PDF Attached

WASHINGTON,

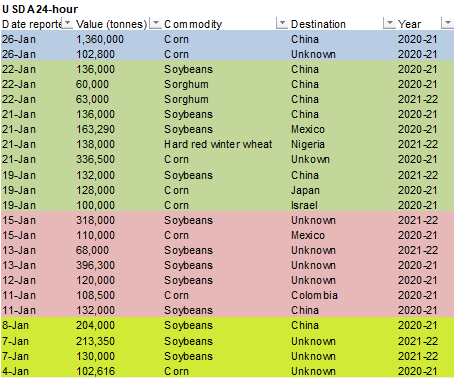

January 26, 2021–Private exporters reported to the U.S. Department of Agriculture the following activity:

–Export

sales of 1,360,000 metric tons of corn for delivery to China during the 2020/2021 marketing year; and

–Export

sales of 102,800 metric tons of corn for delivery to unknown destinations during the 2020/2021 marketing year.

Another

shocking session for agriculture futures. Soybeans and corn led the charge higher in part to Chinese demand. ICE canola hit a 123-year high. Australia confirmed they exported a large amount of wheat to China during December, a complete reversal from very

little exported in November, and a hint Chinese demand for wheat is very strong. China already sold 10 million tons of wheat from reserves through auctions so far in January. Meanwhile ADM sees China eventually importing 25 million tons of corn. Russian

confirmed higher export taxes for wheat and grains.

MARKET

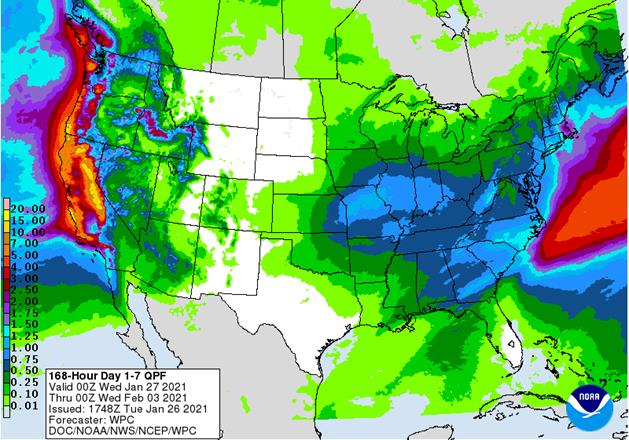

WEATHER MENTALITY FOR CORN AND SOYBEANS:

Conditions

in Brazil and Argentina are not changing and that leaves Brazil crop moisture beneficial in most of the key grain and oilseed production areas. Argentina is expected to still have some pockets of drying that will need to be watched, but the nation (like Rio

Grande do Sul, Brazil) is doing better than some feared. Talk of flooding in the coming week from Corrientes and some immediate neighboring areas of Paraguay and eastern most parts of Chaco and Formosa into Rio Grande do Sul may not cause much damage to crops,

but it will give the market place something else to talk about. Flooding may be most significant in Paraguay and northwestern Rio Grande do Sul where the ground is wettest from previous rain.

India’s

winter crops are dry and will need some moisture in February to support the best yields. South Africa rainfall and temperatures will be nearly ideal for the best possible production potential.

China

and Europe winter crops are still dormant and most are poised to develop favorably in the spring.

Australia’s

sorghum produced in New South Wales will improve with expected rain this week, but Queensland unirrigated crop areas still need rain.

Overall,

weather today will likely support a mixed influence on market mentality.

MARKET

WEATHER MENTALITY FOR WHEAT: Precipitation expected in U.S. hard red winter wheat this week will improve soil moisture for use in the spring. Little to no crop damage occurred from bitter cold in Montana or southwestern parts of Canada’s Prairies in recent

days, despite snow free conditions and temperatures near the damage threshold. This situation will continue into Wednesday before warming evolves.

Other

winter crops in North America, Europe and the western CIS have not experienced any crop damaging cold this year, so far, and mild to warm weather in the coming week will keep that potential very low. The same is true for China. India’s winter crops need rain

in February to induce the best yield potentials. North Africa rainfall will continue limited in the driest areas of southwestern Morocco and northwestern Algeria for the next ten days. A boost in precipitation is needed in the Middle East.

Overall,

weather today will likely induce a mixed influence on market mentality with a slight bearish bias.

