PDF Attached

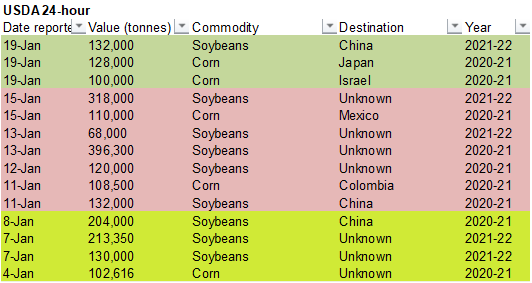

USDA

24-hour:

–Export

sales of 132,000 metric tons of soybeans for delivery to China during the 2021/2022 marketing year;

–Export

sales of 128,000 metric tons of corn for delivery to Japan during the 2020/2021 marketing year; and

–Export

sales of 100,000 metric tons of corn for delivery to Israel during the 2020/2021 marketing year.

We

made an error on our US corn balance sheet issued over the weekend with 2021-22 planted area and updated it to reflect 92 million acres (exports and feed taken higher). Stocks remain the same at 1.582 billion. Attached is the revised balance.

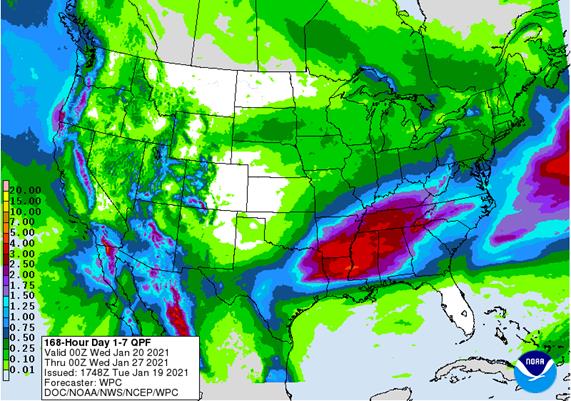

Weather

South

America saw mostly good rain over the 3-day period, bias northern Argentina. Brazil rainfall was widespread from Rio Grande do Sul to southern Minas Gerais and northward into Mato Grosso during the Friday through Monday afternoon. Brazil rainfall this week

will be greatest from northern Rio Grande do Sul, Santa Catarina, Parana and southern Sao Paulo to Mato Grosso. Argentina received rain Friday and Saturday, bias north with 1.00 to 2.00 inches. The wetter areas were from western Entre Rios through central

and northern Santa Fe to Santiago del Estero, Chaco and Formosa. Argentina’s weather outlook looks dry this week but wet for the last week of January.

THE

WORLD’S IMPORTANT WEATHER

- Argentina’s

rainfall during the past week has bolstered soil moisture to the benefit of nearly all crops - Some

pockets of dryness remain, but general crop conditions have been improving and will continue to improve for a few days - Net

drying this week will be of interest and raise the importance of follow up rain the last days of January and February - Argentina’s

second week outlook today is a little drier than that suggested Monday, but that change was needed - The

nation’s weather pattern has not come completely out of the drier mode and rain in February will be extremely important for many crops - La

Nina is still prevailing, although it will start a weakening trend over the next few weeks - Brazil

weather has still not completely straightened out - Rainfall

so far this month has continued below average in parts of Sao Paulo, southern and Mato Grosso, southwestern Minas Gerais, northern and eastern Parana, Tocantins, northeastern Goias or western Bahia

- Recent

rain has, however, improved soil moisture in Sao Paulo and southwestern Minas Gerais, as well as northern Parana - Be

sure to note that these areas received significant rain over the past week even though the data does not completely reflect that fact due to poor population of “official” weather reporting stations, but the supplemental data has certainly suggested improvement - Brazil

weather over the next two weeks will be plenty wet from northern Rio Grande do Sul to western and southern Sao Paulo and northward through Mato Grosso and Goias - Even

if some of the rainfall remains lighter than usual its coverage and frequency will be great enough to support good crop development - Some

concern over early season soybean harvest conditions may evolve later this month if rain falls too frequently, but that is not likely to be a huge issue - East-central

and northeastern Brazil will struggle with dryness for a while - This

first week of the outlook will be one of net drying for crop areas from northeastern Sao Paulo through all of Minas Gerais to eastern Tocantins, southern Piaui, Bahia and Pernambuco - Second

week rainfall should improve in western and southern Minas Gerais and eastern Tocantins, but will continue limited in other areas in the northeast - This

dryness may impact unirrigated coffee, sugarcane and cocoa more significantly than grain and oilseed crops - Brazil’s

greatest rainfall for a while is expected in northern and western Rio Grande do Sul, southern Paraguay, southern Mato Grosso do Sul and parts of both Santa Catarina and southern Parana during the coming ten days - Brazil’s

