beef, 8:30am - USDA

releases Citrus Report on global demand and supply - Port

of Rouen data on French grain exports - Paris

Grain Day virtual conference, day 2 - HOLIDAY:

Malaysia

Friday,

Jan. 29:

- ICE

Futures Europe weekly commitments of traders report, 1:30pm (6:30pm London) - CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm - U.S.

agricultural prices paid, received - U.S.

cattle inventory

Source:

Bloomberg and FI

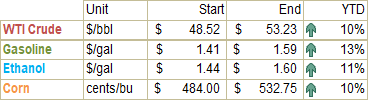

US

DoE Crude Oil Inventories (W/W) 22-Jan: -9910K (est 1500K; prev 4352K)

–

Distillate Inventories: -815K (est -500K; prev 457K)

–

Cushing Crude Inventories: -2281K (prev -4727K)

–

Gasoline Inventories: 2469K (est 1300K; prev -259K)

–

Refinery Utilization: -0.80% (est -0.30%; prev 0.50%)

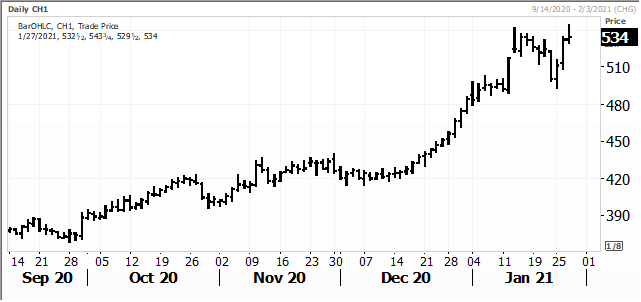

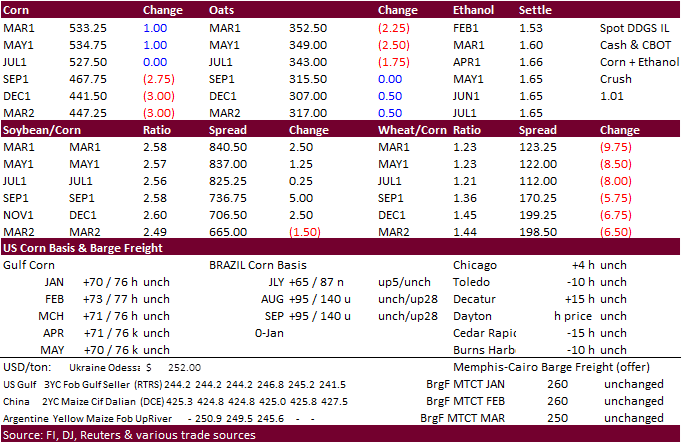

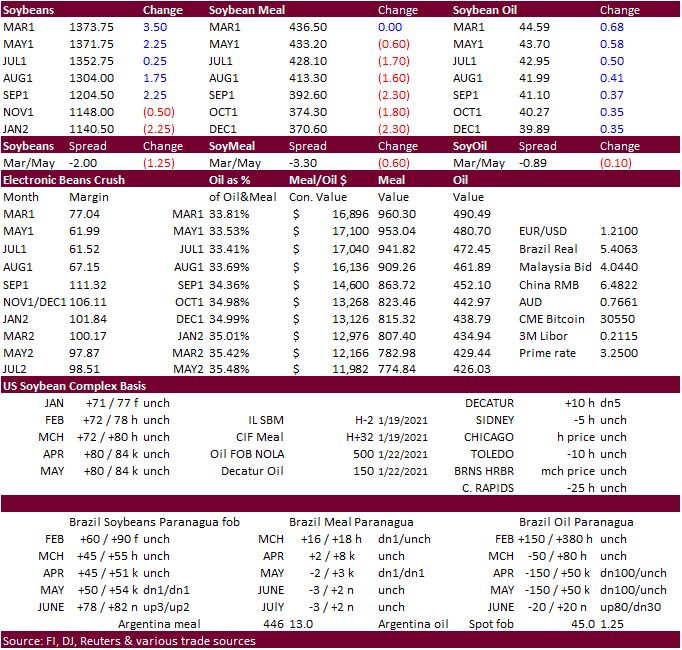

Corn.