Source:

World Weather Inc. and FI

Tuesday,

Jan. 26:

- EARNINGS:

ADM - HOLIDAY:

India, Australia

Wednesday,

Jan. 27:

- EIA

weekly U.S. ethanol inventories, production, 10:30am - National

Coffee Association’s webinar on U.S. coffee outlook in 2021 - Paris

Grain Day virtual conference, day 1 - EARNINGS:

Barry Callebaut

Thursday,

Jan. 28:

- USDA

weekly crop net-export sales for corn, soybeans, wheat, cotton, pork, beef, 8:30am - USDA

releases Citrus Report on global demand and supply - Port

of Rouen data on French grain exports - Paris

Grain Day virtual conference, day 2 - HOLIDAY:

Malaysia

Friday,

Jan. 29:

- ICE

Futures Europe weekly commitments of traders report, 1:30pm (6:30pm London) - CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm - U.S.

agricultural prices paid, received - U.S.

cattle inventory

Source:

Bloomberg and FI

Philadelphia

Non-Manufacturing Regional Business Activity Index Jan: -17.5 (prev -26.6)

Non-Manufacturing

Regional Fed Wage And Benefit Cost Index: 16.4 (prev 8.4)

Non-Manufacturing

Full-Time Employment Index: 3.1 (prev -5.8)

Non-Manufacturing

New Orders Index: 0.2 (prev -9.5)

Non-Manufacturing

Firm-Level Business Activity Index: -14.3 (prev 5.0)

US

FHFA House Price Index (M/M) Nov: 1.0% (est 0.8%; prev 1.5%)

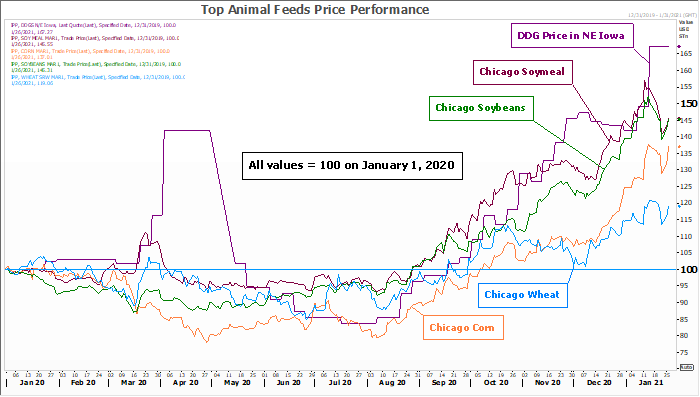

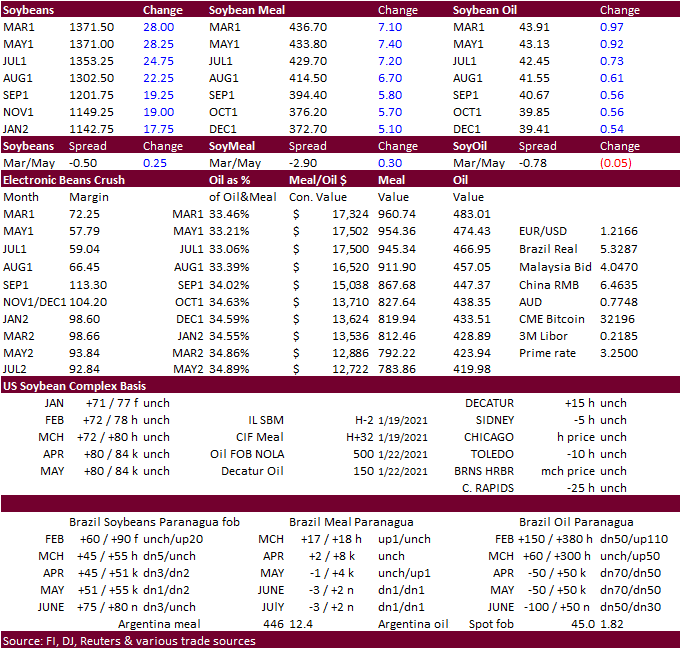

Corn.

-

Corn

futures were

up sharply before the day session open on talk of China picking up US corn on Monday. Prices traded further higher after USDA announced China bought corn. The March contract erased Friday’s losses. We could easily see new contract highs this week if China

continues to secure corn. Out of all the major US commodity and futures markets, grains were up about 2% followed by 1.20 percent increase in softs. Meats were about 1.25 percent lower.

-

USDA

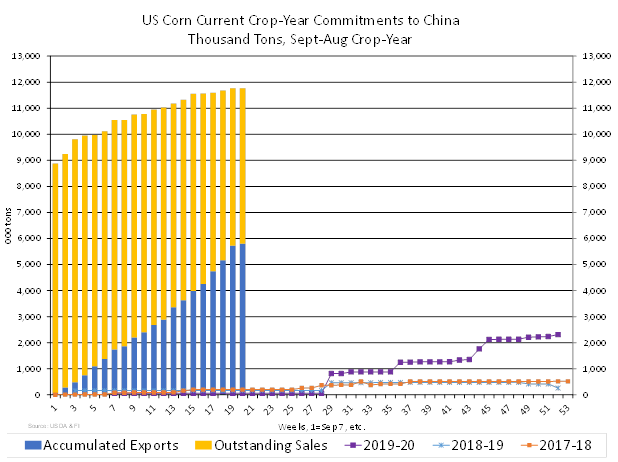

announced 1.36 million tons of 2020-21 corn was sold to China, most since July, and fifth largest 24-hour purchase in history for China (see largest daily sales of corn attached). Some think the China sales were for new-crop. As of Jan 14, China had 5.975

million tons of US corn outstanding and accumulated exports amounted to 5.794 million tons (total commitments of 11.769 million tons versus 60,000 tons this time last year and 165,000 tons year before that). Note the unknown category has 7.786 million tons

outstanding. For new-crop, USDA showed China had no corn on the books, and the unknown category had nothing either.