Rio Grande do Sul crops will be in much better than usual condition for a La Nina year - China

winter crops are in good conditions with little to no winterkill so far this year - There

was some concern over bitter cold in the north earlier this season when snow cover was limited and if there was some damage it should be slight - China’s

weather over the next couple of week should be typical for this time of year - India

has been and will continue to be dry for a while - There

is need for more precipitation in winter crop areas outside of the far south - Recent

drying in the far south has been good for late season harvesting that had been delayed by too much moisture earlier this month and last - Indonesia,

Malaysia and eastern Philippines have been dealing with frequent precipitation events some of which have induced flooding in recent weeks - Some

drying would be welcome and should happen over the next two weeks - Soil

moisture and crop conditions are mostly good and any negative impact from recent flooding has likely been localized and not suspected of having a huge impact on any crop - Europe

is a bit too wet in the west and some southern locations and drier weather would be welcome - Crop

damage because of too much moisture has not likely occurred, but with the wet bias continuing the potential for flooding will increase and that could lead to some potential problems - Recent

precipitation in eastern Spain, Romania, Bulgaria, Greece, Moldova, Ukraine and Russia’s Southern Region has improved soil moisture for spring use - The

precipitation will continue periodically maintaining an improved outlook - Russia’s

Southern Region will not be as wet this week as it has been - Bitter

cold temperatures during the weekend brought temperatures below zero Fahrenheit from the Baltic Plain into Ukraine and northern parts of Russia’s Southern Region as well as other western Russia locations - The

cold induced no crop damage because of sufficient snow coverage

- Warming

is expected in eastern Europe and the western CIS this week which may melt snow cover in southern areas and reduce winter crop protection from harsh weather if it were to suddenly return - There

is no threat of damaging cold for the next two weeks - U.S.

crop weather is still fine in the Midwest, Delta and southeastern states with plenty of soil moisture present and no threat of winterkill in wheat areas - Hard

red winter wheat areas are still dry in Nebraska, northwestern Kansas and northeastern Colorado where significant precipitation is needed for spring crop use - That

precipitation may not come immediately – at least not significantly, but the spring outlook should trend a little more favorably - Northwestern

U.S. Plains and southwestern Canada’s Prairies will see temperatures fall near the damage threshold for winter wheat later this week and into next week, but the combination of sufficient crop hardening against the cold, at least a dusting of snow in some areas

and borderline damaging cold conditions the impact is expected to be low - Montana

and the southwestern Canada Prairies winter crops were not well established last autumn because of dryness - Drought

in the western United States might be eased ever so slightly late this week and during the weekend as snow and rain evolve briefly in some of the dry areas - Much

more precipitation will be needed to seriously change drought conditions and that is not very likely even though another bout of precipitation will evolve early next week - West

Texas will receive some light precipitation this week, but it will not be well distributed and much more precipitation is needed to bolster long term soil moisture - South

Texas remains too dry and needs significant rain in the next few weeks to support early season planting in late February and March, but there is still another few weeks for possible change - U.S.