-

Corn

futures were

higher for the font months on Chinese demand and Brazilian harvest delays. Back months were lower. In our opinion, we will need to see new-crop US prices accelerate to keep plantings of new crop above 89.5 million acres to ensure US 2021-22 stocks remain

above 1.5 billion bushels. A back to back STU for US corn balance below 15 percent suggests +$7.00 wheat and +$14.00 soybeans.

-

March

corn hit a contract high before settling 1.75 cents higher at $5.34/bu.

-

USDA

announced 680,000 tons of corn to China after announcing yesterday 1.36 million tons sold. We think these two sales could be pushed back to 2021-22 delivery as China has already committed a large amount of corn for the current crop year. But in retrospect

we do not know how much corn China is sitting on in reserves, so 5 or 10 million tons of corn imports can seem like a drop in a bucket if they keep expanding their hog population. China, on the other hand, can still import a very large amount of corn from

South America AND Ukraine over the next several months. Weighing in on US corn exports to save China from deficit is still far from reach. China demand is still bullish for CBOT corn, like wheat, converts to a global contract.

-

USD

was 52 points higher! WTI near unchanged spot and gold down 58 cents after starting higher. There is no doubt the outside markets had some influence on CBOT ag spreads today.

-

Refinitiv

estimated the Argentina corn production between 40.7-49.5 million tons, pegging it at 45.6 million tons. Many are at 47.5 million tons.

-

Bloomberg

reported the Biden administration will (would) announce debt relief measures for more than 12,000 financially distressed farmers. USDA confirmed that by suspending debt collection from farmers affected by Covid-19. Borrowing and paying back loans last year

became difficult in a tough economic environment. -

Expect

a YOY decline in corn for feed usage for Q2 crop year corn. -

The

USDA Broiler Report showed eggs set in the US down 1 percent and chicks placed down 1 percent from a year ago. Cumulative placements from the week ending January 9, 2021 through January 23, 2021 for the United States were 566 million. Cumulative placements

were down 1 percent from the same period a year earlier.

USDA

Attaché.

Canada grain and feed update

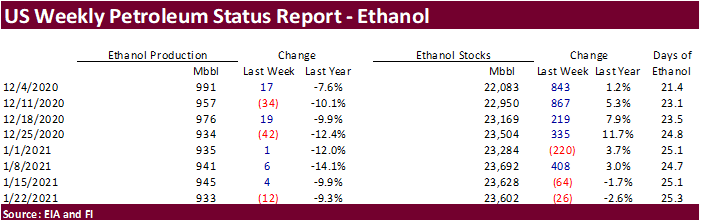

Weekly

ethanol production

declined by 12,000 barrels to 933,000, about in line with a Bloomberg survey. Stocks decreased 26,000 barrels to 23.602 million, an indication use is picking up a tad this month. However, net blender input of ethanol into finished motor gasoline tumbled

over the week ending Jan 22. Early September to date ethanol production is running 8 percent below same period a year ago.

Since

Jan 1, 2021

Corn

Export Developments

- Algeria

seeks 40,000 tons of corn on Jan 28 for Feb 25-Mar 15 shipment, optional origin.

- WASHINGTON,

January 27, 2021–Private exporters reported to the U.S. Department of Agriculture the following activity:

–Export

sales of 680,000 metric tons of corn for delivery to China during the 2020/2021 marketing year

Updated

1/26/21

March

corn is seen trading in a $4.75 and $5.50 range. New contract high could be reached this week.

-

CBOT

soybean

complex was higher led by soybean oil, again. We are short of news for the soybean complex other than the vegetable oil markets are searching for direction in a stage for a rebound from the past two weeks.

-

Note

the Feb 1 Brazil truck strike is around the corner and its gaining popularity leading up to the event. Some Twitter feeds show a robust harvesting season while others show very wet fields.

-

We

heard Argentina sold dome biodiesel to India and possibly China. China was also in for rapeseed oil this week.