-

Meanwhile

ADM sees China eventually importing 25 million tons of corn. They also said China committed to 200 million gallons of ethanol for first half 2021.

-

As

of the grain close, USD was 21 points lower, WTI 0.23 lower and gold down $3.10. US stocks were mostly higher.

-

Ukraine

will limit corn exports in 2020-21 to 24 million tons. Ukraine corn production was 30.3 million tons, a very large output compared to previous years.

-

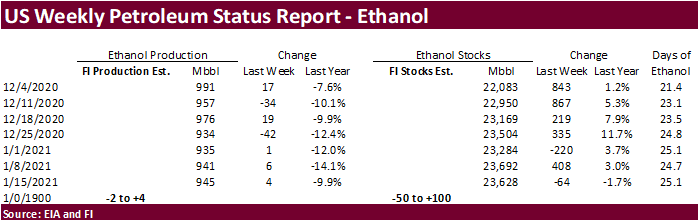

A

Bloomberg poll calls for weekly ethanol production to end up near 939, down from 945 previous week, and stocks at 23.794 million compared to 23.628 million previous week.

-

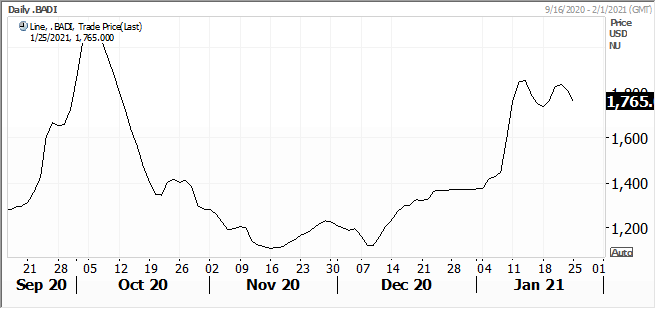

Note

the Baltic Dry Index fell 6 percent from the previous day to 1,659 points. This makes it a touch cheaper to ship grain across the oceans.

Corn

Export Developments

- WASHINGTON,

January 26, 2021–Private exporters reported to the U.S. Department of Agriculture the following activity:

–Export

sales of 1,360,000 metric tons of corn for delivery to China during the 2020/2021 marketing year; and

–Export

sales of 102,800 metric tons of corn for delivery to unknown destinations during the 2020/2021 marketing year.

Updated

1/26/21

March

corn is seen trading in a $4.75 and $5.50 range. New contract high could be reached this week.

-

CBOT

soybeans,

meal and soybean oil charged higher today on good export demand and concerns the US soybean crush could slow during the summer months. Bull spreading was a feature.

China

was an active, but small, buyer of US soybeans on Monday. Yesterday

we saw very good export inspections at a time when some thought shipments from the US would wind down as China shifts imports over to South America. Soybean oil was initially the leader in the products on fund buying before soybean meal ripped higher. March

soybean oil is not too far off from its absolute contract high of 44.69. Expect a contract high this week if the funds add onto their long positions.

-

March

soybean oil share hit its highest level since Jan 8. March crush ended the day unchanged. May was down a penny.

-

ICE

canola hit its highest price in 13 years. -

Summer

soybean meal contracts could firm over the next few months if US crushers slow processing. We are hearing some locations may not be able to find the soybeans to crush this summer, which could support the July and August contracts. We could see crush rates

erode by early as late April. If this is the case, there is a possibility crush margins will decline, unless soybeans can be sourced.