Delta and southeastern states are still plenty moist and will stay that way for a while

- U.S.

soft wheat in the Midwest is in favorable condition with plenty of moisture available and no threat of damaging cold anytime soon - North

America temperature outlook still brings colder than usual air to Canada’s Prairies later this week and into early next week, but it is not as potent as that advertised previously and it will not last as long either - The

cold also fails to get as far to the south into the U.S. Plains or Midwest relative to last week’s forecasts - South

Africa weekend precipitation was erratic resulting in pockets of net drying and pockets of ongoing good crop development - South

Africa will experience net drying this week except in Limpopo where some significant rain may fall during the weekend from a tropical cyclone expected in Mozambique - Rainfall

should improve next week over at least a part of the nation - Tropical

Cyclone Eloise will reach northern Madagascar today and will produce heavy rain and some moderate wind across the region - Flooding

is possible, but damage to rice, corn, sugarcane or vanilla is not very likely - The

storm will move across the Mozambique Channel during the latter part of this week with some re-intensification expected. The storm may make landfall during the weekend in southern Mozambique producing heavy rain across some of that nation’s crop areas; however,

there is potential the storm could curve to the south and stay over open water - Damage

is expected to be light if the storm moves inland - Australia’s

southeastern Queensland and northern New South Wales weather outlook is not very good for significant rainfall in the next two weeks - Net

drying will increase unirrigated crop stress - Temperatures

will be near to below average in eastern Queensland and northeastern New South Wales and a little warmer than usual in the remainder of the nation - West

Africa rainfall will remain mostly confined to coastal areas while temperatures in the interior coffee, cocoa, sugarcane, rice and cotton areas are in a seasonable range for the next ten days - Some

rain fell in coastal areas of Ivory Coast and Ghana during the weekend, but key crop areas were dry - East-central

Africa rainfall will continue limited in Ethiopia as it should be at this time of year while frequent showers and thunderstorms impact Tanzania, Kenya and Uganda over the next ten days - Southern

Oscillation Index remains very strong during the weekend and was at +18.56 today and the index will remain very strong for a while longer - Welcome

rain is expected in central and northern Mexico this week - The

moisture will help bring some badly needed relief to drought conditions, but more rain will be needed

- Winter

crop planting and establishment conditions will improve briefly - Canada

Prairies will trend colder this week with periods of snow into mid-week - The

snow will help improve crop protection for winter wheat in the south and east, but some areas in southern Alberta may stay snow free - Southeast

Canada will receive brief periods of rain and snow this week, but resulting moisture will be lighter than usual - Temperatures

will be seasonably cool

Source:

World Weather Inc. and FI

Tuesday,

Jan. 19:

- USDA

weekly corn, soybean, wheat export inspections, 11am - New

Zealand global dairy trade auction

Wednesday,

Jan. 20:

- China

customs to publish import data split by country - European

Cocoa Association grinding data - Malaysia’s

Jan 1-20 palm oil exports

Thursday,

Jan. 21:

- Port

of Rouen data on French grain exports - USDA

red meat production

Friday,

Jan. 22:

- USDA

weekly crop net-export sales for corn, soybeans, wheat, cotton, pork, beef, 8:30am

- ICE

Futures Europe weekly commitments of traders report, 1:30pm (6:30pm London) - CFTC

commitments of traders weekly report on positions for various U.S. futures and options, 3:30pm - EIA

weekly U.S. ethanol inventories, production, 10:30am (two days later than usual due to federal holidays earlier in the week) - U.S.

Cattle on Feed, poultry slaughter

Source:

Bloomberg and FI

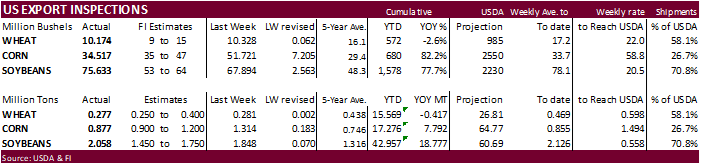

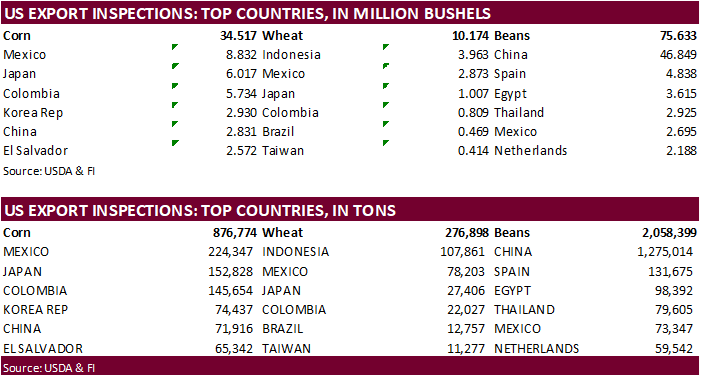

USDA

inspections versus Reuters trade range

Wheat

276,898 versus 200000-400000 range

Corn

876,774 versus 900000-1250000 range

Soybeans

2,058,399 versus 900000-1850000 range

GRAINS

INSPECTED AND/OR WEIGHED FOR EXPORT

REPORTED IN WEEK ENDING JAN 14, 2021

— METRIC TONS —

————————————————————————-

CURRENT PREVIOUS

———–

WEEK ENDING ———- MARKET YEAR MARKET YEAR

GRAIN 01/14/2021 01/07/2021 01/16/2020 TO DATE TO DATE

BARLEY

2,395 0 318 23,339 17,246

CORN

876,774 1,313,767 396,914 17,275,616 9,483,581

FLAXSEED

24 0 0 485 396

MIXED

0 0 0 0 0

OATS

0 0 48 2,393 2,443

RYE

0 0 0 0 0

SORGHUM

159,495 133,461 31,005 2,638,767 988,758

SOYBEANS

2,058,399 1,847,777 1,208,247 42,956,889 24,180,346

SUNFLOWER

0 0 0 0 0

WHEAT

276,898 281,087 516,808 15,568,860 15,985,872

Total

3,373,985 3,576,092 2,153,340 78,466,349 50,658,642

————————————————————————-

CROP

MARKETING YEARS BEGIN JUNE 1 FOR WHEAT, RYE, OATS, BARLEY AND

FLAXSEED;

SEPTEMBER 1 FOR CORN, SORGHUM, SOYBEANS AND SUNFLOWER SEEDS.

INCLUDES

WATERWAY SHIPMENTS TO CANADA.

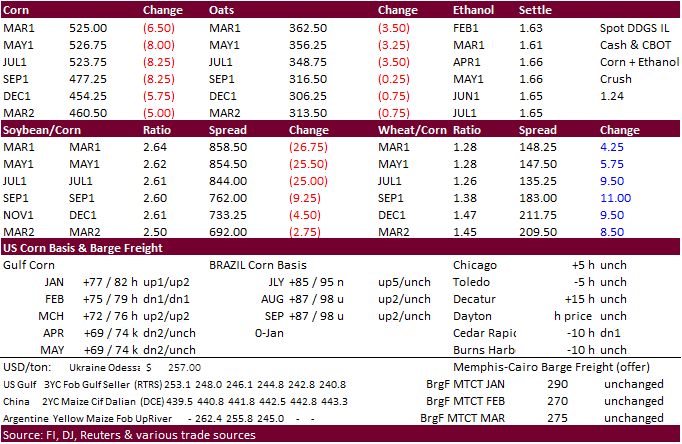

Corn.

-

March

corn futures settled 5.50 cents lower after decent rain fell across South America over the weekend. Price declines were limited on buying in some of the US wheat contracts, and Chinese December trade data that indicated strong corn import demand.

-

USDA

US corn export inspections as of January 14, 2021 were 876,774 tons, below a range of trade expectations, below 1,313,767 tons previous week and compares to 396,914 tons year ago. Major countries included Mexico for 224,347 tons, Japan for 152,828 tons, and

Colombia for 145,654 tons. -

After

Russia announced on Friday to impose and increase wheat export taxes, Ukraine on January 25 will decide whether to limit corn exports to 22 million tons. Ukraine exported nearly 11 million tons so far this season. The Ukraine grain traders union, UGA, sees

no ground to restrict Ukraine corn exports. -

Funds

on Monday sold an estimated net 25,000 corn contracts. -

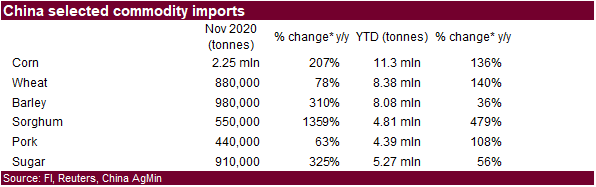

China’s

customs data showed a record 11.3 million tons of corn was imported last year, more than double the previous year. It included 2.25 million tons in December. The 11.3 million tons is above the 7.2 million tons quota.