Oilseeds

Export Developments

- WASHINGTON,

January 27, 2021–Private exporters reported to the U.S. Department of Agriculture the following activity:

–Export

sales of 132,000 metric tons of soybeans for delivery to China during the 2021/2022 marketing year; and

–Export

sales of 126,500 metric tons of soybeans for delivery to unknown destinations during the 2020/2021 marketing year.

Updated

1/26/21

March

soybeans are seen in a $13.25 and $14.75 range

March

soymeal is seen in a $410 and $480 range

March

soybean oil is seen in a 42.50 and 45.00 cent range (up 150 points both ends)

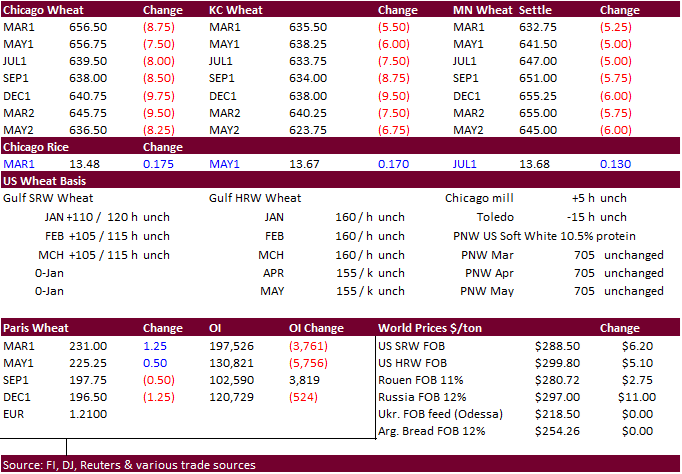

- US

wheat futures were lower on intra commodity spreading and slowing global demand as indicated by Japan overnight after passing on feed wheat. Inter commodity spreading may have spared KC type wheat from dropping more than 8 cents. However, Algeria later confirmed

they bought at least a half million tons of wheat during the session. US wheat futures are a little done to the downside, in our opinion. As we see wheat stocks globally at high levels, recent purchases on high protein wheat by countries that are interested

is keeping high human consumption reserves (Jordan, Egypt, Algeria) may support high protein wheat contracts for the next few months.

- Poor

Black Sea weather is holding up some wheat shipments. - Keep

an eye on Argentina regarding wheat export caps. Rumors are mounting they will restrict shipments. Bigger picture is that wheat, globally, shows the largest amount of stocks among major commodities, but remains the most price sensitive versus other food

commodities, IMO. - EU

March milling wheat was up 1.25 at 231.00 euros. - We

are hearing Russian exporters are trying to get exports done prior to the tax kicking in Feb 15. Below is a link from twitter recognizing this.

https://twitter.com/sizov_andre/status/1354449429277896712

- Algeria’s

state grains agency OAIC bought an unknown amount of wheat between $312 to $314 a ton c&f. Some 500-660k could have been purchased for shipment in two periods from March 1-15 and March 16-31. If sourced from South America or Australia, shipment is between

Feb. 1-15 and Feb. 16-28. - Japan’s

AgMin in a SBS import tender passed on 80,000 tons of feed wheat and bought only 440 tons of (out of 100,000 tons) feed barley for arrival by March 18, on January 27.

- Jordan

bought 60,000 tons of milling wheat, optional origin.

-

Japan

seeks 60,175 tons of Australian food wheat this week.

-

Taiwan

launched an import tender for 85,340 tons of US wheat, set to close Jan 29, for late March through April 22 shipment.

·

Iraq seeks 30,000 tons of rice on Feb 3, valid until Feb 10, optional origin.

·

Syria is in for 39,400 tons of rice on Feb 22. They are also in for 25,000 tons of rice on February 9.

Updated

1/26/21

March

Chicago wheat is seen in a $6.35‐$7.15 range

March

KC wheat is seen in a $6.25‐$6.70 range (up 10 & 15)

March

MN wheat is seen in a $6.00‐$6.55 range

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International

One Lincoln Center

18 W 140 Butterfield Rd.

Oakbrook Terrace, Il. 60181

W: 312.604.1366

ICE IM:

treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered

only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making

your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors

should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or

sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy

of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.