USDA

Attaché: Argentina grain and feed update

Wheat

production 17.5 million tons, in line with USDA

Corn

production 47 million tons, 500,000 less than USDA official

Oilseeds

Export Developments

- None

reported

SMK1-N1

Source:

Reuters and FI

Updated

1/26/21

March

soybeans are seen in a $13.25 and $14.75 range

March

soymeal is seen in a $410 and $480 range

March

soybean oil is seen in a 42.50 and 45.00 cent range (up 150 points both ends)

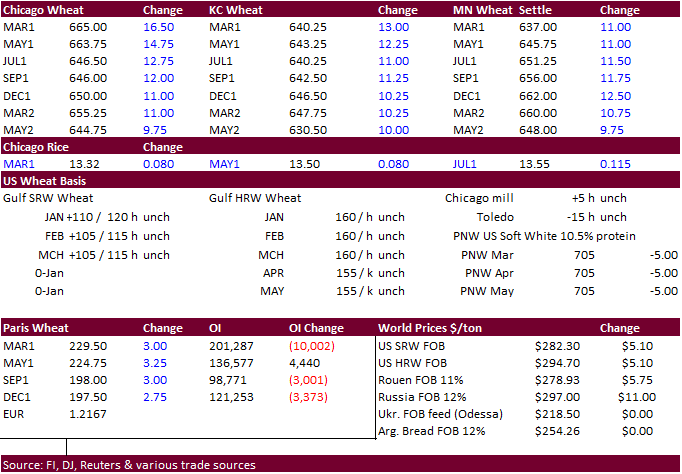

- US

wheat futures traded higher following strength in corn and confirmation Russia will increase its planned export tax on wheat. Chicago wheat was up 11-16.75 cents, KC wheat up 10.25-13.75 cents and MN wheat up 10.75-12.50 cents. In comparison March corn was

20.75 cents higher. - Russia

formally announced a proposal to impose a higher export tax on wheat from March 1, by implementing a 50 euro ($61) per ton tax starting through June 30. This is up from the original 25 euro-per-ton tax set for Feb. 15 to March 1. A barley and corn export

tax are set at 10 euro/t and 25 euro/t, respectively, from March 15 to June 30.

- Russia

plans to continue monitoring domestic food prices and adjust its export taxes if needed.

- The

Australian Bureau of Statistics showed December wheat exports to China amounted to a large 600,000 tons despite high import tariffs.

Prior

to December little

exports were recorded since last August. They took 880 tons in November. The 600,000 tons is the largest monthly wheat export figure from Australia to any single country. Tensions between Australia wheat exporters and China increased in early December.

- Note

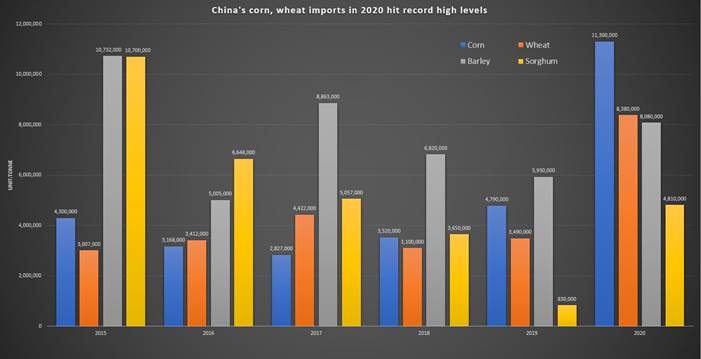

China has sold 10 million tons of wheat out of reserves so far in January. In 2020, China imported a record 8.38 million tons of wheat, against a quota of 9.64 million tons. China also imported 11.3 million tons of corn. Bottom line China’s appetite for

wheat and feedgrains remains very strong. - Jordan

has 1.5 million tons of wheat in reserves and 605,000 tons of barley, enough to last for 191 months and 10 months, respectively. Jordan consumes about 80,000 tons of wheat and 60,000 tons of barley a month.

- EU

March milling wheat was up 3.00 at 229.50 euros.

- Jordan

bought 120,000 tons of animal feed barley. $258.90 and $259/ton was estimated.

-

Japan

seeks 60,175 tons of Australian food wheat this week.

-

Algeria’s

state grains agency OAIC seeks 50,000 tons of wheat on Wed for shipment between Feb. 1-15 and Feb. 16-28.

- Jordan’s

seeks 120,000 tons of milling wheat, optional origin, on Jan. 27.

- Japan’s

AgMin in a SBS import tender seeks 80,000 tons of feed wheat and 100,000 tons of feed barley for arrival by March 18, on January 27.

-

Taiwan

launched an import tender for 85,340 tons of US wheat, set to close Jan 29, for late March through April 22 shipment.

-

Yesterday

Bangladesh suspended an import tender for 50,000 tons of wheat.

·

Syria is in for 39,400 tons of rice on Feb 22. They are also in for 25,000 tons of rice on February 9.

- Today

Bangladesh suspended an import tender for 50,000 tons of rice.

Source:

Updated

1/26/21

March

Chicago wheat is seen in a $6.35‐$7.15 range

March

KC wheat is seen in a $6.25‐$6.70 range (up 10 & 15)

March

MN wheat is seen in a $6.00‐$6.55 range

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International

One Lincoln Center

18 W 140 Butterfield Rd.

Suite 1450

Oakbrook Terrace, Il. 60181

W: 312.604.1366

ICE IM:

treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered

only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making

your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors

should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or

sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy

of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.