-

China

will auction off 30,000 tons of pork on Jan 21. -

China

National Bureau of Statistics reported the following: -

2020

pork output fell 3.3% from a year earlier to 41.13 million tons -

China

slaughtered 527.04 million hogs in 2020, down 3.2% from the same period a year earlier. -

China

pig herd rose to 406.5 million heads at the end of December from 370.39 million at the end of September

- So

far in January, Ukraine corn export prices rose $23-$26 per ton to $256-$264 fob Black Sea, according to APK-Inform. This is $6-$10 per ton higher than the previous record in May 2014.

-

Due

to the Federal holidays of Dr. Martin Luther King Jr. and the Presidential Inauguration the next U.S. Export Sales Report will be released on Friday, January 22, 2021. -

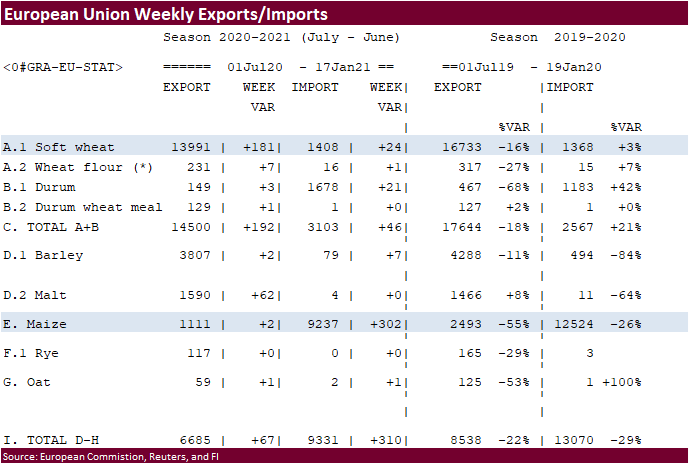

The

European Union granted imports licenses for 302,000 tons of corn imports, bringing cumulative 2020-21 imports to 9.237 MMT, 26 percent below same period year ago. -

Bloomberg

Cattle on Feed placement estimates: Placements are seen down 3.1% y/y to 1.772 million. Placements fell 11% in Oct. and 8.9% in Nov.

Corn

Export Developments

- USDA

reported the following 24-hour sales: - Export

sales of 128,000 metric tons of corn for delivery to Japan during the 2020/2021 marketing year - Export

sales of 100,000 metric tons of corn for delivery to Israel during the 2020/2021 marketing year.

- Taiwan’s

MFIG seeks 65,000 tons of corn on Wednesday for March or April loading.

Trade

News Service

Updated

1/12/21

March

corn is seen trading in a $4.75 and $5.50 range

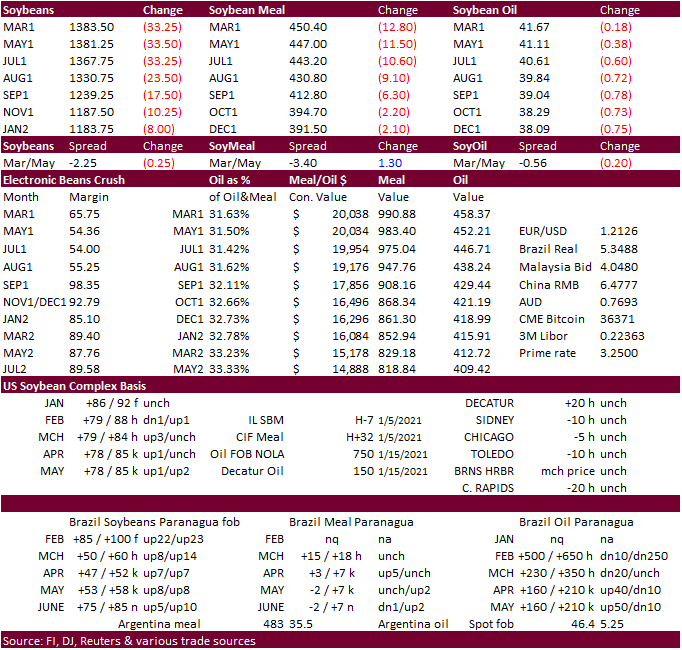

-

CBOT

soybeans traded sharply lower after South America saw rain over the weekend and lower lead by offshore product values. March soybeans fell by a large 31 cents to $13.8575, March meal off a whopping $12.70/short ton to $450.50, and March soybean oil down by

15 points to 41.70 cents. Note the May and July soybean oil contracts fell 30 and 49 points, respectively. With palm oil trading at near a 2-month low, this could drive China to import a little more palm oil going forward over soybean oil and rapeseed oil.

Note European

rapeseed oil demand has been very good by China. Egypt GASC seeks local vegetable oils on January 23.

-

One

factor that may have come into play today were renewed geopolitical concerns between the US and China. “US State Sec. Pompeo: US Has Determined That China Has Committed ‘Genocide’ And ‘Crimes Against Humanity’ In Its Treatment Of Uighur Muslims And Other

Members Of Ethnic And Religious Minority Groups In Western Region Of Xinjiang.”

-

The

selling in soybeans spilled over into ICE canola. March canola fell $19.80 or 2.9% to $664.20 per ton.

-

We

heard the recent driver strike in Argentina that started Jan 15 was not very populated and had little impact on agriculture deliveries. However, some soybean arrivals to ports dependent on lorries were affecting arrivals.

-

USDA

US soybean export inspections as of January 14, 2021 were 2,058,399 tons, above a range of trade expectations, above 1,847,777 tons previous week and compares to 1,208,247 tons year ago. Major countries included China for 1,275,014 tons, Spain for 131,675

tons, and Egypt for 98,392 tons. -

Meanwhile

China was a good buyer last week of US and Brazil soybeans of an estimated 30-32 cargoes, according to AgriCensus.

-

Funds

on Monday sold an estimated net 20,000 soybeans, sold 5,000 soybean meal and sold 1,000 soybean oil.

-

Last

we heard, IL crude SBO was nominal 150 over, East nominal 175 over, West nominal 125 over and crude degummed at the Gulf at 575 over, down from 700 early last week.

-

Argentine

as of late last week planted 94 percent of their soybean crop, one point below average.

-

AgRural

reported Brazil harvested less than one percent of the soybean crop, behind 2 percent a year earlier. MG is less than one percent versus nearly 5 percent average.

-

Brazil

truck workers are planning to go on strike February 1 over fuel prices.

-

India

oilseed meal imports were 512,997 tons in December from 220,404 tons a year earlier. Shipments of soybean meal 251,221 tons vs 72,233 tons.

-

Ukraine’s

sunseed crush may slow over the near term on lack of producer selling and poor crush margins.

-

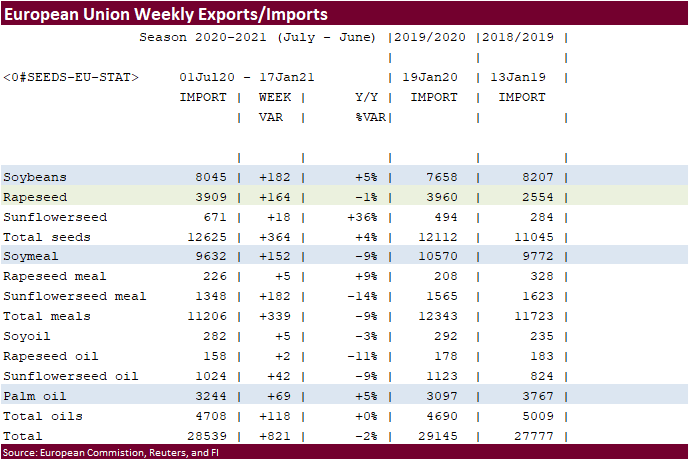

The

European Union reported soybean import licenses since July 1 at 8.045 million tons, below 7.658 million tons a year ago. European Union soybean meal import licenses are running at 9.932 million tons so far for 2020-21, below 10.570 million tons a year ago.

EU palm oil import licenses are running at 3.244 million tons for 2020-21, above 3.097 million tons a year ago, or up 5 percent. -

European

Union rapeseed import licenses since July 1 were 3.909 million tons, down 1 percent from 3.960 million tons from the same period a year ago.

- Egypt’s

GASC seeks 3,000 of local soybean oil and 2,000 tons of local sunflower oil on Jan 23 for arrival between February 18 and March 5. USDA reported the following 24-hour sales: - Export

sales of 132,000 metric tons of soybeans for delivery to China during the 2021/2022 marketing year

- USDA

seeks 6,390 tons of vegetable oil on January 20 under the PL480 program for March 1-31 shipment (Mar 16-Apr 15 for plants at ports).

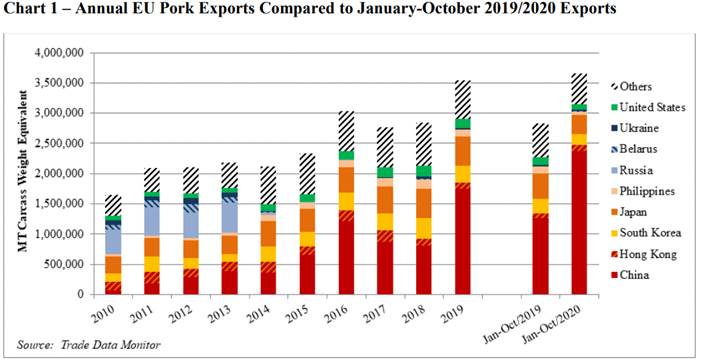

USDA

attaché: EU 2020 pork exports hit record

Updated

1/19/21

March

soybeans are seen in a $13.25 and $14.75 range (unchanged and down 25 cents)

March

soymeal is seen in a $410 and $480 range (down $10 & $20)

March

soybean oil is seen in a 41.00 and 43.50 cent range (down 1 & 2 cents, respectively)

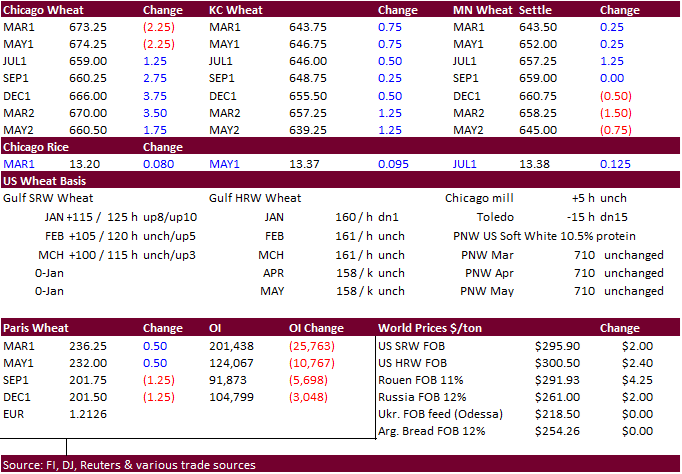

- US

wheat started sharply higher on follow through buying after Russia said they will impose higher export duties than what they previously planned. Prices eventually traded lower after fund buying dried up, but longs returned to the market in part to spreading

against soybeans and bottom picking from a weak USD. Chicago ended mixed with the front two month contracts lower. KC ended 0.75-1.25 cents higher and MN mixed with emphasis on bull spreading. Black Sea cash prices appreciated last week which was supportive

for global prices. EU wheat traded at a 7-1/2 year high Monday into Tuesday morning, but

EU

March milling wheat settled unchanged at 235.75 euros ($285.75) a ton. Some traders will be closely watching an import tender held by Algeria on Wednesday to see how prices are offered. - USDA

US all-wheat export inspections as of January 14, 2021 were 276,898 tons, within a range of trade expectations, below 281,087 tons previous week and compares to 516,808 tons year ago. Major countries included Indonesia for 107,861 tons, Mexico for 78,203 tons,

and Japan for 27,406 tons. - Funds

on Monday

sold an

estimated net 3,000 Chicago wheat contracts. - China’s

customs data showed China imported a record 8.38 million tons of wheat against a quota of 9.64 million tons. - China

sold 3.9 million tons of wheat form reserves, nearly all that was offered at auction at an average price of 2,504 yuan per ton.

- Russia

wheat export prices rose $23/ton last week to $298/ton, according to IKAR.

- Ukraine

wheat export prices rose $3.00 per ton to $284-$293 fob Black Sea, according to APK-Inform.

- Ukraine

grain exports are running 18 percent lower from last season at 27.2 million tons. Flour exports are down 56% so far this year.

- The

European Union granted export licenses for 181,000 tons of soft wheat exports, bringing cumulative 2020-21 soft wheat export commitments to 13.991 MMT, well down from 16.733 million tons committed at this time last year, a 16 percent decrease. Imports are

up 3 percent from year ago at 1.408 million tons.

-

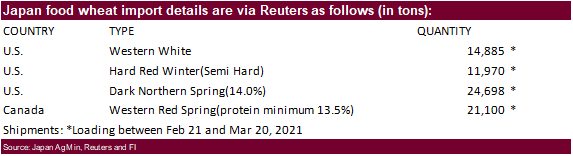

Japan

in a SBS auction passed on 80,000 tons of feed wheat and 100,000 tons of feed barley for arrival in Japan by March 18.

-

The

Philippines may have passed on 100,000 tons of feed wheat and 80,000 tons of barley. Feed wheat may have been offered at $300/ton.

-

Jordan

bought 60,000 tons of feed barley at $262/ton c&f for FH July shipment.

- Algeria

seeks at least 50,000 tons of wheat for February 15-28 shipment on Wednesday.

- One

offer was presented for Bangladesh for 50,000 tons of wheat. Going forward, Bangladesh plans to seek wheat from Ukraine after Russia planned to increased wheat export taxes. Russia has supplied about 200,000 tons, half of the planned export target to Bangladesh.

- Turkey

moved their import tender for 400,000 tons back to January 22 for January 29-February 26 shipment.

- One

trading house participating: Bangladesh seeks 50,000 tons of wheat January 18 for shipment within 40 days of contract signing.

-

Japan

seeks 72,653 tons of milling wheat later this week.

-

Syria

seeks 200,000 tons of wheat on Jan 18 for shipment within 60 days after contract signing.

- Jordan

seeks 120,000 tons of milling wheat, optional origin, on Jan. 20. Possible shipment combinations are between June 1-15, June 16-30, July 1-15, July 16-31, Aug. 1-15 and Aug. 16-31.

-

Turkey

seeks 400,000 tons of milling wheat on Jan 19 for Jan through Feb 25 shipment.

- Bangladesh

seeks 50,000 tons of wheat January 25 for shipment within 40 days of contract signing.

·

Bangladesh seeks 60,000 tons of rice on January 20.

·

Bangladesh seeks 50,000 tons of rice on Jan. 24.

- Bangladesh

seeks 50,000 tons of rice on January 26.

·

South Korea seeks 113,555 tons of US, Thailand, and China rice on Jan 21 for April 30 through July 31 arrival.

·

Syria seeks 25,000 tons of rice on February 9.

Updated

1/12/21

March

Chicago wheat is seen in a $6.35‐$7.15 range

March

KC wheat is seen in a $6.00‐$6.50 range

March

MN wheat is seen in a $6.00‐$6.55 range

Terry Reilly

Senior Commodity Analyst – Grain and Oilseeds

Futures International

One Lincoln Center

18 W 140 Butterfield Rd.

Oakbrook Terrace, Il. 60181

W: 312.604.1366

ICE IM:

treilly1

Skype: fi.treilly

Trading of futures, options, swaps and other derivatives is risky and is not suitable for all persons. All of these investment products are leveraged, and you can lose more than your initial deposit. Each investment product is offered

only to and from jurisdictions where solicitation and sale are lawful, and in accordance with applicable laws and regulations in such jurisdiction. The information provided here should not be relied upon as a substitute for independent research before making

your investment decisions. Futures International, LLC is merely providing this information for your general information and the information does not take into account any particular individual’s investment objectives, financial situation, or needs. All investors

should obtain advice based on their unique situation before making any investment decision. The contents of this communication and any attachments are for informational purposes only and under no circumstances should they be construed as an offer to buy or

sell, or a solicitation to buy or sell any future, option, swap or other derivative. The sources for the information and any opinions in this communication are believed to be reliable, but Futures International, LLC does not warrant or guarantee the accuracy

of such information or opinions. Futures International, LLC and its principals and employees may take positions different from any positions described in this communication. Past results are not necessarily indicative of future results.